Engineering Services Market Size 2026-2030

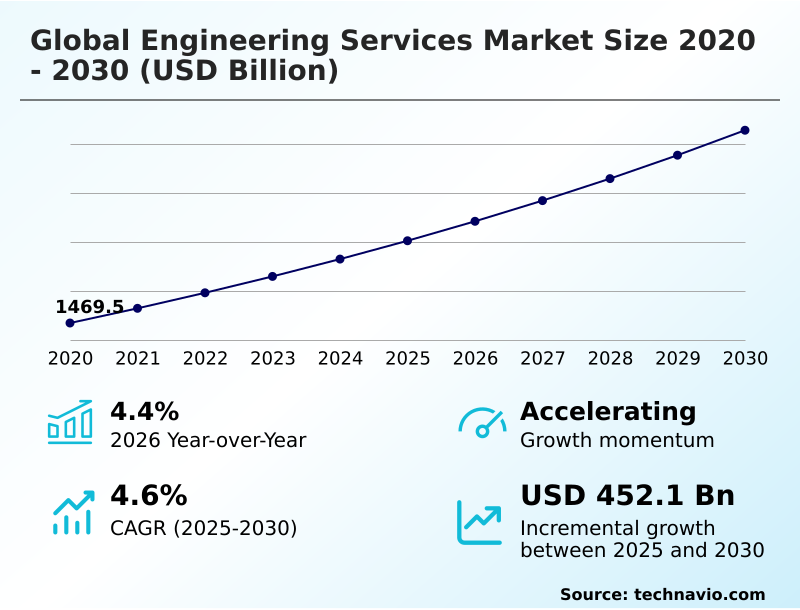

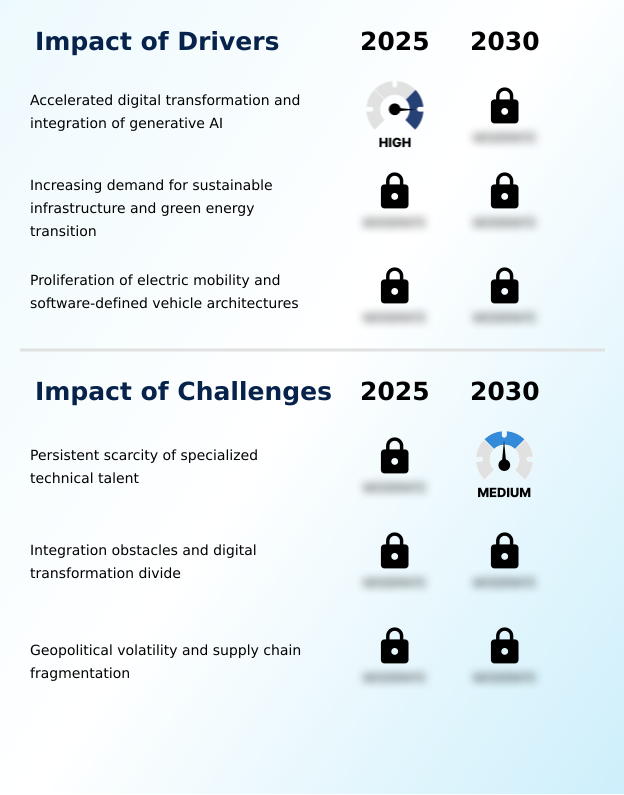

The engineering services market size is valued to increase by USD 452.1 billion, at a CAGR of 4.6% from 2025 to 2030. Accelerated digital transformation and integration of generative AI will drive the engineering services market.

Major Market Trends & Insights

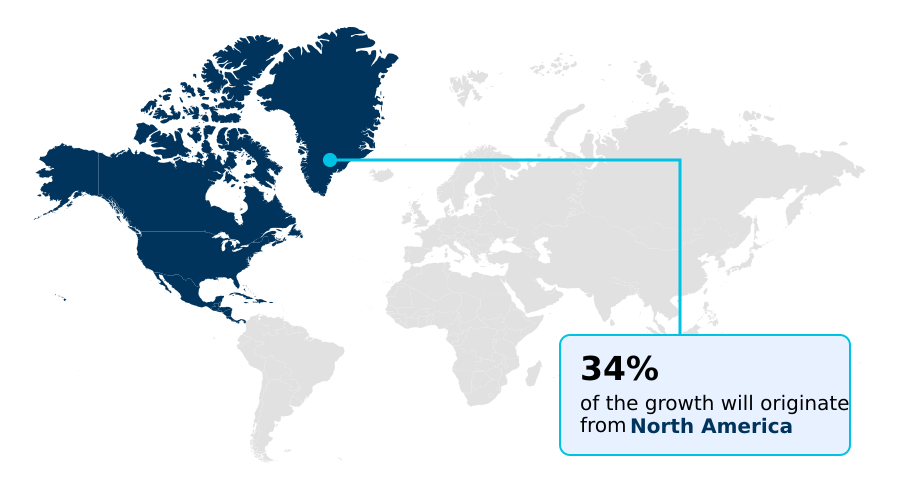

- North America dominated the market and accounted for a 33.8% growth during the forecast period.

