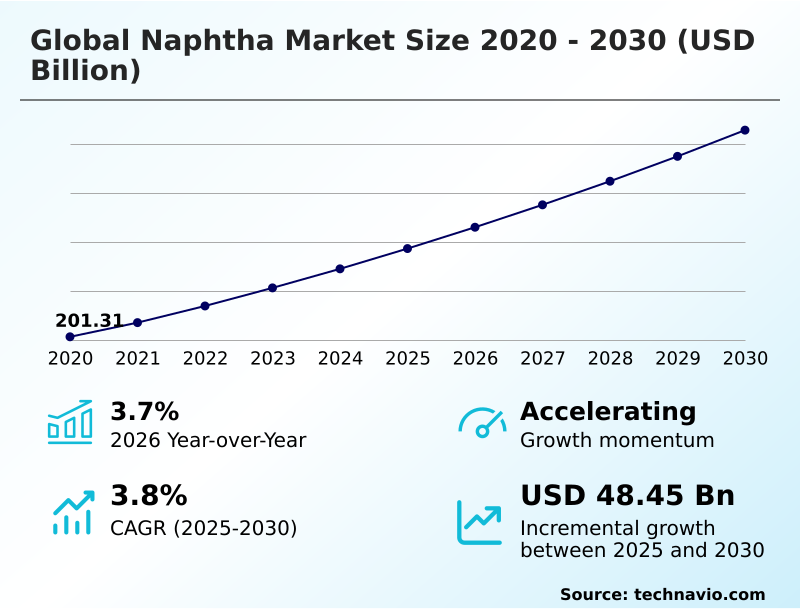

Naphtha Market Size 2026-2030

The naphtha market size is valued to increase by USD 48.45 billion, at a CAGR of 3.8% from 2025 to 2030. Increase in demand for naphtha in petrochemical industry will drive the naphtha market.

Major Market Trends & Insights

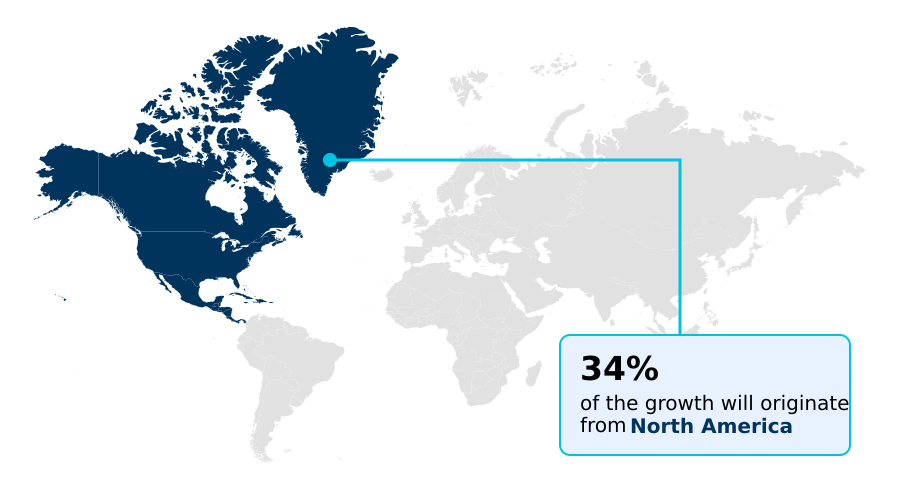

- North America dominated the market and accounted for a 34.5% growth during the forecast period.

