Military Sensor Fusion Market Size 2026-2030

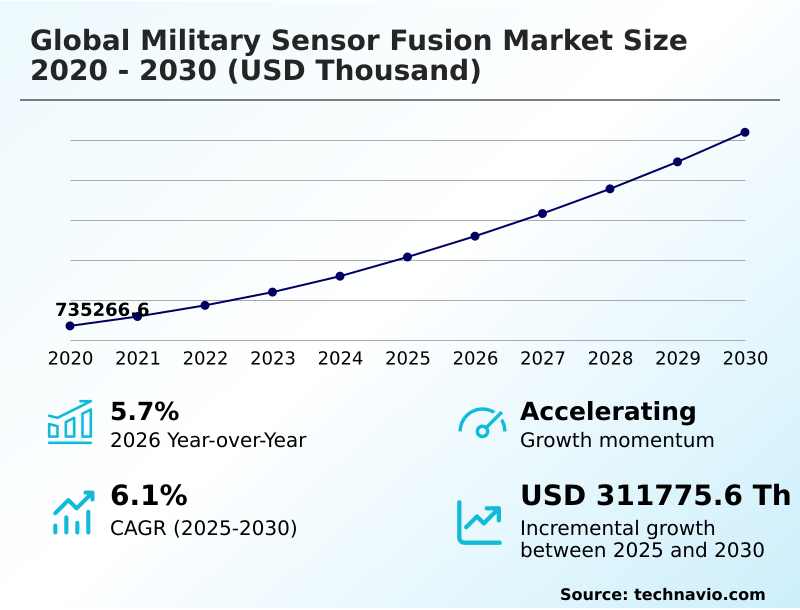

The military sensor fusion market size is valued to increase by USD 311.78 million, at a CAGR of 6.1% from 2025 to 2030. Increasing demand for enhanced situational awareness across multi-domain operations will drive the military sensor fusion market.

Major Market Trends & Insights

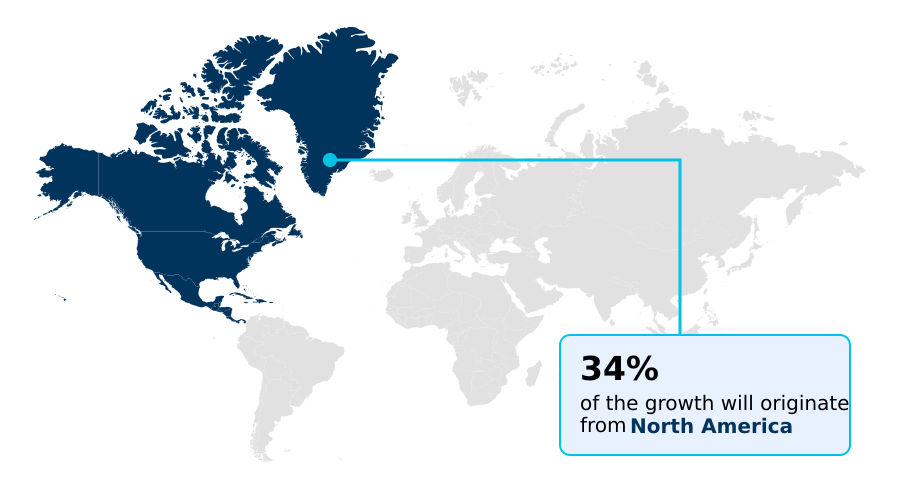

- North America dominated the market and accounted for a 33.8% growth during the forecast period.

