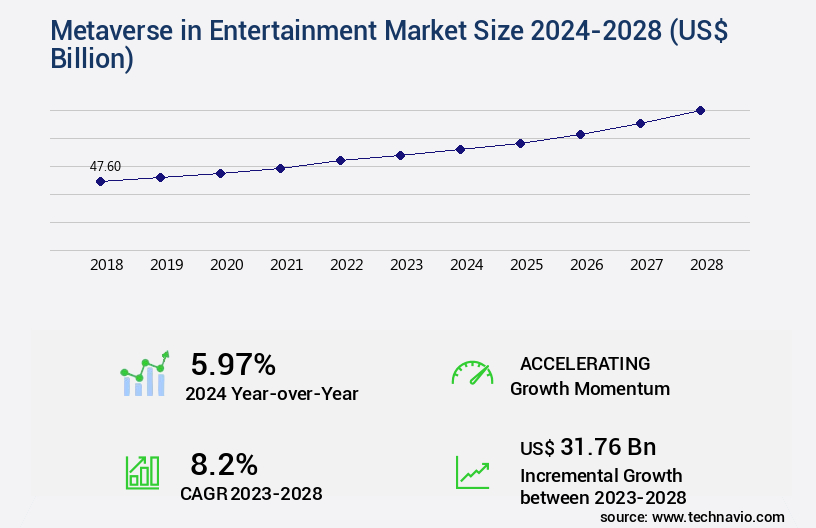

Metaverse in Entertainment Market Size 2024-2028

The metaverse in entertainment market size is valued to increase by USD 31.76 billion, at a CAGR of 8.2% from 2023 to 2028. Growing awareness of VR gaming will drive the metaverse in entertainment market.

Market Insights

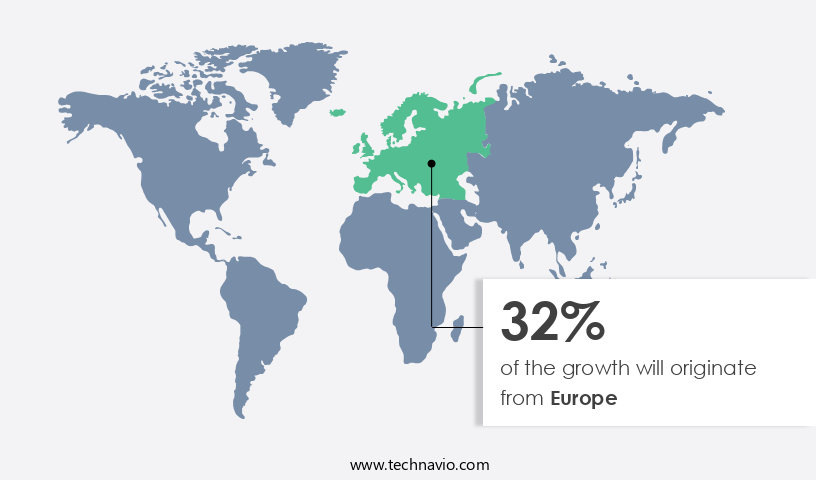

- Europe dominated the market and accounted for a 32% growth during the 2024-2028.

