Steel Manufacturing Market Size 2026-2030

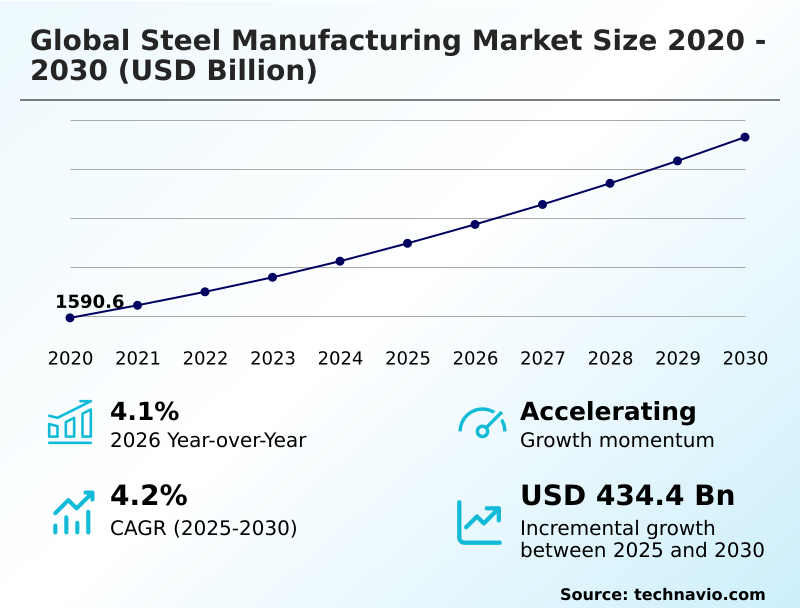

The steel manufacturing market size is valued to increase by USD 434.4 billion, at a CAGR of 4.2% from 2025 to 2030. Robust demand from global construction and infrastructure sectors will drive the steel manufacturing market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 46% growth during the forecast period.

