Oil and Gas Pipeline and Transportation Automation Market Size 2024-2028

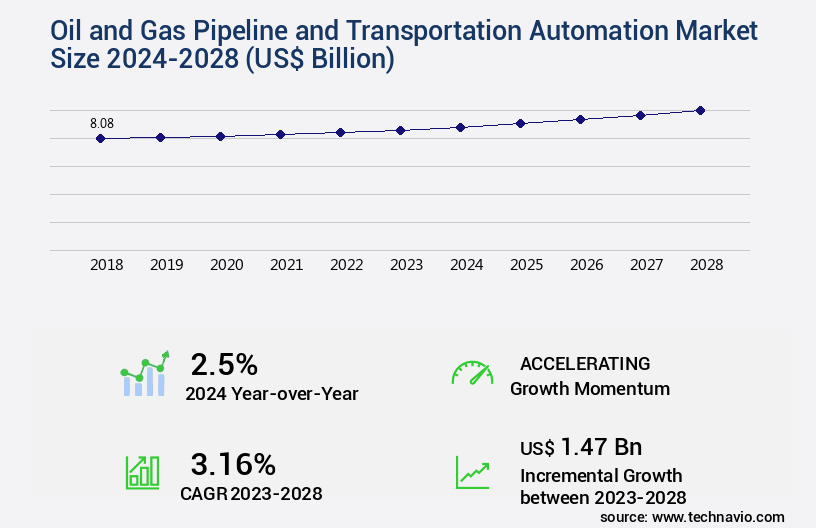

The oil and gas pipeline and transportation automation market size is valued to increase USD 1.47 billion, at a CAGR of 3.16% from 2023 to 2028. Growing expansion of oil terminals will drive the oil and gas pipeline and transportation automation market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 30% growth during the forecast period.

