Medical Connectors Market Size 2025-2029

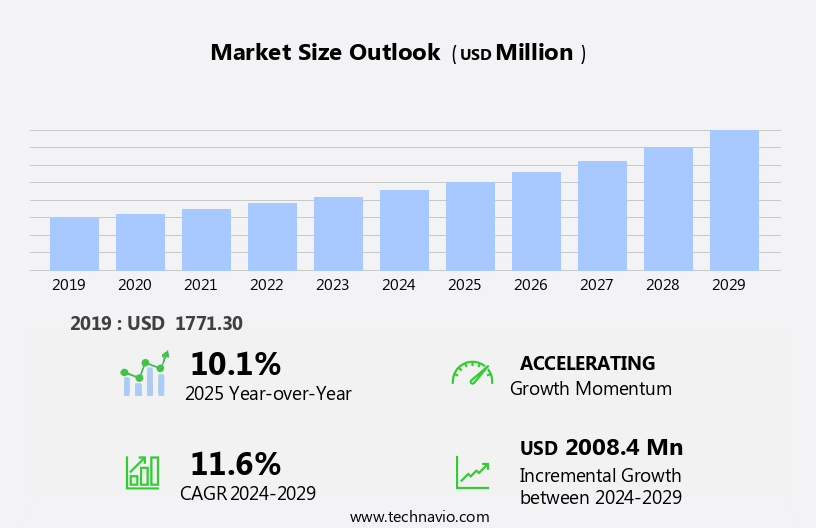

The medical connectors market size is forecast to increase by USD 2.01 billion, at a CAGR of 11.6% between 2024 and 2029.

- The market is experiencing significant growth due to the increasing prevalence of chronic diseases and the subsequent demand for advanced medical devices. This trend is driving the need for reliable and efficient medical connectors to ensure seamless data transfer and power supply between various medical devices. Another key factor fueling market growth is the increasing number of product approvals for medical connectors, which allows manufacturers to bring new and innovative solutions to market. However, the market faces challenges in the form of stringent regulatory compliance requirements associated with the approval of medical connectors. These regulations ensure the safety and effectiveness of medical connectors but add complexity to the development and approval process.

- Companies in the market must navigate these challenges while also staying abreast of the latest technological advancements and consumer needs to maintain a competitive edge. To capitalize on market opportunities and navigate challenges effectively, companies should focus on developing innovative medical connectors that meet regulatory requirements while addressing the unique needs of various medical applications. Additionally, strategic partnerships and collaborations can help companies streamline the approval process and expand their product offerings.

What will be the Size of the Medical Connectors Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market showcases a dynamic and evolving landscape, driven by advancements in technology and the expanding application scope across various sectors. Polymeric materials continue to gain traction due to their lightweight properties and biocompatibility, while electrical stimulation connectors are increasingly utilized in neurological devices and implantable sensors. Metallic materials, meanwhile, offer superior conductivity and durability for surgical equipment and cardiac devices. Quality control and regulatory compliance remain paramount, with CE marking and FDA compliance being essential for market entry. Connector design innovations include gamma irradiation for sterilization and wearable sensors for remote patient monitoring. Insulation materials ensure signal integrity, while connector reliability is crucial for implantable drug delivery systems.

Connector shape and size variations cater to diverse medical applications, from external connectors for diagnostic equipment to reusable connectors for orthopedic implants. Connector termination techniques and connector interoperability are critical for seamless integration in complex medical systems. Biomedical engineering breakthroughs have led to advancements in connector technology, including injection molding for cost-effective production and sterilization techniques like ethylene oxide and EMI shielding for improved performance. Connector life cycle considerations and connector failure analysis are essential for ensuring optimal functionality and longevity. In the ever-evolving market, continuous innovation and adaptability are key. The market's ongoing unfolding is shaped by the interplay of various factors, including technological advancements, regulatory requirements, and the needs of diverse medical applications.

How is this Medical Connectors Industry segmented?

The medical connectors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Hospitals and clinics