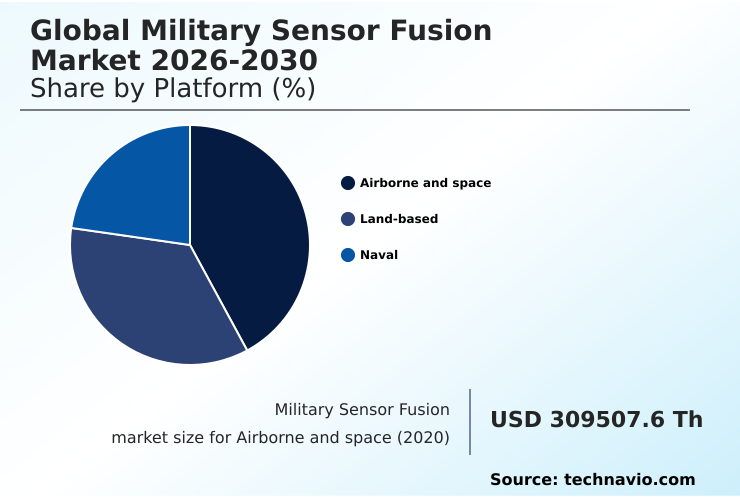

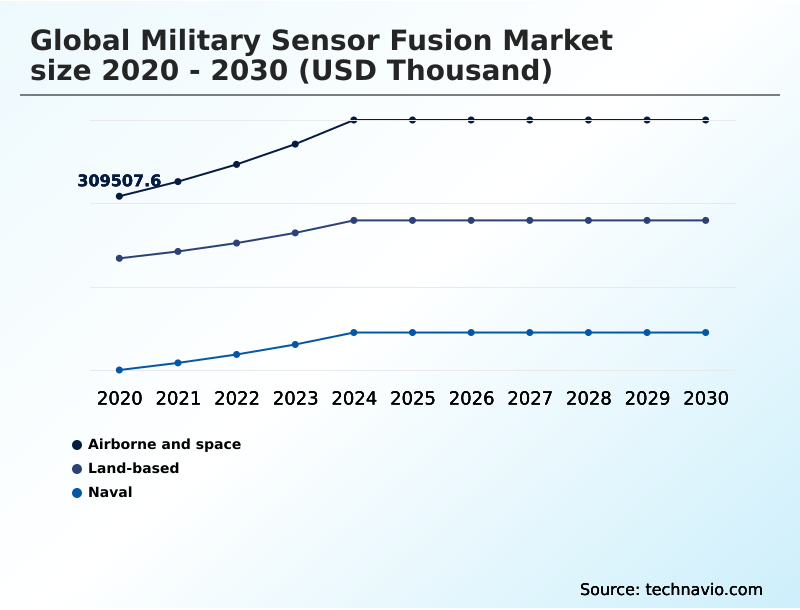

- By Platform - Airborne and space segment was valued at USD 371.98 million in 2024

- By Type - Radar segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities:

- Market Future Opportunities: USD 311.78 million

- CAGR from 2025 to 2030 : 6.1%

Market Summary

- The military sensor fusion market is crucial for modern warfare, integrating data from diverse sensors like radar, EO/IR, and sonar to create a unified operational picture. Key drivers include the necessity for superior enhanced situational awareness in multi-domain operations and the proliferation of unmanned systems.

- The integration of artificial intelligence and machine learning is a pivotal driver, enabling automated target recognition (ATR) and predictive threat analysis to manage the overwhelming data from systems like multi-spectral imaging arrays.

- For instance, in a naval scenario, a fleet's battlefield management system can fuse subsurface acoustic intelligence from an AUV with synthetic aperture radar (SAR) data from a patrol aircraft to generate a weapon-quality track on a hostile submarine, a task impossible for a single platform.

- Key trends include the shift to open systems architecture for improved interoperability standards and the development of quantum sensing technology for navigation in signal-denied environments. However, challenges such as high integration costs, processing latency, and vulnerability to electronic warfare (EW) persist. Addressing the need for cyber-resilient networks and managing lifecycle costs are critical for sustained adoption and operational success.

What will be the Size of the Military Sensor Fusion Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Military Sensor Fusion Market Segmented?

The military sensor fusion industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD thousand" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Platform

- Airborne and space

- Land-based

- Naval

- Type

- Radar

- Electro optical and infrared

- Electronic warfare

- Sonar

- Application

- ISR

- Situational awareness

- Target tracking

- Battlefield management

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- Israel

- UAE

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Platform Insights

The airborne and space segment is estimated to witness significant growth during the forecast period.

The airborne platform segment is defined by capital-intensive programs integrating technologies like active electronically scanned array (AESA) and hypersonic and ballistic tracking systems.

For successful multi-domain operations, platforms must utilize synthetic aperture radar (SAR) and phased-array radar to provide a common operating picture (COP). The use of advanced tactical data links enables real-time decision support, enhancing command and control (C2) agility.

This integration is critical for achieving an information dominance strategy and maintaining persistent surveillance capabilities. Onboard edge computing hardware is essential for processing data from electro-optical/infrared (EO/IR) systems, achieving target acquisition speed in contested environments.

Retrofitting legacy fleets with these capabilities often increases lifecycle costs by over 25%.

The Airborne and space segment was valued at USD 371.98 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Military Sensor Fusion Market Demand is Rising in North America Request Free Sample

The North America region leads the market, driven by substantial defense spending on battlefield management systems and modernization programs focused on cooperative engagement capability (CEC). This region's focus on weapon-quality track generation results in a 5.8% growth rate.

However, the APAC region is forecast to expand at a much faster rate of 7.6%, fueled by indigenous development of millimeter-wave radar, acoustic sensor arrays, and technologies for subsurface acoustic intelligence.

This push for self-reliance addresses unique regional needs for anti-access/area denial (A2/AD) capabilities.

