Manganese Mining Market Size 2024-2028

The manganese mining market size is forecast to increase by USD 10.94 billion, at a CAGR of 6.78% between 2023 and 2028.

- The market is experiencing significant growth, driven by the increasing demand for steel and the rising adoption of stainless steel in various industries. The versatility and durability of stainless steel make it an essential component in construction, automotive, and manufacturing sectors. Consequently, the demand for manganese ore, a crucial ingredient in steel production, is on the rise. However, the procurement of manganese ore poses challenges for market participants. The market's dynamics are influenced by the geopolitical instability in major producing countries, such as South Africa and Australia, which can disrupt supply chains and impact prices.

- Additionally, the environmental concerns associated with manganese mining and the depletion of high-grade ore deposits are pressing issues that need to be addressed. Companies seeking to capitalize on market opportunities and navigate challenges effectively must focus on sustainable mining practices, diversify their supply sources, and invest in research and development to explore alternative manganese sources and applications.

What will be the Size of the Manganese Mining Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, shaped by a complex interplay of factors. Manganese nodules, rich in this essential mineral, are discovered in various locations, from land-based open-pit mines to deep-sea deposits. Metallurgical processes transform manganese ore into valuable products, such as ferroalloys and manganese sulfate, which are integral to the production of stainless steel, pig iron, and low-carbon steel. Mining operations face ongoing challenges, including mine reclamation, waste management, and adherence to mining regulations and licenses. Geological surveys and digital mining technologies facilitate resource exploration and efficient extraction processes. Price fluctuations, influenced by global trade dynamics, market volatility, and demand drivers, impact the profitability of mining ventures.

Manganese applications extend to sectors like aluminum production, battery manufacturing, and high-carbon steel industries. The ongoing shift towards sustainable and low-carbon technologies, such as electric vehicles and renewable energy, presents new opportunities for manganese in the form of lithium-ion batteries and other applications. Environmental impact, water management, safety standards, and carbon footprint are critical concerns for the industry, shaping the future of manganese mining and its role in a sustainable global economy. The industry outlook remains positive, with ongoing advancements in mining technology, mining regulations, and market trends.

How is this Manganese Mining Industry segmented?

The manganese mining industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Alloys

- Others

- Type

- Braunite

- Pyrolusite

- Psilomelane

- Rhodochrosite

- Geography

- North America

- US

- APAC

- Australia

- China

- India

- South America

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The alloys segment is estimated to witness significant growth during the forecast period.

The market is characterized by various market dynamics and trends. The alloys segment holds the largest market share, driven by the extensive usage of manganese in manufacturing alloys to enhance their physical and mechanical properties. Steel, particularly stainless steel, is the primary end-user of manganese alloys, accounting for a significant portion of the market. Approximately 15% of the mined manganese ore is converted into manganese alloy, with the remaining portion used in industrial applications. Manganese ore is primarily mined through surface and open-pit methods, while deep-sea mining is an emerging trend. Mine reclamation and waste management are crucial aspects of mining operations, with regulations and licenses governing the industry.

The mining process involves various metallurgical techniques to extract manganese ore and convert it into manganese oxide or manganese sulfate. Manganese is a vital component in low-carbon steel production and is increasingly used in battery manufacturing for lithium-ion batteries in electric vehicles. Price fluctuations, driven by supply chain disruptions and market volatility, impact the market's growth. Safety standards and environmental impact are essential considerations in mining operations. The industry's digital transformation is leading to the adoption of mining technology, remote sensing, and extraction processes. Manganese reserves are abundant, with significant deposits in South Africa, Australia, China, and Gabon.

The market's outlook is positive, with increasing demand from various end-users, including the aluminum industry. Occupational health and carbon footprint are essential concerns, with ongoing research focusing on improving mining technology and processes. The market's export and import markets are influenced by global trade policies and regulations.

The Alloys segment was valued at USD 19.93 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

