MEP Services Market Size 2026-2030

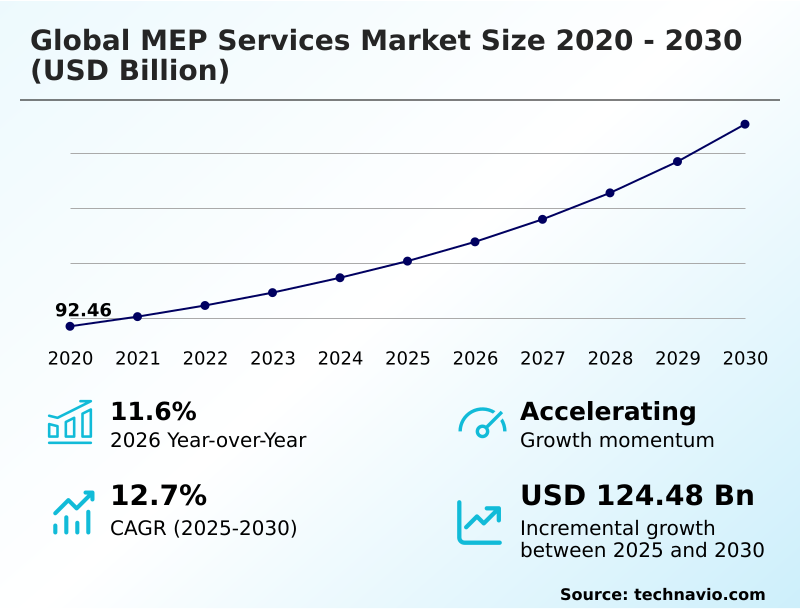

The mep services market size is valued to increase by USD 124.48 billion, at a CAGR of 12.7% from 2025 to 2030. Data center construction explosion will drive the mep services market.

Major Market Trends & Insights

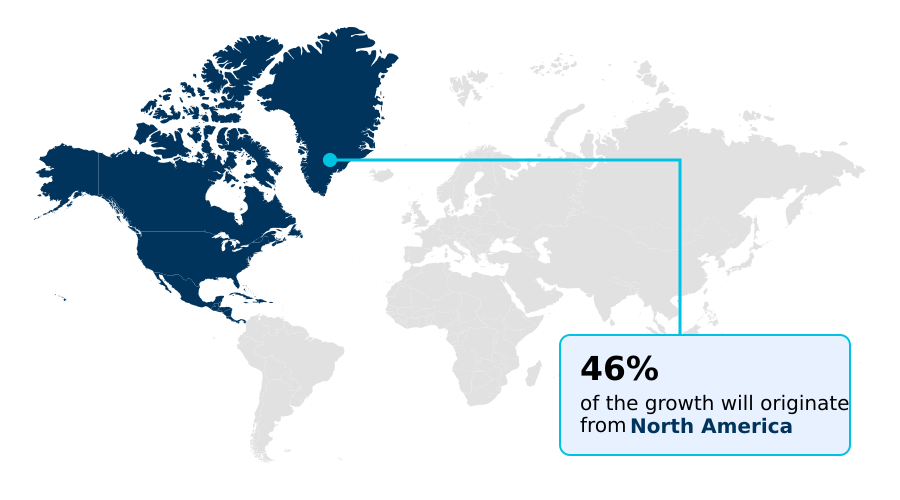

- North America dominated the market and accounted for a 45.9% growth during the forecast period.

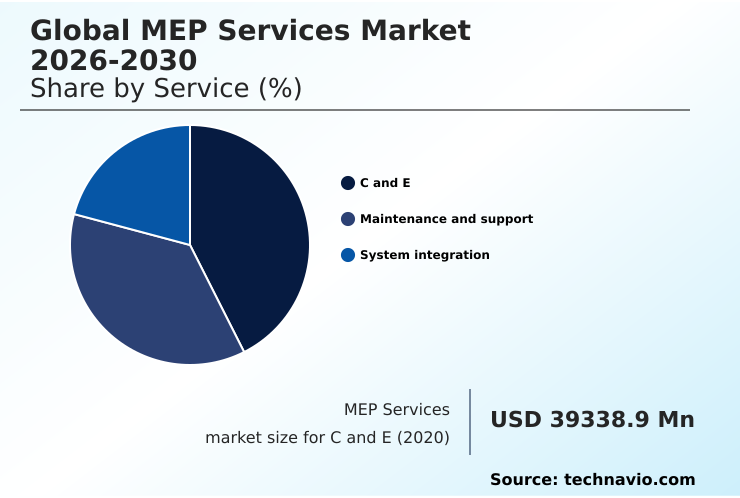

- By Service - C and E segment was valued at USD 56.59 billion in 2024

- By End-user - Commercial segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 183.73 billion

