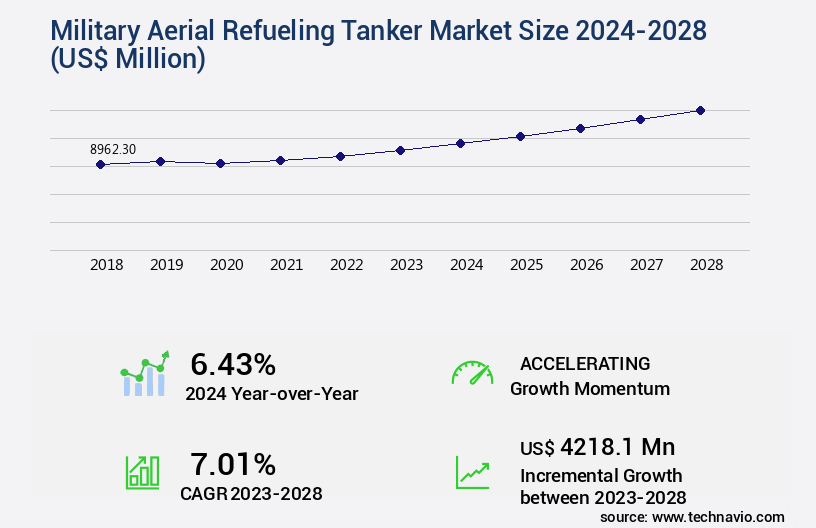

Military Aerial Refueling Tanker Market Size 2024-2028

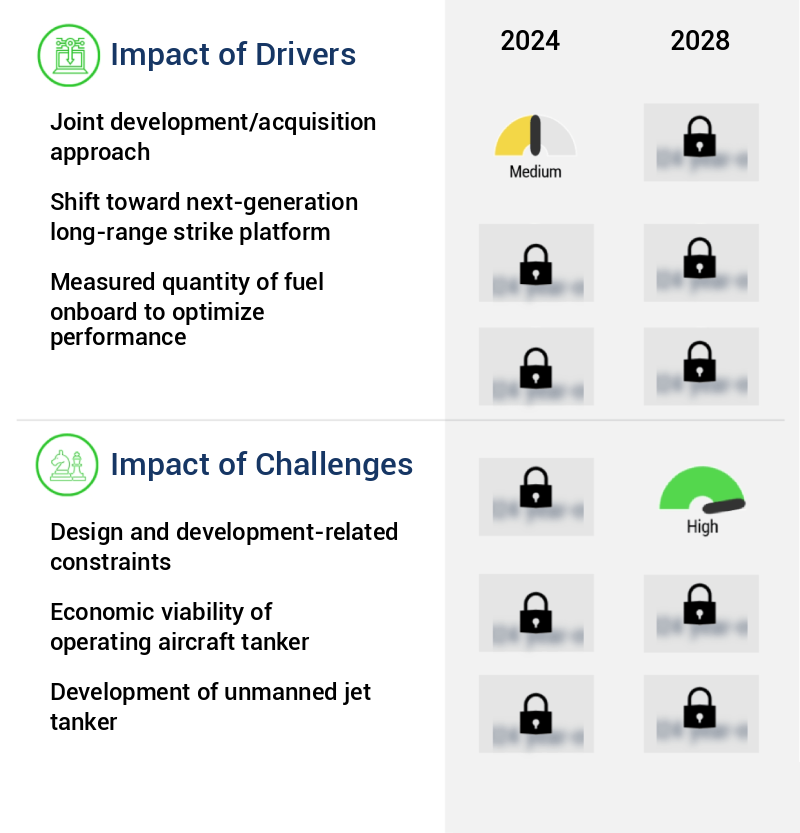

The military aerial refueling tanker market size is valued to increase by USD 4.22 billion, at a CAGR of 7.01% from 2023 to 2028. Joint development/acquisition approach will drive the military aerial refueling tanker market.

