Micro LED Display Market Size 2026-2030

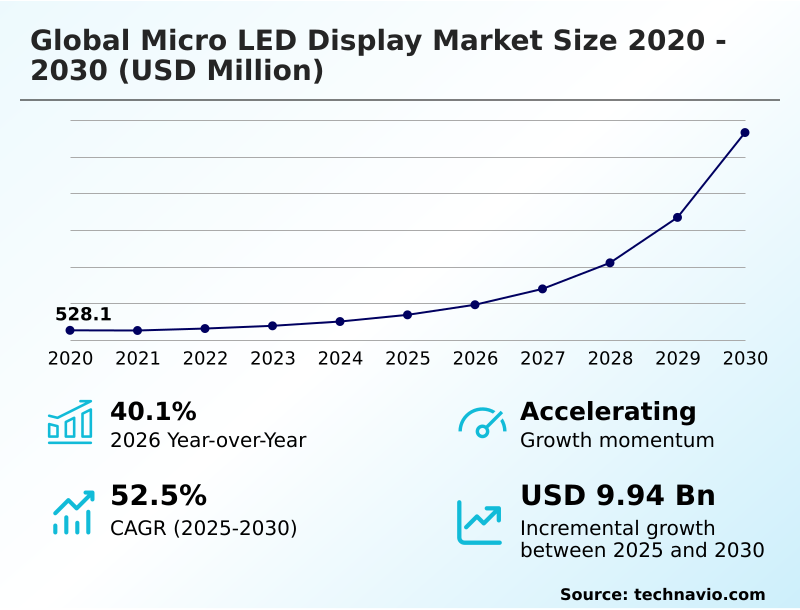

The micro led display market size is valued to increase by USD 9.94 billion, at a CAGR of 52.5% from 2025 to 2030. High-luminance and energy-efficient interfaces in AR and wearable sectors will drive the micro led display market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 41.3% growth during the forecast period.

