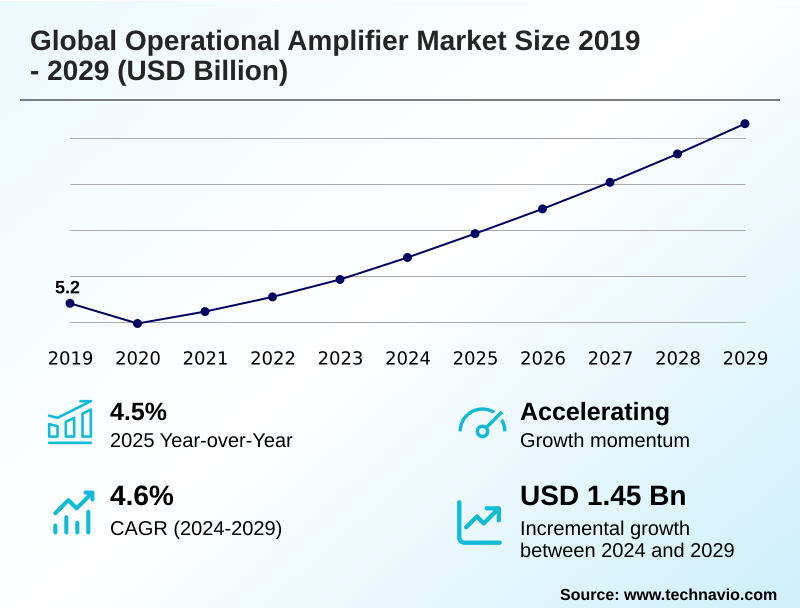

Operational Amplifier Market Size 2025-2029

The operational amplifier market size is valued to increase by USD 1.45 billion, at a CAGR of 4.6% from 2024 to 2029. Proliferation of Internet of Things and connected devices will drive the operational amplifier market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 39.1% growth during the forecast period.

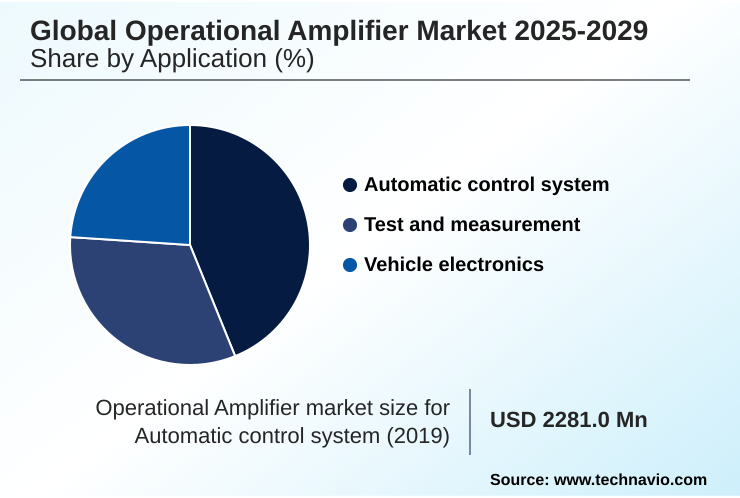

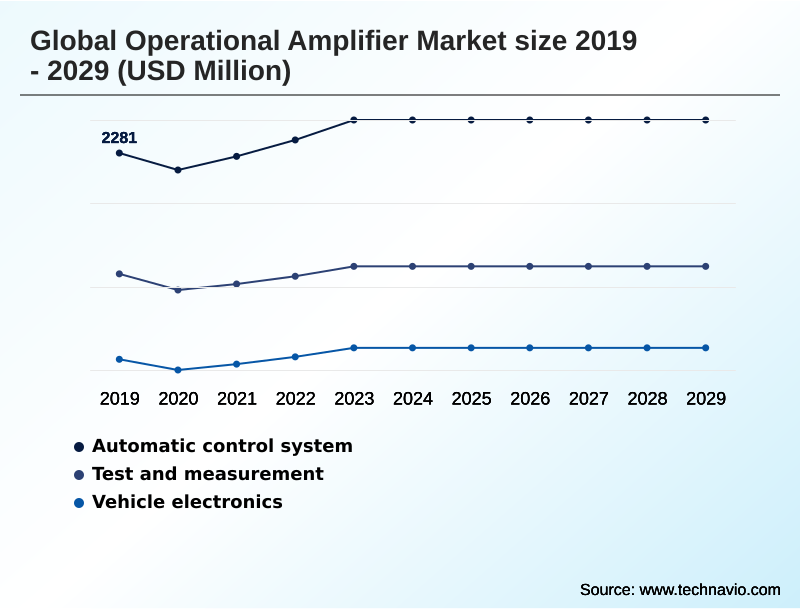

- By Application - Automatic control system segment was valued at USD 2.45 billion in 2023