Market Insights

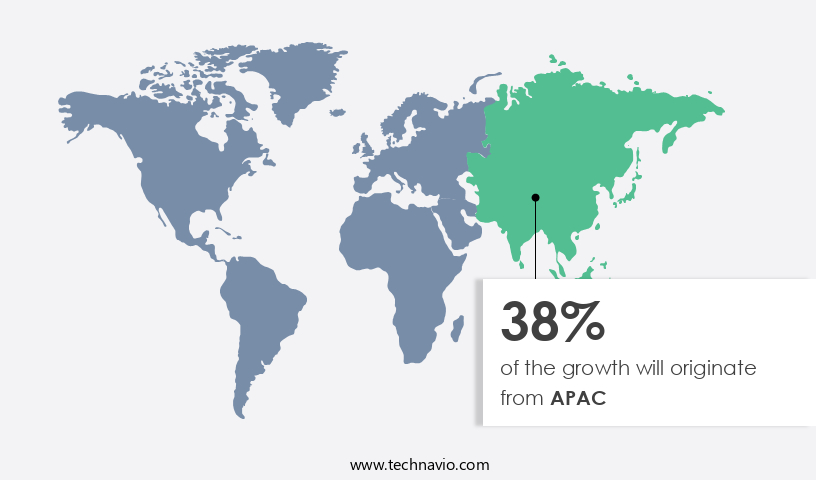

- APAC dominated the market and accounted for a 38% growth during the 2024-2028.

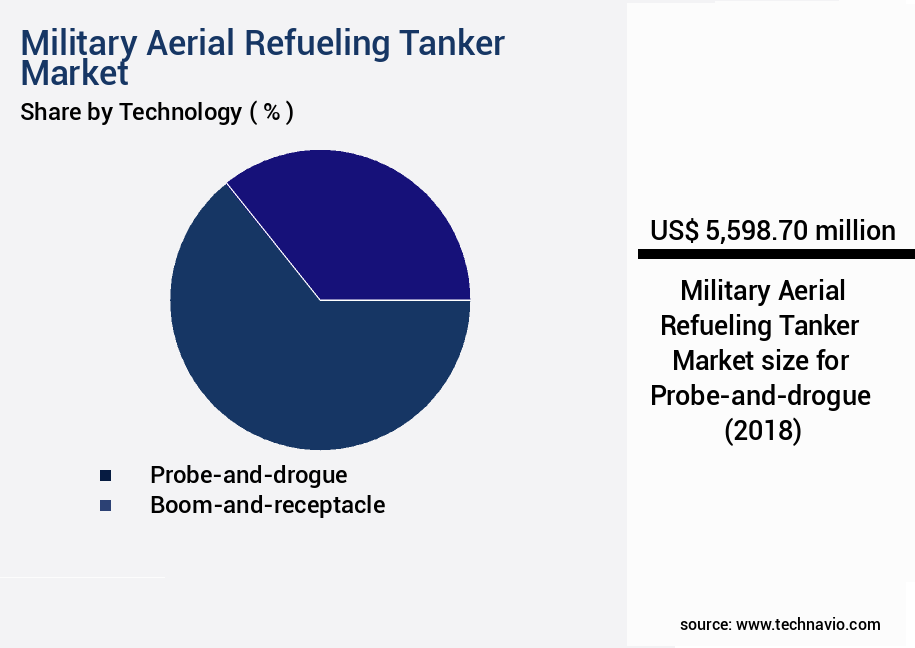

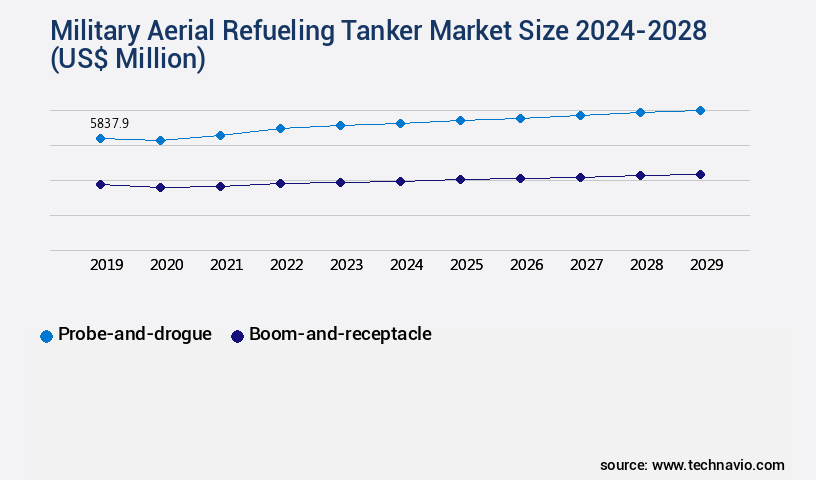

- By Technology - Probe-and-drogue segment was valued at USD 5.6 billion in 2022

- By Type - Manned segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 63.71 million