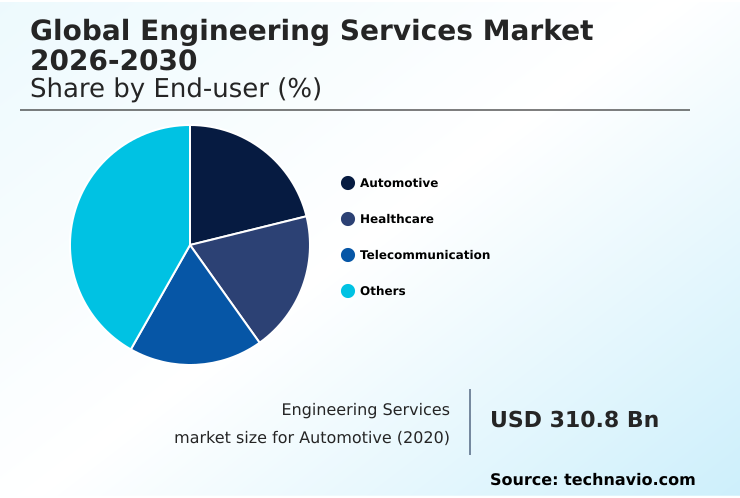

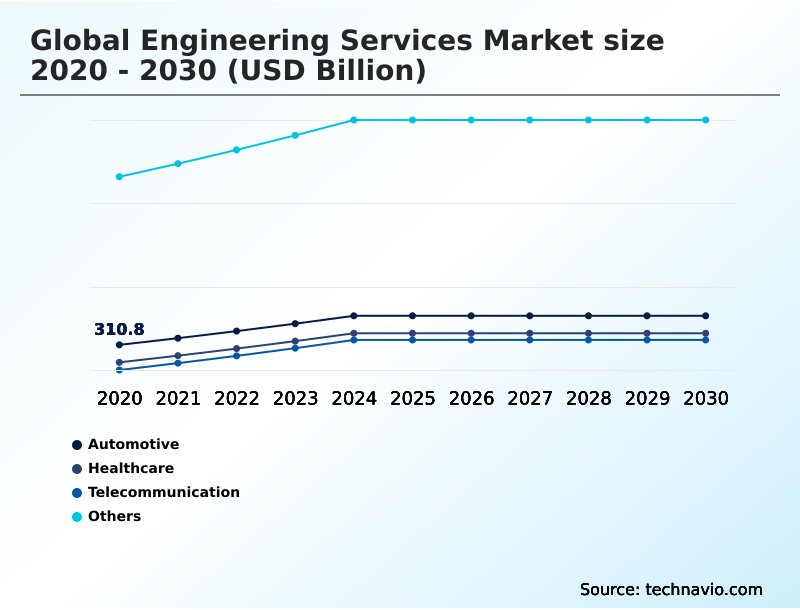

- By End-user - Automotive segment was valued at USD 363.2 billion in 2024

- By Deployment - Outsourcing segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 788.6 billion

- Market Future Opportunities: USD 452.1 billion

- CAGR from 2025 to 2030 : 4.6%

Market Summary

- The engineering services market is undergoing a fundamental transformation, driven by the integration of digital technologies and a global focus on sustainability. This evolution moves beyond traditional methodologies toward data-centric approaches that utilize digital twins, generative AI, and high-performance computing to optimize the entire product lifecycle.

- A key business scenario involves using real-time simulation tools to model a new manufacturing line, allowing engineers to identify and resolve potential bottlenecks before construction begins, which has been shown to reduce physical prototyping costs by over 40%. The demand for green design services and adherence to sustainable infrastructure standards are creating new opportunities, particularly in energy and transportation.

- However, the industry faces significant challenges from the persistent scarcity of specialized technical talent needed for complex tasks like system integration engineering and cyber-physical security protocols, which can delay project timelines and increase operational risk for firms unable to scale their workforces.