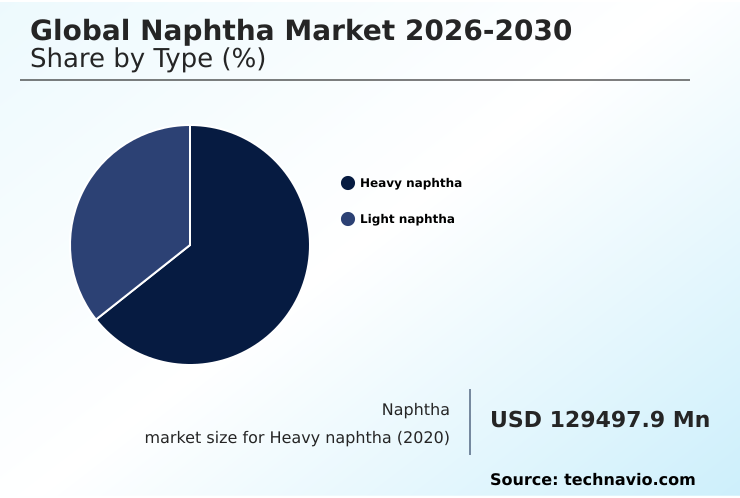

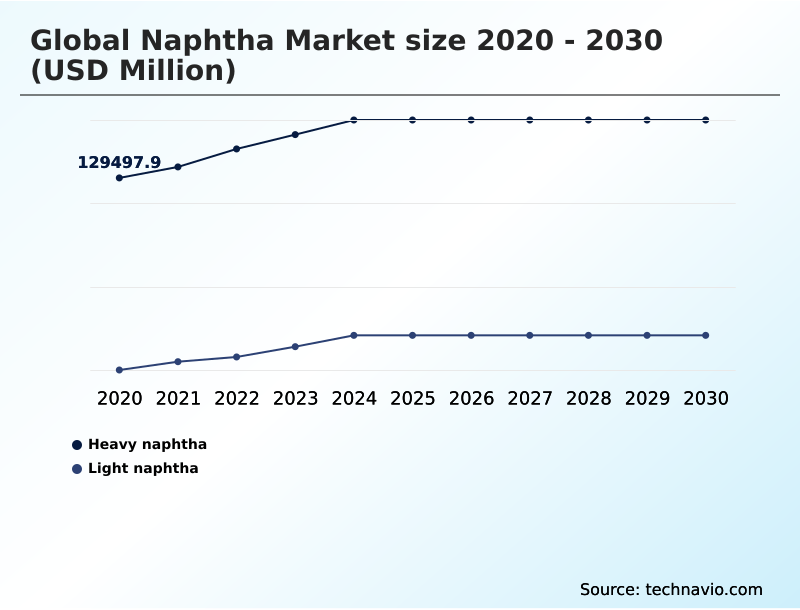

- By Type - Heavy naphtha segment was valued at USD 146.89 billion in 2024

- By Application - Chemicals segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 84.54 billion

- Market Future Opportunities: USD 48.45 billion

- CAGR from 2025 to 2030 : 3.8%

Market Summary

- The naphtha market serves as a critical link between upstream refining and downstream chemical manufacturing. Its primary role as a petrochemical feedstock for producing plastics, synthetic resins, and other derivatives underpins industrial activity. A dominant market driver is the sustained demand from the petrochemical sector, which is expanding capacity to meet consumer needs for lightweight materials and advanced polymers.

- Concurrently, a key trend is the strategic shift within refineries toward crude-to-chemicals configurations, maximizing naphtha yields over transportation fuels. This transition involves significant capital investment in advanced distillation and molecular conversion technologies. However, the industry faces challenges from stringent environmental regulations targeting emissions and the chemical composition of hydrocarbon streams.

- To navigate this landscape, a refiner might implement a predictive analytics platform. This system analyzes real-time data on feedstock quality and market prices, optimizing blending ratios for steam crackers to ensure consistent output and operational efficiency, thereby mitigating the impact of both feedstock variability and regulatory constraints while improving margins through enhanced process optimization and better feedstock reliability.

What will be the Size of the Naphtha Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Naphtha Market Segmented?

The naphtha industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Heavy naphtha

- Light naphtha

- Application

- Chemicals

- Energy or fuel

- Others

- End-user

- Petrochemicals

- Paints and coatings

- Agriculture

- Aerospace

- Others

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Type Insights

The heavy naphtha segment is estimated to witness significant growth during the forecast period.

The heavy naphtha segment is integral to the production of high-octane gasoline and key aromatic hydrocarbons. Its primary application is feedstock for catalytic reforming units, where the paraffin-naphthene-aromatic composition is transformed.

Modern refinery process control leverages AI-driven process optimization for this hydrocarbon stream processing, enhancing aromatics yield improvement. Through predictive maintenance systems and real-time process monitoring, operators can fine-tune reactor conditions, which extends the operational window before catalyst regeneration is required.

This digital transformation initiative and focus on refinery process integration allows refiners to maximize the output of high-value components, with some achieving an 8% improvement in aromatics yield while minimizing energy consumption, demonstrating a clear return on technology investment.

The Heavy naphtha segment was valued at USD 146.89 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Naphtha Market Demand is Rising in North America Get Free Sample

The geographic landscape of the market is primarily shaped by regional petrochemical demand and refining capabilities. APAC stands as the central demand hub, driven by massive petrochemical capacity expansion in countries like China and India.

