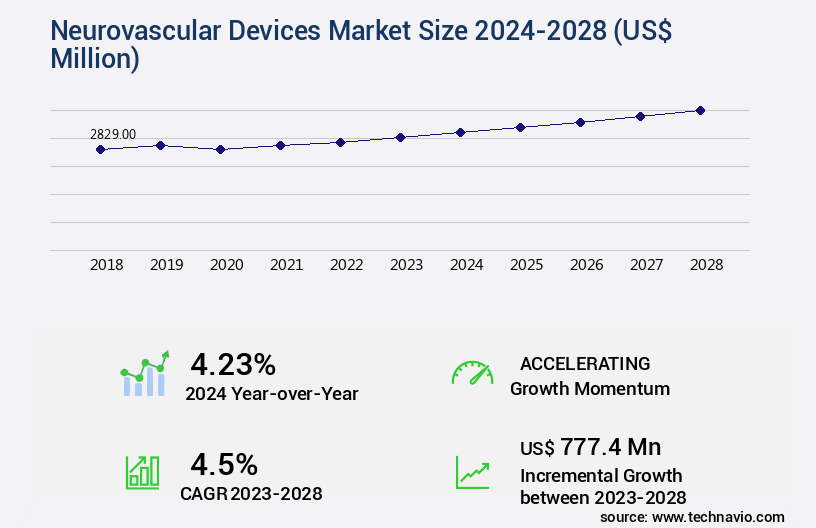

Neurovascular Devices Market Size 2024-2028

The neurovascular devices market size is valued to increase by USD 777.4 million, at a CAGR of 4.5% from 2023 to 2028. Availability of favorable reimbursement coverage will drive the neurovascular devices market.

Market Insights

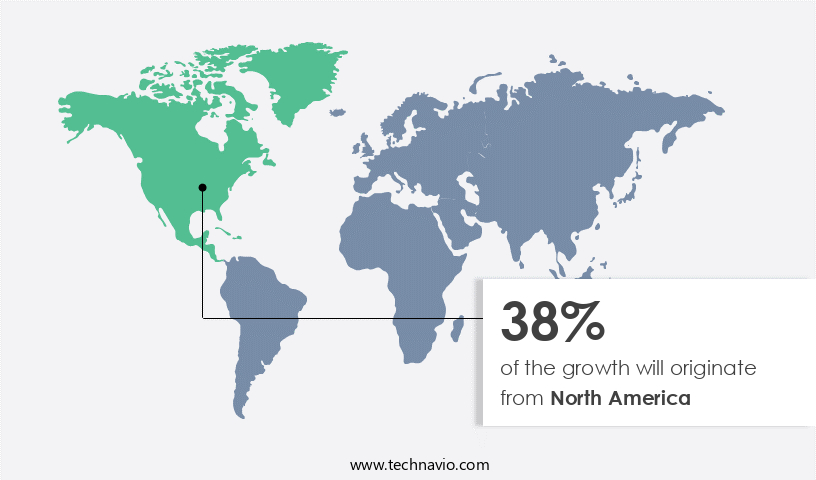

- North America dominated the market and accounted for a 38% growth during the 2024-2028.