What will be the Size of the Engineering Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Engineering Services Market Segmented?

The engineering services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Automotive

- Healthcare

- Telecommunication

- Others

- Deployment

- Outsourcing

- Onsite

- Service type

- Product engineering

- Process engineering

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By End-user Insights

The automotive segment is estimated to witness significant growth during the forecast period.

The automotive segment is undergoing a profound transformation as the industry pivots toward the software-defined vehicle and electrification.

This shift is driven by the integration of advanced driver-assistance systems and complex powertrains, necessitating specialized expertise in embedded systems design, power electronics design, and thermal management solutions.

OEMs are increasingly outsourcing these requirements to manage product lifecycle management and accelerate development, moving toward outcome-based service models. Demand for advanced structural modeling analysis and additive manufacturing design is also surging to support lightweighting initiatives.

This transition to digital-first development has enabled cycle-time reductions of up to 50% in certain validation processes, underscoring the critical role of specialized engineering partnerships in this evolving landscape.

The Automotive segment was valued at USD 363.2 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Engineering Services Market Demand is Rising in North America Get Free Sample

The market landscape is shaped by distinct regional priorities. North America leads in high-value sectors, focusing on electronic design automation and aerospace.

Europe champions smart factory integration and circular manufacturing principles, with firms leveraging augmented engineering solutions to maintain a competitive edge. The adoption of the industrial internet of things (IIoT) is widespread, improving efficiency by over 20% in some manufacturing plants.

APAC is a critical hub for both manufacturing and outsourced services, particularly for network functions virtualization and smart city infrastructure. Talent shortages remain a global issue, with critical engineering roles often staying vacant for more than 60 days.

This drives interest in advanced technologies like computational fluid dynamics and federated learning implementation to optimize limited resources across regions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the market is profoundly shaped by the convergence of digital and physical domains, particularly with engineering services for electric mobility and the increasing use of generative ai in product engineering. This trend is exemplified by the software-defined vehicle architecture design, which relies heavily on ai-powered software engineering solutions and platform engineering for software development.

- To manage the complexity of modern assets, the use of a digital twin for infrastructure management is becoming standard, supported by high-performance computing for simulation. Concurrently, ensuring cybersecurity for cyber-physical systems and building digital resilience for critical infrastructure are top priorities.

- Sustainability is another core driver, fueling demand for sustainable engineering design services and the application of the circular economy in engineering design, leading to broader engineering solutions for decarbonization. Operationally, robotic process automation manufacturing and process optimization in manufacturing engineering are enhancing efficiency.

- Firms that effectively implement predictive maintenance engineering services have reported up to a 40% reduction in unplanned equipment downtime compared to those with reactive strategies. Success in this environment requires strong interdisciplinary engineering team collaboration, the adoption of model-based systems engineering adoption, and leveraging agentic ai for design automation, while strategically managing supply chain fragmentation through outsourcing engineering r&d services.

What are the key market drivers leading to the rise in the adoption of Engineering Services Industry?

- The market's growth is primarily driven by accelerated digital transformation and the widespread integration of generative AI.

- Accelerated adoption of digital engineering platforms and the integration of generative AI are key market drivers. These technologies enable the use of digital twins and real-time simulation tools, which can reduce development cycles by up to 50%.

- A worldwide commitment to sustainability is also propelling growth, increasing demand for green design services that incorporate life-cycle assessment methodology and carbon capture technology.

- This focus on decarbonization mandates adherence to new sustainable infrastructure standards, creating a surge in demand for specialized expertise.

- The complexity of these projects is also boosting the use of high-performance computing for advanced analysis, with investments in green R&D in some sectors doubling over previous years.

What are the market trends shaping the Engineering Services Industry?

- The market is experiencing a significant trend toward the proliferation of interdisciplinary collaboration. This shift is driven by the increasing integration of complex software systems across engineering domains.

- A primary trend is the expansion of autonomous mobility systems and the robotic process integration into industrial environments, where agentic artificial intelligence is automating complex tasks. This requires advanced system integration engineering to connect disparate cyber-physical systems. Concurrently, the prioritization of digital security is driving the adoption of digital resilience architecture and zero-trust security frameworks to protect critical infrastructure.

- In some markets, project abandonment rates surged over 80% due to supply chain volatility, fueling the adoption of building information modeling for better planning. Model-based systems engineering is becoming standard practice, with adoption rates among manufacturers for physical AI expected to increase by 22% as firms seek to enhance operational agility.

What challenges does the Engineering Services Industry face during its growth?