- Ambulatory surgical centers

- Diagnostic laboratories and imaging centers

- Application

- Patient monitoring devices

- Electrosurgical devices

- Diagnostic imaging devices

- Cardiology devices

- Others

- Material

- Plastic

- Metal

- Silicone

- Composite materials

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- Spain

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

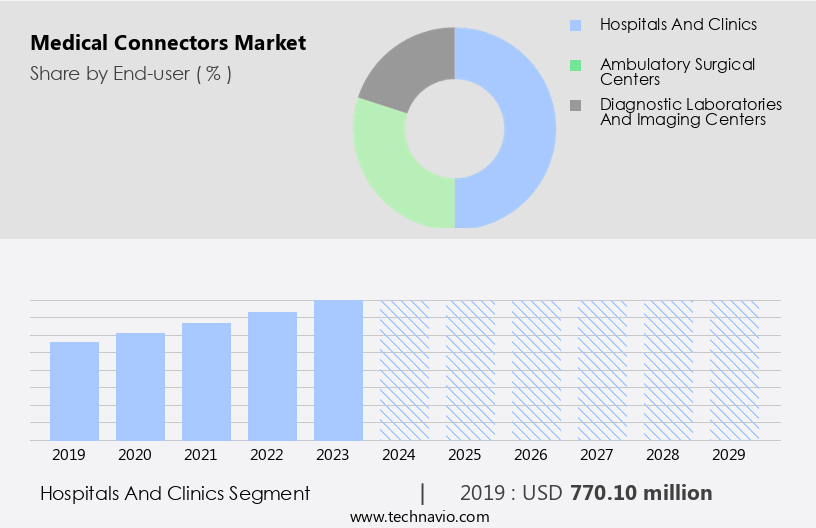

By End-user Insights

The hospitals and clinics segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth due to the increasing demand for advanced medical devices in hospitals and clinics. The hospitals and clinics segment is currently the largest and fastest-growing end-user segment, driven by the rising prevalence of chronic diseases and medical conditions requiring hospitalization and surgical intervention. The geriatric population's increasing number and the adoption of technologically advanced ophthalmologic and diagnostic devices are further fueling the demand for medical devices in hospitals, leading to an increased need for medical connectors. Ceramic materials and metallic materials are commonly used in connector design due to their biocompatibility and electrical conductivity.

Voltage ratings, current carrying capacity, and signal integrity are essential factors considered during connector design. Injection molding and other sterilization techniques, such as ethylene oxide and gamma irradiation, are employed to ensure connector reliability and biocompatibility. Implantable sensors and neurological devices require single-use connectors to maintain sterility and prevent contamination. Reusable connectors are widely used in surgical equipment, cardiac devices, and diagnostic equipment. CE marking and FDA compliance are crucial regulatory requirements for connector design and manufacturing. Connector size, connector shape, and connector termination are essential design considerations for medical connectors. Connector interoperability and connector life cycle are crucial factors in ensuring seamless data transmission and minimizing connector failure.

Quality control and regulatory compliance are essential to ensure the safety and effectiveness of medical connectors. Polymeric materials and insulation materials are commonly used in connector assembly and packaging. Electrical impedance, EMI shielding, and RFI shielding are essential considerations for connector design to minimize interference and ensure signal integrity. Wearable sensors and drug delivery systems are emerging applications for medical connectors, driving innovation and growth in the market. In conclusion, the market is witnessing significant growth due to the increasing demand for advanced medical devices in hospitals and clinics. The market is driven by factors such as the rising prevalence of chronic diseases, the increasing number of geriatric population, and the adoption of technologically advanced medical devices.

Ceramic materials, metallic materials, and polymeric materials are commonly used in connector design, and injection molding and sterilization techniques are employed to ensure connector reliability and biocompatibility. Regulatory compliance and connector interoperability are essential considerations for connector design and manufacturing. The market is witnessing innovation and growth in emerging applications such as wearable sensors and drug delivery systems.

The Hospitals and clinics segment was valued at USD 770.10 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The North American market is experiencing notable growth due to several driving factors. The increasing prevalence of chronic diseases, growing health consciousness among consumers, and substantial investments in healthcare infrastructure are primary contributors to this market's expansion. The US, as the largest market for medical connectors globally, leads the North American region with a significant revenue share. With over 6,500 medical device companies in the US, most of which are small and medium-sized enterprises, the demand for advanced medical connectors is expected to remain robust. Key trends in the market include the use of biocompatible materials, such as ceramics and polymerics, for connector manufacturing.

These materials ensure the durability and reliability of connectors in various medical applications, including implantable sensors, neurological devices, and cardiac devices. Voltage ratings, connector size, and current carrying capacity are crucial factors in connector design, ensuring signal integrity and electrical impedance. Regulatory compliance, such as CE marking and FDA approval, is essential for connector manufacturers to ensure their products meet the stringent requirements of the medical industry. Sterilization techniques, including ethylene oxide and gamma irradiation, are critical in maintaining connector hygiene and preventing contamination. Connector termination, connector assembly, and connector housing design are essential aspects of connector manufacturing, ensuring reliable and efficient connections in medical devices.

