Medical Imaging Software Market Size 2026-2030

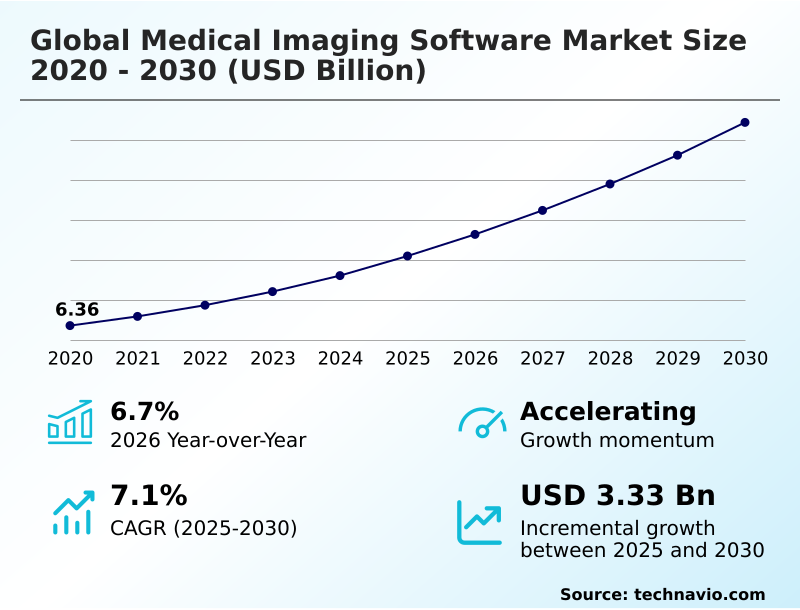

The medical imaging software market size is valued to increase by USD 3.33 billion, at a CAGR of 7.1% from 2025 to 2030. Transition toward precision medicine and utilization of quantitative imaging biomarkers will drive the medical imaging software market.

Major Market Trends & Insights

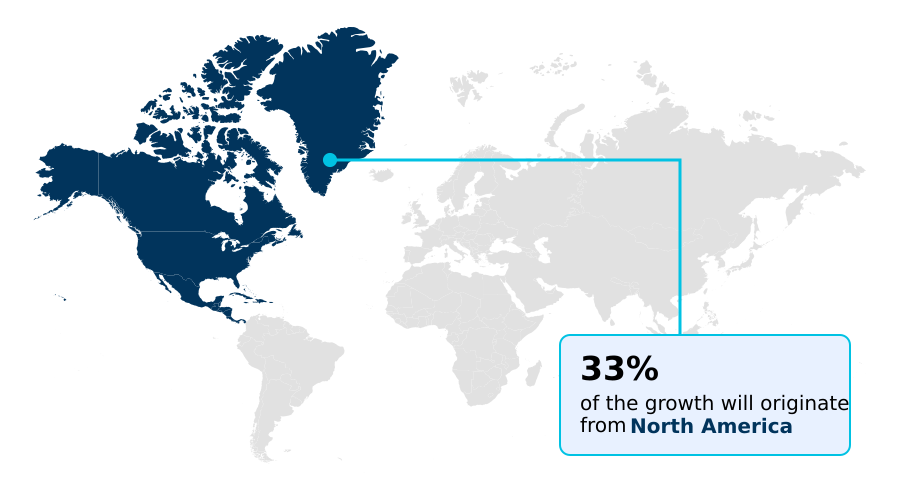

- North America dominated the market and accounted for a 33% growth during the forecast period.