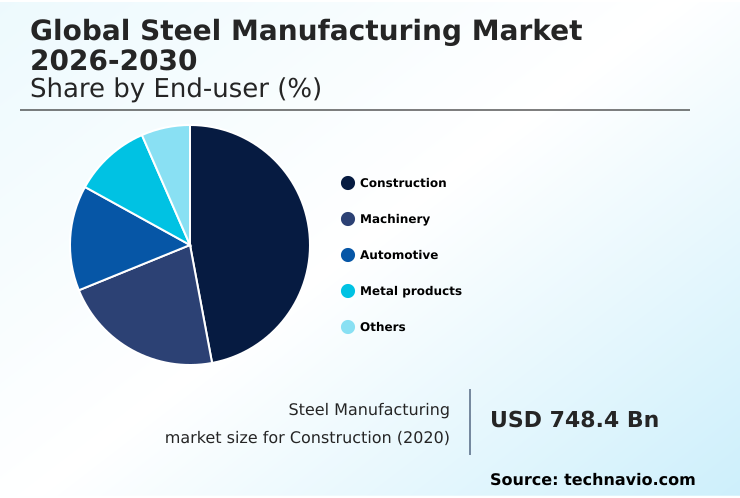

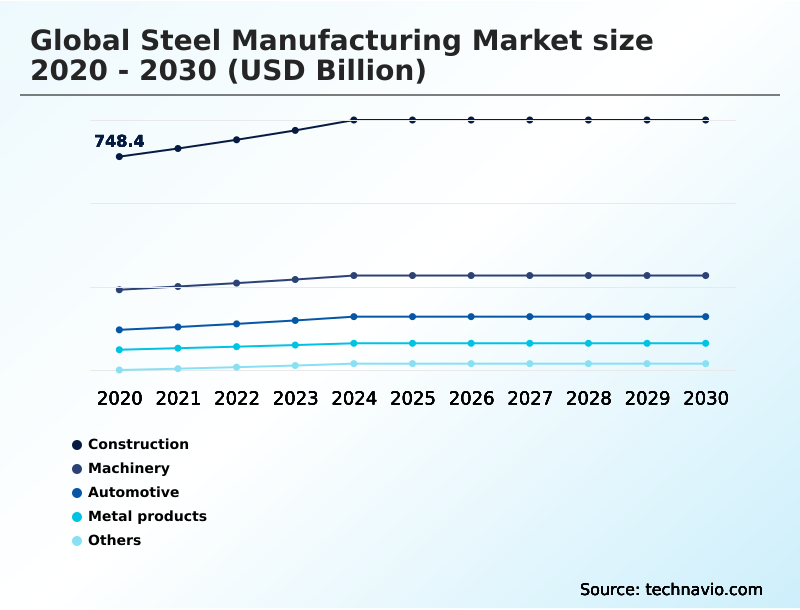

- By End-user - Construction segment was valued at USD 858.9 billion in 2024

- By Type - Flat segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 739.3 billion

- Market Future Opportunities: USD 434.4 billion

- CAGR from 2025 to 2030 : 4.2%

Market Summary

- The steel manufacturing market is defined by its foundational role in global industrial and economic development. Sustained demand from the construction and automotive sectors acts as a primary driver, fostering innovation in materials such as advanced high-strength steels and other value-added products designed to meet sophisticated engineering requirements for lightweighting and durability.

- The industry is concurrently undergoing a profound transformation, driven by the strategic imperative to decarbonize. A key business scenario involves steelmakers navigating intense raw material volatility by leveraging process optimization and digital technologies.

- For instance, producers are adopting AI-driven analytics to manage blast furnace and electric arc furnace operations more efficiently, ensuring consistent quality control for critical applications while mitigating the impact of fluctuating input costs for materials like iron ore and scrap steel.

- This dual focus on product innovation and operational resilience against challenges like global overcapacity and environmental compliance is crucial for maintaining competitiveness. The strategic pivot towards green steel production, utilizing technologies like direct reduced iron and hydrogen-based steelmaking, is reshaping capital investment strategies and competitive dynamics across the entire value chain.

What will be the Size of the Steel Manufacturing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Steel Manufacturing Market Segmented?

The steel manufacturing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Construction

- Machinery

- Automotive

- Metal products

- Others

- Type

- Flat

- Long

- Application

- Automotive

- Mechanical equipment

- Building and construction

- Metal products

- Others

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Italy

- Spain

- Middle East and Africa

- Turkey

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By End-user Insights

The construction segment is estimated to witness significant growth during the forecast period.

The construction sector is the primary end-user, representing approximately 47% of total market consumption. This segment's demand for flat products and long products underpins global steel manufacturing, with structural steel and rebar forming the backbone of modern infrastructure.

The processing of slabs into these essential materials requires significant capital expenditure, but achieves crucial economies of scale. For downstream manufacturing, ensuring strict quality control and lifecycle assessment is paramount.

Innovations in galvanized steel offer enhanced durability, while ongoing process optimization efforts aim to improve efficiency, ensuring steel remains the foundational material for building and civil engineering projects worldwide amid evolving architectural standards.

The Construction segment was valued at USD 858.9 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 46% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Steel Manufacturing Market Demand is Rising in APAC Get Free Sample

The global landscape is dominated by APAC, which accounts for over 46% of incremental growth, largely due to its control over the seaborne market for iron ore.

This region's national industrial policy has fostered massive production of crude steel, billets, and blooms.

In contrast, North America has leveraged electric arc furnace technology, which relies heavily on scrap steel, to create a more resilient domestic supply chain with a recycling rate of over 70%.

This strategic divergence is influenced by geopolitical factors and the use of trade defense instruments.

A complete value chain analysis shows Europe focusing on high-value steel plates while investing heavily in green hydrogen to decarbonize production and maintain its competitive position, reshaping the flow of semi-finished products globally.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global steel manufacturing market 2026-2030 is at a critical inflection point, shaped by interconnected strategic imperatives. The ongoing digitalization trends in steel mills, a core component of industry 4.0 in steel manufacturing, are providing essential tools to address the formidable decarbonization challenges for integrated mills.