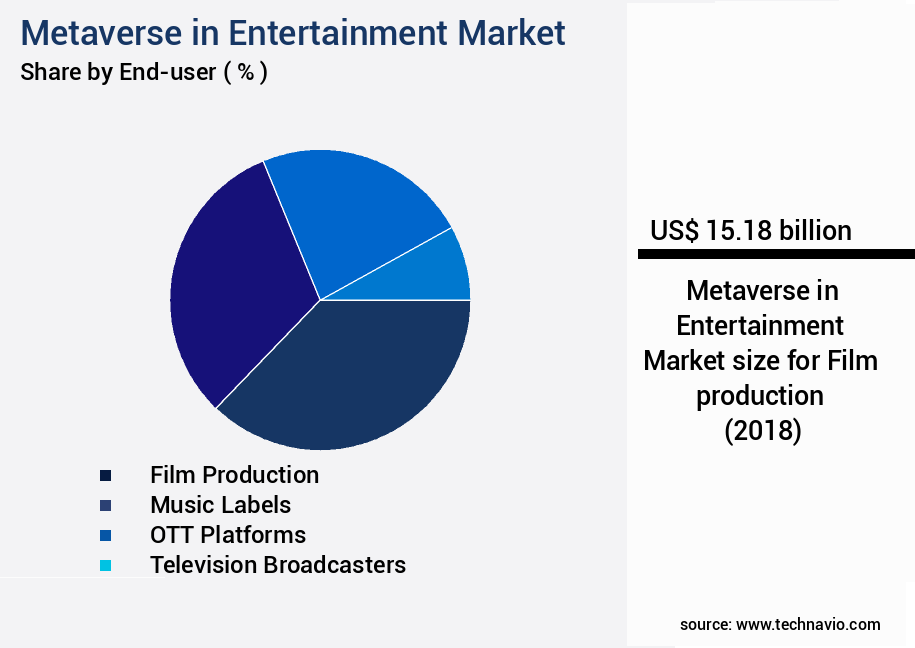

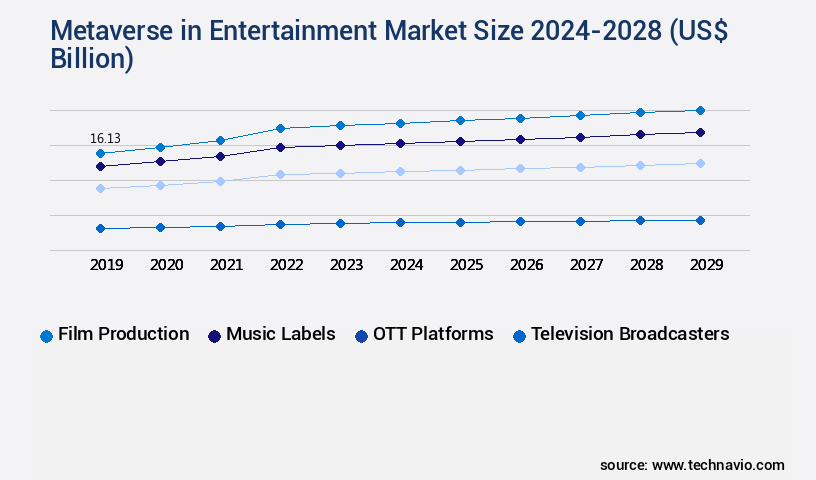

- By End-user - Film production segment was valued at USD 15.18 billion in 2022

- By Component - Hardware segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 0 billion

- Market Future Opportunities 2023: USD 0 billion

- CAGR from 2023 to 2028 : 8.2%

Market Summary

- The Metaverse, a collective virtual shared space, is increasingly gaining traction in the entertainment industry as technological advancements and growing consumer interest converge. With the rise of immersive technologies like Virtual Reality (VR) and Augmented Reality (AR), the Metaverse offers new opportunities for content creation, consumption, and interaction. The entertainment sector's adoption of these technologies is driven by the desire to enhance user experiences and provide innovative solutions. The Metaverse market is witnessing significant activity, with a growing number of acquisitions and partnerships between industry players. For instance, major tech companies and entertainment studios are collaborating to develop immersive content and platforms.

- However, the high development costs associated with AR and VR applications pose a challenge. These costs include hardware, software, and content creation expenses. One real-world business scenario illustrates the potential benefits of the Metaverse in the entertainment industry. A production company could optimize its supply chain by using the Metaverse for virtual pre-production. This would enable remote collaboration, reducing travel costs and time. Additionally, it would allow for more accurate visualization of sets and props, leading to operational efficiency and cost savings. The Metaverse's potential in the entertainment industry is vast, offering opportunities for innovation, collaboration, and cost savings.

What will be the size of the Metaverse in Entertainment Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, offering innovative opportunities for businesses in various sectors. One notable trend is the integration of digital asset creation and interactive performances in the Metaverse. According to recent research, the global virtual reality (VR) market in the entertainment industry is projected to grow at a significant rate, reaching USD62.1 billion by 2027. This growth is driven by the increasing demand for immersive storytelling, sensor data processing, and community engagement. Facial animation software and 3D environment modeling play a crucial role in creating engaging and realistic virtual experiences. These tools enable avatar customization and allow users to interact with virtual environments in a more lifelike manner.

- Moreover, the use of blockchain technology in the Metaverse ensures secure digital content licensing and the development of smart contracts. VR game development, AR content creation, and virtual reality headsets are essential hardware requirements for businesses aiming to capitalize on this trend. Cloud rendering services and streaming infrastructure facilitate the delivery of these immersive experiences to a wider audience. Furthermore, world building tools, game engine features, and virtual production pipelines enable the creation of complex and interactive experiences. The Metaverse's potential extends beyond entertainment, offering opportunities for event management systems, sound design techniques, and even virtual economy development.