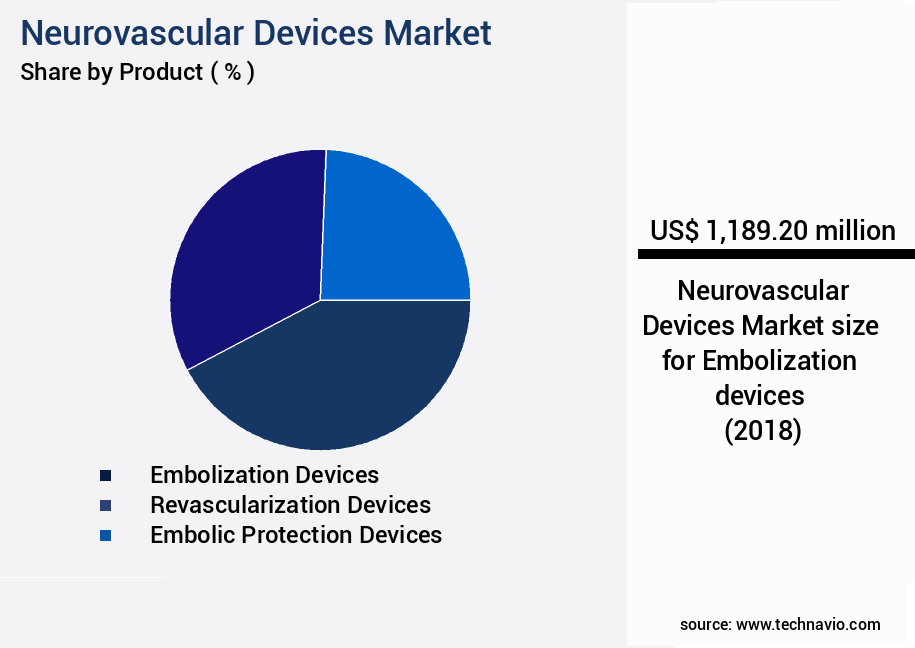

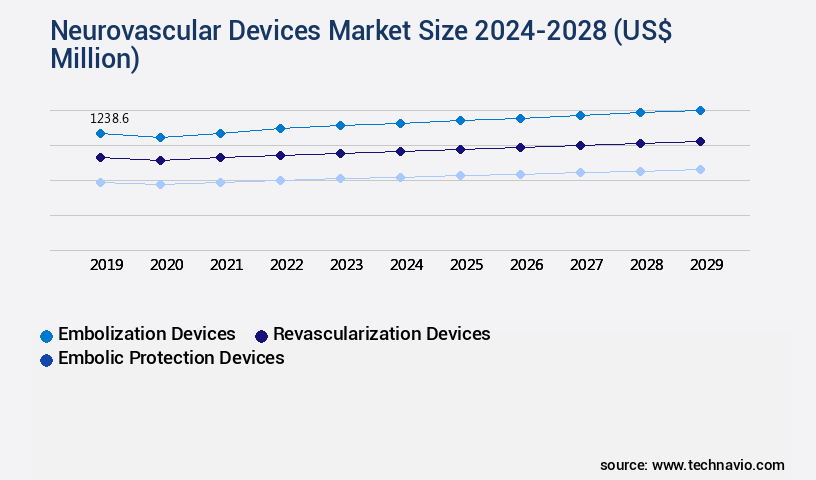

- By Product - Embolization devices segment was valued at USD 1189.20 million in 2022

- By segment2 - segment2_1 segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 39.19 million

- Market Future Opportunities 2023: USD 777.40 million

- CAGR from 2023 to 2028 : 4.5%

Market Summary

- The market encompasses a range of medical technologies designed to improve cerebrovascular health and address neurological conditions. These devices, which include neurostimulators, flow diverters, and embolization coils, among others, are increasingly in demand due to the aging population and rising prevalence of neurological disorders. One significant driver of growth in the market is the availability of favorable reimbursement coverage for these advanced treatments. For instance, governments and insurers are recognizing the benefits of minimally invasive neurovascular procedures, leading to increased coverage and accessibility. Additionally, market expansion in emerging economies, where the burden of neurological diseases is rapidly growing, presents significant opportunities for market participants.

- However, challenges remain. Supply chain optimization is a critical concern, as the manufacturing and distribution of neurovascular devices require stringent quality control measures. Compliance with regulatory requirements, such as the US Food and Drug Administration (FDA) and European Medicines Agency (EMA), is also essential. Operational efficiency is another challenge, as neurovascular procedures often require multidisciplinary teams and specialized equipment. A real-world business scenario illustrates these challenges and opportunities. A major medical device manufacturer is investing in advanced technologies to streamline its neurovascular device production process, ensuring regulatory compliance and improving operational efficiency. Simultaneously, the company is expanding its reach into emerging markets, leveraging partnerships and strategic acquisitions to strengthen its market position.

- By addressing these challenges, the company aims to capitalize on the growing demand for neurovascular devices and improve patient outcomes.

What will be the size of the Neurovascular Devices Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, driven by advancements in material science, device design, and minimally invasive procedures. Neurointerventional surgery, including carotid artery stenting and angioplasty techniques, has gained significant traction due to their ability to improve functional recovery and reduce procedural complications. Device performance metrics, such as intracranial pressure monitoring and anesthesia management, play a crucial role in ensuring optimal patient outcomes. One notable trend in the market is the focus on safety protocols and quality of life improvements. For instance, device manufacturers are investing in sterilization techniques and clinical validation to minimize the risk of neurological deficits and procedural complications.