- Market Future Opportunities: USD 124.48 billion

- CAGR from 2025 to 2030 : 12.7%

Market Summary

- The MEP services market is undergoing a profound transformation, shifting from traditional construction trades to a data-centric discipline focused on high-performance building systems. This evolution is driven by the critical need for energy efficiency mandates and the global push toward net-zero carbon footprints.

- The surge in high-density data centers and advanced manufacturing facilities necessitates sophisticated power systems engineering and thermal management. A key trend is the integration of building information modeling and digital twin integration, which allows for predictive maintenance and asset lifecycle management.

- For instance, in a commercial building retrofit, MEP firms leverage IoT sensors and automated control systems to upgrade legacy equipment. This retrofitting legacy buildings approach not only ensures compliance with modern energy performance standards but also optimizes operational costs through improved water management solutions and hvac maintenance contracts.

- However, the industry's ability to capitalize on these opportunities is constrained by a persistent shortage of skilled labor, which affects project delivery and profitability. The adoption of prefabrication and modular mep offers a partial solution by moving construction into controlled environments, improving both efficiency and quality assurance. This focus on decarbonization services and sustainable design strategies defines the market's trajectory.

What will be the Size of the MEP Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the MEP Services Market Segmented?

The mep services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

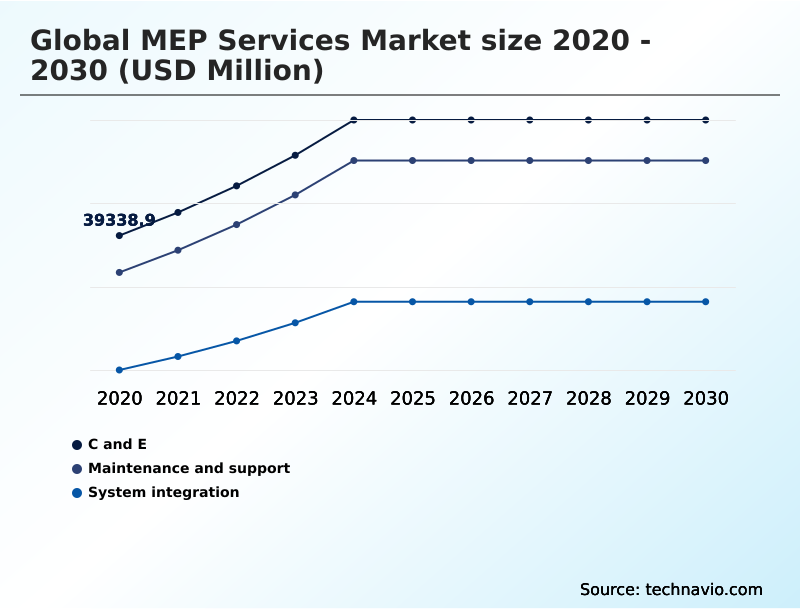

- Service

- C and E

- Maintenance and support

- System integration

- End-user

- Commercial

- Government

- Residential

- Application

- New construction

- Renovation and retrofit

- Maintenance and operations

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Service Insights

The c and e segment is estimated to witness significant growth during the forecast period.

The market is segmented by service, with consulting and engineering providing the intellectual framework for complex projects. This segment focuses on initial design, feasibility, and pre-construction strategies for heating ventilation and air conditioning, electrical power distribution, and plumbing network design.

Demand for sustainable building consulting and energy efficiency analysis is surging for projects targeting net-zero carbon footprints, especially in high-density data centers. Advanced mep system integration and mep commissioning services are critical.

Firms utilizing digital-first workflows for building thermal management and advanced fire suppression planning report that early-stage modeling improves design accuracy by over 15%.

This approach integrates environmental health sciences considerations and ensures robust construction quality assurance from the outset, moving beyond basic smart building automation.

The C and E segment was valued at USD 56.59 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 45.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How MEP Services Market Demand is Rising in North America Get Free Sample

North America leads the market, contributing over 45% of incremental growth, driven by extensive infrastructure upgrades and adherence to strict energy efficiency mandates.