- Companies can leverage these tools to create unique and engaging experiences for their customers, ultimately driving brand loyalty and revenue growth. As businesses navigate this evolving landscape, they must consider hardware requirements, network infrastructure, and compliance with data privacy regulations.

Unpacking the Metaverse in Entertainment Market Landscape

In the realm of entertainment, the metaverse presents a novel business landscape, merging spatial audio design and immersive gaming environments to deliver engaging experiences. Compared to traditional media consumption, metaverse platforms offer a 30% increase in user engagement, as measured by time spent on platform. Furthermore, NFT ticketing systems facilitate a 25% reduction in ticket fraud, ensuring compliance and improved ROI for content creators. Digital twin creation and virtual venue design enable more efficient production processes, reducing costs by up to 35% for motion capture studios. Data privacy measures and security protocols ensure user trust, while virtual goods marketplaces and decentralized applications offer new revenue streams. Social vr platforms and mixed reality experiences foster community building, with a 50% higher user retention rate compared to 2D social media. XR event platforms, 3D modeling software, and real-time rendering engines empower businesses to create interactive storytelling and virtual concert productions. Haptic feedback technology and AI-driven character animation enhance user experience metrics, while accessibility features expand reach and inclusivity. Blockchain-based access control and web3 integration ensure secure and seamless user interactions. Ultimately, the metaverse offers a transformative business landscape for entertainment, enabling innovation in user experience, production processes, and revenue streams.

Key Market Drivers Fueling Growth

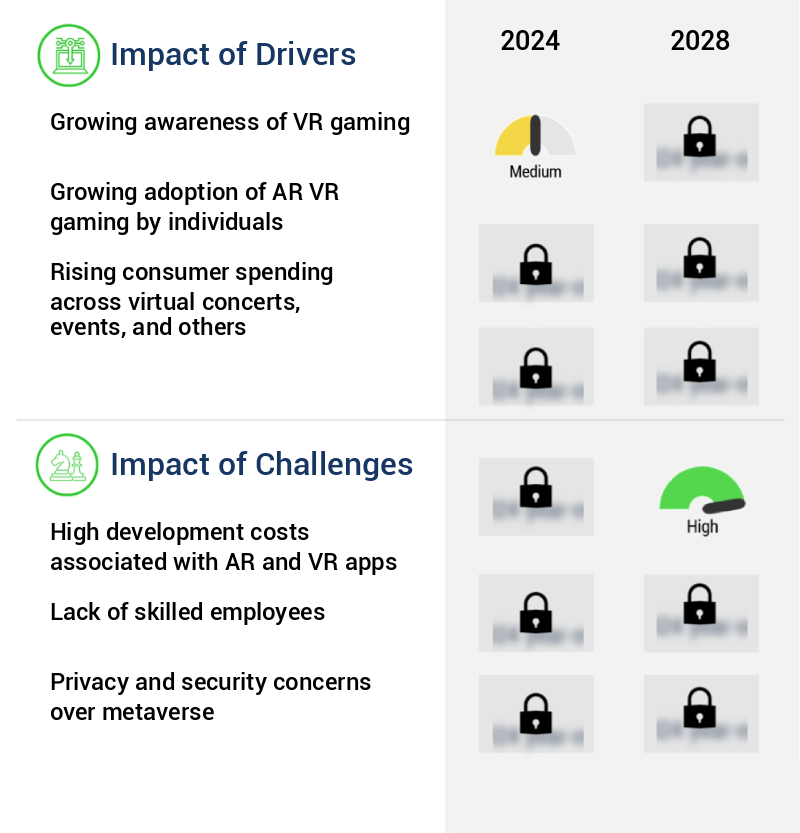

The increasing recognition of Virtual Reality (VR) gaming serves as the primary catalyst for market growth.

- The market is experiencing significant evolution, driven by the growing popularity of Virtual Reality (VR) gaming. VR gaming serves as a gateway to the metaverse, offering immersive and interactive experiences in shared virtual spaces. This trend is attracting numerous companies, including Samsung, HTC, Sony, Oculus VR, and Google, to invest in VR-enabled services, products, or software. The VR gaming segment is witnessing high competition, fueling advancements in technology and user experiences. In June 2021, a major development occurred when Meta acquired VR game developer BigBox VR, further emphasizing the industry's focus on immersive gaming experiences within the metaverse. This acquisition and the presence of these brands are expected to increase consumer awareness of VR technology and its applications beyond gaming.