This region's reliance on imports makes feedstock flexibility and naphtha blending optimization critical for managing costs and ensuring steam cracker efficiency.

North America is projected to capture 34.5% of the market's incremental growth, fueled by abundant natural gas condensates that provide a cost-advantaged source for light naphtha.

In Europe, the market is characterized by a strong focus on environmental compliance and process optimization to adhere to stringent emission standards.

AI-driven platforms have demonstrated the ability to improve production yields by 3-5% in some APAC refineries, highlighting the role of technology in maintaining competitiveness across diverse regional markets.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the market requires a holistic view of the entire value chain. The future of naphtha in energy transition is closely tied to its role in producing essential materials, making the economics of naphtha versus ethane cracking a central consideration for producers.

- Optimizing steam cracker naphtha feed is critical for profitability, especially when considering the naphtha price volatility business impact. Technologies for high purity naphtha output and hydrotreating processes for naphtha quality are essential for meeting the specifications of the petrochemical industry. The increasing aromatics from heavy naphtha via advanced heavy naphtha catalytic reforming process underpins the production of high-value chemicals.

- At the same time, managing benzene in naphtha streams and adhering to environmental regulations for naphtha storage are non-negotiable operational mandates. AI in naphtha refinery operations helps manage these complexities, from blending optimization for naphtha feedstock to navigating supply chain challenges in naphtha transport.

- The impact of shale gas on naphtha supply has reshaped regional dynamics, while emerging bio-based naphtha production pathways and circular economy models for naphtha offer a glimpse into a more sustainable future for light naphtha for ethylene production and its role in gasoline blending.

What are the key market drivers leading to the rise in the adoption of Naphtha Industry?

- The increasing demand for naphtha within the petrochemical industry, where it serves as a fundamental feedstock for producing vital olefins, is a key driver for market growth.

- Market growth is fundamentally driven by robust demand from the petrochemical industry for light naphtha as a primary petrochemical feedstock for olefin production.

- The global expansion of petrochemical capacity, particularly for ethylene and propylene, fuels the need for reliable inputs for steam cracking. This demand is amplified by the growing consumption of synthetic resins and advanced polymers in manufacturing sectors.

- Major integrated refining and chemical projects are being developed to create cost-effective basic chemicals and support synthetic resin manufacturing at scale. As a result, the steam cracking furnace remains a core asset, with petrochemical complexes designed to maximize conversion.

- The adoption of technologies like waste plastic pyrolysis also contributes by creating alternative feedstock streams, with some plants achieving a 70% conversion rate from plastic waste to liquid hydrocarbons.

What are the market trends shaping the Naphtha Industry?

- An increase in investment toward enhancing naphtha extraction is a significant market trend. This involves deploying advanced distillation technologies to maximize yields from diverse crude oil qualities.

- Key trends are reshaping the production landscape, driven by a strategic move toward crude-to-chemicals configurations. This approach prioritizes the output of chemical feedstock through advanced crude oil distillation and molecular conversion technologies. Refiners are making significant investments in refining infrastructure upgrades, integrating sophisticated hydrotreaters and distillation technologies to achieve a high purity output of specialty aromatics and ensure feedstock reliability.

- The development of sustainable biofuel production is also introducing bio-based naphtha variants and circular renewable naphtha into the supply chain. These innovations in feedstock recovery efficiency enhance operational resilience, with advanced processing units improving feedstock-to-chemical conversion rates by up to 10%, creating a more flexible and profitable operating model.

What challenges does the Naphtha Industry face during its growth?

- Stringent regulations governing the usage, handling, and chemical composition of naphtha present a key challenge affecting the industry's operational landscape and growth.

- The market faces significant challenges from an increasingly stringent regulatory environment. The enforcement of industrial emissions standards and rules on volatile organic compounds necessitates substantial investment in vapor recovery units and advanced emission control techniques. Mandates on benzene content and feedstock composition require precise management of hydrocarbon streams, adding complexity to atmospheric distillation processes.

- Furthermore, the push for decarbonization of cracking processes introduces cost pressures, as compliance can increase operational expenses by up to 15%. Navigating the framework of toxic substances control and ensuring environmental compliance across jurisdictions has become a critical operational hurdle for producers of this flammable hydrocarbon.