- This digital transformation is critical for enabling process optimization in steelmaking, where firms that invest in smart factory technologies report a nearly twofold increase in supply chain visibility over peers. This enhanced visibility is crucial for managing geopolitical factors in steel and the subsequent impact of tariffs on steel trade, which has accelerated the regionalization of steel supply chains.

- The EAF vs blast furnace emissions debate is central to this transition, with significant investments directed toward green hydrogen in steel production and carbon capture technologies in steel. Innovation is also thriving in output, driven by construction sector steel demand drivers and the need for automotive lightweighting with advanced steel, which in turn fuels value-added steel product innovation.

- Companies are developing resilient steel supply chains to navigate environmental compliance costs, which are heavily influenced by national industrial policy and trade protectionism in the steel market. Ultimately, managing raw material cost volatility impact remains a constant challenge that advanced analytics and regional sourcing strategies aim to mitigate.

What are the key market drivers leading to the rise in the adoption of Steel Manufacturing Industry?

- Robust demand from the global construction and infrastructure sectors serves as a primary driver for market growth.

- The strategic imperative for decarbonization is a major driver, catalyzing investment in green steel production. This transition involves shifting from pig iron-based methods toward direct reduced iron and pioneering hydrogen-based steelmaking, which significantly lowers energy intensity.

- Adherence to circular economy principles and strict environmental compliance mandates is now a competitive differentiator. Demand for high-performance materials, like cold-rolled steel and specialized electrical steel, is increasing for use in electric vehicles and renewable energy infrastructure.

- The capital expenditure for this transition is immense, but it is essential for producing the semi-finished products and performing the necessary beneficiation that next-generation industries require.

What are the market trends shaping the Steel Manufacturing Industry?

- A prominent trend is the rise of protectionist trade policies, which is compelling a strategic regionalization of supply chains across the industry.

- A key trend is the pervasive adoption of Industry 4.0 integration, creating the smart factory of the future. The use of digital twin technology has accelerated the development of value-added products, such as advanced high-strength steels, reducing new grade validation times by 20%.

- This innovation in hot-rolled coil and specialty steel is crucial for lightweighting initiatives in automotive, where inter-material competition is fierce. Furthermore, AI-driven predictive maintenance is improving operational efficiency by cutting unplanned downtime by up to 15%. This digital shift, coupled with supply chain regionalization driven by anti-dumping duties, is fundamentally reshaping competitive dynamics and process standards.

What challenges does the Steel Manufacturing Industry face during its growth?

- Persistent global overcapacity and the resulting intense price competition present a key challenge to industry growth and profitability.

- Persistent global overcapacity is a structural challenge, intensifying price-based inter-material competition and hindering the economies of scale needed for profitability. Producers using the traditional blast furnace route are particularly vulnerable to raw material volatility, especially in the coking coal market, with cost fluctuations of up to 40% in a single quarter.

- Navigating complex regulatory frameworks like the emissions trading system introduces high costs and the risk of carbon leakage. This environment complicates investment in advanced materials like alloy steel and stainless steel, which require sophisticated tempering and carburizing processes, as well as in commodity products such as tinplate. The pressure of carbon pricing further squeezes margins across the industry.