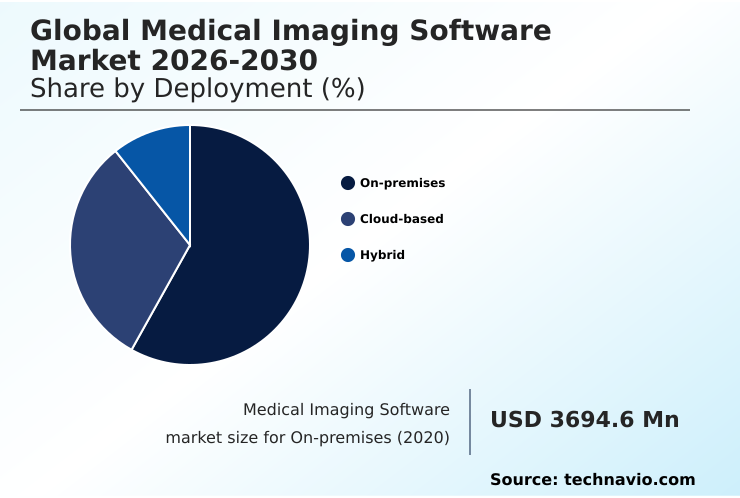

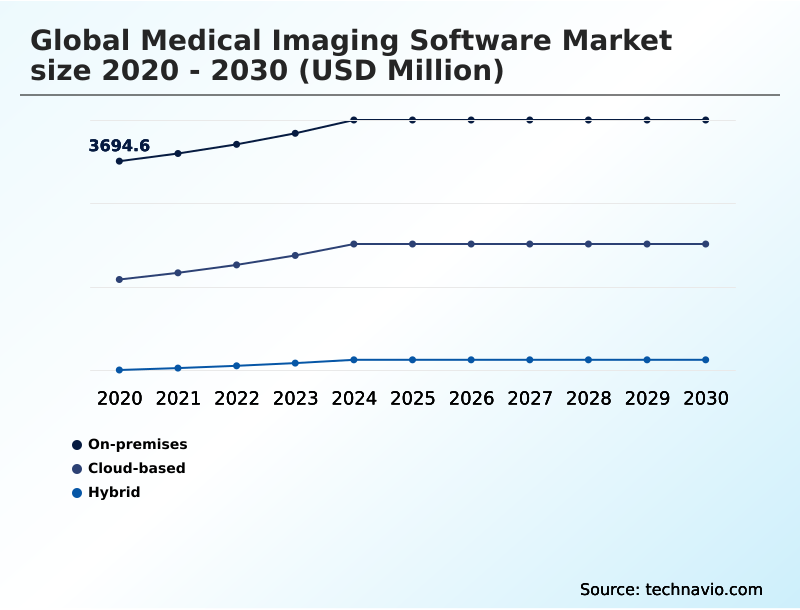

- By Deployment - On-premises segment was valued at USD 4.29 billion in 2024

- By End-user - Hospitals segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 5.08 billion

- Market Future Opportunities: USD 3.33 billion

- CAGR from 2025 to 2030 : 7.1%

Market Summary

- The medical imaging software market is undergoing a period of robust expansion, driven by the increasing integration of advanced digital technologies within clinical settings. This growth is primarily motivated by the rising prevalence of chronic conditions and the subsequent demand for precise diagnostic tools.

- Healthcare organizations are progressively adopting sophisticated software solutions to streamline the interpretation of complex datasets and to reduce the workload of radiologists. The shift toward digital health ecosystems has made high levels of interoperability essential, allowing for the smooth exchange of information. For instance, a multi-site hospital network can implement an enterprise imaging platform that standardizes diagnostic protocols for oncology.

- This enables seamless sharing of computed tomography and magnetic resonance imaging scans, facilitates AI-driven analysis for early tumor detection, and supports collaborative treatment planning, ultimately improving patient outcomes and operational efficiency across all facilities. The growth of the market is also supported by the increasing preference for non-invasive diagnostic procedures, which rely heavily on high-resolution imaging and sophisticated visualization tools.

- Cloud-native solutions are becoming the standard for data storage and analysis, providing healthcare practitioners with the flexibility to access critical images from remote locations while maintaining data security.

What will be the Size of the Medical Imaging Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Medical Imaging Software Market Segmented?

The medical imaging software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- On-premises

- Cloud-based

- Hybrid

- End-user

- Hospitals

- Diagnostic imaging centers

- Others

- Modality

- Computed tomography

- Magnetic resonance imaging

- Ultrasound imaging

- X-ray imaging

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Asia

- Rest of World (ROW)

- North America

By Deployment Insights

The on-premises segment is estimated to witness significant growth during the forecast period.

On-premises deployment remains a significant segment, largely driven by the need for high-speed data access and maximum control over patient data privacy compliance.

Healthcare institutions prioritize this model for its local system performance, which is crucial for real-time diagnostic workflows using picture archiving and communication systems.

This approach minimizes latency, reducing data access times by over 90% for critical cases that rely on server-side rendered medical images. However, achieving seamless electronic health records integration requires adherence to strict interoperability standards and data standardization protocols.

While digital health ecosystems are evolving toward cloud-based remote diagnostics platforms and centralized imaging archives, the security and performance benefits of on-premises solutions, governed by the digital imaging and communications in medicine standard, ensure their continued relevance in the market.

The On-premises segment was valued at USD 4.29 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Medical Imaging Software Market Demand is Rising in North America Get Free Sample

The geographic landscape of the market is characterized by varied adoption rates and technological priorities. In North America, the focus is on optimizing mature digital health ecosystems with advanced ai-integrated enterprise imaging and ai-powered brain imaging solutions.