European efforts often involve multinational collaboration on systems using multi-static radar configurations and time difference of arrival (TDOA) techniques for passive surveillance techniques, emphasizing shared development to manage costs and enhance coalition effectiveness.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic implementation of military sensor fusion is rapidly evolving, driven by specific operational demands across different domains. A primary focus is on sensor fusion for dismounted soldiers, where miniaturized systems provide unprecedented situational awareness. Concurrently, the use of AI in military target tracking is revolutionizing air and missile defense, improving accuracy and reducing response times.

- The proliferation of autonomous platforms makes sensor fusion for unmanned systems and sensor fusion for autonomous vehicles critical for navigation and mission execution in contested environments. In naval contexts, data fusion in naval warfare, which combines acoustic and non-acoustic sensor fusion, is key to maintaining undersea dominance.

- Similarly, sensor fusion for missile defense is paramount for national security, requiring the seamless integration of ground-based and space-based assets. Emerging fields like quantum sensing for secure navigation promise to overcome GPS vulnerabilities.

- The core technology relies on robust sensor data fusion algorithms, such as the Kalman filter for target tracking, which are increasingly processed at the tactical edge through edge computing for sensor fusion. Adopting an open architecture for sensor integration is essential for managing multi-domain sensor fusion challenges and avoiding vendor lock-in.

- The benefits of military sensor fusion, especially in providing enhanced sensor fusion for situational awareness, are undeniable. However, significant challenges in multi-sensor data fusion persist, particularly in complex scenarios like sensor fusion for urban warfare or coordinating data from UAV swarms.

- These challenges are also present in sensor fusion in electronic warfare, where distinguishing between hostile and friendly signals is crucial. Finally, integrating disparate sensor types, such as combining radar and EO/IR sensor fusion, remains a complex but vital task, with advanced platforms showing a 30% faster target engagement cycle compared to legacy, non-integrated systems.

What are the key market drivers leading to the rise in the adoption of Military Sensor Fusion Industry?

- The increasing demand for enhanced situational awareness across multi-domain operations is a key driver fueling market growth.

- The drive for enhanced situational awareness in joint all-domain command and control (JADC2) frameworks is a primary market driver.

- The proliferation of unmanned surface vessels (USV) and autonomous underwater vehicles (AUV) demands sophisticated fusion for autonomous navigation and asymmetric threat detection. The integration of AI and cognitive radar systems allows for dynamic spectrum management and electromagnetic spectrum dominance.

- This advanced processing, using methods like Kalman filtering algorithms, improves threat classification accuracy and enables predictive threat analysis. For instance, AI-driven fusion engines have demonstrated a 60% improvement in distinguishing hostile targets from civilian traffic in dense scenarios.

- This leads to network-centric warfare and effective counter-UAV measures.

What are the market trends shaping the Military Sensor Fusion Industry?

- The miniaturization of micro-electromechanical systems is a significant trend, enabling advanced sensor fusion capabilities for dismounted soldier applications.

- A major market trend is the move toward open systems architecture, enabling rapid technology insertion and improved interoperability standards. This modularity supports the integration of next-generation quantum sensing technology for resilient navigation and timing (PNT) in signal-denied environments. The miniaturization of components like inertial measurement units (IMU) is facilitating deployment on unmanned aerial vehicle (UAV) swarms and dismounted soldiers.

- These smaller systems utilize augmented reality overlays to reduce cognitive load and enhance human-machine teaming. The adoption of these architectures has been shown to reduce platform modernization timelines by up to 40%, a significant improvement over proprietary systems. This shift promotes platform modernization programs and unmanned systems integration.

What challenges does the Military Sensor Fusion Industry face during its growth?

- High costs associated with system integration and lifecycle maintenance present a key challenge to market growth.

- A key challenge is data overload mitigation, as multi-spectral imaging and distributed aperture systems (DAS) generate immense data volumes. This can lead to significant processing latency reduction issues, which are critical in fast-paced engagements. The high costs associated with lifecycle cost management and ensuring supply chain security for microelectronics present considerable financial hurdles.

- Moreover, integrated systems are vulnerable to cyberattacks, requiring robust cyber-resilient networks. For example, integrating a new electronic warfare (EW) support measures suite can require a 15% increase in a platform's power and cooling capacity. Protecting low probability of intercept (LPI) signals and ensuring effective combat identification (CID) in a contested electromagnetic environment remain complex technical challenges for multi-domain battle management.

Exclusive Technavio Analysis on Customer Landscape

The military sensor fusion market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the military sensor fusion market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Military Sensor Fusion Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, military sensor fusion market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ASELSAN AS - Provides integrated combat management systems and multi-sensor fusion radar, specializing in advanced data synthesis for enhanced operational command and control.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ASELSAN AS

- BAE Systems Plc

- CACI International Inc.