Innovations in medical connectors include the development of reusable connectors, which reduce the overall cost of medical devices and minimize waste. EMI shielding and RFI shielding are essential features in medical connectors, ensuring the protection of sensitive electronic components from electromagnetic interference. Connector failure analysis and data transmission rates are critical factors in connector reliability, ensuring seamless communication between various medical devices. The market is witnessing significant advancements in wearable sensors, drug delivery systems, and orthopedic implants. These applications require connectors with high durability, low weight, and precise dimensions. Injection molding and other advanced manufacturing techniques are being employed to create connectors with intricate shapes and complex geometries, enabling the development of more advanced medical devices.

Regulatory bodies, such as the FDA, are implementing stringent testing standards to ensure the safety and efficacy of medical connectors. Biomedical engineering and connector design are critical aspects of the medical connectors industry, with a focus on developing connectors that meet the unique requirements of various medical applications while ensuring patient safety and comfort. Overall, the market is expected to continue its growth trajectory, driven by the increasing demand for advanced medical devices and the ongoing innovation in connector technology.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses a diverse range of specialized components that facilitate the transfer of fluids, gases, and data between medical devices and patients. These connectors are essential in various medical applications, including infusion systems, anesthesia delivery systems, and patient monitoring equipment. Key players in this market prioritize materials like silicone, polyurethane, and PVC for their biocompatibility and resistance to chemicals and bacteria. Advanced technologies, such as radiofrequency identification (RFID) and barcode scanning, enhance the functionality and safety of medical connectors. Other critical factors include miniaturization, ease of use, and sterilization compatibility. The market is driven by factors like an aging population, increasing prevalence of chronic diseases, and technological advancements in healthcare.

What are the key market drivers leading to the rise in the adoption of Medical Connectors Industry?

- The rising prevalence of chronic diseases serves as the primary market driver, significantly expanding its scope and demand.

- The medical connector market is experiencing significant growth due to the increasing prevalence of chronic diseases and the resulting demand for advanced medical devices. These devices, including neurological and cardiac devices, surgical equipment, and diagnostic tools, require high-quality connectors for precise and reliable connectivity solutions. The importance of medical connectors is amplified by the ongoing need for monitoring and management of chronic conditions, leading to a continuous demand for patient monitoring devices, imaging equipment, and other medical devices. Medical connectors must meet stringent requirements, such as sterilization techniques, FDA compliance, and biocompatible materials. Injection molding is a common manufacturing process used to produce medical connectors due to its ability to create complex shapes and sizes while maintaining connector weight and current carrying capacity.

- Connector interoperability and connector life cycle are also crucial considerations in the medical connector market. Medical connectors come in various sizes, from small connectors used in neurological devices to larger connectors used in cardiac devices. Regardless of size, these connectors must maintain the highest level of reliability and precision to ensure optimal performance in medical applications. By focusing on these key factors, medical connector manufacturers can meet the evolving needs of the medical device industry and contribute to improved patient outcomes.

What are the market trends shaping the Medical Connectors Industry?

- The approval of medical connectors for more products is a significant market trend that is gaining momentum. This trend underscores the increasing demand for advanced medical technology and the importance of reliable connectors in ensuring their effective integration.

- The market continues to evolve, driven by technological advancements and growing demand for advanced medical devices. Innovations in connector design, material selection, and manufacturing processes are leading to the launch of new and improved connector solutions. For instance, Fischer Connectors introduced First Mate Last Break connectors in its low-voltage multipole Fischer Core Series, offering superior electrical safety, mechanical dependability, and user-friendliness for medical device operators. Additionally, Nicomatic and SnapEDA collaborated to make CAD models of over 8 million Nicomatic connectors available, enhancing design efficiency and facilitating faster time-to-market for medical device manufacturers. Quality control and regulatory compliance remain top priorities in the market, with a focus on insulation materials, connector shape, and metallic materials to ensure connector reliability and gamma irradiation resistance.

- Furthermore, the integration of medical connectors into drug delivery systems, electrical stimulation devices, wearable sensors, and electrical impedance monitoring systems is expanding the market's scope and driving growth.

What challenges does the Medical Connectors Industry face during its growth?

- The stringent regulatory compliance required for the approval of medical connectors poses a significant challenge to the growth of the industry. Adhering to these regulations adds complexity and cost to the manufacturing process, delaying product launches and increasing operational expenses. Ensuring compliance with various standards, such as ISO 13485 and FDA regulations, is essential to prevent potential risks to patient safety and maintain market credibility. Consequently, companies must invest heavily in research and development, quality assurance, and regulatory affairs to meet these demands and stay competitive in the market.

- Medical connectors play a vital role in ensuring the proper functioning of various medical devices, including orthopedic implants and implantable connectors. The regulatory approval process for these connectors is stringent and complex, with the Food and Drug Administration (FDA) overseeing the process in the US. Manufacturers must adhere to quality system regulations and undergo a comprehensive premarket submission process, which includes substantial documentation and clinical testing. This rigorous process aims to ensure patient safety and product quality but can lead to prolonged approval timelines and increased development costs. In Europe, the European Medicines Agency (EMA) and notified bodies under the Medical Device Regulation (MDR) govern the approval process.