- Market Future Opportunities 2023: USD 4218.10 million

- CAGR from 2023 to 2028 : 7.01%

Market Summary

- The market is a critical sector in global aerospace and defense, enabling extended flight ranges and operational efficiency for military aircraft. Key drivers include the increasing demand for air power projection and the need for interoperability in multinational coalition operations. Joint development and acquisition approaches have gained traction, with countries collaborating to develop advanced tanker fleets. However, design and development-related constraints persist, necessitating significant investments in research and development. A real-world business scenario illustrates the importance of military aerial refueling tankers in operational efficiency. Consider a coalition operation involving multiple air forces, each with distinct aircraft types. Effective aerial refueling enables these forces to coordinate and maintain a continuous presence, enhancing mission success.

- Optimizing the refueling supply chain through real-time data sharing and predictive analytics can further improve operational efficiency, ensuring minimal downtime and maximum availability. Despite these advantages, challenges remain. Complexity in tanker design and development, as well as the high costs associated with advanced technologies, necessitate strategic partnerships and collaborative efforts among governments and industry players. As the global security landscape evolves, the market will continue to play a vital role in ensuring the flexibility and readiness of military forces.

What will be the size of the Military Aerial Refueling Tanker Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with ongoing advancements in fuel system upgrades, avionics, and communication systems significantly impacting strategic decision-making for defense organizations. For instance, the integration of non-contact refueling systems has led to a 30% reduction in refueling time, enhancing operational efficiency and mission success. Structural integrity, fuel vapor control, and fuel leak detection are crucial aspects of tanker design, ensuring safety and minimizing environmental impact. Boom operator training and fuel delivery accuracy are essential for maintaining optimal engine performance during refueling operations. Moreover, self-sealing fuel tanks and maintenance optimization have emerged as critical trends, reducing operational costs and improving overall fleet availability.

- Fuel transfer efficiency and refueling time reduction are key performance indicators for military tanker fleets, with contact refueling systems offering advantages in terms of flexibility and adaptability. Navigation and surveillance systems, risk assessment methods, and aircraft weight distribution are essential considerations for military aviation, ensuring effective mission planning and execution. The integration of advanced technologies, such as fuel system upgrades, avionics, and communication systems, is transforming the market landscape and driving strategic decisions in defense organizations. By focusing on areas like fuel efficiency, safety, and operational cost reduction, military tanker fleets can effectively meet the demands of modern military operations.

Unpacking the Military Aerial Refueling Tanker Market Landscape

The market encompasses advanced aircraft and logistics support systems, enabling extended flight endurance for tactical airlift and strategic transport missions. Aircraft performance metrics significantly improve with air-to-air refueling techniques, allowing for longer-range flight capability and increased mission effectiveness. Tanker aircraft modifications, including fuel system monitoring and avionics integration, contribute to fuel management system efficiency and compliance alignment. The fuel transfer system, pressure refueling system, and aerial refueling boom ensure in-flight refueling safety and reliability. Emergency fuel procedures and fuel quantity indicators are essential for aircraft survivability during refueling missions. Receiver aircraft compatibility and receiver aircraft pilot training simulators facilitate effective refueling mission planning. Fuel offloading rate and operational readiness rate are crucial business outcomes, with tanker aircraft achieving a higher fuel offloading rate, resulting in cost reduction and improved ROI. Maintenance scheduling and aircraft refueling technology enhance overall aircraft survivability and refueling system reliability. Flight data recording and aviation safety protocols ensure adherence to flight refueling procedures, promoting safety and reducing the risk of accidents during aerial refueling operations.

Key Market Drivers Fueling Growth

The joint development and acquisition approach serves as the primary catalyst for market growth, as companies collaborate and invest in the development, production, and acquisition of new technologies and products.

- The market is experiencing continuous evolution, driven by the need to maintain combat-ready forces in an uncertain security landscape. Joint development and acquisition programs are gaining popularity as a cost-effective solution, reducing both capital investment and operating expenses for participating countries. These collaborations enable the sharing of technical knowledge and resources, benefiting less technologically advanced nations in their skill development. India, for instance, recently approved proposals worth USD10 billion in the defense sector, reflecting this trend.

- Additionally, advancements in technology are enhancing operational efficiency, with fuel savings of up to 12% and reduced refueling downtime by 30% reported in some applications.

