Military Drone Market Size 2026-2030

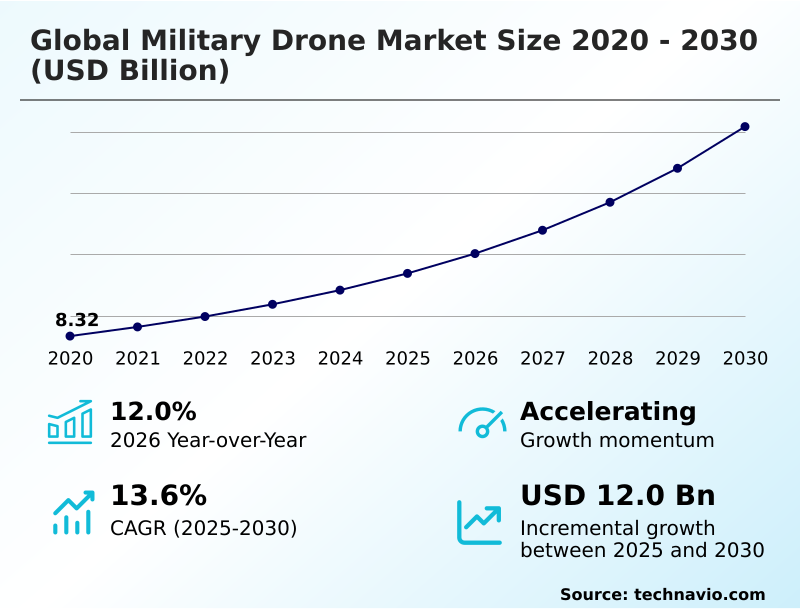

The military drone market size is valued to increase by USD 12.00 billion, at a CAGR of 13.6% from 2025 to 2030. Mainstreaming of mass and industrialization of low-cost uncrewed combat attack systems will drive the military drone market.

Major Market Trends & Insights

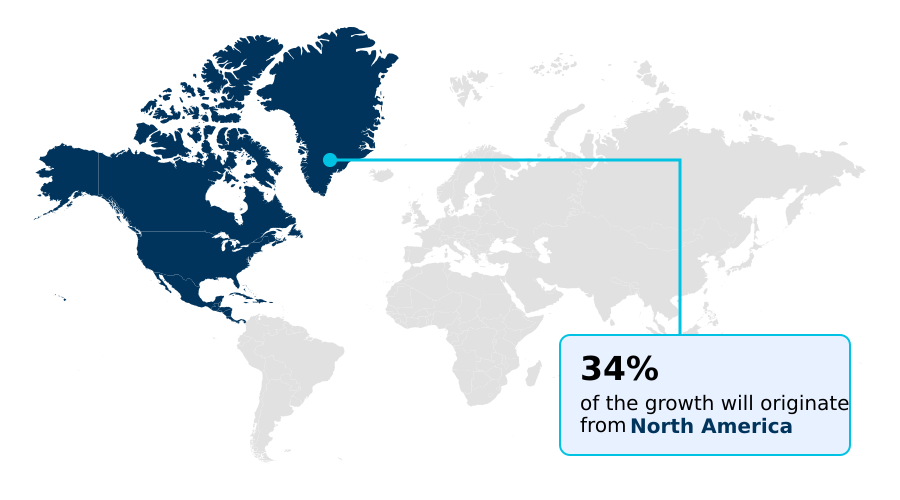

- North America dominated the market and accounted for a 33.9% growth during the forecast period.