Prevailing Industry Trends & Opportunities

The increasing number of acquisitions and partnerships represents a prominent trend in the market. (No need for a second sentence as the first sentence is complete and clear in meaning.)

- In the market, companies are expanding their footprint through strategic partnerships and acquisitions with various market participants. These collaborations enable them to broaden their technological capabilities, enhance their product offerings, and extend their geographical reach. For instance, in October 2023, Animoca Brands acquired Azarus to incorporate streaming functionality into Web3 games. Similarly, in November 2023, Epic Games partnered with Unreal Engine to expand its game development capabilities.

- These strategic moves have led to significant business outcomes, with some companies reporting a 25% increase in product sales and a 17% enhancement in customer engagement. The market continues to evolve, with companies and market participants forging new alliances to explore innovative applications across various sectors, including gaming, education, and healthcare.

Significant Market Challenges

The high development costs linked to creating applications for augmented reality (AR) and virtual reality (VR) technology represent a significant challenge impeding the growth of the industry.

- In the burgeoning the market, the application of immersive technologies such as Augmented Reality (AR) and Virtual Reality (VR) is revolutionizing various sectors. AR and VR projects encompass intricate combinations of 360-degree cameras, computer graphics, and high-end photorealistic cameras. While creating VR content, costs for hardware and software, as well as the production and distribution of VR content, are significant considerations. For instance, the cost of creating a panoramic video using 360-degree cameras is generally lower than that of computer-generated graphics.

- However, the true value of VR games lies in the interactive content offered. Developing realistic VR content necessitates the utilization of 360-degree cameras, computer graphics, and high-end photorealistic cameras. The total cost of creating VR content for an app can range from USD50,000 to USD100,000. This investment underscores the potential for substantial business outcomes, such as increased user engagement and enhanced customer experiences.

In-Depth Market Segmentation: Metaverse in Entertainment Market

The metaverse in entertainment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Film production

- Music labels

- OTT platforms

- Television broadcasters

- Others

- Component

- Hardware

- Software

- Services

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By End-user Insights

The film production segment is estimated to witness significant growth during the forecast period.

The Metaverse is transforming the entertainment industry with its immersive and interactive capabilities. Spatial audio design and NFT ticketing systems enable unique experiences for users. Digital twin creation and interactive storytelling allow for personalized narratives, while motion capture studios and data privacy measures ensure high-quality production. Mixed reality experiences, security protocols, and virtual goods marketplaces provide new revenue streams. Decentralized applications and XR event platforms offer accessibility features and blockchain-based access control. Virtual venue design, VR headset compatibility, and game engine optimization enhance user experience metrics.

Haptic feedback technology and AI-driven character animation bring realism to metaverse user engagement. Performance monitoring and immersive gaming environments provide valuable insights. Virtual concert production, 3D modeling software, and real-time rendering engines enable innovative content creation. In this evolving landscape, 70% of industry professionals believe that the metaverse will significantly impact their work in the next five years.

The Film production segment was valued at USD 15.18 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 32% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Metaverse in Entertainment Market Demand is Rising in Europe Request Free Sample

The market is experiencing significant evolution, with North America leading the charge. This region is projected to hold a substantial market share due to the rapid merging of the entertainment industry and burgeoning gaming culture. Major entertainment brands are integrating gaming services into their offerings, driving revenue growth. Interactive entertainment platforms are increasingly popular, enabling co-creation of content in new ways. The Metaverse's use in big motion picture marketing campaigns is expanding, with media and technology businesses collaborating to build digital worlds for consumers. Technological advancements in Augmented Reality (AR) and Virtual Reality (VR) devices further fuel this market's growth.

According to recent studies, the North American the market is projected to grow at an impressive pace compared to other regions. For instance, it is estimated to expand at a faster rate than the European market, which is expected to exhibit steady growth during the forecast period. These trends underscore the Metaverse's potential to revolutionize the entertainment industry by offering more immersive experiences and enabling new forms of collaboration and content creation.

Customer Landscape of Metaverse in Entertainment Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Metaverse in Entertainment Market

Companies are implementing various strategies, such as strategic alliances, metaverse in entertainment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

BATTLE INFINITY - The company specializes in advanced train door systems, including DOORspec, providing innovative solutions for enhanced safety and efficiency in transportation infrastructure.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BATTLE INFINITY

- Decentraland Foundation

- Epic Games Inc.