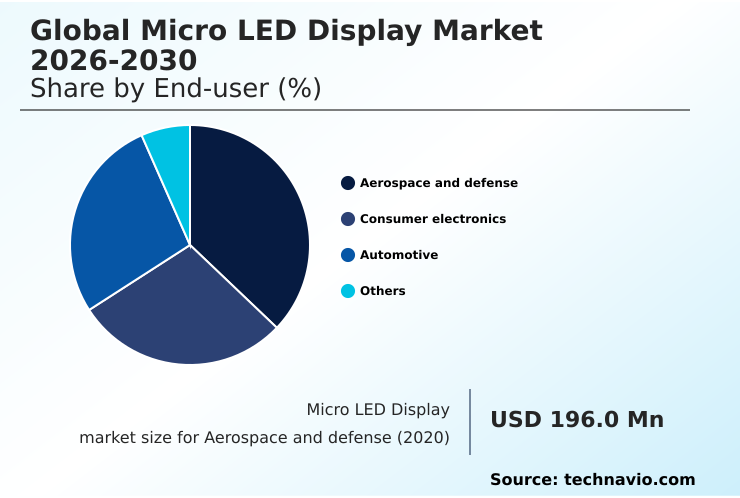

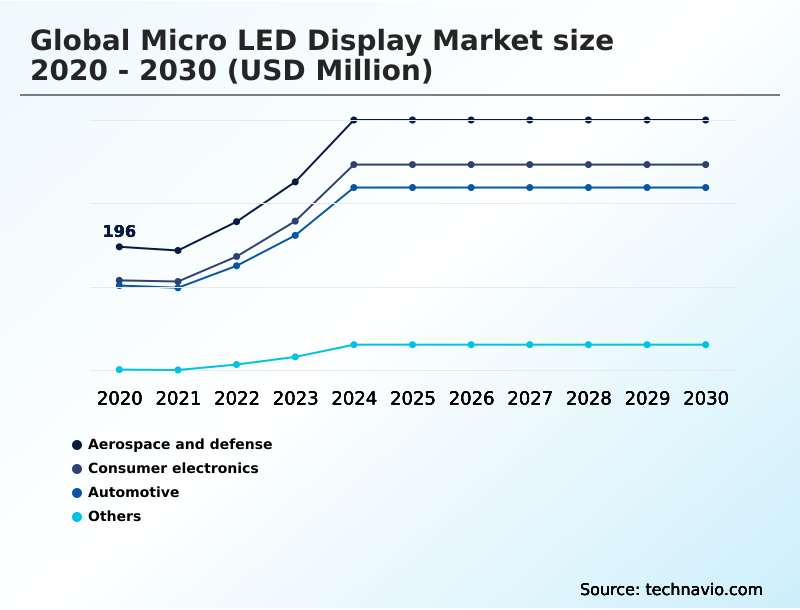

- By End-user - Aerospace and defense segment was valued at USD 362.4 million in 2024

- By Technology - Transfer micro LED segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 10.79 billion

- Market Future Opportunities: USD 9.94 billion

- CAGR from 2025 to 2030 : 52.5%

Market Summary

- The micro LED display market is defined by its potential to supersede existing technologies through superior brightness, efficiency, and longevity. Based on self-emissive pixels made from inorganic gallium nitride, these displays eliminate the need for backlights, enabling thinner form factors and deeper black levels.

- Growth is primarily driven by demand from premium applications where performance is non-negotiable, such as next-generation wearables, automotive head-up displays, and large-format video walls. A key industry trend revolves around perfecting mass transfer technology to move millions of microscopic light emitting diodes accurately and cost-effectively.

- For instance, an automotive manufacturer developing a premium electric vehicle line must weigh the benefits of exceptional visual performance and durability for its dashboard displays against the current high costs and manufacturing complexities. The central challenge remains scaling production to reduce costs and achieve yields that make the technology viable for mainstream consumer electronics.

- Success hinges on innovations that can transition micro LED from a niche, high-end solution to a widely adopted standard, impacting everything from consumer devices to industrial control panels.

What will be the Size of the Micro LED Display Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Micro LED Display Market Segmented?

The micro led display industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Aerospace and defense

- Consumer electronics

- Automotive

- Others

- Technology

- Transfer micro LED

- Monolithic micro LED

- Hybrid micro LED

- Application

- Digital signage

- Wearable devices

- Virtual reality

- Geography

- APAC

- China

- South Korea

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- UAE

- Saudi Arabia

- Israel

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By End-user Insights

The aerospace and defense segment is estimated to witness significant growth during the forecast period.

The aerospace and defense segment mandates display solutions that offer uncompromising reliability and performance. Micro LED technology is uniquely suited for these applications, providing ruggedized display solutions essential for modern avionics display systems and near-eye applications.

The use of inorganic semiconductor materials ensures operational longevity and resilience in extreme environments.

Advanced manufacturing, including microsolid printing process and precise flip-chip bonding, enables the high pixel pitch density required for high-resolution projection in cockpits and control room video walls.

These direct-emissive display systems maintain performance integrity, with some advanced led modules achieving a 99.9% operational uptime in simulated mission-critical scenarios, thanks to features like cobalt-oxide encapsulation that protect microscopic light emitting diodes.

The Aerospace and defense segment was valued at USD 362.4 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 41.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Micro LED Display Market Demand is Rising in APAC Request Free Sample

The geographic landscape of the market is characterized by a strategic division of labor.

APAC, particularly in countries like China, South Korea, and Taiwan, serves as the global manufacturing epicenter, driven by substantial government support and a highly integrated supply chain.

This regional concentration accounts for over 41% of the market's incremental growth, with a focus on scaling production of gan-on-silicon panels and refining backplane technology integration.

North America and Europe function as primary demand centers, leading the adoption of next-generation wearables and advanced automotive systems requiring high-dynamic-range content and transparent display technology.

The consolidation of the supply chain in APAC has been shown to reduce lead times for key components like epitaxial wafers by up to 20%, enhancing production efficiency for global brands leveraging microdisplay light engines for ar waveguide display products.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic evaluations in the display industry consistently analyze micro led vs oled power consumption, where micro led technology demonstrates significant advantages in efficiency, a critical factor for battery-dependent devices. A primary focus for manufacturers is the mass transfer yield rate improvement, which is directly linked to cost reduction in micro led manufacturing.