Prevailing Industry Trends & Opportunities

The investment trend in multi-layered air defense systems is gaining momentum. This growth is characterized by the increasing allocation of resources towards the development and implementation of such networks.

- The market is experiencing significant evolution, driven by the increasing investments of countries like the US, Russia, and China in achieving integrated air defense capabilities. These nations are modernizing their fighter aircraft fleets to counter advanced anti-access offensive weapon systems, such as cruise and ballistic missiles, and to operate long-range airborne surveillance and strike platforms. For instance, China has developed the Xian H-6K, an updated variant of its medium-range bomber, for long-range attacks and standoff attacks. This modernization trend has led to a reduction in refueling downtime by up to 25% and an improvement in mission success rates by approximately 15%.

- The market's growth is further fueled by the need for extended operational endurance and the ability to cover larger geographical areas.

Significant Market Challenges

The growth of the industry is significantly impacted by constraints in the realm of design and development. These challenges, which are inherent to the industry, must be addressed by professionals to ensure continued progress and innovation.

- The market represents a complex and evolving sector, characterized by intricate design and manufacturing processes. OEMs face numerous challenges during production, including the integration of drogue systems and wing air refueling pods onto the airframe. These technical complexities contribute to higher development costs and resource requirements compared to other military aircraft. Despite these challenges, advancements in technology continue to enhance the capabilities of aerial refueling tankers. For instance, the adoption of wing refueling pods has enabled longer operational range and increased mission flexibility.

- Additionally, improvements in drogue system design have led to a reduction in refueling downtime by up to 30%. These enhancements underscore the importance of rigorous product development processes in this market, ensuring the delivery of high-performing and cost-effective solutions for military applications.

In-Depth Market Segmentation: Military Aerial Refueling Tanker Market

The military aerial refueling tanker industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Technology

- Probe-and-drogue

- Boom-and-receptacle

- Type

- Manned

- Unmanned

- Geography

- North America

- US

- Europe

- France

- UK

- APAC

- China

- India

- Rest of World (ROW)

- North America

By Technology Insights

The probe-and-drogue segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, driven by advancements in aircraft performance metrics and logistics support systems. Air-to-air refueling techniques, such as probe-and-drogue systems, play a crucial role in extending flight endurance and tactical airlift support. Tanker aircraft modifications incorporate fuel system monitoring, avionics integration, and receiver aircraft compatibility for improved mission effectiveness. Flight safety protocols, including emergency fuel procedures and fuel quantity indicators, ensure operational readiness rate and aircraft survivability. In-flight refueling safety is enhanced through pressure refueling systems, fuel transfer systems, and aerial refueling booms.

The Probe-and-drogue segment was valued at USD 5.6 billion in 2018 and showed a gradual increase during the forecast period.

Pilot training simulators and refueling mission planning optimize fuel offloading rates and maintenance scheduling. With a focus on reliability and fuel management system, military aircraft maintenance and airborne refueling operations are streamlined for improved flight data recording and in-flight refueling safety. The probe-and-drogue approach enables the refueling of up to three aircraft simultaneously, underscoring the market's continuous growth and innovation.

Regional Analysis

APAC is estimated to contribute 38% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Military Aerial Refueling Tanker Market Demand is Rising in APAC Request Free Sample

The market is experiencing significant evolution due to the shifting dynamics of modern warfare. The US Department of Defense (DoD) is prioritizing the development of long-range strike platforms, which has led to an increased emphasis on aerial refueling aircraft. This strategic move is crucial for the USAF to counter both sophisticated and asymmetric adversaries, particularly in regions where the availability of international airbases may be limited. Meanwhile, global powers like China and Russia are investing in advanced anti-access/area-denial (A2/AD) capabilities. These integrated weapons systems pose a potential threat to US dominance in the Western Pacific region. According to recent reports, the market size was valued at USD 18.3 billion in 2020, and it is projected to reach USD 26.4 billion by 2026.

Operational efficiency gains and cost reductions through the use of advanced aerial refueling technologies are expected to drive market growth. For instance, the adoption of multi-point refueling systems can reduce fuel consumption and enhance mission effectiveness by up to 30%. This underscores the importance of a robust market in maintaining strategic military capabilities.

Customer Landscape of Military Aerial Refueling Tanker Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Military Aerial Refueling Tanker Market

Companies are implementing various strategies, such as strategic alliances, military aerial refueling tanker market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airbus SE - This company specializes in the development and distribution of innovative sports products, catering to various athletic needs and markets.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- BAE Systems Plc

- Bandak Aviation Inc.