- Consequently, operators are leveraging smart refinery projects and advanced demand forecasting models to optimize production while managing these constraints.

Exclusive Technavio Analysis on Customer Landscape

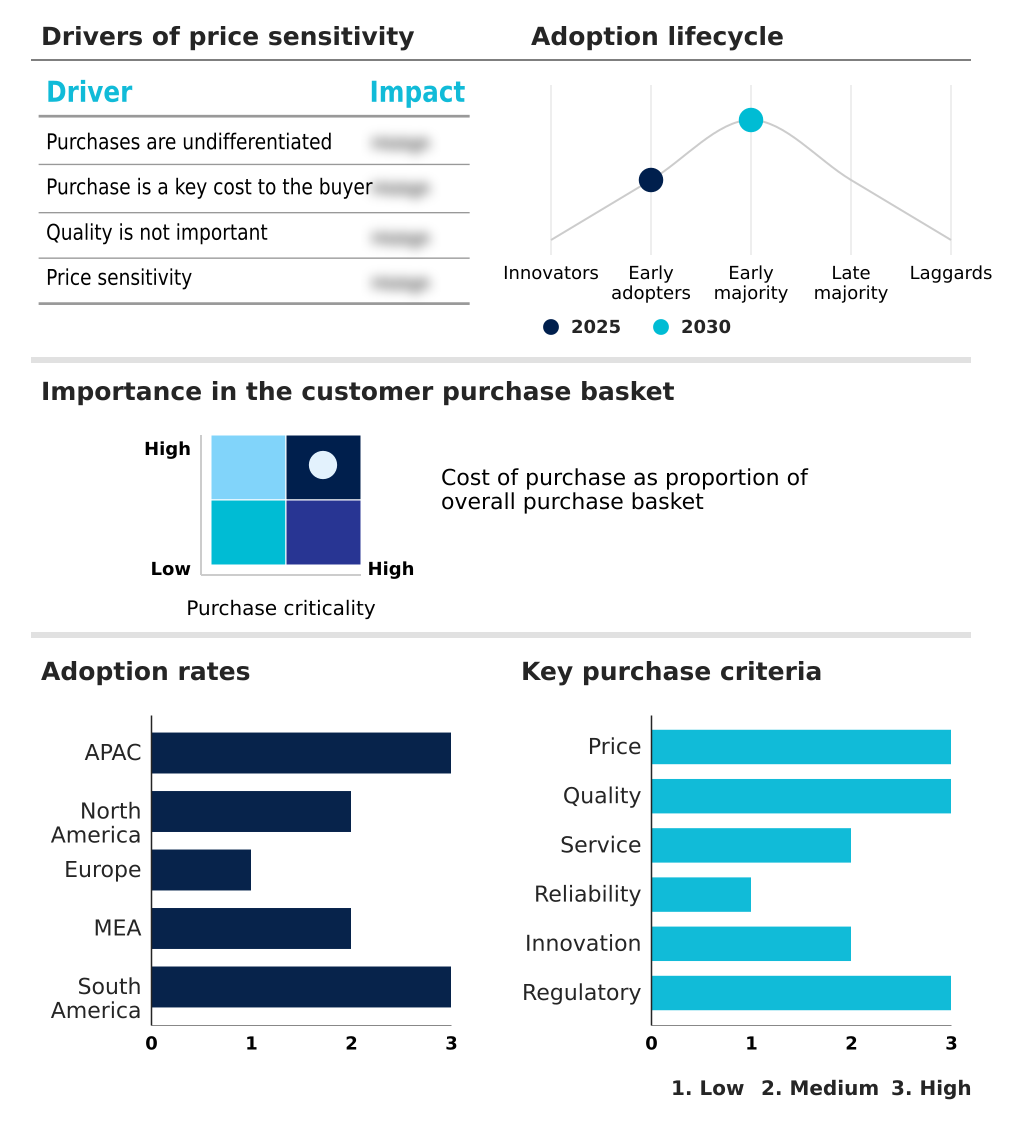

The naphtha market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the naphtha market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Naphtha Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, naphtha market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

2M Holdings Ltd. - Offers a diversified portfolio of chemical distribution services, including hydrocarbon solvents, sample management, and custom blending solutions for industrial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 2M Holdings Ltd.

- Alexandria Mineral Oils Co.

- Bajrang Petrochemicals Ltd.

- Chevron Corp.

- China Petrochemical Corp.

- Exxon Mobil Corp.