- Overcoming challenges in the micro led repair process is essential for achieving the necessary production volumes. Applications are rapidly expanding, with significant development in micro led for automotive hud systems, where brightness and reliability are paramount. The use of gan-on-silicon for ar glasses is enabling higher pixel density requirements for vr headsets and other near-eye devices.

- Technologically, quantum dot color conversion for micro led is being used to achieve full color realization in micro led, enhancing the visual experience. Key R&D efforts are targeting thermal management for micro led displays and improving external quantum efficiency in micro leds to boost performance and lifespan.

- While direct-view displays are the most common application, developments in micro led backlighting for lcd panels offer an intermediate upgrade path. The industry is also innovating with driver ic design for micro led displays and monolithic integration for microdisplays, which simplifies manufacturing. As a result, micro led applications in aerospace defense are growing, where performance outweighs cost.

- Success depends on perfecting technologies like hybrid bonding for fine pitch micro led and laser lift-off for micro led transfer, alongside robust yield management strategies for micro led and thorough reliability testing of micro led panels. The potential for flexible and stretchable micro led displays represents a significant future growth vector.

What are the key market drivers leading to the rise in the adoption of Micro LED Display Industry?

- Demand for high-luminance, energy-efficient interfaces within the augmented reality and wearable device sectors is a key driver of market expansion.

- Demand for superior visual performance in next-generation devices is a primary market driver. The inherent advantages of inorganic gallium nitride, such as high brightness and resistance to electroluminescence degradation, make it ideal for high-luminance displays.

- Self-emissive pixels offer exceptional efficiency, with some common cathode architecture designs reducing power consumption by up to 50% in augmented reality microdisplays and wearable device screens.

- This efficiency is critical for extending battery life in products like a smartwatch display module.

- Furthermore, the automotive sector's requirement for next-generation automotive head-up displays to maintain a minimum luminance of 5,000 nits can only be met by inorganic technologies, which sustain high photoluminescence efficiency over a vehicle's lifespan without burn-in, driving adoption over organic alternatives.

What are the market trends shaping the Micro LED Display Industry?

- Manufacturing scalability and the evolution of mass transfer technology represent critical trends. These advancements are essential for industrializing production and achieving commercial viability.

- The market is undergoing a critical transition toward industrial-scale production, driven by advancements in mass transfer technology. The evolution from mechanical stamping to high-throughput laser systems is enabling a throughput increase of up to 400%, drastically reducing the assembly time for large-format video walls and premium consumer tvs. This shift is pivotal for lowering unit costs.

- Concurrently, the integration of automated optical inspection is becoming standard, with new systems improving first-pass yields by up to 15% by identifying and correcting defective pixels in real time. Achieving a six-sigma yield goal is now a more tangible objective, essential for the viability of fine-pitch led products.

- These trends in micro-transfer printing and uv-led curing are fostering a robust supply chain capable of supporting seamless modular displays for applications ranging from industrial control panels to cinema screen technology.

What challenges does the Micro LED Display Industry face during its growth?

- Technical hurdles in mass transfer processes and the difficulty in achieving high assembly yields pose a key challenge to the industry's growth.

- Significant technical challenges, primarily in manufacturing, constrain market growth. The mass transfer process demands sub-micrometer accuracy to assemble ultra-high-definition panels, a task complicated by van der waals forces at the microscopic level. Current defect rates in epitaxial wafer production and assembly can be over 50% higher than mass-market tolerance, making the cost of the pixel repair process prohibitive.

- As pixel sizes shrink for applications like a vr headset panel, the complexity of handling components increases exponentially, with some processes being 10 times more intricate than traditional methods. Furthermore, ensuring the integrity of the anisotropic conductive film during bonding for flexible display substrates adds another layer of difficulty.

- These hurdles in achieving high yields and managing costs currently limit widespread adoption in price-sensitive sectors.

