Military Hybrid Electric Vehicle (HEV) And Electric Vehicle (EV) Market Size 2025-2029

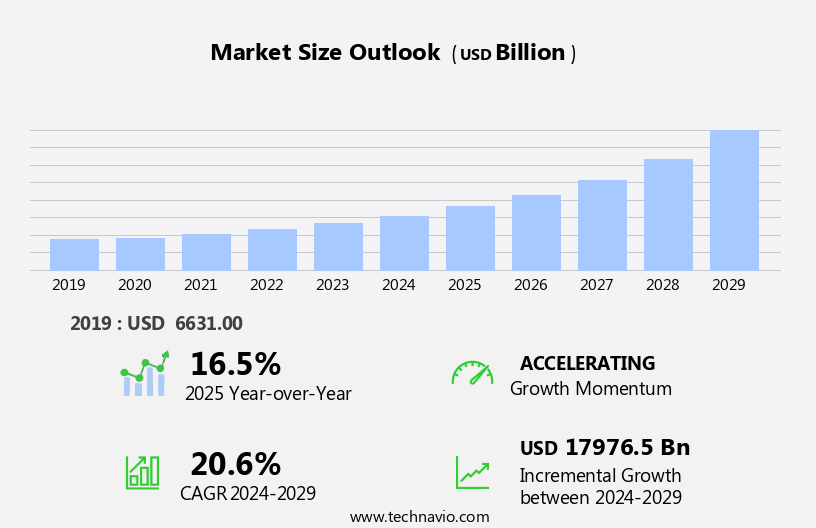

The military hybrid electric vehicle (HEV) and electric vehicle (EV) market size is forecast to increase by USD 17,976.5 billion, at a CAGR of 20.6% between 2024 and 2029.

- The market is driven by the increasing push towards adopting eco-friendly transportation solutions in military applications. Advancements in battery technology have significantly improved the performance and efficiency of both HEVs and EVs, making them increasingly attractive options for military operations. However, the high total cost of ownership of HEVs remains a significant challenge for their widespread adoption. Despite this obstacle, key players in the market continue to invest in HEV and EV technologies to meet the growing demand for sustainable military transportation. For instance, BAE Systems' Flexible Hybrid Electric Vehicle System (FHEV) and General Dynamics' Tactical Electric Hybrid Vehicle (TEHV) are notable examples of HEVs that offer improved fuel efficiency and reduced emissions. Command & control systems, sensor fusion, and machine learning (ML) are enhancing situational awareness and mission planning.

- In the EV segment, companies such as Tesla and Rivian are developing advanced battery technologies and electric powertrains to meet the unique requirements of military applications. However, the integration of these advanced technologies into military vehicles poses unique challenges, such as the need for ruggedized batteries and specialized charging infrastructure. Additionally, the high upfront cost of EVs and HEVs compared to traditional internal combustion engine vehicles remains a significant barrier to entry for some military organizations. Hydrogen storage and fast charging are crucial for extended range and quick refueling.

What will be the Size of the Military Hybrid Electric Vehicle (HEV) And Electric Vehicle (EV) Market during the forecast period?

- In the dynamic military transportation landscape, Hybrid Electric Vehicles (HEVs) and Electric Vehicles (EVs) are gaining momentum, integrating advanced technologies such as autonomous mobility, wireless charging, and fuel cell technology. Smart charging systems, powered by renewable energy sources like solar panels and wind turbines, are enabling efficient energy management. Military communication systems and satellite communication ensure seamless connectivity for vehicle cybersecurity and data analytics. Logistics optimization, fleet management, and thermal management are essential for efficient operations.

- Object tracking, connected vehicles, and traffic management contribute to improved situational awareness and mission effectiveness. Battery recycling and swapping are addressing sustainability concerns, while mission planning and machine learning (ML) enable predictive maintenance and improved performance. Military automation, including robotics and image recognition, is revolutionizing various applications.

How is this Military Hybrid Electric Vehicle (HEV) And Electric Vehicle (EV) Industry segmented?

The military hybrid electric vehicle (hev) and electric vehicle (ev) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Manned military HEV and EV

- Unmanned military HEV and EV

- Type

- AC charging

- DC charging

- Application

- Combat vehicles

- Support vehicles

- Unmanned vehicles

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Product Insights

The manned military HEV and EV segment is estimated to witness significant growth during the forecast period. The market is primarily driven by the manned military segment in 2024. Manned military HEVs and EVs are operated by one or more personnel and are utilized for transporting fuel, cargo, and passengers during military operations. Compared to unmanned military HEVs and EVs, manned vehicles offer greater efficiency due to the presence of command and control systems and reduced autonomy requirements. Additionally, manned military HEVs and EVs are well-suited for large-scale military operations, reducing the likelihood of technical errors. Military standards and technology transfer play a significant role in the development and adoption of these vehicles.

