Needle-Free Injection Systems Market Size 2024-2028

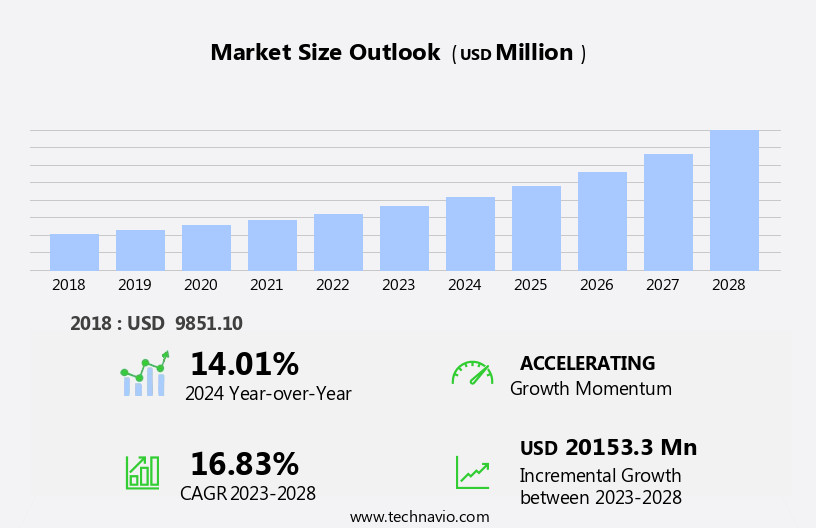

The needle-free injection systems market size is forecast to increase by USD 20.15 billion, at a CAGR of 16.83% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing preference for minimally invasive medical procedures, particularly in biopsies. This trend is driven by the desire to reduce patient discomfort and improve overall healthcare efficiency. Another key factor fueling market expansion is the rising incidence of needlestick infections, which pose a significant risk to healthcare workers and patients alike. However, the market faces challenges from stringent regulations on medical devices, which necessitate rigorous testing and certification processes. These regulations ensure the safety and efficacy of needle-free injection systems but add to the cost and time required to bring new products to market.

- Companies seeking to capitalize on market opportunities must navigate these regulatory hurdles while also addressing the evolving needs of healthcare providers and patients. Effective collaboration with regulatory bodies and continuous innovation in needle-free technology will be essential for market success.

What will be the Size of the Needle-Free Injection Systems Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in bioavailability enhancement and innovative delivery methods. These systems, which include disposable injectors, self-injection devices, and jet injectors, offer advantages such as improved patient compliance, reduced injection site reactions, and painless administration. The market encompasses various sectors, including vaccine delivery, pharmaceutical injection, and transdermal drug applications. Bioavailability enhancement is a significant focus, with micro-needle arrays and electromechanical actuators enabling targeted drug delivery and optimizing injection depth and volume. Portable injectors and wearable devices add to the market's dynamism, providing convenience and ease of use. Automated injection systems streamline processes, ensuring consistent injection rates and reducing human error.

Painless injection technologies, such as high-pressure jet injectors and solid jets, are gaining popularity due to their ability to penetrate the skin without the need for needles. Dermal delivery and cosmetic applications are also growing sectors, with needle-free injectors offering localized drug delivery and enhanced drug stability. The power source and injection rate are crucial factors in the development of these systems, with ongoing research focusing on improving efficiency and reducing costs. Injection site reactions, drug absorption rate, and patient compliance remain key challenges in the market. Continuous advancements in technology aim to address these issues, ensuring the market's ongoing growth and evolution.

How is this Needle-Free Injection Systems Industry segmented?