Exclusive Technavio Analysis on Customer Landscape

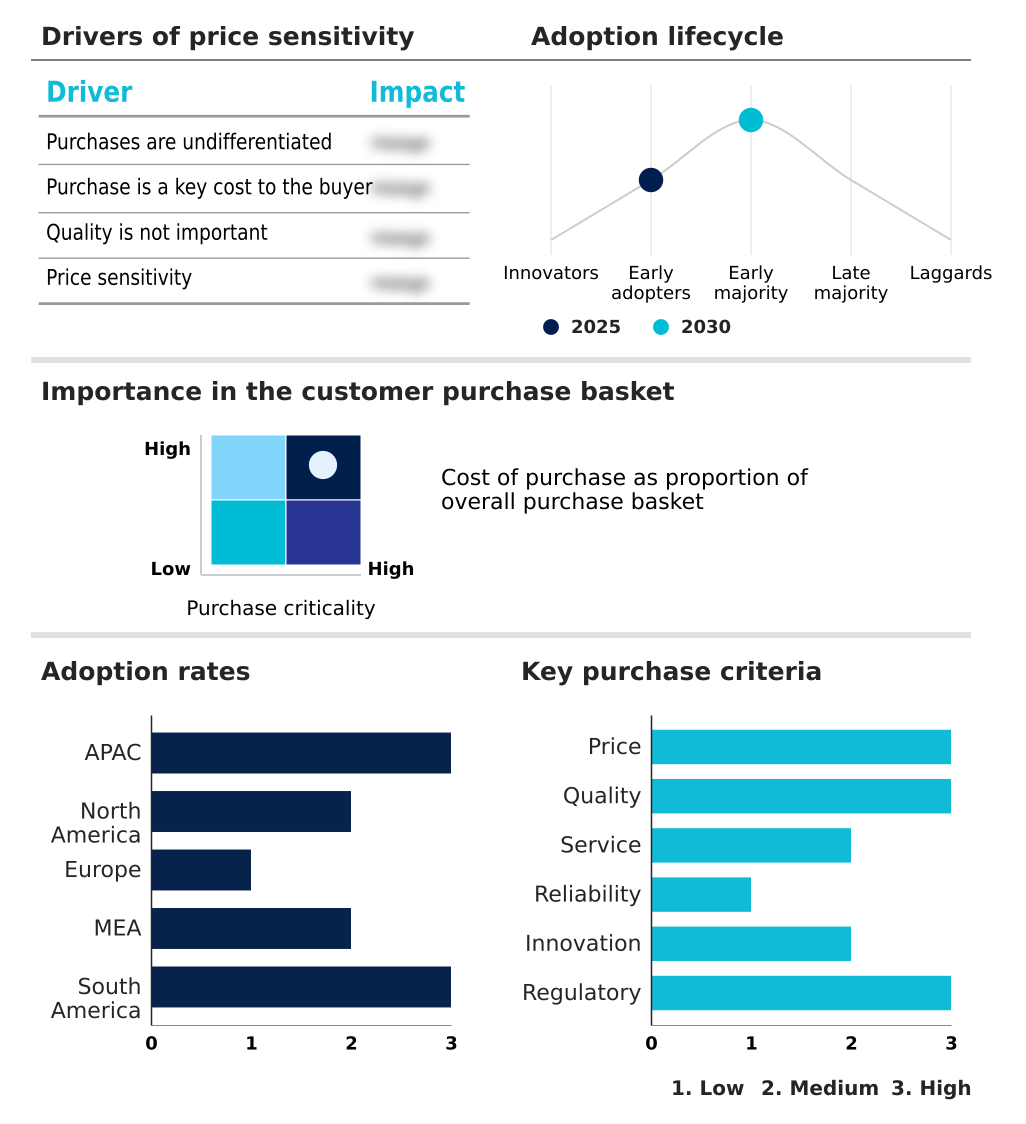

The micro led display market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the micro led display market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Micro LED Display Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, micro led display market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aledia SA - Specializes in developing advanced micro-LED display technology, leveraging a unique 3D nanowire-on-silicon architecture for next-generation visual applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aledia SA

- Apple Inc.