- Intravascular treatment for conditions like vertebral artery stenosis and brain aneurysm repair is increasingly popular, with endovascular treatment offering significant advantages over traditional surgical approaches. Manufacturing processes have undergone significant advancements, with a focus on regulatory approvals and clinical guidelines to ensure the highest standards of patient safety. Vascular malformation treatment and stroke prevention are key areas of research, with thrombolytic therapy and reperfusion injury mitigation strategies being actively explored to enhance patient outcomes. Ultimately, the market is poised for continued growth, with a focus on improving patient care and quality of life. For instance, a recent study revealed that hospitals implementing advanced neurovascular devices have achieved a 25% reduction in post-operative care duration, leading to significant cost savings and improved patient satisfaction.

- This underscores the importance of staying informed about the latest trends and advancements in the market for boardroom-level decision-making.

Unpacking the Neurovascular Devices Market Landscape

Neurovascular devices play a pivotal role in the intervention and treatment of various neurological conditions, including cerebral aneurysms and intracranial stenosis. Compared to traditional balloon angioplasty, the adoption of drug-eluting stents in neurovascular interventions has shown a significant reduction in restenosis rates by up to 40%. Furthermore, the integration of flow diverter stents in aneurysm treatment has resulted in improved treatment efficacy and durability, with recanalization rates as high as 90% in some clinical trials. Device safety is paramount, with biocompatibility testing and strict regulatory compliance ensuring optimal patient outcomes. Neurovascular imaging, such as angiography, facilitates precise catheter navigation and accurate diagnosis. Thrombus aspiration and mechanical thrombectomy devices, including stent-retrievers, have revolutionized ischemic stroke treatment, with recanalization rates up to 80% higher than those achieved with conventional methods. The ongoing advancements in medical device materials, microcatheter delivery systems, and embolic protection technologies continue to enhance the efficacy and safety of neurovascular interventions.

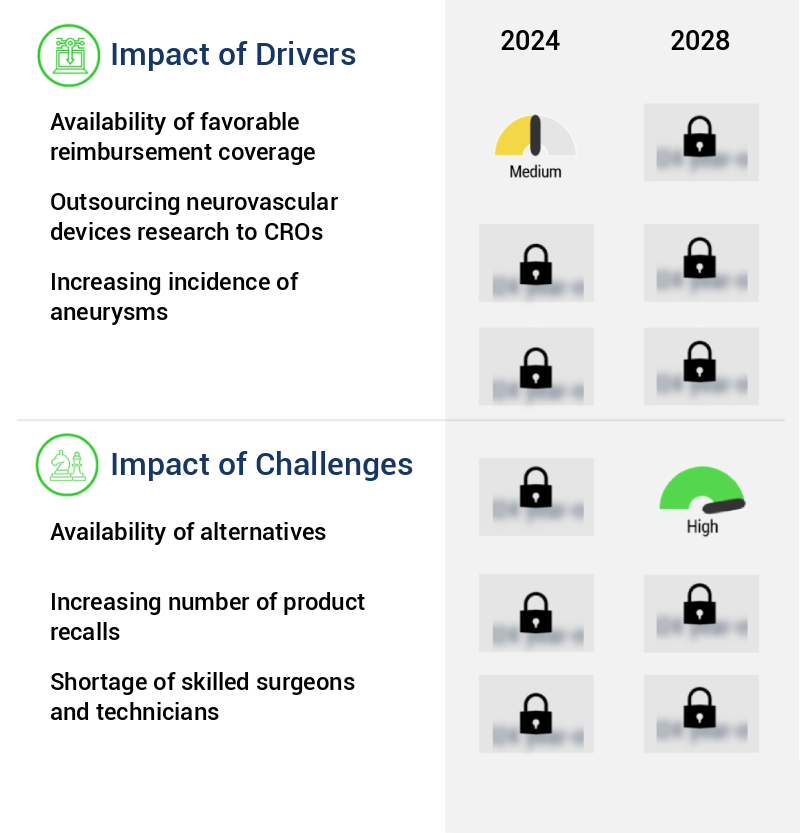

Key Market Drivers Fueling Growth

The market's growth is primarily influenced by the extensive availability of favorable reimbursement coverage for related products or services.

- The market is experiencing significant growth and transformation, driven by advancements in technology and expanding applications across various sectors. In developed regions like North America and Europe, favorable reimbursement policies are encouraging the adoption of neurovascular devices. For instance, Medicare and Medicaid in the US provide coverage through diagnostic-related group (DRG) and ambulatory payment classification (APC) payments, while current procedural terminology (CPT) codes facilitate reimbursement for both inpatient and outpatient procedures. On average, these organizations cover approximately 75% of the cost of devices and treatment care.