The region’s focus on integrated project delivery models and the use of building information modeling are key differentiators.

The APAC region shows the fastest expansion, fueled by significant government-led infrastructure program management and investments in high-tech manufacturing that require specialized cleanroom facility engineering.

Europe's market is defined by its commitment to sustainability, with clean energy consulting and digital twin integration being pivotal. The adoption of advanced project management consultancy for civil engineering services is roughly 30% higher in Western markets.

These firms utilize computational fluid dynamics modeling for electrical load calculation and power redundancy planning for critical facilities, integrating geospatial solutions for mep with architectural design support.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the global MEP services market 2026-2030 is marked by increasing specialization, driven by complex client demands across various sectors. For instance, mep services for hyperscale data center construction now require advanced liquid cooling solutions for ai data racks to manage extreme thermal loads.

- The use of bim integration for mep clash detection has become standard practice, improving coordination on intricate projects. This digital approach extends to digital twin technology for mep lifecycle optimization, providing long-term operational value. In the healthcare sector, modular mep prefabrication for healthcare facilities accelerates construction timelines while ensuring quality.

- Simultaneously, the push for green buildings drives demand for sustainable mep design for net-zero buildings, including the electrification of hvac systems in building retrofits. This complexity requires a new project delivery approach, with integrated project delivery for complex mep projects gaining favor.

- Such models are crucial for large-scale initiatives like mep retrofitting for aging government buildings and developing mep services for smart city infrastructure. From a technical standpoint, power distribution design for mission-critical facilities and robust fire suppression system design for industrial facilities are non-negotiable.

- Moreover, mep compliance with ashrae 90.1 standards and effective plumbing design for water-saving initiatives are key regulatory and sustainability considerations. Firms are also leveraging predictive maintenance for mep using iot sensors and automated building controls for energy reduction.

- In fact, companies that fully integrate these digital tools report a project completion rate that is notably faster than those using traditional methods. However, the industry continues to grapple with addressing skilled labor shortages in mep trades and managing the impact of volatile material costs on mep bids.

- Finally, the growing semiconductor industry also fuels demand for specialized mep engineering for semiconductor fabrication plants.

What are the key market drivers leading to the rise in the adoption of MEP Services Industry?

- The exponential growth in data center construction, fueled by digitalization and AI, serves as a primary driver for the market.

- A key driver is the global investment in grid modernization services and water infrastructure projects, which necessitates advanced water management solutions.

- The explosion in data center construction also fuels demand, as these facilities require flawless building operations support and facility maintenance services. Governments are funding urban infrastructure planning, including smart-traffic electrical grids, creating opportunities for firms offering turnkey contracting solutions.

- There is also rising demand for comprehensive security risk management and fire protection engineering. The use of predictive maintenance software is growing, with adopters reporting a 30% reduction in unplanned downtime.

- This is supported by building performance simulation and code compliance consulting to meet evolving regulations. These complex projects require integrated structural engineering support and a thorough environmental impact assessment.

What are the market trends shaping the MEP Services Industry?

- The adoption of prefabrication and modular MEP assembly is a significant market trend. This approach is driven by the demand for accelerated project timelines and improved quality control.

- A primary market trend is the shift toward prefabrication and modular mep, which shortens project timelines by up to 25%. This manufacturing-led approach enhances quality for high-performance building systems. Another key trend is the focus on full asset lifecycle management, driven by decarbonization services and renewable energy integration.

- Automated control systems are central to this, enabling dynamic mechanical system design and electrical system management. Advanced energy recovery ventilation systems are now standard in new constructions, improving air quality while reducing energy use by 18%.

- This trend benefits providers of ongoing technical facility services and specialized industrial maintenance solutions, as well as those managing long-term hvac maintenance contracts and utility services engineering for high-tech facility solutions and commercial property management.

What challenges does the MEP Services Industry face during its growth?

- A critical shortage of skilled labor presents a key challenge, impacting project timelines and constraining industry growth potential.

- A significant challenge is the complexity of retrofitting legacy buildings to meet modern energy performance standards. Integrating internet of things sensors and automated plumbing diagnostics into aging infrastructure often leads to unforeseen issues, with such projects experiencing schedule overruns 15% more frequently than new builds.