- By Type - General-purpose segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.95 billion

- Market Future Opportunities: USD 1.45 billion

- CAGR from 2024 to 2029 : 4.6%

Market Summary

- The Operational Amplifier Market is foundational to modern electronics, serving as the critical interface between real-world analog signals and digital processing. Growth is fueled by the relentless expansion of industrial process control, the proliferation of advanced driver-assistance systems (ADAS) in the automotive sector, and the sheer volume of sensors deployed in IoT networks.

- A key trend is the bifurcation of the market into high-volume, general-purpose components and highly specialized devices, such as the zero-drift amplifier, engineered for specific high-performance applications.

- For instance, an OEM developing a portable medical device must navigate complex design trade-offs, balancing the need for low quiescent current to maximize battery life against the requirement for low voltage noise density to ensure the diagnostic accuracy of a high-impedance sensor interface. This scenario highlights the core tension in the market, where innovation in analog front-end design is critical.

- However, the persistent threat of system-on-chip integration, which can cannibalize the market for discrete components, remains a significant strategic challenge for manufacturers who must continuously demonstrate value through superior performance in areas like high gain-bandwidth product and AEC-Q100 qualified component reliability.

What will be the Size of the Operational Amplifier Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Operational Amplifier Market Segmented?

The operational amplifier industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Automatic control system

- Test and measurement

- Vehicle electronics

- Type

- General-purpose

- Precision

- High-speed

- Low-noise

- Others

- End-user

- Consumer electronics

- Automotive

- Healthcare

- Aerospace and defense

- Others

- Product type

- Open-loop

- Closed-loop

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- UAE

- Saudi Arabia

- Rest of World (ROW)

- APAC

By Application Insights

The automatic control system segment is estimated to witness significant growth during the forecast period.

The automatic control system segment relies on components that ensure high-fidelity analog signal conditioning in demanding industrial environments.

These devices are fundamental to the industrial control loop within a programmable logic controller (PLC) and are crucial for robotics control system stability.

Designs incorporate active filter implementation to reduce noise and leverage a negative feedback network between the inverting input terminal and output.

Performance is defined by high common-mode rejection and low input bias current, critical for applications from industrial process control to automated test equipment (ATE).

For instance, advanced designs for strain gauge signal conditioning in a source measure unit (SMU) can achieve signal deviation reductions of up to 15%, enhancing process reliability through superior schmitt trigger circuit performance.

The Automatic control system segment was valued at USD 2.45 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 39.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Operational Amplifier Market Demand is Rising in APAC Get Free Sample

The market's geographic landscape reflects a split between volume and value. While APAC commands the largest share of incremental growth at 39.1% due to high-volume electronics manufacturing, the North American market is expanding nearly 25% faster, driven by high-value sectors.

These regions prioritize different performance metrics; for instance, North American demand in high-speed data acquisition (DAQ) and medical imaging front-end systems focuses on fast slew rate and short settling time.

In contrast, European industrial applications for grid monitoring infrastructure and solar inverter control demand minimal input offset voltage and superior differential voltage amplification.

This specialization is also seen in the components themselves, such as a voltage-to-current converter for industrial controls or a low current noise density amplifier for a spectrum analyzer front-end, with smart grid energy management applications pushing requirements for both precision and robustness.