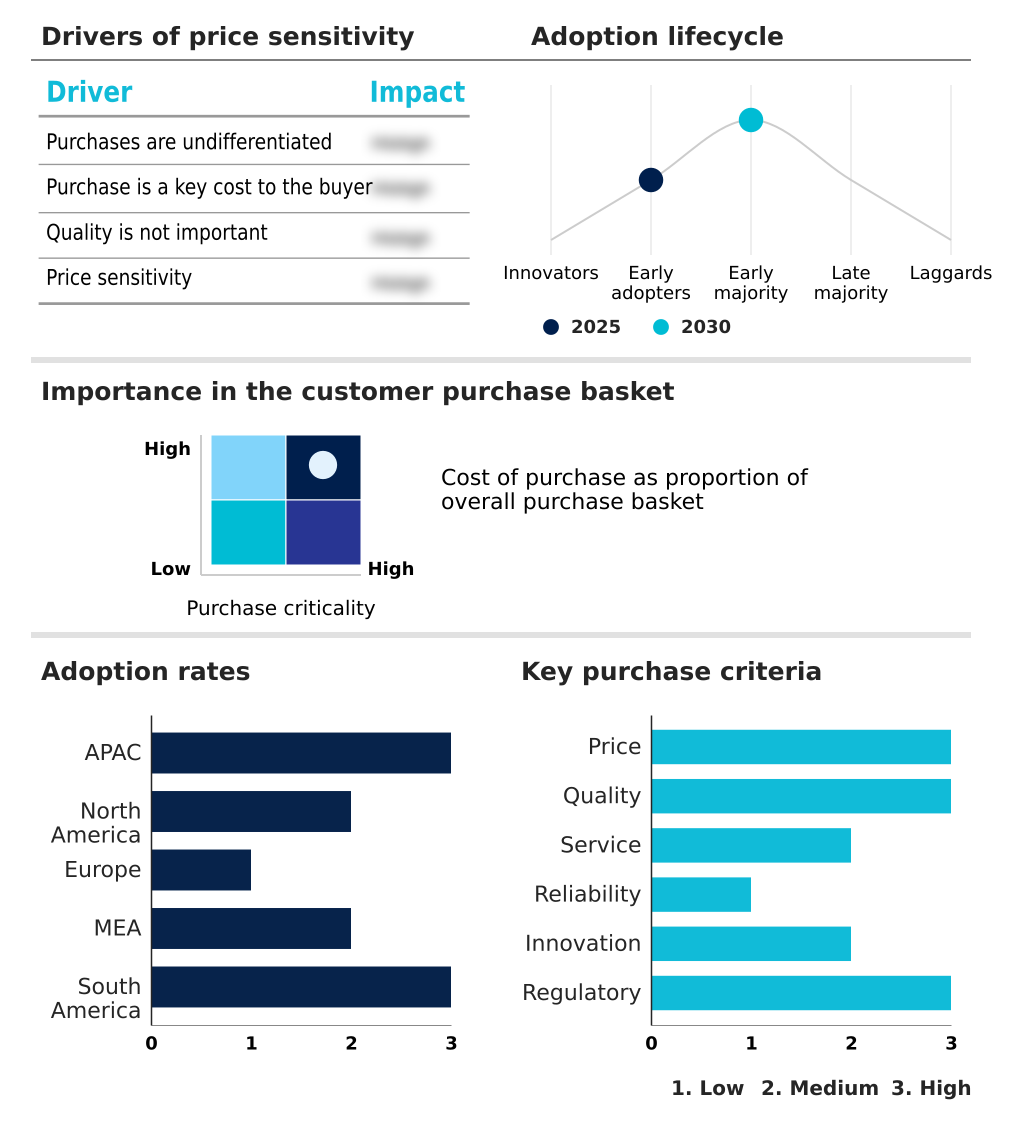

Exclusive Technavio Analysis on Customer Landscape

The steel manufacturing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the steel manufacturing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Steel Manufacturing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, steel manufacturing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ArcelorMittal SA - The vendor provides a diverse portfolio of flat, long, and tubular steel products, including specialized electrical steels for advanced industrial and automotive applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ArcelorMittal SA

- BAOWU Metal

- Benteler International AG

- Essar

- Gerdau SA

- Hyundai Steel Co.

- JFE Holdings Inc.

- Jiangsu Shagang Group

- Jingye Steel Group Co.

- JSW Holdings Ltd.

- Mukand Ltd.

- Nippon Steel Corp.

- NLMK Group

- Nucor Corp.

- Steel Authority of India Ltd.

- Steel Dynamics Inc.