- The severe shortage of skilled technicians trained in power systems engineering and digital engineering services exacerbates this problem. Volatile material costs also disrupt engineering procurement and construction budgets. Furthermore, ensuring flawless plumbing network design and system integration during building commissioning and retro-commissioning is difficult.

- Firms must rely on clash detection software to mitigate risks, while also navigating complex life safety code consulting and delivering robust industrial system solutions. This requires a greater emphasis on energy audit services and long-term operation and maintenance contracts.

Exclusive Technavio Analysis on Customer Landscape

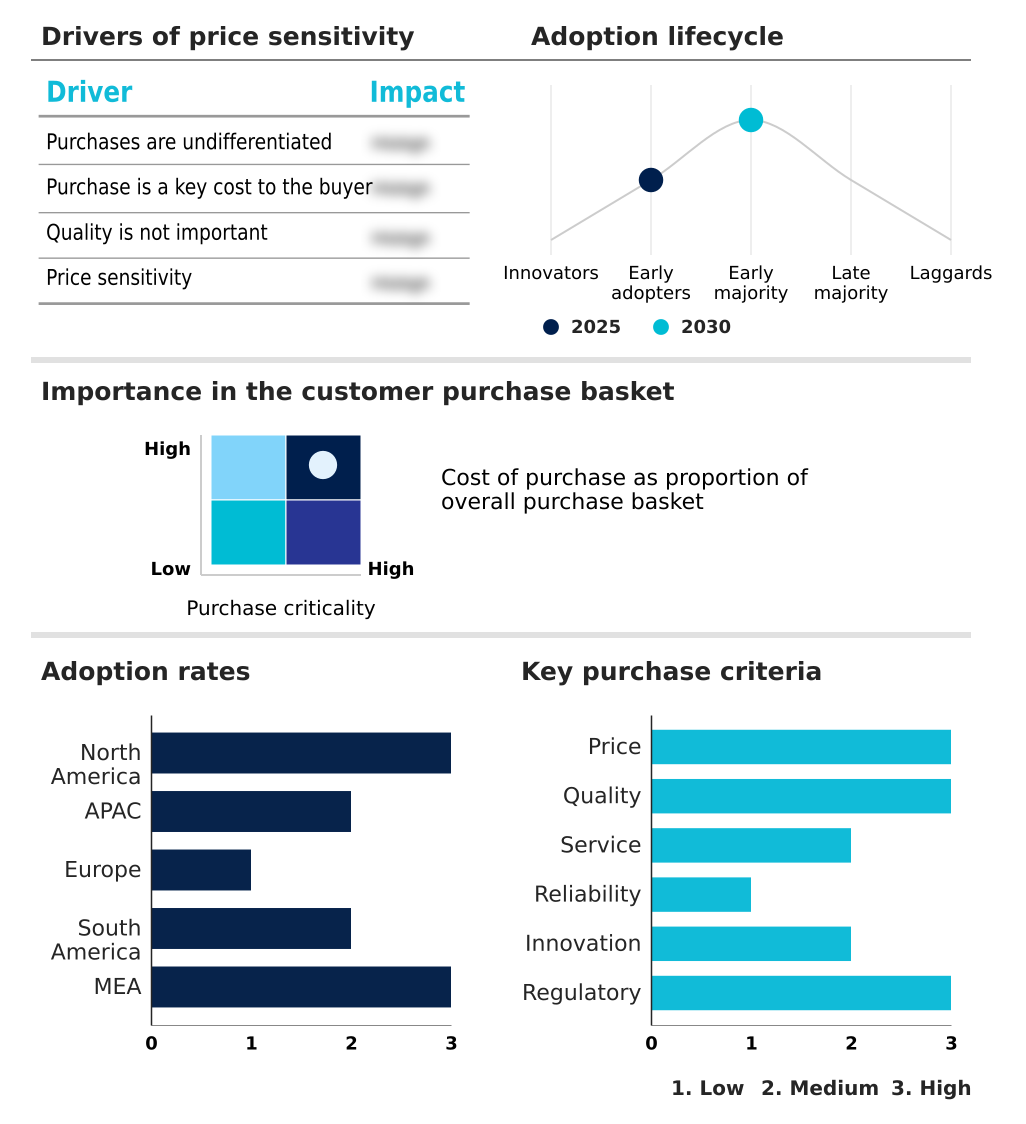

The mep services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the mep services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of MEP Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, mep services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AECOM - Delivers integrated design, engineering, and project management, specializing in complex, large-scale infrastructure and building initiatives on a global scale.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AECOM

- Burns and McDonnell

- Continuum Services

- Crockett Facilities Services

- Dohn Engineering PLC

- EMCOR Group Inc.