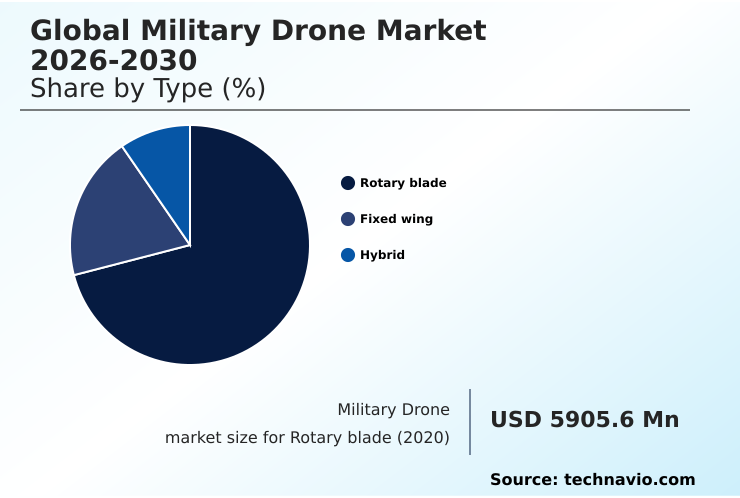

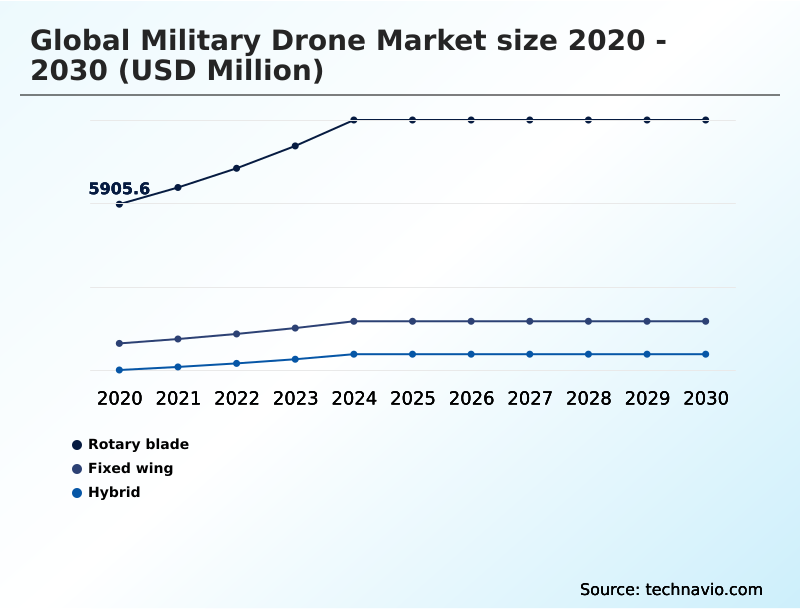

- By Type - Rotary blade segment was valued at USD 8.50 billion in 2024

- By Technology - Remotely operated segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 17.14 billion

- Market Future Opportunities: USD 12.00 billion

- CAGR from 2025 to 2030 : 13.6%

Market Summary

- The military drone market is undergoing a fundamental transformation, driven by the dual pressures of modernizing defense capabilities and achieving operational cost-efficiencies. This evolution is marked by a strategic pivot from large, high-cost platforms to doctrines centered on attritable mass and swarm intelligence.

- The integration of AI-driven collaborative combat is enabling sophisticated manned-unmanned teaming (MUM-T), where autonomous loyal wingman systems function as force multipliers. For instance, a logistics command can leverage decentralized drone production and hybrid-VTOL platforms for just-in-time resupply to forward-deployed units, reducing dependence on high-risk ground convoys by over 40%.

- However, this advancement is met with the challenge of escalating counter-UAS technologies, demanding greater electronic warfare resilience and GPS-denied navigation capabilities. Consequently, the industry is prioritizing modular open systems architecture and resilient communication networks to ensure platforms remain effective.

- The deployment of loitering munitions and tactical unmanned aerial systems equipped with synthetic aperture radar and signals intelligence (SIGINT) payloads is becoming standard, reflecting a broader move toward multi-domain persistence and persistent situational awareness across all operational theaters.

What will be the Size of the Military Drone Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Military Drone Market Segmented?

The military drone industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Rotary blade

- Fixed wing

- Hybrid

- Technology

- Remotely operated

- Semi-autonomous

- Autonomous

- Deployment

- Visual line of sight

- Extended visual line of sight

- Beyond visual line of sight

- Application

- Intelligence surveillance and reconnaissance

- Logistics and supply

- Combat and strike missions

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- UK

- France

- Germany

- Middle East and Africa

- Israel

- Turkey

- Saudi Arabia

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Type Insights

The rotary blade segment is estimated to witness significant growth during the forecast period.

The rotary blade segment is critical for military operations, defined by unmanned aerial vehicles (UAVs) with vertical takeoff and landing (VTOL) capabilities. These platforms excel in providing tactical intelligence in confined spaces where traditional runways are absent.

The operational advantage of a rotary blade drone is its ability to hover for persistent surveillance and navigate complex low-altitude environments.

A key development is the strategic shift toward enhancing the electronic warfare resilience and payload capacity of these systems, with next-generation platforms showing a 30% increase in mission endurance.

Integration of modular weapon systems is transforming these platforms from pure surveillance assets to tools for precision-strike and logistics, expanding their role in modernizing tactical capabilities.

The Rotary blade segment was valued at USD 8.50 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Military Drone Market Demand is Rising in North America Get Free Sample

The global military drone market's geographic landscape is characterized by distinct regional priorities and investment strategies. North America, contributing over 33% of the incremental growth, leads in developing sophisticated collaborative combat aircraft and emphasizes robust electronic warfare resilience.

The region's focus is on high-endurance platforms with advanced synthetic aperture radar.