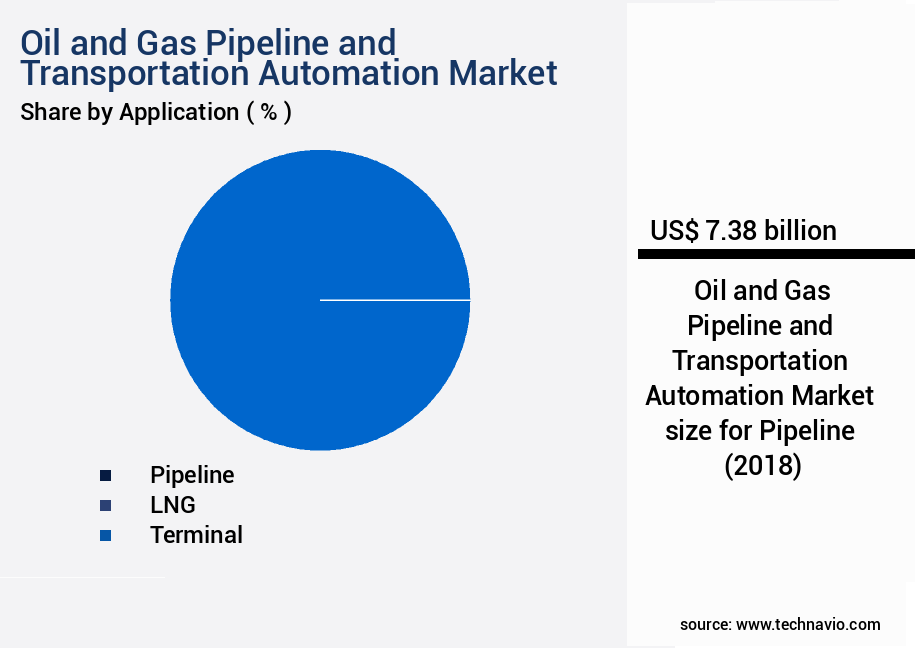

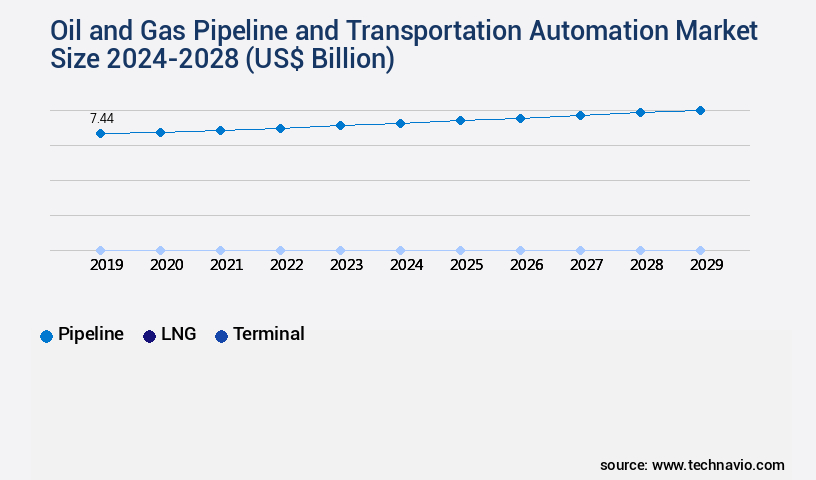

- By Application - Pipeline segment was valued at USD 7.38 billion in 2022

- By Solution - SCADA segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 26.04 billion

- Market Future Opportunities: USD 1.47 billion

- CAGR from 2023 to 2028 : 3.16%

Market Summary

- The market is experiencing significant growth, with a reported value of USD12.5 billion in 2020. This expansion is driven by the increasing adoption of Internet of Things (IoT) technology in midstream oil and gas operations. By automating pipeline monitoring and transportation processes, companies can enhance efficiency, reduce costs, and improve safety. The integration of advanced analytics and machine learning algorithms into pipeline management systems enables real-time monitoring of pipeline performance and predictive maintenance. This proactive approach to maintenance reduces downtime and minimizes the risk of costly repairs or environmental incidents. Moreover, the use of drones and remote sensing technologies for pipeline inspections further enhances the market's functionality.

- These technologies allow for non-destructive testing and real-time data collection, reducing the need for manual inspections and improving overall operational efficiency. Despite these advancements, challenges persist. Cybersecurity concerns and the high cost of implementing and maintaining automation systems remain significant barriers to entry for some companies. However, as technology continues to evolve and costs decrease, the market is poised for continued growth. In conclusion, the market is a dynamic and evolving industry, driven by technological advancements and the need for increased operational efficiency. With a reported value of USD12.5 billion in 2020, this market is expected to grow as companies continue to adopt automation technologies to improve pipeline performance, reduce costs, and enhance safety.

What will be the Size of the Oil and Gas Pipeline and Transportation Automation Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Oil and Gas Pipeline and Transportation Automation Market Segmented ?

The oil and gas pipeline and transportation automation industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Pipeline

- LNG

- terminal

- Solution

- SCADA

- DCS

- PLC

- Geography

- North America

- US

- Canada

- Europe

- Russia

- APAC

- China

- Rest of World (ROW)

- North America

By Application Insights

The pipeline segment is estimated to witness significant growth during the forecast period.

Pipelines play a pivotal role in the oil and gas midstream sector, serving as the preferred choice for transporting vast quantities of fluids. These intricate systems are subjected to rigorous performance metrics, including flow rate optimization, throughput capacity increase, and pressure monitoring. Pipeline infrastructure caters to diverse operating environments and a range of fluids, from crude oil and natural gas to refined products and liquefied gases. With the ongoing evolution of pipeline technology, automation has become a cornerstone, integrating predictive maintenance models, automated valve control, and pipeline stress analysis for enhanced pipeline safety. Distributed control systems, pipeline risk assessment, and operational efficiency metrics are essential components of pipeline management, ensuring regulatory compliance and cost reduction.