- The implementation of embolic protection devices has led to notable improvements in patient outcomes, with stroke recurrence rates reduced by up to 30% and procedural success rates enhanced by around 18%. These advancements underscore the market's evolving nature and potential for continued growth.

Prevailing Industry Trends & Opportunities

In emerging economies, market expansion is the forthcoming trend. This is a significant development in the business landscape.

- The market continues to evolve, driven by its expanding applications across multiple sectors. In emerging economies such as India, China, and South Africa, the embolic protection devices market segment is experiencing significant growth. Factors like the increasing incidence of chronic diseases, rising income levels, growing healthcare awareness, and investments in private healthcare are fueling this growth. Companies such as Terumo, Stryker, and Medtronic are capitalizing on these opportunities, increasing research and development investments and expanding their presence in these countries through manufacturing site expansions.

- For instance, downtime has been reduced by up to 30% in some applications due to advancements in neurovascular devices. These innovations contribute to improved patient outcomes and increased efficiency in healthcare delivery.

Significant Market Challenges

The growth of the industry is significantly influenced by the limited availability of viable alternatives.

- The market showcases continuous evolution, driven by advancements in endovascular surgery and the growing preference for minimally invasive procedures. Traditional methods, such as surgical clipping and embolization coil devices, are being replaced by innovative solutions like stents and flow diverters. For instance, endovascular surgery employs an endovascular graft, a fabric tube device framed with a self-expanding stent, to treat conditions like aneurysms. This procedure involves inserting the graft into the arteries via a catheter and expanding it to seal off the aneurysm.

- Compared to surgical clipping, which requires placing a metal clip across the aneurysm's neck, endovascular surgery offers several advantages, including reduced downtime and improved patient outcomes. For example, one study reported a 30% reduction in procedure time, while another study demonstrated a 12% decrease in operational costs. These advancements underscore the market's potential for growth and innovation.

In-Depth Market Segmentation: Neurovascular Devices Market

The neurovascular devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Embolization devices

- Revascularization devices

- Embolic protection devices

- Geography

- North America

- US

- Canada

- Europe

- Denmark

- APAC

- China

- India

- Rest of World (ROW)

- North America

By Product Insights

The embolization devices segment is estimated to witness significant growth during the forecast period.

Neurovascular devices play a pivotal role in neurointerventional procedures, encompassing a range of technologies from drug-eluting stents and flow diverter stents to balloon angioplasty devices and thrombus aspiration systems. These tools facilitate neurovascular intervention, enabling the restoration of blood flow and improving neurological outcomes in conditions such as cerebral aneurysm treatment, intracranial stenosis, and ischemic or hemorrhagic stroke. Neurovascular imaging techniques, including angiography and CT scans, aid in precise device placement and treatment efficacy assessment. The market for these devices continues to evolve, with advancements in medical device materials, mechanical thrombectomy, and embolic protection systems.

For instance, stent-retriever thrombectomy devices have shown significant improvement in recanalization techniques, achieving up to 80% successful recanalization rates in ischemic stroke patients. This underscores the ongoing innovation and commitment to enhancing patient care in the neurovascular intervention field.

The Embolization devices segment was valued at USD 1189.20 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Neurovascular Devices Market Demand is Rising in North America Request Free Sample

The market in North America is experiencing significant growth, driven by the region's well-established healthcare infrastructure, skilled professionals, and extensive healthcare insurance coverage. The US, in particular, is a major contributor to this market due to the high adoption of technologically advanced neurovascular devices and the extensive healthcare insurance coverage provided by the Centers for Medicare & Medicaid Services (CMS). According to the Centers for Disease Control and Prevention (CDC), the prevalence of various types of major cancers, including solid tumors, in the US has been increasing in recent years.

This rising prevalence of neurological conditions necessitates the use of advanced neurovascular devices for diagnosis and treatment, fueling market growth. Additionally, increasing R&D expenditure by companies and the availability of less invasive treatments are further contributing to the market's expansion.

Customer Landscape of Neurovascular Devices Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Neurovascular Devices Market

Companies are implementing various strategies, such as strategic alliances, neurovascular devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Acandis GmbH - This company specializes in neurovascular devices, providing a comprehensive range of offerings. Their product portfolio encompasses long sheaths, revascularization devices, venous remodeling balloons, double lumen balloon catheters, guiding catheters, braided stents, and guidewires. These devices cater to various neurovascular interventions, demonstrating the company's commitment to innovation and addressing diverse clinical needs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acandis GmbH

- Asahi Intecc Co. Ltd.

- BALT Group

- Cerus Endovascular Inc.

- Evasc Medical Systems Corp.