Growth in Asia outpaces other regions, with an 8.9% expansion rate compared to 6.2% in North America, driven by widespread digital health transformation and the deployment of cloud-native ris/pacs platforms.

Tele-radiology frameworks are critical in geographically dispersed areas like Australia, where tele-ultrasound capabilities have reduced diagnostic turnaround times by up to 40%. The adoption of point-of-care diagnostics and quantitative magnetic resonance imaging is accelerating globally.

Advanced techniques such as three-dimensional reconstruction and elastography software are becoming standard in surgical planning applications, improving procedural accuracy and patient outcomes.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the global medical imaging software market 2026-2030 is defined by a strategic shift from standalone systems to interconnected, intelligent platforms. Central to this transformation is the ai integration in diagnostic workflows, which leverages deep learning for image segmentation to automate analysis and improve accuracy.

- The adoption of a cloud native architecture for medical imaging is accelerating, enabling saas models in radiology software that offer scalability and reduce capital expenditure. This infrastructure supports advanced applications like 3d visualization in surgical planning and multimodal imaging for oncology planning, which are critical for modern treatment paradigms.

- Ensuring the interoperability of pacs and ehr systems remains a core objective, facilitated by vendor neutral archive data management solutions that break down data silos. Facilities using such platforms report up to 25% lower data migration costs compared to proprietary systems.

- Concurrently, heightened cybersecurity in medical imaging data is a non-negotiable requirement, with gdpr compliance for imaging software and software as a medical device regulation shaping development standards. Innovations in point of care ultrasound software, virtual reality for preoperative rehearsals, and the use of quantitative biomarkers in precision medicine are pushing the boundaries of diagnostics.

- Teleradiology frameworks for rural healthcare are expanding access, while developments like server side rendered image viewing, ai driven clinical data management, and ris pacs for automated workflows are optimizing efficiency. Furthermore, ai powered brain imaging analysis and the growth of theranostics in molecular imaging highlight the industry's trajectory toward highly personalized and predictive healthcare.

What are the key market drivers leading to the rise in the adoption of Medical Imaging Software Industry?

- The transition toward precision medicine, underscored by the increasing utilization of quantitative imaging biomarkers, serves as a key driver propelling market expansion.

- Market growth is fundamentally driven by the push for more precise and personalized healthcare. Precision medicine initiatives rely on quantitative imaging biomarkers and radiomics data characterization to provide deeper clinical insights, which aligns with the objectives of value-based healthcare models.

- Advanced visualization software and multimodal imaging fusion are critical for complex cases, especially in oncology, where they support multi-disciplinary tumor boards and automated diagnostic reporting.

- The use of longitudinal tracking software to facilitate longitudinal disease monitoring for chronic conditions has demonstrated a 95% consistency rate in tracking disease progression. As more software as a medical device solutions receive regulatory approval, their adoption is accelerating.

- These tools, which include capabilities for positron emission tomography reconstruction, are essential for population health management and are improving patient outcomes.

What are the market trends shaping the Medical Imaging Software Industry?

- The integration of artificial intelligence and machine learning algorithms into diagnostic workflows represents a defining market trend. This evolution is fundamentally enhancing diagnostic accuracy and operational efficiency.

- Key trends are reshaping diagnostic capabilities, with a pronounced shift toward intelligent and immersive technologies. The adoption of deep learning algorithms for automated image segmentation and the deployment of predictive analytics models are enhancing diagnostic precision, with some systems improving anomaly detection accuracy by over 25%.

- Cloud-native architectures are becoming standard, facilitating software-as-a-service models that reduce data retrieval times for remote consultations by up to 50%. This supports advanced applications in diagnostic imaging workflows, including virtual and augmented reality for minimally invasive procedures planning. Additionally, the market is seeing growth in real-time four-dimensional imaging and theranostics quantification, supported by ai-powered imaging informatics and ai-driven visualization software.

- These innovations, combined with advances in cloud-based imaging informatics, are creating a more dynamic and responsive diagnostic environment.

What challenges does the Medical Imaging Software Industry face during its growth?

- Prohibitive capital investment requirements and substantial ongoing maintenance expenditures present a significant challenge affecting widespread industry adoption and growth.

- Despite technological advancements, significant challenges related to integration, cost, and security persist. The lack of standardized protocols across different enterprise imaging platforms impedes the creation of unified clinical workflows and vendor-neutral data management. This fragmentation can increase manual data reconciliation efforts by up to 30% and complicate the use of radiology information systems.