Pipeline simulation software, corrosion detection methods, and regulatory compliance audits are integral to maintaining pipeline integrity. Smart pipeline technology, real-time pipeline control, and flow assurance strategies enable efficient pigging operations scheduling and effective leak detection. SCADA system integration, data acquisition systems, pipeline material selection, automated pipeline welding, pipeline network optimization, and emergency shutdown systems are all crucial elements of pipeline infrastructure. According to recent reports, the global oil and gas pipeline automation market is projected to grow at a CAGR of 5.5% between 2021 and 2026, underscoring the continuous advancements in pipeline technology.

The Pipeline segment was valued at USD 7.38 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 30% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Oil and Gas Pipeline and Transportation Automation Market Demand is Rising in APAC Request Free Sample

North America, as the second-largest consumer of crude oil globally, is home to significant demand for fuel in the United States, Canada, and Mexico. The high production costs of oil and gas and the extensive utilization of advanced oilfield technologies, including transportation automation, position North America as a leading regional market for oil and gas pipeline and transportation automation. Notable companies in this sector include Emerson Electric Co.

And Honeywell International Inc. The market's growth can be attributed to increasing investments in offshore fields in the Gulf of Mexico.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to the increasing demand for advanced pipeline monitoring and optimization solutions. This market encompasses a range of technologies, including real-time pipeline monitoring systems, automated pipeline pigging optimization, predictive modeling for pipeline maintenance, and data-driven pipeline operational efficiency. Geographic information systems pipeline mapping plays a crucial role in improving pipeline throughput capacity and ensuring pipeline integrity. By integrating SCADA systems for pipeline management, pipeline integrity management software solutions can provide remote pipeline valve control technology and advanced pipeline corrosion detection techniques. High-pressure pipeline design and safety are paramount, and pipeline risk assessment and mitigation strategies are essential for effective pipeline asset management. Implementing pipeline automation systems is a key trend in this market, with a focus on optimizing pipeline maintenance scheduling and minimizing operational risks. Advanced pipeline control system architecture and pipeline sensor network deployment strategies are essential for ensuring regulatory compliance and improving pipeline safety. Predictive modeling and data analytics are also becoming increasingly important for pipeline operators, enabling them to make informed decisions about pipeline maintenance and operations. In summary, the market is undergoing a transformation, driven by the need for advanced pipeline monitoring, optimization, and safety solutions. From real-time pipeline monitoring to predictive modeling and advanced pipeline control systems, these technologies are helping pipeline operators improve efficiency, reduce risks, and ensure regulatory compliance.

What are the key market drivers leading to the rise in the adoption of Oil and Gas Pipeline and Transportation Automation Industry?

- The expanding growth of oil terminals serves as the primary catalyst for market expansion.

- Oil terminals play a pivotal role in the oil and gas supply chain, facilitating the storage of crude oil and petroleum products while serving as hubs for transportation. The escalating global energy demand has fueled an increase in new oil terminal and pipeline constructions, particularly in Asia-Pacific and Africa, where the continuous energy requirement calls for new infrastructure. Notable developments include Saudi Aramco's expansion of its partnership program, Aramco Namaat, with 22 new Memorandums of Understanding (MoUs) and one joint venture agreement focusing on advanced materials, technology, industrial and energy services, and sustainability (Saudi Aramco, 2021).

- In addition, India's petroleum regulator granted approval for the expansion of its natural gas pipeline network by 33,764 km, extending the country's gas grid (Petroleum and Natural Gas Regulatory Board, 2021). These projects underscore the ongoing investment in oil and gas infrastructure to meet the evolving energy landscape.

What are the market trends shaping the Oil and Gas Pipeline and Transportation Automation Industry?

- The increasing adoption of IoT in midstream oil and gas operations represents a significant market trend. This technological advancement is transforming the sector by enhancing operational efficiency and productivity.