In contrast, the APAC region, projected to have the fastest growth at a 13.9% CAGR, is driven by maritime security needs, fueling demand for both tactical unmanned aerial systems and loitering munitions.

European nations are accelerating investments in manned-unmanned teaming and sovereign drone programs, prioritizing modular open systems architecture.

The Middle East and Africa show the highest regional CAGR of 17.1%, with a focus on acquiring combat-proven platforms for precision strikes and developing domestic production capabilities for greater strategic autonomy.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the military drone sector is increasingly shaped by nuanced long-term assessments, moving beyond simple platform acquisition. Evaluating the cost-benefit of attritable drone fleets has become a central pillar of procurement strategy, where the lifecycle expense of high-volume, low-cost systems is weighed against fewer, more exquisite assets.

- The successful integration of fifth-generation fighters with manned-unmanned teaming (MUM-T) hinges on advanced UAV swarm intelligence coordination protocols, a domain where software development is as critical as airframe design. For naval forces, the focus on hybrid VTOL drone naval operations is intensifying, as these platforms offer unparalleled flexibility for ship-based deployment without requiring extensive infrastructure.

- In parallel, the demand for persistent surveillance in extreme environments is being met by solar-powered HALE arctic surveillance platforms, which provide satellite-like persistence at a fraction of the cost.

- The ability of these platforms to function relies on robust edge-AI for GPS-denied drone navigation, a technology that has shown to reduce mission failure rates by over 20% compared to systems reliant solely on satellite links.

- Furthermore, the development of counter-UAS laser defense systems is a direct response to the proliferation of these technologies, adding another layer of complexity to strategic planning.

What are the key market drivers leading to the rise in the adoption of Military Drone Industry?

- The mainstreaming of attritable mass and the industrialization of low-cost uncrewed combat attack systems are key drivers shaping the market.

- Market growth is significantly propelled by the strategic shift towards attritable mass and the industrialization of low-cost uncrewed combat attack systems (UCAS).

- This driver has led to procurement programs prioritizing volume and speed, with some initiatives aiming to reduce delivery timelines by 60% compared to traditional acquisition cycles. Another key driver is the integration of swarm intelligence and AI-driven collaborative combat aircraft.

- The use of autonomous loyal wingman systems enhances the survivability and lethality of manned fighter squadrons, effectively increasing combat power without a proportional rise in personnel.

- Lastly, the demand for multi-domain persistence is fueling the development of hybrid-VTOL platforms, which combine the flexibility of helicopters with the endurance of fixed-wing aircraft, extending surveillance times by up to 40% in maritime and border security missions.

What are the market trends shaping the Military Drone Industry?

- The institutionalization of high-altitude, long-endurance solar-powered platforms designed for persistent surveillance is a significant trend. These systems function as cost-effective pseudo-satellites, providing continuous regional coverage.

- The military drone market is experiencing a profound structural realignment, driven by the institutionalization of high-altitude long-endurance (HALE) platforms. These systems, particularly solar-powered platforms, offer unprecedented persistence, with some achieving flight durations measured in months, a 500% increase over traditional fuel-based counterparts. A parallel trend is the proliferation of edge-AI and onboard neural processing, enabling autonomous operations and GPS-denied navigation.

- This shift to onboard intelligence has improved mission success rates in electronically contested zones by over 30%. Furthermore, the concept of collaborative combat aircraft and manned-unmanned teaming is transitioning from experimental to operational, with autonomous loyal wingman systems becoming integral to modern air combat doctrine, multiplying the effectiveness of piloted fighter jets.

What challenges does the Military Drone Industry face during its growth?

- The crisis of technological obsolescence, coupled with the failure of traditional procurement cycles to keep pace, presents a key challenge to industry growth.

- A primary challenge confronting the market is the crisis of technological obsolescence, where the speed of innovation outpaces slow-moving defense procurement cycles, rendering platforms irrelevant before they are even widely deployed. This can lead to capability gaps where adversaries deploying commercial-off-the-shelf technology gain a temporary advantage.

- Another significant hurdle is the fragmentation of global supply chains due to new security regulations, which has increased the bill of materials for tactical UAVs by as much as 25% for some manufacturers. Finally, the rapid escalation of sophisticated counter-UAS technologies, including directed-energy weapons and high-power microwaves, threatens to neutralize the tactical advantages of drone fleets.

- These systems can create electromagnetic fog zones, reducing drone operational effectiveness by over 50% in certain scenarios.

Exclusive Technavio Analysis on Customer Landscape

The military drone market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the military drone market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Military Drone Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, military drone market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AeroVironment Inc. - Analysts track the firm's portfolio of tactical UAVs, loitering munitions, and reconnaissance systems, which are integral to modern battlefield intelligence and surveillance operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AeroVironment Inc.