- Tata Steel Ltd.

- thyssenkrupp AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Steel manufacturing market

- In February 2025, Gerdau announced a landmark investment of over $2 billion to construct a new green steel facility at its Ouro Branco mill in Brazil, centered on a new Direct Reduced Iron (DRI) plant capable of transitioning to green hydrogen.

- In February 2025, Baosteel Group signed a memorandum of understanding with Siemens Energy to collaborate on the development and acceleration of hydrogen-based steelmaking technology.

- In January 2025, JFE Steel Corp. announced the first sale of its JGreeX green steel to a Japanese steel distributor, JFE Shoji Pipe and Fitting Corp., expanding sustainable products into the steel pipe sector.

- In April 2025, the Indian government implemented significant revisions to its domestic steel procurement policy, mandating the use of domestically manufactured iron and steel for all government tenders and public projects to bolster local production.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Steel Manufacturing Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 327 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.2% |

| Market growth 2026-2030 | USD 434.4 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.1% |

| Key countries | China, India, Japan, South Korea, Indonesia, Australia, US, Canada, Mexico, Germany, Italy, Spain, France, The Netherlands, UK, Turkey, Saudi Arabia, South Africa, UAE, Israel, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The global steel manufacturing market 2026-2030 is undergoing a fundamental pivot from volume to value, driven by the dual pressures of decarbonization and sophisticated end-user demand. The industry's trajectory is no longer defined solely by crude steel output but by the strategic production of advanced high-strength steels, specialty steel, and other value-added products.

- Boardroom-level decisions now center on massive capital allocation for green steel initiatives, weighing the long-term benefits of new direct reduced iron plants against retrofitting existing blast furnace operations with carbon capture technology.

- This strategic shift is validated by financial performance, as producers of high-performance flat products and long products report margins up to 20% higher than those for commodity-grade rebar or hot-rolled coil. Success depends on mastering complex metallurgy, including tempering and carburizing for alloy steel and tool steels, while managing volatile input costs for iron ore and coking coal.

- The transition to electric arc furnace production, fueled by scrap steel, is accelerating this trend toward a more sustainable and profitable future.

What are the Key Data Covered in this Steel Manufacturing Market Research and Growth Report?

-

What is the expected growth of the Steel Manufacturing Market between 2026 and 2030?

-

USD 434.4 billion, at a CAGR of 4.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Construction, Machinery, Automotive, Metal products, and Others), Type (Flat, and Long), Application (Automotive, Mechanical equipment, Building and construction, Metal products, and Others) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Robust demand from global construction and infrastructure sectors, Persistent global overcapacity and intense price competition

-

-

Who are the major players in the Steel Manufacturing Market?

-

ArcelorMittal SA, BAOWU Metal, Benteler International AG, Essar, Gerdau SA, Hyundai Steel Co., JFE Holdings Inc., Jiangsu Shagang Group, Jingye Steel Group Co., JSW Holdings Ltd., Mukand Ltd., Nippon Steel Corp., NLMK Group, Nucor Corp., Steel Authority of India Ltd., Steel Dynamics Inc., Tata Steel Ltd. and thyssenkrupp AG

-

Market Research Insights

- The market is shaped by intense inter-material competition and a strategic pivot toward sustainable production methods. This shift is creating new operational benchmarks, as the adoption of predictive maintenance has led to a 15% reduction in unplanned downtime, directly enhancing operational efficiency.

- Furthermore, process optimization through digital twin technology is improving energy intensity, with some facilities reporting a 10% improvement in energy use. These advancements are critical as companies navigate complex environmental compliance standards and manage significant capital expenditure.

- The pursuit of circular economy principles is not just a regulatory requirement but a competitive advantage, forcing a comprehensive lifecycle assessment of products and processes. This focus on decarbonization and efficiency is fundamentally altering the industry’s value chain analysis and long-term investment priorities.

We can help! Our analysts can customize this steel manufacturing market research report to meet your requirements.

RIA -

RIA -