Autonomous driving and electric powertrains are emerging trends, with electric motors and vehicle armor enhancing vehicle capabilities. Blast protection and combat support vehicles are essential components of military operations, and the integration of HEV and EV technologies can improve their performance and reduce their environmental impact. Government procurement and strategic partnerships are key drivers of market growth, with quiet operation a desirable feature for military applications. Electric power generation and electrical grid integration are essential for energy independence and resilience.

_and_electric_vehicle_(ev)_market_size_abstract_2024_v2.jpg)

The Manned military HEV and EV segment was valued at USD 4,806.50 billion in 2019 and showed a gradual increase during the forecast period.

Fuel efficiency is a critical factor, as military budgets and logistics rely on minimizing energy consumption. Counter-IED measures and off-road capability are essential features for military vehicles, and electric drive systems and traction control systems are integral to achieving these capabilities. Military grade components, such as lithium-ion batteries and power electronics, ensure durability and reliability. Regenerative braking and emissions reduction contribute to the environmental sustainability of military operations. Vehicle connectivity and national security are also crucial considerations, as military vehicles require secure communication systems. Joint ventures and operational testing are essential for the development and implementation of military HEVs and EVs, with a focus on life cycle cost, payload capacity, and vehicle dynamics control.

Regional Analysis

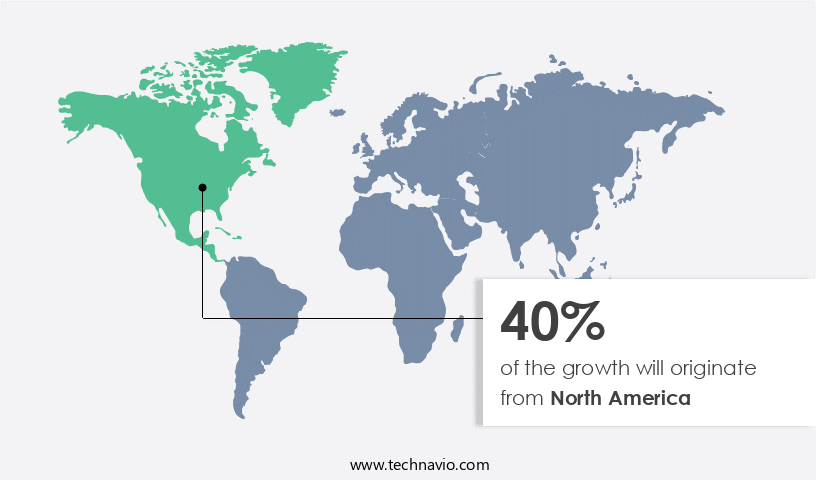

North America is estimated to contribute 40% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market witnesses significant growth, with North America leading as a major manufacturing region. Fiscal incentives for manufacturers, tax credits for HEVs and EVs, and state incentives for hybrid vehicles in this region are driving the market's expansion. The demand for eco-friendly military HEVs and EVs from the government further boosts sales. Military HEV manufacturers are expanding their distributor networks to enhance vehicle availability and awareness. Military standards ensure the integration of advanced technology in these vehicles, such as electric drive systems, traction control systems, and vehicle dynamics control. Military operations require off-road capability and fuel efficiency, making HEVs and EVs attractive alternatives to traditional vehicles.

Counter-IED measures and vehicle armor are crucial considerations in military vehicle design, and HEVs and EVs offer potential solutions with their quiet operation and energy storage capabilities. The military supply chain benefits from the use of HEVs and EVs, as these vehicles have lower emissions and require less frequent refueling. Military budgets and logistics are under constant scrutiny, and the lower life cycle cost of HEVs and EVs compared to traditional vehicles is a significant factor in their adoption. Operational testing and joint ventures between military organizations and vehicle manufacturers are essential for the development and implementation of military-grade components, such as lithium-ion batteries, power electronics, and blast protection.

Electric powertrains, electric motors, and autonomous driving technologies are transforming military vehicle design, offering increased payload capacity and improved vehicle connectivity for tactical applications. The integration of sustainable technologies, such as regenerative braking and emissions reduction systems, aligns with national security objectives and contributes to environmental sustainability. Strategic partnerships between military organizations and vehicle manufacturers facilitate the operational testing and implementation of these advanced technologies in military vehicles.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Military Hybrid Electric Vehicle (HEV) And Electric Vehicle (EV) market drivers leading to the rise in the adoption of Industry?