- A persistent scarcity of specialized technical talent presents a key challenge to the industry's growth.

- Geopolitical instability is forcing a shift from global supply chains to resilient near-shoring supply models, challenging traditional predictive program management. This volatility has caused material cost fluctuations leading to project abandonment rates increasing by as much as 88% in certain markets. Concurrently, the transition to digital-first engineering requires significant investment in technologies like computer-aided engineering and finite element analysis.

- Firms are also pressed to adopt agile procurement processes and secure platform engineering workflows with robust cyber-physical security protocols to manage intellectual property. While over 75% of firms plan to increase hiring for roles related to network functions virtualization and software-defined networking, a persistent talent deficit remains a significant operational bottleneck.

Exclusive Technavio Analysis on Customer Landscape

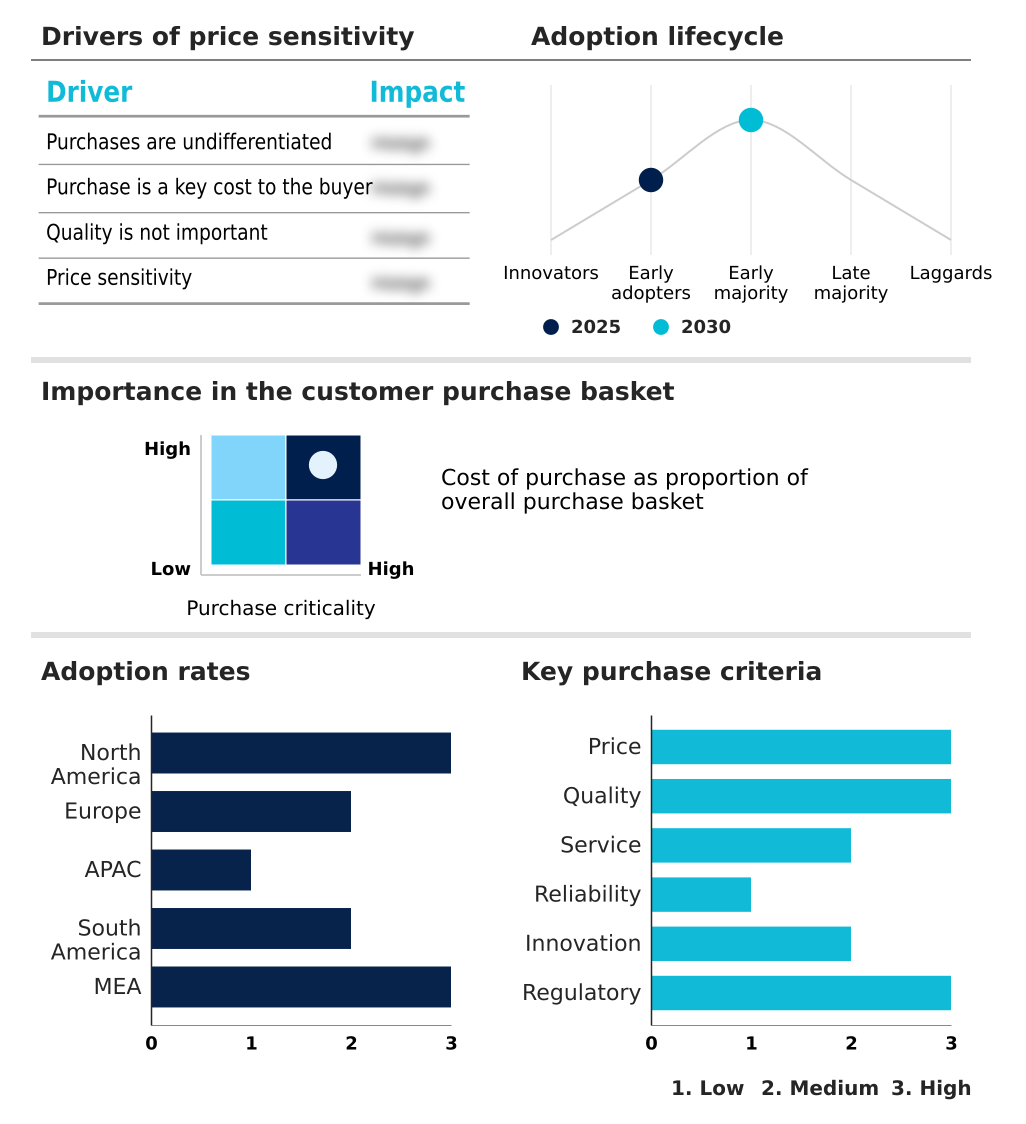

The engineering services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the engineering services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Engineering Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, engineering services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AECOM - Delivers engineering solutions for complex infrastructure, energy, and environmental projects, specializing in critical assets like bridges, tunnels, and clean energy facilities.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AECOM

- AKKA Technologies SE

- Babcock International Group Plc

- Balfour Beatty Plc

- Bechtel Corp.