- The stringent requirements for medical connectors help maintain signal integrity, connector durability, and compliance with testing standards, such as rfi shielding and data transmission rates. Biomedical engineering and connector applications continue to evolve, requiring ongoing research and development to meet the demands of the medical industry. Connector housings and external connectors must also meet these stringent requirements, with connector failure analysis playing a crucial role in identifying and addressing any issues.

Exclusive Customer Landscape

The medical connectors market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the medical connectors market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, medical connectors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amphenol Corp. - This company specializes in supplying medical connectors, including Pulse-Lok connectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amphenol Corp.

- CFE Corp. Co. Ltd.

- Clear Path Medical

- Eaton Corp. plc

- Fischer Connectors Holding SA

- ITT Inc.

- KEL Corp.

- Koch Industries Inc.

- KYOCERA Corp.

- LEMO SA

- Neutrik AG

- Nicomatic

- ODU GmbH and Co. KG

- Rosenberger Hochfrequenztechnik GmbH and Co. KG

- Samtec Inc.

- SENKO Advanced Components Inc.

- Shenzhen Medke Technology Co. Ltd.

- Shenzhen Medplus Electronic Tech Co. Ltd.

- Smiths Group Plc

- TE Connectivity Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Medical Connectors Market

- In January 2024, Medtech Connectors, a leading medical connector manufacturer, announced the launch of their new line of radiofrequency (RF) sealing connectors, designed for minimally invasive surgical procedures. These connectors ensure airtight seals, reducing the risk of complications and improving patient safety (Medtech Connectors Press Release).

- In March 2024, Smiths Medical and Medtronic, two major players in the medical device industry, entered into a strategic partnership to co-develop advanced medical connectors for infusion and enteral feeding systems. This collaboration aims to enhance product offerings and expand their market reach (Smiths Medical Press Release).

- In May 2024, TE Connectivity, a global industrial technology leader, completed the acquisition of Conexant Systems, a medical connector and cable assembly provider. This acquisition strengthened TE Connectivity's position in the market, broadening their product portfolio and expanding their customer base (TE Connectivity SEC Filing).

- In February 2025, the US Food and Drug Administration (FDA) approved the use of a new type of silicone medical connector, designed by 3M, for use in hemodialysis systems. This approval marked a significant technological advancement in medical connectors, enabling more flexible and durable connections for long-term patient care (FDA Press Release).

Research Analyst Overview

- The market encompasses a diverse range of products, from custom connectors to high-speed and wireless solutions, all designed to facilitate signal transmission and ensure reliable communication between medical devices and systems. The market is driven by various trends, including miniaturization, end-user preferences, and the need for increased connector reliability and safety. Connector design software plays a crucial role in creating efficient and effective connector solutions. Material science advances have led to the development of new raw materials, enabling the production of connectors with enhanced mechanical strength, hermeticity, and material biocompatibility. Connector sterilization methods and safety standards are essential considerations, as medical connectors must withstand rigorous cleaning and sterilization processes without compromising their electrical resistance or waterproofing capabilities.

- Industry standards, such as IEC and UL, ensure consistency and interoperability across various connector types and applications. Connector failure modes and lifespan are critical factors in supply chain management, as connector reliability testing and assembly processes must be optimized to minimize the risk of defects and ensure consistent performance over extended periods. Future trends include the adoption of automation in connector manufacturing and the integration of wireless connectivity to enable remote monitoring and data transfer. Pricing strategies and distribution channels continue to evolve, with an increasing focus on cost-effective solutions and direct-to-customer models. Connector assembly processes and material sourcing are key areas of focus for manufacturers seeking to improve efficiency and reduce costs.

- Low-profile connectors and high-speed solutions are in high demand, as medical devices become more complex and compact. In the realm of material science, research continues to explore new methods for enhancing connector electrical resistance, waterproofing, and mechanical strength, while ensuring biocompatibility and compliance with safety standards. Overall, the market is characterized by ongoing innovation, stringent regulatory requirements, and a focus on reliability, safety, and efficiency.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Medical Connectors Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

228 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 11.6% |

|

Market growth 2025-2029 |

USD 2008.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

10.1 |

|

Key countries |

US, China, Japan, Canada, Germany, UK, France, India, Italy, and Spain |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Medical Connectors Market Research and Growth Report?

- CAGR of the Medical Connectors industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the medical connectors market growth of industry companies

We can help! Our analysts can customize this medical connectors market research report to meet your requirements.

RIA -

RIA -