- Formosa Petrochemical Corp.

- Ganga Rasayanie Pvt. Ltd.

- Indian Oil Corp. Ltd.

- LG Chem Ltd.

- PAO NOVATEK

- Pyroplast Energy Ltd.

- Reliance Industries Ltd.

- Sasol Ltd.

- Saudi Arabian Oil Co.

- Shell plc

- The Mitsubishi Chemical Group

- TotalEnergies SE

- UPM Kymmene Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Naphtha market

- In January, 2025, the Yulong petrochemical complex commenced full commercial operations in China, a facility designed to process millions of tons of naphtha annually to produce high-value chemicals for the domestic manufacturing sector.

- In January, 2025, Saudi Aramco announced a multi-billion dollar investment to upgrade its refining infrastructure, focusing on integrating new molecular conversion technologies to increase the recovery rate of light naphtha from heavy crude oil grades.

- In January, 2025, the European Union's Industrial Emissions Directive entered its enhanced monitoring phase, mandating stricter controls on benzene and other aromatics in facilities processing naphtha, directly impacting refiners in Germany and The Netherlands.

- In October, 2024, Shell plc announced the successful deployment of an AI-driven process optimization system at its Pernis refinery, aiming to improve the efficiency and output of heavy naphtha distillation and reforming operations.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Naphtha Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 301 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.8% |

| Market growth 2026-2030 | USD 48449.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.7% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is defined by a strategic pivot where refiners are re-evaluating asset utilization and capital allocation. This shift is driven by the need to maximize value from every barrel of crude oil, favoring the production of chemical feedstock over traditional fuels. Key boardroom decisions now center on funding refining infrastructure upgrades that incorporate advanced molecular conversion and distillation technologies.

- These systems are essential for processing a wider range of hydrocarbon streams and achieving the high purity output required for specialty aromatics. Adherence to industrial emissions directives and managing benzene content have become critical operational mandates, compelling investment in vapor recovery units and advanced refinery process control.

- The adoption of AI-driven process optimization enables a more granular management of the flammable hydrocarbon, from crude oil distillation and natural gas condensates to the final petrochemical feedstock. By leveraging these technologies, facilities can improve cracking yields from specific paraffinic grades, extend the time between catalyst regeneration cycles, and ensure feedstock reliability.

- This approach, focused on enhancing feedstock composition, has enabled some operators to improve aromatics recovery by over 5%, demonstrating a clear path to maintaining competitiveness.

What are the Key Data Covered in this Naphtha Market Research and Growth Report?

-

What is the expected growth of the Naphtha Market between 2026 and 2030?

-

USD 48.45 billion, at a CAGR of 3.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Heavy naphtha, and Light naphtha), Application (Chemicals, Energy or fuel, and Others), End-user (Petrochemicals, Paints and coatings, Agriculture, Aerospace, and Others) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increase in demand for naphtha in petrochemical industry, Stringent regulations on usage of naphtha

-

-

Who are the major players in the Naphtha Market?

-

2M Holdings Ltd., Alexandria Mineral Oils Co., Bajrang Petrochemicals Ltd., Chevron Corp., China Petrochemical Corp., Exxon Mobil Corp., Formosa Petrochemical Corp., Ganga Rasayanie Pvt. Ltd., Indian Oil Corp. Ltd., LG Chem Ltd., PAO NOVATEK, Pyroplast Energy Ltd., Reliance Industries Ltd., Sasol Ltd., Saudi Arabian Oil Co., Shell plc, The Mitsubishi Chemical Group, TotalEnergies SE and UPM Kymmene Corp.

-

Market Research Insights

- Market dynamics are increasingly shaped by a strategic pivot toward high-value chemical production and operational excellence. This shift is driving investment in refining infrastructure upgrades and crude-to-chemicals configurations, with some operators improving feedstock recovery efficiency by over 12%.

- Advanced demand forecasting models and supply chain logistics platforms are being adopted to navigate price volatility, leading to a 15% reduction in inventory carrying costs. Furthermore, the focus on petrochemical capacity expansion is supported by digital transformation initiatives integrating the industrial internet of things for real-time process monitoring.

- These smart refinery projects enhance feedstock flexibility and steam cracker efficiency, enabling producers to maintain higher margins in a competitive environment where cost-effective basic chemicals are paramount.

We can help! Our analysts can customize this naphtha market research report to meet your requirements.

RIA -

RIA -