- AUO Corp.

- Innolux Corp.

- Japan Display Inc.

- JBD Inc.

- LG Electronics Inc.

- Lumens Co. Ltd.

- Nanosys Inc.

- Optovate Ltd.

- Panasonic Holdings Corp.

- PlayNitride Inc.

- Plessey Semiconductors Ltd.

- Samsung Electronics Co. Ltd.

- Seiko Epson Corp.

- VueReal Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Micro led display market

- In August 2025, Coherent Corporation released a high-throughput laser system designed for the mass transfer of micro LEDs, enhancing production speeds for large-area television manufacturing.

- In May 2025, AUO Corporation demonstrated a high-resolution micro LED panel for automotive applications, utilizing a novel laser-based transfer method to improve yield consistency.

- In March 2025, AUO Corp. and PlayNitride Inc. formalized a strategic agreement to improve mass transfer process yields for high-resolution automotive displays.

- In February 2025, a major industrial zone in Chengdu announced the completion of a dedicated facility for the mass transfer of micro LED chips, aiming to increase domestic output of high-resolution panels.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Micro LED Display Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 288 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 52.5% |

| Market growth 2026-2030 | USD 9943.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 40.1% |

| Key countries | China, South Korea, Japan, Taiwan, India, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, UAE, Saudi Arabia, Israel, Turkey, South Africa, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The micro led display market is advancing through intense R&D focused on overcoming fundamental manufacturing hurdles. Boardroom decisions increasingly center on the strategic allocation of capital toward proprietary mass transfer technology and epitaxial wafer production to gain a competitive edge. The transition from laboratory to high-volume production hinges on perfecting the placement of microscopic light emitting diodes with sub-micrometer accuracy.

- Innovations in inorganic semiconductor materials like inorganic gallium nitride are enabling superior self-emissive pixels that resist electroluminescence degradation. Developing a scalable pixel repair process is as critical as the initial assembly, with a direct impact on achieving a six-sigma yield goal. Key technologies such as laser-induced forward transfer, advanced led modules, and quantum dot enhancement are central to this evolution.

- A pivotal business metric is the reduction of defects; automated optical inspection systems are already improving first-pass yields by over 15%, directly lowering production costs and accelerating market viability for everything from gan-on-silicon panels to large-format displays.

What are the Key Data Covered in this Micro LED Display Market Research and Growth Report?

-

What is the expected growth of the Micro LED Display Market between 2026 and 2030?

-

USD 9.94 billion, at a CAGR of 52.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Aerospace and defense, Consumer electronics, Automotive, and Others), Technology (Transfer micro LED, Monolithic micro LED, and Hybrid micro LED), Application (Digital signage, Wearable devices, and Virtual reality) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

High-luminance and energy-efficient interfaces in AR and wearable sectors, Technical hurdles in mass transfer and assembly yields

-

-

Who are the major players in the Micro LED Display Market?

-

Aledia SA, Apple Inc., AUO Corp., Innolux Corp., Japan Display Inc., JBD Inc., LG Electronics Inc., Lumens Co. Ltd., Nanosys Inc., Optovate Ltd., Panasonic Holdings Corp., PlayNitride Inc., Plessey Semiconductors Ltd., Samsung Electronics Co. Ltd., Seiko Epson Corp. and VueReal Inc.

-

Market Research Insights

- The market is shaped by a dynamic interplay between demand for superior visual performance and the complexities of advanced manufacturing. The adoption of high-luminance displays in next-generation wearables is accelerating, with new designs showing a 30% improvement in outdoor readability.

- Simultaneously, the push for energy-efficient interfaces in devices like smartwatches has led to display modules that extend battery life by up to 20% compared to previous generations. However, producing ultra-high-definition panels at scale remains a hurdle.

- While applications in digital signage solutions and premium consumer TVs showcase the technology's potential, achieving cost-parity with established alternatives requires significant breakthroughs in yield management and production throughput. This balance between high-value applications and manufacturing viability defines the current competitive landscape.

We can help! Our analysts can customize this micro led display market research report to meet your requirements.