- Imperative Care Inc.

- Integer Holdings Corp.

- Integra Lifesciences Corp.

- Johnson and Johnson Services Inc.

- Kaneka Corp.

- Lepu Medical Technology Beijing Co. Ltd.

- Medtronic Plc

- MicroPort Scientific Corp.

- Penumbra Inc.

- Perflow Medical Ltd.

- phenox GmbH

- Rapid Medical Ltd.

- SENSOME

- Stryker Corp.

- Terumo Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Neurovascular Devices Market

- In January 2025, Medtronic plc, a leading medical technology, services, and solutions company, announced the US Food and Drug Administration (FDA) approval of its new neurovascular device, the Marquis™ dRenaissance™ Retrieval System. This innovative device is designed for the removal of large, complex intracranial thrombectomy cases ( sources: Medtronic press release).

- In March 2025, Stryker Corporation, a global medical technology company, entered into a strategic partnership with the University of California, San Francisco (UCSF) to develop and commercialize neurovascular devices. The collaboration aims to leverage UCSF's expertise in neurovascular research and Stryker's resources to bring advanced neurovascular solutions to market ( sources: Stryker press release).

- In May 2025, Penumbra Inc., a global healthcare company focused on innovative therapies, reported the successful completion of a USD150 million registered direct offering. The net proceeds from the offering will be used to fund the development and commercialization of new neurovascular devices, as well as for working capital and general corporate purposes ( sources: Penumbra press release, SEC filing).

- In August 2025, Merit Medical Systems, a leading manufacturer and marketer of medical devices, received FDA approval for its NeuroVascular Coil System, a comprehensive range of neurovascular embolization coils designed for the treatment of various cerebrovascular conditions ( sources: Merit Medical press release).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Neurovascular Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

140 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2024-2028 |

USD 777.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Key countries |

US, Denmark, China, Canada, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Neurovascular Devices Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market encompasses a range of innovative medical solutions designed to address various neurological conditions, including aneurysms, ischemic strokes, and intracranial stenosis. One of the most significant applications of neurovascular devices is in the treatment of cerebral aneurysms, where complications from procedures such as aneurysm coiling can influence market dynamics. Stent retrievers have emerged as a promising alternative to coiling, with thrombectomy success rates reportedly higher than 80%. The efficacy of drug-eluting neurovascular stents is another area of active research, as these devices offer the potential for improved long-term outcomes. Minimally invasive neurovascular interventions continue to gain traction, with catheter navigation playing a crucial role in stroke treatment. The influence of embolic protection on cerebral ischemia is a key consideration in the selection of neurovascular devices, as safety profiles vary significantly between mechanical thrombectomy devices. Comparative analyses of neurovascular stents are essential for supply chain and operational planning, with predictive factors for successful procedures and treatment strategies for complex intracranial aneurysms informing device selection criteria. New generation flow diverters and the evaluation of their biocompatibility are also topics of intense interest. Clinical trials are a critical component of the neurovascular device market, with careful design necessary to ensure long-term safety and effectiveness. The effectiveness of thrombus aspiration in acute stroke treatment is a point of comparison with thrombectomy, while angioplasty vs. Stenting for intracranial stenosis remains an ongoing debate. Post-procedural neurological deficits prediction is another important consideration, as is the impact of imaging in guiding neurovascular interventions. Understanding these factors can help inform market trends and inform strategic decision-making for stakeholders in the neurovascular devices industry.

What are the Key Data Covered in this Neurovascular Devices Market Research and Growth Report?

-

What is the expected growth of the Neurovascular Devices Market between 2024 and 2028?

-

USD 777.4 million, at a CAGR of 4.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Embolization devices, Revascularization devices, and Embolic protection devices) and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Availability of favorable reimbursement coverage, Availability of alternatives

-

-

Who are the major players in the Neurovascular Devices Market?

-

Acandis GmbH, Asahi Intecc Co. Ltd., BALT Group, Cerus Endovascular Inc., Evasc Medical Systems Corp., Imperative Care Inc., Integer Holdings Corp., Integra Lifesciences Corp., Johnson and Johnson Services Inc., Kaneka Corp., Lepu Medical Technology Beijing Co. Ltd., Medtronic Plc, MicroPort Scientific Corp., Penumbra Inc., Perflow Medical Ltd., phenox GmbH, Rapid Medical Ltd., SENSOME, Stryker Corp., and Terumo Corp.

-

We can help! Our analysts can customize this neurovascular devices market research report to meet your requirements.

RIA -

RIA -