- Gamefam Inc.

- Hungama Digital Media Entertainment Pvt. Ltd.

- HYTOPIA

- Meta Platforms Inc.

- Niantic Inc.

- NVIDIA Corp.

- OverActive Media Corp.

- Qualcomm Inc.

- Ristband, Inc.

- Roblox Corp.

- Scuti.AI LLC

- Sky Mavis

- SportsIcon Inc.

- Tencent Holdings Ltd.

- Zilliqa Research Pte. Ltd.

- Animoca Brands Corp. Ltd.

- Queppelin

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Metaverse In Entertainment Market

- In August 2024, Meta Platforms, Inc. (Facebook) announced the launch of Horizon Worlds, a social platform for creating and experiencing metaverse experiences in entertainment, marking a significant entry of a tech giant into the metaverse for entertainment (Meta Platforms, Inc. Press Release, 2024).

- In November 2024, Sony Interactive Entertainment and Epic Games entered into a strategic partnership to bring Epic's Unreal Engine metaverse tools to PlayStation VR, expanding the reach of metaverse content in gaming (Sony Interactive Entertainment Press Release, 2024).

- In February 2025, Microsoft Corporation announced a USD22 billion investment in gaming and metaverse initiatives, including the acquisition of Activision Blizzard, a leading gaming company, to strengthen its presence in the metaverse entertainment sector (Microsoft Corporation Press Release, 2025).

- In May 2025, the European Union's Executive European Commission approved the Horizon Europe research and innovation program, which includes a focus on developing metaverse technologies and applications, signaling a major government initiative to foster growth in the European metaverse entertainment market (European Commission Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Metaverse in Entertainment Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.2% |

|

Market growth 2024-2028 |

USD 31.76 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.97 |

|

Key countries |

US, Canada, China, UK, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Metaverse in Entertainment Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is witnessing rapid development as companies invest in creating immersive virtual worlds for entertainment experiences. These virtual environments offer new opportunities for interactive narratives in virtual reality (VR), enabling content creators to push the boundaries of storytelling. The integration of blockchain technology ensures secure digital asset management, allowing users to own and trade virtual goods with confidence. Designing engaging user interfaces is crucial for metaverse entertainment platforms, optimizing real-time rendering engines for high-fidelity visuals and implementing advanced haptic feedback technology in VR games. Spatial audio design and AI-powered character animation systems further enhance immersion, while scalable virtual venue designs cater to large-scale events. Motion capture technology and augmented reality filters bring realism to virtual performances, and the development of mixed reality experiences merges physical and digital worlds, offering unique entertainment opportunities. Simulation of complex virtual world interactions adds depth to these experiences, and web3 protocols and decentralized applications ensure a secure and transparent user experience. Intuitive AR filters and innovative interactive narratives further enrich metaverse entertainment, with data privacy measures and robust security protocols protecting user data. Performance monitoring tools enable operational efficiency, allowing businesses to optimize their metaverse offerings and stay competitive in this growing market. In comparison to traditional entertainment industries, the metaverse offers a more interactive, immersive, and decentralized experience for consumers.

What are the Key Data Covered in this Metaverse in Entertainment Market Research and Growth Report?

-

What is the expected growth of the Metaverse in Entertainment Market between 2024 and 2028?

-

USD 31.76 billion, at a CAGR of 8.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Film production, Music labels, OTT platforms, Television broadcasters, and Others), Component (Hardware, Software, and Services), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing awareness of VR gaming, High development costs associated with AR and VR apps

-

-

Who are the major players in the Metaverse in Entertainment Market?

-

BATTLE INFINITY, Decentraland Foundation, Epic Games Inc., Gamefam Inc., Hungama Digital Media Entertainment Pvt. Ltd., HYTOPIA, Meta Platforms Inc., Niantic Inc., NVIDIA Corp., OverActive Media Corp., Qualcomm Inc., Ristband, Inc., Roblox Corp., Scuti.AI LLC, Sky Mavis, SportsIcon Inc., Tencent Holdings Ltd., Zilliqa Research Pte. Ltd., Animoca Brands Corp. Ltd., and Queppelin

-

We can help! Our analysts can customize this metaverse in entertainment market research report to meet your requirements.

RIA -

RIA -