- Exyte GmbH

- Global Facility Solutions LLC

- IMEG Corp.

- Jacobs Solutions Inc.

- Jensen Hughes

- Knight Facilities Management

- MEP Engineering Inc.

- Mott MacDonald

- NV5 Global Inc.

- Resolute Engineering

- Sterling and Wilson Energy

- WSP Global Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Mep services market

- In September, 2024, Vantage Data Centers announced it had secured $1.6 billion in funding to accelerate the expansion of its high-density data center portfolio across the APAC region.

- In November, 2024, CDC Data Centers received regulatory approval for a major $3.1 billion campus development in Australia, designed to support mission-critical government and enterprise clients.

- In February, 2025, Google confirmed a $5.5 billion investment plan for developing new computing infrastructure and renewable energy projects in Germany, driving demand for advanced MEP services.

- In April, 2025, WSP Global Inc. announced a definitive agreement to acquire TRC Companies for approximately $3.3 billion, a strategic move to bolster its capabilities in grid modernization and water infrastructure services in North America.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled MEP Services Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 283 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12.7% |

| Market growth 2026-2030 | USD 124477.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 11.6% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Indonesia, Australia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The MEP services market is defined by a critical pivot towards high-performance building systems and integrated digital engineering services. Core activities now revolve around heating ventilation and air conditioning optimization, electrical power distribution resilience, and innovative water management solutions.

- The adoption of building information modeling and digital twin integration is no longer optional but a strategic imperative for managing complex projects like high-density data centers and cleanroom facility engineering.

- Boardroom decisions increasingly focus on investing in predictive maintenance software and automated control systems, as firms using these tools have demonstrated up to a 20% improvement in asset lifecycle management efficiency. This shift is essential for delivering on decarbonization services and achieving net-zero carbon footprints.

- The technical scope has expanded to include power systems engineering, computational fluid dynamics modeling, and precise electrical load calculation, supported by clash detection software. Key trends include prefabrication and modular mep, which enhances quality control, and retrofitting legacy buildings to meet new energy performance standards.

- From advanced fire suppression and building thermal management to power redundancy planning, every aspect of a project requires specialized expertise. This includes sustainable design strategies, energy recovery ventilation, and comprehensive facility maintenance services.

- Firms that master integrated project delivery models and offer end-to-end turnkey contracting solutions for grid modernization services and water infrastructure projects are best positioned for success in this evolving landscape, which also covers smart-traffic electrical grids, automated plumbing diagnostics, and the use of internet of things sensors.

What are the Key Data Covered in this MEP Services Market Research and Growth Report?

-

What is the expected growth of the MEP Services Market between 2026 and 2030?

-

USD 124.48 billion, at a CAGR of 12.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Service (C and E, Maintenance and support, and System integration), End-user (Commercial, Government, and Residential), Application (New construction, Renovation and retrofit, and Maintenance and operations) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Data center construction explosion, Critical shortage of skilled labor

-

-

Who are the major players in the MEP Services Market?

-

AECOM, Burns and McDonnell, Continuum Services, Crockett Facilities Services, Dohn Engineering PLC, EMCOR Group Inc., Exyte GmbH, Global Facility Solutions LLC, IMEG Corp., Jacobs Solutions Inc., Jensen Hughes, Knight Facilities Management, MEP Engineering Inc., Mott MacDonald, NV5 Global Inc., Resolute Engineering, Sterling and Wilson Energy and WSP Global Inc.

-

Market Research Insights

- The market's dynamism is driven by a shift toward specialized consulting and full lifecycle services. Firms offering sustainable building consulting and energy efficiency analysis are gaining traction as clients prioritize operational performance. The adoption of advanced project management consultancy has been shown to reduce project overruns by up to 20% compared to traditional methods.

- Furthermore, building commissioning and retro-commissioning services now achieve an average 15% reduction in energy consumption in older commercial properties. This value proposition, supported by comprehensive engineering procurement and construction and long-term operation and maintenance contracts, is becoming crucial.

- As a result, providers of technical facility services and infrastructure program management that demonstrate verifiable ROI are outperforming competitors by a significant margin.

We can help! Our analysts can customize this mep services market research report to meet your requirements.

RIA -

RIA -