The needle-free injection systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Hospitals and clinics

- Home care settings

- Research laboratories

- Product

- Fillable

- Pre-filled

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

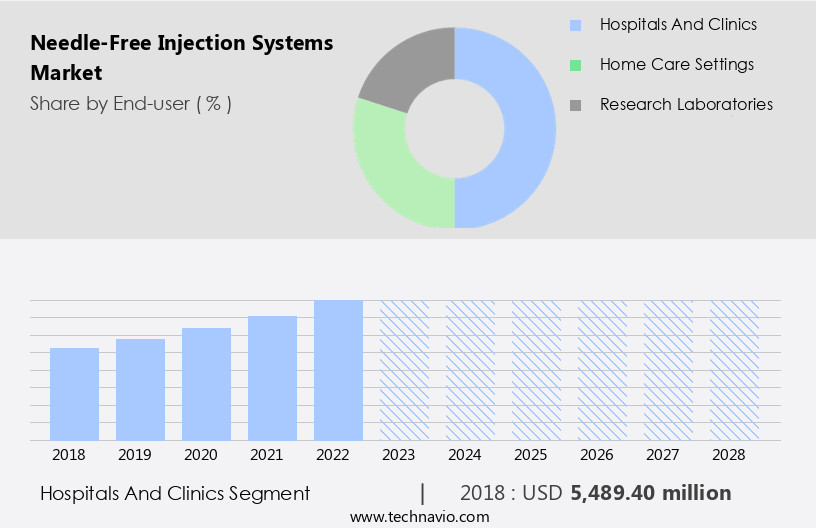

By End-user Insights

The hospitals and clinics segment is estimated to witness significant growth during the forecast period.

Needle-free injection systems have gained significant traction in the healthcare industry, particularly in hospitals and clinics, which collectively hold a substantial market share. These systems offer numerous advantages, including painless injection, improved patient compliance, and precise drug dosing, making them increasingly popular among healthcare professionals. The use of needle-free injection systems is prevalent in hospitals for administering vaccines, anticoagulants, biologics, and various pharmaceutical drugs. The convenience and ease of use of these systems have led to a shift from conventional needles and syringes for drug delivery. Clinics and privately operated healthcare facilities prioritize patient care and convenience.

They focus on offering diagnostic, therapeutic, or preventive healthcare treatments to outpatients. Needle-free injection systems, with their ability to ensure accurate drug delivery and minimize injection site reactions, are a preferred choice for these facilities. Technological advancements in needle-free injection systems include micro-needle arrays, electromechanical actuators, and high-pressure injection systems, which enhance drug absorption rate, bioavailability, and localized drug delivery. Portable and wearable injectors further expand the application scope of these systems, offering added convenience and flexibility. Pneumatic and solid jet injection technologies ensure drug stability during delivery. Overall, the market is driven by the growing demand for painless, accurate, and convenient drug delivery methods.

The Hospitals and clinics segment was valued at USD 5.49 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

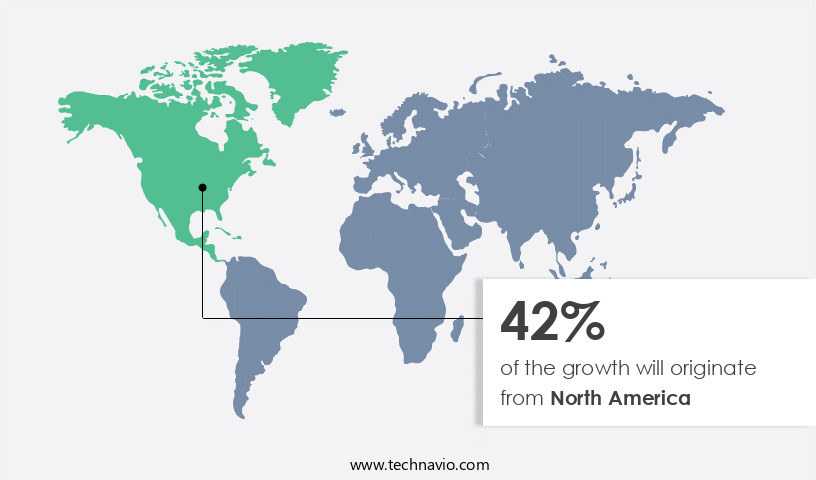

North America is estimated to contribute 42% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in the US is experiencing significant growth due to several factors. The widespread availability of insurance coverage and reimbursements, increasing research and development expenditure, a growing geriatric population with chronic diseases, and the demand for self-administered drugs are key drivers. According to NCBI data, approximately six million needlestick injuries occur annually in the US, leading to the adoption of needle-free injection systems for safety reasons. Advanced medical facilities in states like Indiana, Ohio, and Illinois are also fueling market growth. These systems, including disposable injectors, self-injection devices, and jet injectors, offer advantages such as painless injection, improved patient compliance, and reduced injection site reactions.