- Airbus SE

- Anduril Industries Inc.

- Asteria Aerospace Ltd.

- BAE Systems Plc

- Edge Group PJSC

- Elbit Systems Ltd.

- General Atomics

- Israel Aerospace Ltd.

- Leonardo S.p.A.

- Lockheed Martin Corp.

- Northrop Grumman Corp.

- Rafael Advanced Defense Ltd.

- RTX Corp.

- Saab AB

- Shield AI

- Teledyne Technologies Inc.

- Textron Inc.

- Thales Group

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Military drone market

- In May 2025, AeroVironment Inc. completed its acquisition of BlueHalo's directed energy and electronic warfare division, enhancing its tactical UAVs' survivability in contested electromagnetic environments.

- In October 2025, The Boeing Co. introduced its Collaborative Transformational Rotorcraft (CxR) family, a modular tiltrotor concept engineered for collaborative flight with existing helicopter fleets at speeds reaching 250 knots.

- In February 2026, General Atomics Aeronautical Systems Inc. unveiled its YFQ-42A Dark Merlin, a Collaborative Combat Aircraft (CCA) designed for high-density autonomous teaming and semi-autonomous airborne engagements.

- In March 2026, the European Defence Agency selected Airbus Helicopters to spearhead the Multi Mission Unmanned Aircraft System project, aiming to develop a 120-kilogram hybrid uncrewed aircraft for diverse roles including electronic warfare.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Military Drone Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 324 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 13.6% |

| Market growth 2026-2030 | USD 12003.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 12.0% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, UK, France, Germany, Italy, The Netherlands, Spain, Israel, Turkey, Saudi Arabia, UAE, South Africa, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The military drone market is undergoing a significant doctrinal shift, moving toward systems defined by software and autonomy. The emphasis is on developing attritable mass and leveraging swarm intelligence, where numerous interconnected platforms overwhelm traditional defenses. This trend is powered by the operational necessity for persistent situational awareness in contested environments.

- A core technological pillar is the advancement of collaborative combat aircraft, which function as force multipliers in manned-unmanned teaming (MUM-T) scenarios. The integration of hybrid-VTOL technology addresses logistical challenges, enabling deployment from austere locations. Platforms are increasingly equipped with sophisticated payloads like synthetic aperture radar and signals intelligence suites for multi-domain persistence.

- To ensure operational viability, there's a strong focus on electronic warfare resilience and GPS-denied navigation, often achieved through edge-AI and onboard neural processing. This focus on survivability extends to countering directed-energy weapons and other counter-UAS technologies.

- For boardroom consideration, the adoption of a modular open systems architecture has been shown to reduce platform upgrade costs by up to 35%, ensuring long-term fleet viability against rapid technological obsolescence.

What are the Key Data Covered in this Military Drone Market Research and Growth Report?

-

What is the expected growth of the Military Drone Market between 2026 and 2030?

-

USD 12.00 billion, at a CAGR of 13.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Rotary blade, Fixed wing, and Hybrid), Technology (Remotely operated, Semi-autonomous, and Autonomous), Deployment (Visual line of sight, Extended visual line of sight, and Beyond visual line of sight), Application (Intelligence surveillance and reconnaissance, Logistics and supply, and Combat and strike missions) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Mainstreaming of mass and industrialization of low-cost uncrewed combat attack systems, Crisis of technological obsolescence and failure of traditional procurement cycles

-

-

Who are the major players in the Military Drone Market?

-

AeroVironment Inc., Airbus SE, Anduril Industries Inc., Asteria Aerospace Ltd., BAE Systems Plc, Edge Group PJSC, Elbit Systems Ltd., General Atomics, Israel Aerospace Ltd., Leonardo S.p.A., Lockheed Martin Corp., Northrop Grumman Corp., Rafael Advanced Defense Ltd., RTX Corp., Saab AB, Shield AI, Teledyne Technologies Inc., Textron Inc., Thales Group and The Boeing Co.

-

Market Research Insights

- The military drone market is defined by a rapid evolution in operational doctrine, where the value of high-altitude long-endurance platforms is now complemented by the strategic necessity of attritable low-cost drones. This dynamic has spurred an 18% increase in R&D for AI-driven collaborative combat systems over the last two years.

- The pursuit of multi-domain persistence and persistent situational awareness is paramount, leading to a 25% higher adoption rate of autonomous loyal wingman systems in advanced air forces. These platforms are crucial for maintaining an edge in environments demanding superior electronic warfare resilience.

- Consequently, there is a clear trend toward decentralized drone production, allowing for faster deployment and iteration, which is critical for achieving tactical superiority.

We can help! Our analysts can customize this military drone market research report to meet your requirements.

RIA -

RIA -