- The oil and gas midstream sector has undergone significant shifts in recent years, serving as a critical link between demand and supply centers while optimizing the oil and gas supply chain. The sector's transformation gained momentum following the 2015 crude oil price downturn, which compelled numerous companies to reconsider their investments in upstream projects. In response to the price decrease, firms prioritized cost reduction and adopted advanced technologies. One pressing concern in the midstream sector is reliability, encompassing pipeline and transportation automation. According to industry insights, the sector's focus on technology integration has led to substantial improvements in efficiency and operational resilience.

- Moreover, the integration of data analytics and machine learning algorithms has enabled predictive maintenance, minimizing downtime and enhancing overall performance. This data-driven approach to midstream operations is expected to continue evolving, further optimizing the oil and gas supply chain and addressing the challenges posed by fluctuating market conditions.

What challenges does the Oil and Gas Pipeline and Transportation Automation Industry face during its growth?

- The expansion of alternative energy sources' utilization poses a significant challenge to the industry's growth trajectory.

- The global oil and gas industry is experiencing significant shifts due to escalating investments in various alternative energy sources. Renewable energy sectors, including solar, geothermal, small hydroelectric, biofuels/bioenergy, and nuclear/thermal energy, are gaining traction. This trend is driven by environmental concerns, geopolitical risks, and the desire to reduce energy dependence on a single source. According to industry reports, the adoption of oil and gas pipeline and transportation automation technologies is increasing to optimize operational efficiency and reduce costs. However, these investments in automation are not enough to offset the declining demand for traditional energy sources.

- The energy landscape is evolving, with countries prioritizing energy diversification and sustainability over reliance on oil and gas. This shift is expected to continue, with renewable energy sources poised to capture a larger market share in the coming years.

Exclusive Technavio Analysis on Customer Landscape

The oil and gas pipeline and transportation automation market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the oil and gas pipeline and transportation automation market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Oil and Gas Pipeline and Transportation Automation Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, oil and gas pipeline and transportation automation market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - This company specializes in automation technologies for oil and gas pipeline and transportation operations. Their offerings include Distributed Control Systems, Operations Management Software, and SCADAvantage. These solutions enhance efficiency, safety, and productivity in the energy sector through advanced technology applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Andritz AG

- Azbil Corp.

- Beckhoff Automation GmbH and Co. KG

- Eaton Corp. Plc

- Emerson Electric Co.

- Endress Hauser Group Services AG

- FANUC Corp.

- Furukawa Electric Co. Ltd.

- Honeywell International Inc.

- INTECH Process Automation Inc.

- Mitsubishi Electric Corp.

- OMRON Corp.

- Robert Bosch GmbH

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Toshiba Corp.

- Valmet Corp.

- Yokogawa Electric Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Oil And Gas Pipeline And Transportation Automation Market

- In January 2024, Emerson Electric Company, a leading automation technology and engineering firm, announced the launch of its new Ovation MECS Control System for oil and gas pipelines, designed to optimize process control and improve safety (Emerson Electric Company Press Release, 2024).

- In March 2024, Honeywell International Inc. And Schneider Electric signed a strategic collaboration agreement to integrate Honeywell's Uniformance PHD and Experion Process Knowledge System with Schneider Electric's EcoStruxure for Oil & Gas, enhancing their combined offerings in pipeline automation (Honeywell International Inc. Press Release, 2024).

- In May 2024, ABB Ltd. Secured a USD100 million contract from Saudi Aramco to provide automation and electrical systems for the Marjan and Berri offshore oil fields, expanding its presence in the Middle East oil and gas sector (ABB Ltd. Press Release, 2024).