- The push towards adopting eco-friendly vehicles serves as the primary catalyst for market growth. The military sector is increasingly embracing green technologies to reduce the environmental footprint of its combat support vehicles. Electric Vehicles (EVs) and Military Hybrid Electric Vehicles (Hevs) are gaining traction due to their ability to operate quietly and emit zero tailpipe emissions. These vehicles offer significant advantages, including reduced fuel consumption, lower CO2 emissions, and improved vehicle upfitting with advanced power electronics and blast protection systems. Government procurement agencies are prioritizing the adoption of these vehicles to meet sustainability targets and enhance combat capabilities.

- Quiet operation is a crucial factor in military applications, as it allows for stealthier missions and reduced risk of detection. Moreover, the use of EVs and HEVs in combat support roles can help minimize the need for frequent refueling, thereby reducing the logistical burden and improving overall mission efficiency. The adoption of EVs and HEVs in military applications is a significant trend driven by the need for reduced emissions, improved efficiency, and enhanced capabilities. The development and integration of these vehicles in military fleets require strategic partnerships and advanced power electronics to ensure optimal performance and reliability.

What are the Military Hybrid Electric Vehicle (HEV) And Electric Vehicle (EV) market trends shaping the Industry?

- Advancements in battery technology are currently driving market trends in both electric vehicles (EVs) and hybrid electric vehicles (HEVs). The continuous improvement of battery performance and capacity is a key focus in the automotive industry. The market is experiencing significant growth due to advancements in battery technology. High-performance batteries, such as lithium-ion, are essential for enhancing the range, fuel efficiency, and off-road capability of military EVs and HEVs. These technological improvements enable militaries worldwide to incorporate electric drive systems into various applications, including logistics vehicles and combat platforms.

- The supply chain for military EVs and HEVs is also benefiting from technology transfer, as advancements in civilian electric vehicle technology are being adapted for military applications. Overall, the military budget continues to prioritize the development and adoption of electric propulsion systems for its vehicle fleet. Companies like Lockheed Martin, General Dynamics Corp., and BAE Systems Plc are leading the way in developing and supplying advanced battery technologies for military use. The military standards for terrain mobility and counter-IED measures are driving the demand for these vehicles, as they offer increased fuel efficiency and reduced emissions.

How does Military Hybrid Electric Vehicle (HEV) And Electric Vehicle (EV) market faces challenges face during its growth?

- The high total cost of ownership for Hybrid Electric Vehicles (HEVs) represents a significant challenge that could hinder industry growth. This cost encompasses not only the initial purchase price but also ongoing expenses such as battery replacement and charging infrastructure. To remain competitive, manufacturers must continually find ways to reduce these costs and make HEVs more affordable for consumers. Military Hybrid Electric Vehicles (HEVs) and Electric Vehicles (EVs) are gaining traction in military logistics due to their potential to reduce environmental impact and enhance operational capabilities. The defense sector's significant spending on research and development in these areas has led to field trials of military-grade components, such as lithium-ion batteries, regenerative braking systems, and vehicle connectivity. These advanced technologies offer benefits like longer operational hours, increased vehicle range, and improved tactical mobility.

- For instance, a 24 kWh battery in a popular economic hybrid vehicle, like the Nissan Leaf, costs approximately USD12,000. This amount could instead be used to purchase a plush sedan model of an ICE car. Similarly, the Chevrolet Volt, which uses a 6 kWh battery pack, has an additional price tag of USD5,000 compared to ICE vehicles. Despite the higher costs, military HEVs and EVs offer several advantages, including reduced fuel consumption, lower emissions, and enhanced vehicle connectivity. These features are crucial for military operations, as they contribute to national security and mission success. Additionally, the use of these vehicles aligns with the broader trend towards environmental sustainability and reducing carbon footprints. Military HEVs and EVs come with a higher total cost of ownership compared to traditional Internal Combustion Engine (ICE) vehicles. The primary reason for this is the use of high-capacity batteries and advanced electronic components.

Exclusive Customer Landscape

The military hybrid electric vehicle (HEV) and electric vehicle (EV) market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the military hybrid electric vehicle (HEV) and electric vehicle (EV) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, military hybrid electric vehicle (HEV) and electric vehicle (EV) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AeroVironment Inc. - The company specializes in military-grade hybrid electric vehicles (HEV) and electric vehicles (EV), engineered for extended mission durations exceeding 24 hours.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AeroVironment Inc.

- Alke s.r.l.

- BAE Systems Plc

- Elbit Systems Ltd.