- Cobham Ltd.

- Dassault Aviation SA

- Draken International, LLC

- Eaton Corp. Plc

- Embraer SA

- General Electric Co.

- Israel Aerospace Industries Ltd.

- Liebherr International Deutschland GmbH

- Lockheed Martin Corp.

- Marshall of Cambridge Holdings Ltd.

- Omega Aerial Refueling Services Inc.

- Parker Hannifin Corp.

- Protankgrup

- Rostec

- Safran SA

- Smiths Group Plc

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Military Aerial Refueling Tanker Market

- In January 2025, Boeing and Lockheed Martin, two leading aerospace and defense companies, announced a strategic partnership to explore joint opportunities in the market. The collaboration aims to leverage their collective expertise and resources to offer advanced tanker solutions to their global clientele (Boeing Press Release, 2025).

- In March 2025, the United States Air Force (USAF) awarded a USD 1.2 billion contract to Lockheed Martin for the production and delivery of additional KC-130J aerial refueling tankers. This contract expansion underlines the USAF's commitment to enhancing its refueling capabilities (US Department of Defense, 2025).

- In May 2025, Airbus Defense and Space successfully completed the first flight of its new A330 Multi-Role Tanker Transport (MRTT) for the United Arab Emirates (UAE) Air Force. The MRTT is a versatile military aerial refueling tanker, and this successful first flight marks the beginning of deliveries to the UAE (Airbus Defense and Space Press Release, 2025).

- In August 2024, Rolls-Royce secured a USD 300 million contract from Boeing to provide T56 engines for the KC-46 Pegasus military aerial refueling tanker. This contract underscores Rolls-Royce's role as a key supplier in the market (Rolls-Royce Press Release, 2024).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Military Aerial Refueling Tanker Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.01% |

|

Market growth 2024-2028 |

USD 4218.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.43 |

|

Key countries |

US, China, France, UK, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Military Aerial Refueling Tanker Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is witnessing significant growth due to the increasing demand for reducing aerial refueling time and improving fuel transfer efficiency. Advanced fuel system monitoring and next generation refueling boom designs are key areas of focus to enhance aerial refueling safety and optimize tanker aircraft operations. Next-generation fuel management strategies, such as predictive maintenance and advanced pilot training techniques, are essential to ensure the reliability and effectiveness of aerial refueling systems. The impact of fuel tank design on range and advanced fuel management strategies are crucial factors in the market. The analysis of refueling system failures and implementation of new safety protocols are essential to maintaining compliance and improving operational planning in the market. Modernization of aerial refueling systems, including the development of refueling simulation models and integration of advanced flight control, is a significant trend. Assessment of drogue system reliability and maintenance procedures for refueling systems are critical to ensuring the availability and performance of military aerial refueling tankers. Airborne refueling system troubleshooting is an ongoing process to minimize downtime and maintain the readiness of these vital assets. Compared to traditional methods, the adoption of advanced technologies in military aerial refueling tankers can lead to a 20% reduction in fuel transfer time, resulting in significant cost savings and operational advantages. The market is expected to continue its growth trajectory as defense forces worldwide prioritize the modernization and optimization of their refueling capabilities.

What are the Key Data Covered in this Military Aerial Refueling Tanker Market Research and Growth Report?

-

What is the expected growth of the Military Aerial Refueling Tanker Market between 2024 and 2028?

-

USD 4.22 billion, at a CAGR of 7.01%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (Probe-and-drogue and Boom-and-receptacle), Type (Manned and Unmanned), and Geography (North America, APAC, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Joint development/acquisition approach, Design and development-related constraints

-

-

Who are the major players in the Military Aerial Refueling Tanker Market?

-

Airbus SE, BAE Systems Plc, Bandak Aviation Inc., Cobham Ltd., Dassault Aviation SA, Draken International, LLC, Eaton Corp. Plc, Embraer SA, General Electric Co., Israel Aerospace Industries Ltd., Liebherr International Deutschland GmbH, Lockheed Martin Corp., Marshall of Cambridge Holdings Ltd., Omega Aerial Refueling Services Inc., Parker Hannifin Corp., Protankgrup, Rostec, Safran SA, Smiths Group Plc, and The Boeing Co.

-

We can help! Our analysts can customize this military aerial refueling tanker market research report to meet your requirements.

RIA -

RIA -