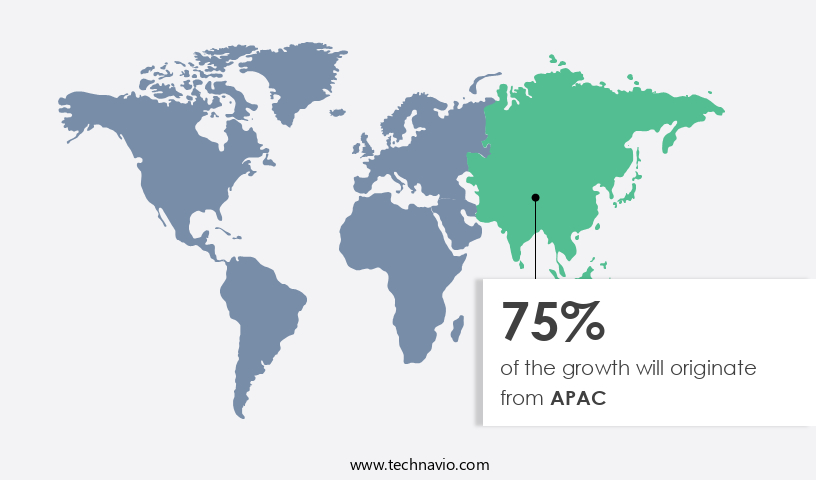

APAC is estimated to contribute 75% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market experienced significant activity in 2020, with APAC as the leading region due to its vast consumer base, abundant raw materials, and low labor costs. The market's growth is primarily driven by the applications of manganese in industries such as automotive, transportation, and construction. Manganese is a crucial component in steel and aluminum alloys, which are extensively used in automobile and construction sectors. Developing countries like China and India, set to become major automobile manufacturing hubs, further fuel market expansion. Mining operations in the manganese market encompass surface and underground techniques, with open-pit and open-cast methods being the most common for mining manganese ore.

Contract negotiation and mining regulations play a significant role in the industry, influencing production costs and schedules. Manganese ore is processed through various metallurgical methods to produce manganese oxide and manganese sulfate, essential for the production of ferroalloys and batteries. Mining technology advances and digital mining have transformed the industry, improving efficiency and reducing waste. However, environmental concerns and safety standards are increasingly important, necessitating mine reclamation and water management strategies. Price fluctuations and market volatility, influenced by global trade policies and supply chain disruptions, pose challenges to the industry's stability. The demand for low-carbon steel and pig iron, key components in stainless steel production, is a significant driver for the manganese market.

The emergence of electric vehicles and lithium-ion batteries has created new opportunities for manganese sulfate and manganese dioxide in the battery manufacturing sector. Geological surveys and mining licenses are essential for resource exploration and production. Mining regulations, mining licenses, and environmental impact assessments are critical factors influencing the market's growth. Export markets and import markets, along with demand drivers and import markets, shape the industry's dynamics. The industry outlook remains positive, with aluminum production and occupational health concerns also impacting market trends. The carbon footprint of manganese mining and the potential for deep-sea mining and seabed mining are areas of ongoing debate and research.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Manganese Mining Industry?

- The market is significantly driven by the increasing demand for steel, which serves as a key growth factor.

- Manganese is an essential element in the production of steel and batteries. The market is experiencing significant dynamics due to various factors. Supply chain disruptions, primarily caused by mining regulations and the acquisition of mining licenses, have impacted the market's growth. Surface mining is the primary method used for manganese ore extraction, and mining technology advancements have increased mine efficiency and productivity. Manganese sulfate, a byproduct of manganese mining, is in high demand due to its application in low-carbon steel production and battery manufacturing. Mine reclamation is a crucial aspect of the mining process, ensuring minimal environmental impact.

- Contract negotiation between mining companies and governments or local communities can be complex, influencing production costs and market prices. Manganese ore is a critical input for the global steel industry, which is experiencing steady growth due to increasing demand from end-user industries such as construction and automotive. Mining regulations and licenses can impact the supply chain, potentially leading to price volatility. Staying updated on mining technology and regulatory changes is essential for businesses operating in the market.

What are the market trends shaping the Manganese Mining Industry?

- Stainless steel is gaining increasing popularity in the market, serving as an emerging trend. This material's adoption is on the rise due to its durability, resistance to corrosion, and versatility.

- Manganese is an essential element used as an alloy in the production of stainless steel and pig iron. The demand for manganese is driven by its application in various industries, including mining, quarrying, chemical and petrochemical sectors, electrical engineering, power generation, and the food and beverage industry. The primary source of manganese is manganese nodules found in the ocean floor. Mining operations for these nodules can be conducted through open-pit mining or deep-sea mining. Manganese nodules contain high concentrations of manganese, which is extracted through metallurgical processes. The extracted manganese is then used in the production of ferroalloys, which are crucial in the manufacturing of stainless steel and pig iron.

- Price fluctuations in the manganese market can significantly impact the production of these alloys and, consequently, the industries that rely on them. Effective waste management is crucial in manganese mining operations to minimize environmental impact and ensure sustainable practices. The geological survey of potential mining sites is essential to assess the feasibility of mining operations and to determine the most efficient mining methods. Market volatility in the manganese industry can be attributed to various factors, including supply and demand dynamics, geopolitical risks, and technological advancements. Despite these challenges, the demand for manganese is expected to remain strong due to its critical role in the production of stainless steel and pig iron.

What challenges does the Manganese Mining Industry face during its growth?

- The procurement of manganese ore presents significant challenges that hinder industry growth. This challenge is particularly noteworthy due to the critical role manganese ore plays in various industries, including steel production and batteries. Effective management of this challenge is essential for ensuring the sustainability and expansion of businesses reliant on this essential resource.

- The market is influenced by various factors, primarily the availability and pricing of raw materials. Manganese ore, the primary source of manganese, is processed using hydrometallurgical and electrolytic methods to produce manganese metal and derivative products. The supply of manganese ore is contingent upon its mining and availability in countries with significant reserves. Manganese dioxide, a derivative product, is widely used in the production of high-carbon steel and as a key component in lithium-ion batteries for electric vehicles. Water management is a critical concern in manganese mining due to the potential environmental impact of mining operations. Safety standards are essential to ensure the safety of workers and minimize the risk of accidents.