- Ford Motor Co.

- General Atomics

- General Dynamics Corp.

- General Motors Co.

- Honeywell International Inc.

- L3Harris Technologies Inc.

- Lockheed Martin Corp.

- Logos Technologies LLC

- Milrem AS

- Nikola Corp.

- Northrop Grumman Corp.

- Oshkosh Corp.

- QinetiQ Ltd.

- Singapore Technologies Engineering Ltd.

- The Boeing Co.

- Zero Motorcycles Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Military Hybrid Electric Vehicle (HEV) And Electric Vehicle (EV) Market

- In February 2023, General Dynamics Land Systems announced the successful integration of a hybrid electric power system into their Stryker Infantry Vehicle, marking a significant step forward in military land vehicle electrification (General Dynamics Press Release). This development is expected to enhance the vehicle's operational efficiency and reduce its carbon footprint.

- In October 2022, Lockheed Martin and Tesla entered into a strategic partnership to collaborate on the development of electric propulsion systems for military applications. This collaboration is set to leverage Tesla's expertise in battery technology and Lockheed Martin's experience in military systems engineering (Lockheed Martin Press Release).

- In July 2021, the U.S. Army awarded a contract to BAE Systems for the production of 495 Next-Generation Combat Vehicles, with an option for an additional 1,185 vehicles. These vehicles will be hybrid electric, featuring a diesel engine and an electric motor, aiming to improve fuel efficiency and reduce emissions (BAE Systems Press Release).

- In April 2020, the U.S. Department of Defense released a policy statement emphasizing the importance of electrification in military vehicles. The statement outlined plans to invest in research and development, as well as the acquisition of electric and hybrid electric vehicles, to reduce the military's reliance on fossil fuels and improve operational readiness (Department of Defense Press Release).

Research Analyst Overview

The military HEV and EV market continues to evolve, driven by the need for terrain mobility, military standards, and advanced technology. Military vehicles are undergoing significant transformations, integrating electric drive systems and traction control systems to enhance off-road capability and fuel efficiency. Military budgets and defense spending are prioritizing sustainable technologies, such as lithium-ion batteries and regenerative braking, to reduce emissions and improve operational readiness. Military logistics and supply chain are also adapting to the shift towards electric powertrains, with electric motors and power electronics becoming increasingly important components. Counter-IED measures and vehicle armor are being integrated into electric vehicles to ensure military standards are met.

Field trials and operational testing are ongoing, with military grade components undergoing rigorous evaluation to ensure they meet the demands of military operations. Joint ventures and strategic partnerships are forming between defense contractors and automotive companies to accelerate technology transfer and innovation. The evolving nature of military vehicle applications extends to tactical vehicles, combat support vehicles, and even autonomous driving capabilities. Vehicle connectivity and energy storage are also critical considerations, as military operations require reliable and efficient communication and power systems. National security and quiet operation are also driving the adoption of electric vehicles in military applications, as they offer reduced environmental impact and improved stealth capabilities.

The ongoing integration of electric powertrains and military standards is shaping the future of military mobility, with continued advancements in vehicle dynamics control and emissions reduction expected. The Military Hybrid Electric Vehicle (HEV) and Electric Vehicle (EV) Market is evolving rapidly, driven by advancements in electric grid integration, enabling efficient power management in defense operations. Battery swapping technology enhances mission readiness, allowing quick energy replenishment in combat zones. The incorporation of artificial intelligence (AI) optimizes vehicle performance, autonomy, and predictive maintenance. Vehicle-to-Vehicle (V2V) communication improves coordination among military fleets, while Vehicle-to-Infrastructure (V2I) communication strengthens connectivity with command centers and logistics hubs. The integration of military robotics in HEVs and EVs boosts operational efficiency, offering automation in surveillance and tactical maneuvers.

Dive into Technavio's strong research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Military Hybrid Electric Vehicle (HEV) And Electric Vehicle (EV) Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

218 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 20.6% |

|

Market growth 2025-2029 |

USD 17,976.5 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

16.5 |

|

Key countries |

US, China, Canada, India, Japan, Germany, France, South Korea, Australia, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Military Hybrid Electric Vehicle (HEV) And Electric Vehicle (EV) Market Research and Growth Report?

- CAGR of the Military Hybrid Electric Vehicle (HEV) And Electric Vehicle (EV) industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the military hybrid electric vehicle (hev) and electric vehicle (ev) market growth of industry companies

We can help! Our analysts can customize this military hybrid electric vehicle (hev) and electric vehicle (ev) market research report to meet your requirements.

RIA -

RIA -