Technologies like micro-needle arrays, transdermal drugs, and targeted drug delivery enhance bioavailability and drug stability. Portable injectors and wearable injectors provide convenience, while high-pressure injection and electromechanical actuators ensure accurate injection rates and skin penetration. The market is expected to continue growing due to the increasing focus on painless and automated injection systems, as well as the development of solid jet and localized drug delivery technologies.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Needle-Free Injection Systems Industry?

- The growing demand for minimally invasive biopsy procedures is the primary market driver, reflecting a significant trend towards less invasive diagnostic methods in healthcare.

- Needle-Free Injection Systems have gained significant attention in the pharmaceutical industry as an alternative to traditional injection methods. These systems offer several advantages, including reduced pain, elimination of needles, and minimized risk of cross-contamination. The disposable injector technology in these systems ensures hygiene and safety, making them ideal for vaccine delivery and self-injection devices. The injection depth and pressure are critical factors in ensuring effective drug delivery and optimal drug absorption rate. Pressure injection systems use compressed air or gas to propel the drug into the skin, ensuring consistent and accurate dosing. In contrast, pharmaceutical injection systems rely on syringes and needles for drug administration.

- Needle-Free Injection Systems have the potential to revolutionize drug delivery systems, particularly in the context of self-administration. They offer a more immersive and harmonious experience for patients, reducing the emphasis on invasive procedures and the associated complications, such as bruising, swelling, bleeding, and infections. The market dynamics of Needle-Free Injection Systems are driven by several factors, including the increasing prevalence of chronic diseases, the growing demand for painless and non-invasive drug delivery methods, and the advancements in technology. These factors are expected to fuel the growth of the market in the coming years. In conclusion, Needle-Free Injection Systems represent a promising solution for pharmaceutical companies and healthcare professionals looking to improve drug delivery and patient experience.

- With their ability to offer painless, non-invasive, and hygienic drug administration, these systems are poised to transform the drug delivery landscape.

What are the market trends shaping the Needle-Free Injection Systems Industry?

- The rising prevalence of needlestick infections represents a significant trend in the healthcare industry. This issue warrants increased attention and innovation in the development of safer medical devices to mitigate the risk of such infections.

- Needle-free injection systems have emerged as a promising alternative to traditional syringe injections in the healthcare industry. These systems utilize technologies such as micro-needle arrays, jet injection, and liquid jets for transdermal drug delivery. The primary advantage of needle-free injectors is the elimination of needles, thereby reducing the risk of cross-contamination and infection. Poor healthcare practices, such as the use of reused or contaminated needles, have resulted in the transmission of infectious diseases, including hepatitis B, hepatitis C, and HIV. Moreover, needle-free injectors offer enhanced patient compliance due to their painless and non-invasive nature. They also minimize the risk of injection site reactions, such as swelling, pain, rash, redness, or bleeding.

- The market dynamics for needle-free injection systems are driven by the growing demand for safe and effective drug delivery systems, the increasing prevalence of chronic diseases, and the rising focus on patient-centric care. The use of needle-free injectors is expected to increase significantly in the coming years due to their numerous benefits and the growing awareness of patient safety.

What challenges does the Needle-Free Injection Systems Industry face during its growth?

- The stringent regulations governing the medical device industry pose a significant challenge to its growth.

- The market is subject to rigorous regulations due to past product recalls and regulatory challenges. The US Food and Drug Administration (FDA) classifies medical devices, including needle-free injection systems, into three categories based on risk levels. Class I devices have the lowest risk, while Class III devices undergo the most extensive scrutiny. Clinical trials are mandatory for marketing approval, which is a lengthy, costly, and uncertain process. A failed clinical trial may result in the rejection of marketing authorization. These stringent regulations ensure the safety and efficacy of needle-free injection systems, which are used for various applications, such as bioavailability enhancement, cosmetic injections, and dermal delivery.