- Extraction processes must comply with environmental regulations to mitigate the environmental impact. The demand for manganese is driven by its use in various industries, including steel and electric vehicle batteries. Seabed mining is an emerging trend in manganese mining, offering potential for increased supply but raising concerns regarding its environmental impact. Pricing models are crucial in determining the profitability of manganese mining operations. In conclusion, The market is influenced by the availability and pricing of raw materials, environmental concerns, safety standards, and industry trends. Understanding these factors is essential for businesses looking to invest in or expand their operations in the manganese mining industry.

- Recent research suggests that the market is expected to remain competitive, with several players vying for market share.

Exclusive Customer Landscape

The manganese mining market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the manganese mining market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, manganese mining market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

African Rainbow Minerals Ltd. - The company specializes in the extraction of premium manganese ore from the black rock mine. Leveraging advanced mining techniques, we ensure the delivery of high-quality manganese resources to meet diverse industrial demands. Our commitment to innovation and sustainability underpins our operations, enhancing search engine visibility and establishing us as a trusted supplier in the global market.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- African Rainbow Minerals Ltd.

- Anglo American plc

- Asia Minerals Ltd.

- BHP Group plc

- CITIC Ltd.

- Consolidated Minerals Ltd.

- Element 25 Ltd.

- Eramet

- Ferroglobe Plc

- Grupo Buritipar

- Guangxi Jinmeng Manganese Industry Co. Ltd.

- Hickman Williams and Co.

- Maithan Alloys Ltd.

- Manganese X Energy Corp

- Marubeni Tetsugen Co. Ltd.

- Mesa Minerals Ltd.

- MOIL LTD

- Nava Ltd.

- OM Holdings Ltd.

- Vale SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Manganese Mining Market

- In January 2024, Australian manganese miner, Fortescue Metals Group (FMG), announced the commissioning of its Greenbushes Mine's Phase 3 expansion, increasing its annual manganese production capacity by 2 million wet metric tonnes (wmt) to 6.5 million wmt, making it the world's largest integrated manganese producer (Fortescue Metals Group Press Release, 2024).

- In March 2024, South African manganese producer, Samancor Manganese, signed a memorandum of understanding (MoU) with Chinese steel giant, Baosteel, to collaborate on the development of a manganese alloy plant in China. The partnership aimed to secure a stable supply of high-grade manganese ore for Baosteel's expanding steel production (Samancor Manganese Press Release, 2024).

- In May 2024, the South African government granted a mining license to Australian mining company, Mineral Commodities Limited (MRC), for its Manganese Hill Mine project in the Northern Cape province. The project was expected to create over 1,000 jobs and contribute approximately USD300 million to the local economy (Mineral Commodities Limited Press Release, 2024).

- In February 2025, German specialty chemicals company, Evonik Industries AG, and Brazilian manganese producer, Vale SA, announced a strategic partnership to develop a new manganese-based battery material, Li-Mn, for the electric vehicle (EV) market. The collaboration aimed to reduce EV battery production costs and improve energy density (Evonik Industries AG Press Release, 2025).

Research Analyst Overview

- The market encompasses various manganese-based products, including manganese phosphate, manganese chloride, manganese acetate, and manganese sulfate monohydrate. These minerals find applications in diverse industries, such as steel, electronics, and battery manufacturing. Manganese mining and processing involve hydrometallurgical and pyrometallurgical methods. Hydrometallurgical processes, like solvent extraction, are favored for their environmental benefits. However, they can pose water pollution risks if not managed properly. Air pollution is another concern, as manganese mining and processing can release harmful particulate matter. Social impact and community engagement are crucial considerations, with the need for environmental permits and responsible land use essential for minimizing negative effects.

- Manganese is a key component in cathode materials for nickel-manganese-cobalt (NMC) batteries, which are gaining popularity due to their high charge capacity and electrochemical properties. The demand for NMC cathodes drives the market for manganese, with manganese alloys and manganese silicates also playing significant roles. Mineral processing techniques, such as those used for manganese carbonates, aim to optimize energy density and improve the cycle life of electrode materials. Pyrometallurgical processes, while energy-intensive, remain essential for producing manganese from low-grade ores. In the battery sector, manganese's role extends to anode materials, making it a versatile mineral with far-reaching market implications.

- As the demand for clean energy technologies grows, so does the importance of sustainable manganese mining and processing practices.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Manganese Mining Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

181 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Decelerate at a CAGR of 6.78% |

|

Market growth 2024-2028 |

USD 10940.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.23 |

|

Key countries |

China, India, Australia, US, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Manganese Mining Market Research and Growth Report?

- CAGR of the Manganese Mining industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the manganese mining market growth of industry companies

We can help! Our analysts can customize this manganese mining market research report to meet your requirements.

RIA -

RIA -