- In February 2025, the U.S. Department of Transportation's Pipeline and Hazardous Materials Safety Administration (PHMSA) approved the use of advanced automation technologies, including artificial intelligence and machine learning, for pipeline leak detection and response, promoting increased safety and efficiency in pipeline operations (U.S. Department of Transportation Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Oil and Gas Pipeline and Transportation Automation Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

180 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.16% |

|

Market growth 2024-2028 |

USD 1.47 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

2.5 |

|

Key countries |

US, Canada, Saudi Arabia, China, and Russia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The oil and gas pipeline and transportation market continues to evolve, driven by the need for increased throughput capacity, improved operational efficiency, and enhanced safety regulations. Flow rate optimization and predictive maintenance models are key areas of focus, with automated valve control and pipeline compression playing crucial roles in maximizing throughput. Pressure monitoring sensors and pipeline stress analysis are essential components of pipeline safety regulations, while distributed control systems enable real-time pipeline control and flow assurance strategies. Pipeline risk assessment and operational efficiency metrics are critical for pipeline integrity management and cost reduction. Pipeline simulation software and corrosion detection methods help optimize pipeline network design and selection of pipeline materials.

- Automated pipeline welding and SCADA system integration are essential for pipeline asset management and hydraulics pipeline design. Geographic information systems and emergency shutdown systems are integral to remote pipeline monitoring and regulatory compliance audits. Smart pipeline technology and real-time pipeline control are transforming the industry, with a growing emphasis on leak detection technology and pipeline inspection tools. The market is expected to grow at a robust rate, with industry experts projecting a 10% annual increase in pipeline transportation demand. For instance, a leading oil and gas company implemented a flow assurance strategy using pipeline simulation software, resulting in a 15% increase in pipeline throughput and a 12% reduction in maintenance costs.

- This demonstrates the significant impact of technology and automation on pipeline operations and the industry as a whole.

What are the Key Data Covered in this Oil and Gas Pipeline and Transportation Automation Market Research and Growth Report?

-

What is the expected growth of the Oil and Gas Pipeline and Transportation Automation Market between 2024 and 2028?

-

USD 1.47 billion, at a CAGR of 3.16%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Pipeline, LNG, and terminal), Solution (SCADA, DCS, and PLC), and Geography (North America, APAC, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Growing expansion of oil terminals, Increasing use of alternative energy sources

-

-

Who are the major players in the Oil and Gas Pipeline and Transportation Automation Market?

-

ABB Ltd., Andritz AG, Azbil Corp., Beckhoff Automation GmbH and Co. KG, Eaton Corp. Plc, Emerson Electric Co., Endress Hauser Group Services AG, FANUC Corp., Furukawa Electric Co. Ltd., Honeywell International Inc., INTECH Process Automation Inc., Mitsubishi Electric Corp., OMRON Corp., Robert Bosch GmbH, Rockwell Automation Inc., Schneider Electric SE, Siemens AG, Toshiba Corp., Valmet Corp., and Yokogawa Electric Corp.

-

Market Research Insights

- The market is a dynamic and ever-evolving industry, driven by the constant need to enhance operational efficiency and ensure pipeline integrity. Two key areas of focus are pipeline risk management and control system automation. Pipeline risk management incorporates various technologies such as pipeline integrity assessment, operational risk management, control valve automation, real-time data visualization, and automated pipeline operations. For instance, machine learning algorithms are used to analyze historical data and predict potential failures, allowing for preventive maintenance and reducing the risk of costly downtime. Moreover, the industry is expected to grow at a significant pace, with industry experts projecting a 15% compound annual growth rate over the next five years.

- This growth is attributed to the increasing adoption of advanced technologies like predictive maintenance analytics, maintenance scheduling software, and digital twin technology, which enable more efficient and effective pipeline operations. An example of the impact of these technologies can be seen in a major pipeline operator, which experienced a 20% reduction in maintenance costs after implementing a data analytics platform and remote monitoring dashboard system. This allowed for real-time monitoring of pipeline performance and proactive identification of potential issues, resulting in fewer unscheduled shutdowns and reduced maintenance expenses.

We can help! Our analysts can customize this oil and gas pipeline and transportation automation market research report to meet your requirements.

RIA -

RIA -