- Portable injectors, automated injection, painless injection, and electromechanical actuators are essential features of these systems. Despite the challenges, the market continues to grow due to the advantages offered by needle-free injection systems, such as reduced injection site reactions and improved patient experience.

Exclusive Customer Landscape

The needle-free injection systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the needle-free injection systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, needle-free injection systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aijex Pharma International Inc. - The company pioneers needle-free injection technology with innovative solutions like Injex 50, revolutionizing the healthcare industry by enhancing patient comfort and convenience while ensuring efficient drug delivery.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aijex Pharma International Inc.

- AKRA DERMOJET

- Amico Group

- ANTARES PHARMA INC.

- Becton Dickinson and Co.

- Crossject

- Endo International Plc

- Ferring BV

- Inovio Pharmaceuticals Inc.

- Lepu Medical Technology Beijing Co. Ltd.

- Medbitz Pte Ltd.

- Mika Medical Co.

- Needle Free Injection System

- NuGen Medical Devices

- PharmaJet Inc.

- PORTAL INSTRUMENTS INC

- QUINOVARE and TECHiJET

- Recipharm AB

- Technologies Médicales Internationales Inc.

- West Pharmaceutical Services Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Needle-Free Injection Systems Market

- In January 2024, Becton, Dickinson and Company (BD), a leading medical technology company, announced the launch of its new BD Prolatech AutoJect 2 Needle-Free Injection System, designed for use in hospitals and clinics. This system offers improved patient comfort and reduced waste, making it a significant advancement in needle-free technology (BD press release).

- In March 2024, Pfizer and Valero Medical Technologies, a leading needle-free injection systems manufacturer, entered into a strategic collaboration to develop and commercialize Pfizer's vaccines using Valero's needle-free technology. This partnership aimed to enhance vaccine delivery and administration efficiency (Pfizer press release).

- In May 2024, Gerresheimer AG, a global partner for pharma and healthcare, acquired the needle-free injection systems business of Nemera, a French pharmaceutical services provider. This acquisition expanded Gerresheimer's portfolio in the market and strengthened its position in the pharmaceutical industry (Gerresheimer press release).

- In February 2025, the European Medicines Agency (EMA) granted marketing authorization for the use of the Microsafe NanoJet Needle-Free Injection System, manufactured by Merck KGaA, for the administration of certain vaccines. This approval marked a significant milestone for needle-free injection systems in Europe and increased market potential for the technology (Merck KGaA press release).

Research Analyst Overview

- The market is witnessing significant advancements in technology, driven by the need for safer, more comfortable, and efficient drug delivery solutions. These systems employ various manufacturing processes to ensure product lifecycle management, from sterilization method selection to skin integrity testing and dose accuracy assessment. Safety is a top priority, with rigorous clinical trials conducted to evaluate drug efficacy, injection pain reduction, and patient safety. Skin integrity and material compatibility are crucial factors, as are system reliability, durability testing, and injection mechanism design. The user interface plays a vital role in ensuring ease of use for long-term applications.

- Regulatory approval processes are stringent, requiring extensive performance testing, system automation, and quality control measures. Microfluidic devices are gaining popularity due to their efficiency and minimal tissue damage. Injection speed, system maintenance, and drug formulation compatibility are essential considerations in the development of these devices. Dose accuracy and drug potency are critical factors in maintaining patient safety and ensuring optimal therapeutic outcomes. Safety testing and injection pain reduction are key trends, with needle-free systems offering potential benefits for patients and healthcare providers alike. The market is focused on improving system efficiency, durability, and user experience while adhering to regulatory requirements and ensuring optimal drug delivery.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Needle-Free Injection Systems Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

153 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 16.83% |

|

Market growth 2024-2028 |

USD 20153.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

14.01 |

|

Key countries |

US, Germany, China, UK, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Needle-Free Injection Systems Market Research and Growth Report?

- CAGR of the Needle-Free Injection Systems industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the needle-free injection systems market growth of industry companies

We can help! Our analysts can customize this needle-free injection systems market research report to meet your requirements.

RIA -

RIA -