- Elbit Systems Ltd.

- General Dynamics Corp.

- HENSOLDT AG

- Indra Sistemas SA

- Kongsberg Gruppen ASA

- L3Harris Technologies Inc.

- Leidos Holdings Inc.

- Leonardo S.p.A.

- Lockheed Martin Corp.

- Northrop Grumman Corp.

- Palantir Technologies Inc.

- QinetiQ Ltd.

- Rheinmetall AG

- RTX Corp.

- Saab AB

- Textron Systems

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Military sensor fusion market

- In May 2025, L3Harris Technologies and Thales Group launched development of a combined short-range air defense system designed to counter emerging aerial threats.

- In April 2025, L3Harris Technologies announced its advanced missile-tracking sensor, developed under the Hypersonic and Ballistic Tracking Space Sensor (HBTSS) initiative, reached maturity for full-rate production.

- In January 2025, Lockheed Martin Corp. secured a significant contract modification to upgrade the Aegis Combat System, enhancing its sensor fusion capabilities for multi-mission surface combatants.

- In November 2024, Northrop Grumman Corp. announced a successful demonstration of its Integrated Battle Command System (IBCS), showcasing enhanced sensor data fusion from multiple disparate systems in a complex, simulated threat environment.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Military Sensor Fusion Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 311 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.1% |

| Market growth 2026-2030 | USD 311775.6 thousand |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.7% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, Israel, UAE, Turkey, South Africa, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The military sensor fusion market is defined by the integration of sophisticated hardware and software to achieve dominance in multi-domain operations. Core technologies like active electronically scanned array (AESA) and phased-array radar are fundamental, providing the raw data for advanced processing.

- The strategic push towards joint all-domain command and control (JADC2) necessitates the fusion of inputs from electro-optical/infrared (EO/IR) systems, synthetic aperture radar (SAR), and electronic warfare (EW) support measures. This creates a unified common operating picture (COP), which is essential for modern battlefield management systems.

- A key boardroom-level consideration is the adoption of open systems architecture, which can reduce long-term sustainment costs by over 20% by enabling modular upgrades. The development of hypersonic and ballistic tracking capabilities, alongside cognitive radar systems, addresses emerging high-speed threats. For undersea warfare, combining acoustic sensor arrays with magnetic anomaly detectors (MAD) is critical.

- On land and in the air, the fusion of inertial measurement units (IMU) with quantum sensing technology ensures navigation resilience. This complex data synthesis, managed by powerful edge computing hardware and shared via tactical data links, is the cornerstone of future military superiority, involving platforms from unmanned aerial vehicle (UAV) swarms to autonomous underwater vehicles (AUV).

What are the Key Data Covered in this Military Sensor Fusion Market Research and Growth Report?

-

What is the expected growth of the Military Sensor Fusion Market between 2026 and 2030?

-

USD 311.78 million, at a CAGR of 6.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Platform (Airborne and space, Land-based, and Naval), Type (Radar, Electro optical and infrared, Electronic warfare, and Sonar), Application (ISR, Situational awareness, Target tracking, and Battlefield management) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for enhanced situational awareness across multi-domain operations, High costs associated with system integration and maintenance

-

-

Who are the major players in the Military Sensor Fusion Market?

-

ASELSAN AS, BAE Systems Plc, CACI International Inc., Elbit Systems Ltd., General Dynamics Corp., HENSOLDT AG, Indra Sistemas SA, Kongsberg Gruppen ASA, L3Harris Technologies Inc., Leidos Holdings Inc., Leonardo S.p.A., Lockheed Martin Corp., Northrop Grumman Corp., Palantir Technologies Inc., QinetiQ Ltd., Rheinmetall AG, RTX Corp., Saab AB, Textron Systems and The Boeing Co.

-

Market Research Insights

- The dynamics of the military sensor fusion market are shaped by the imperative for an information dominance strategy and command and control (C2) agility. The adoption of network-centric warfare principles has led to a 40% increase in demand for platforms with robust unmanned systems integration.

- Achieving enhanced situational awareness is paramount, with advanced fusion algorithms demonstrating a 60% improvement in threat classification accuracy in cluttered environments. This capability directly supports real-time decision support and reduces the cognitive load on operators by over 50%.

- While these systems are critical for operations in degraded visual environments and achieving electromagnetic spectrum dominance, ensuring robust cyber-resilient networks and effective interoperability standards across allied forces remain key focus areas for defense organizations.

We can help! Our analysts can customize this military sensor fusion market research report to meet your requirements.

RIA -

RIA -