- Brasfield and Gorrie LLC

- Capgemini Service SAS

- CIMIC Group

- Cyient Ltd.

- Design Systems Inc.

- EMCOR Group Inc.

- Fluor Corp.

- Infosys Ltd.

- Jacobs Solutions Inc.

- Kiewit Corp.

- KKR BOSE DESIGN SERVICES Ltd.

- NV5 Global Inc.

- Tata Consultancy Services

- TRIPLAN India Pvt. Ltd.

- Virtuoso Projects and Engineers

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Engineering services market

- In May 2025, an Aecon-Kiewit-led consortium secured a contract worth approximately $934 million for the engineering and construction of the Darlington Small Modular Reactor in Ontario, signaling a major investment in advanced nuclear technology.

- In April 2025, Balfour Beatty plc secured an eight hundred and thirty-three million pound contract for civil and electrical engineering works for the Net Zero Teesside Power project, reinforcing the shift toward low-carbon energy infrastructure.

- In October 2024, Capgemini Service SAS launched a new portfolio of augmented engineering solutions that leverage generative AI to accelerate R&D cycles for manufacturing clients.

- In September 2024, InfoBeans Technologies launched its Insane SDD Accelerator, an AI-powered software engineering solution designed to reduce production defects and improve delivery cycles by up to 50%.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Engineering Services Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.6% |

| Market growth 2026-2030 | USD 452.1 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.4% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Egypt and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The engineering services market is advancing through the integration of sophisticated digital tools that redefine product and infrastructure lifecycles. The use of generative AI and agentic artificial intelligence is automating complex design tasks, while digital twins provide a virtual environment for testing and validation.

- This digital shift is critical in sectors developing the software-defined vehicle, where model-based systems engineering and advanced driver-assistance systems are standard. Core technologies like computer-aided engineering, finite element analysis, and computational fluid dynamics are powered by high-performance computing, enabling more complex structural modeling analysis.

- In electronics, electronic design automation is key, while smart factory integration and system integration engineering are transforming manufacturing. A strategic focus on sustainability is driving the adoption of circular manufacturing principles, carbon capture technology, and green design services, with life-cycle assessment methodology demonstrating an ability to reduce environmental impact by over 25% in certain projects.

- This requires specialized knowledge in power electronics design and thermal management solutions. Overall, success is increasingly dependent on predictive program management and delivering augmented engineering solutions that address these interconnected demands.

What are the Key Data Covered in this Engineering Services Market Research and Growth Report?

-

What is the expected growth of the Engineering Services Market between 2026 and 2030?

-

USD 452.1 billion, at a CAGR of 4.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Automotive, Healthcare, Telecommunication, and Others), Deployment (Outsourcing, and Onsite), Service Type (Product engineering, Process engineering, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Accelerated digital transformation and integration of generative AI, Persistent scarcity of specialized technical talent

-

-

Who are the major players in the Engineering Services Market?

-

AECOM, AKKA Technologies SE, Babcock International Group Plc, Balfour Beatty Plc, Bechtel Corp., Brasfield and Gorrie LLC, Capgemini Service SAS, CIMIC Group, Cyient Ltd., Design Systems Inc., EMCOR Group Inc., Fluor Corp., Infosys Ltd., Jacobs Solutions Inc., Kiewit Corp., KKR BOSE DESIGN SERVICES Ltd., NV5 Global Inc., Tata Consultancy Services, TRIPLAN India Pvt. Ltd. and Virtuoso Projects and Engineers

-

Market Research Insights

- The market is characterized by rapid shifts as firms adopt digital engineering platforms and outcome-based service models to enhance competitiveness. This transition allows for greater agility, with the adoption of agile procurement processes improving project startup times by up to 25%.

- A focus on product lifecycle management from concept to decommissioning is becoming standard, supported by real-time simulation tools that reduce physical prototyping needs by over 40%. The strategic move toward near-shoring supply models aims to mitigate geopolitical risks, while the demand for embedded systems design surges with the proliferation of smart, connected products.

- These dynamics create a landscape where specialization and technological proficiency are paramount for success.

We can help! Our analysts can customize this engineering services market research report to meet your requirements.

RIA -

RIA -