- High capital costs for advanced technologies like high-intensity focused ultrasound and tomosynthesis software create barriers to adoption. Moreover, ensuring compliance with evolving cybersecurity mandates for healthcare is a constant concern, requiring robust security in both on-premise and cloud-enabled clinical decision support systems.

- Efficiently processing data from digital radiography processing and utilizing tools like bone densitometry software and fluoroscopy image guidance depend on effective image reconstruction algorithms and interoperable infrastructure.

Exclusive Technavio Analysis on Customer Landscape

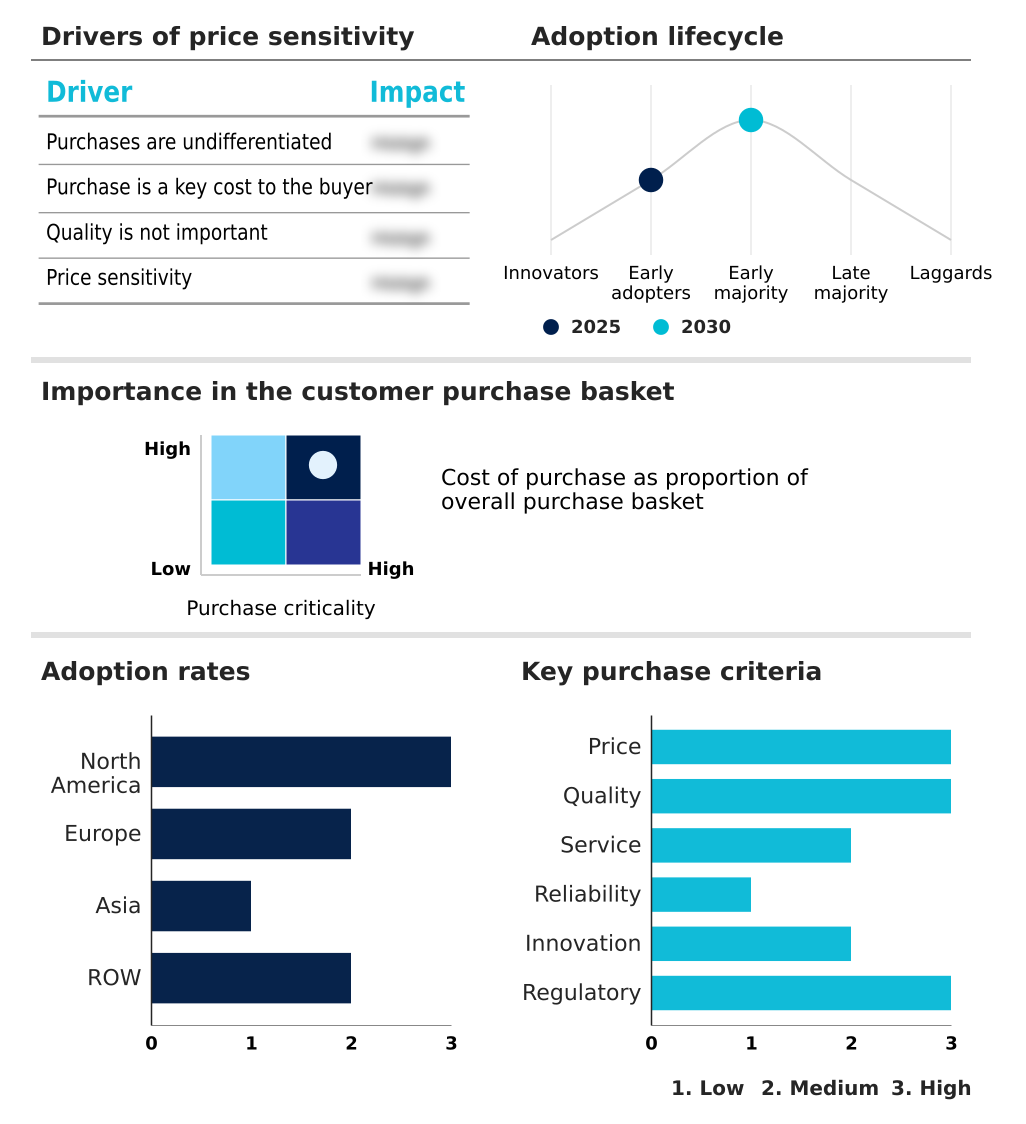

The medical imaging software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the medical imaging software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Medical Imaging Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, medical imaging software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agfa Gevaert NV - Enterprise imaging platforms consolidate image management, unifying diagnostic data across diverse medical departments for streamlined clinical workflows.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agfa Gevaert NV

- Aidoc Medical Ltd.

- AnalyzeDirect Inc.

- Canon Medical Systems Corp.

- Carestream Health Inc.

- FUJIFILM Holdings Corp.

- GE HealthCare Technologies

- INFINITT North America

- Koninklijke Philips N.V.

- Merative L.P.

- Microsoft Corp.

- MIM Software Inc.

- Mirada Medical Ltd.

- NovaRad

- NVIDIA Corp.

- RamSoft Inc.

- Sectra AB

- Siemens Healthineers AG

- United Health Group Inc.

- Visage Imaging

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Medical imaging software market

- In February, 2025, the United States Department of Health and Human Services implemented a new cybersecurity mandate for all medical imaging software utilized in federal healthcare programs, aiming to protect patient data against advanced digital threats.

- In January, 2025, Quibim secured $50 million in Series A financing to advance its development of AI-powered imaging biomarkers, accelerating its mission to integrate advanced imaging analytics into clinical decision-making for precision medicine.

- In September, 2024, GE HealthCare announced an agreement to acquire icometrix, a company specializing in AI-powered brain imaging analysis for neurological disorders, to enhance its diagnostic capabilities in neurology.

- In December, 2024, Philips announced an agreement to acquire SpectraWAVE Inc., aiming to advance next-generation coronary intravascular imaging and physiological assessment through the integration of artificial intelligence technologies.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Medical Imaging Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.1% |

| Market growth 2026-2030 | USD 3332.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.7% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, The Netherlands, Spain, Russia, China, India, Japan, South Korea, Indonesia, Thailand, Singapore, Australia, Brazil, South Africa, Saudi Arabia, UAE and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The medical imaging software market is driven by the imperative to translate vast amounts of visual data into actionable clinical insights. The integration of quantitative imaging biomarkers and radiomics data characterization is foundational to this shift, enabling a transition from qualitative assessment to objective measurement.

- Boardroom decisions increasingly center on adopting advanced visualization software and multimodal imaging fusion technologies to maintain a competitive edge and improve diagnostic certainty. Deploying longitudinal tracking software is now a strategic priority for managing chronic diseases effectively. The adoption of deep learning algorithms for automated image segmentation has proven to increase radiologist throughput by over 20%.

- Technologies such as three-dimensional reconstruction, virtual and augmented reality, and theranostics quantification are no longer niche but are becoming central to personalized treatment planning. Furthermore, the backbone of this evolution rests on cloud-native architectures, which support predictive analytics models and ensure seamless electronic health records integration through standards like digital imaging and communications in medicine.

- Investments in picture archiving and communication systems and vendor-neutral archives are critical for future-proofing healthcare IT infrastructure.

What are the Key Data Covered in this Medical Imaging Software Market Research and Growth Report?

-

What is the expected growth of the Medical Imaging Software Market between 2026 and 2030?

-

USD 3.33 billion, at a CAGR of 7.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (On-premises, Cloud-based, and Hybrid), End-user (Hospitals, Diagnostic Imaging Centers, and Others), Modality (Computed tomography, Magnetic resonance imaging, Ultrasound imaging, X-ray imaging, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Transition toward precision medicine and utilization of quantitative imaging biomarkers, Prohibitive capital investment and maintenance expenditures

-

-

Who are the major players in the Medical Imaging Software Market?

-

Agfa Gevaert NV, Aidoc Medical Ltd., AnalyzeDirect Inc., Canon Medical Systems Corp., Carestream Health Inc., FUJIFILM Holdings Corp., GE HealthCare Technologies, INFINITT North America, Koninklijke Philips N.V., Merative L.P., Microsoft Corp., MIM Software Inc., Mirada Medical Ltd., NovaRad, NVIDIA Corp., RamSoft Inc., Sectra AB, Siemens Healthineers AG, United Health Group Inc. and Visage Imaging

-

Market Research Insights

- The market's momentum is shaped by the convergence of advanced technology and evolving healthcare demands. The expansion of tele-radiology frameworks has broadened diagnostic access, while the adoption of software-as-a-service models is lowering financial barriers to entry, reducing upfront IT expenditure by over 60% compared to traditional installations.

- Value-based healthcare models are driving investment in solutions that deliver measurable clinical and financial returns. This shift is supported by AI-driven visualization software and cloud-enabled clinical decision support tools that improve diagnostic precision. The integration of ai-powered brain imaging is enhancing neurological assessments, with some algorithms improving anomaly detection rates by 25%.

- Consequently, unified clinical workflows are becoming standard, streamlining operations from image acquisition to reporting.

We can help! Our analysts can customize this medical imaging software market research report to meet your requirements.

RIA -

RIA -