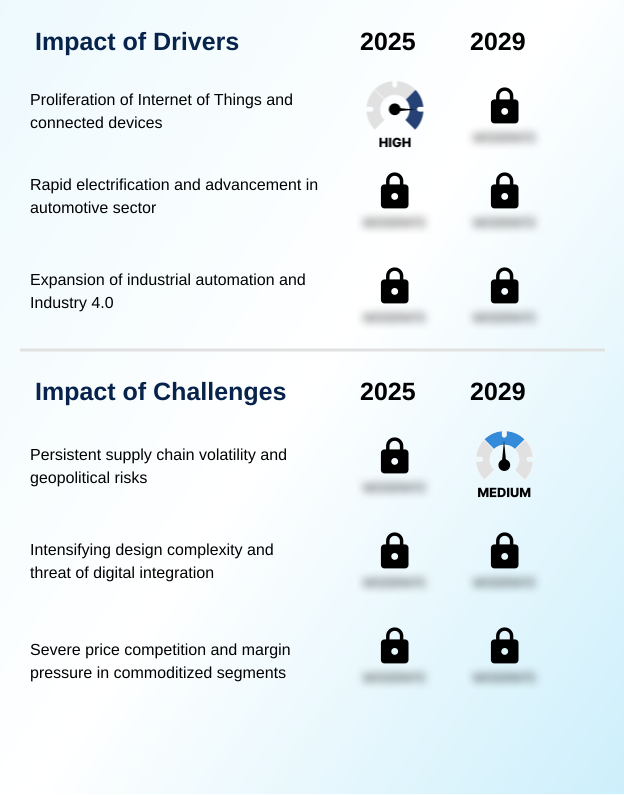

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The market's expansion is driven by the diverse requirements of modern electronics, compelling a move toward application-specific solutions. For consumer products, a low noise op-amp for audio is essential for high-fidelity sound, whereas portable gadgets demand a micropower op-amp for battery devices to extend operational life.

- In the industrial sector, the need for a high voltage op-amp for industrial applications is growing with the adoption of 48V systems, while a general purpose cost effective op-amp remains a staple for less critical functions.

- The automotive industry is a key driver, requiring a robust automotive grade op-amp for ADAS and an AEC-Q100 qualified automotive op-amp for all safety-critical systems. Telecommunications progress depends on a high speed op-amp for 5G, with a high slew rate video amplifier serving related media applications.

- Medical and scientific fields push performance boundaries, using a precision op-amp for medical devices and a chopper stabilized amplifier for instrumentation to ensure accuracy. The adoption of a fast settling data acquisition amplifier over a standard part can improve system throughput by over 15%, directly impacting operational efficiency.

- Specialized needs are met by a zero drift amplifier for sensors, a radiation hardened op-amp for space, and a rail-to-rail op-amp for single supply systems.

- Further niche applications use a low bias current FET input op-amp, a wide bandwidth differential amplifier, a high common mode rejection amplifier, a low distortion audio op-amp, and a programmable gain instrumentation amplifier to meet precise functional goals.

What are the key market drivers leading to the rise in the adoption of Operational Amplifier Industry?

- A primary driver for the operational amplifier market is the exponential proliferation of Internet of Things (IoT) devices, which require analog components for sensor signal conditioning.

- The market's momentum is strongly linked to the electrification of the automotive sector and the expansion of smart factory automation.

- The need for an AEC-Q100 qualified component is now standard in any electric vehicle powertrain, where precision current sensing is critical for efficiency.

- The use of a zero-drift amplifier in battery management system (BMS) applications improves state-of-charge accuracy by up to 5%, directly enhancing vehicle range.

- In industrial settings, advanced analog front-end design is integral to LiDAR sensor signal processing and the overall success of advanced driver-assistance systems (ADAS).

- This industrial push, coupled with the build-out of 5G telecommunications infrastructure, drives demand for components with a high gain-bandwidth product, which defines their ability to process high-frequency signals from the non-inverting input terminal and inverting input terminal with minimal distortion.

What are the market trends shaping the Operational Amplifier Industry?

- A dominant trend shaping the operational amplifier market is the persistent drive toward component miniaturization. This is coupled with an intense focus on enhancing power efficiency to meet the demands of battery-powered and portable devices.

- A dominant trend is the bifurcation toward specialized components, driven by miniaturization and power efficiency. The adoption of advanced WLCSP packaging and DFN package format technologies has reduced component footprints by up to 40%, enabling denser designs for devices like a wearable health monitor.

- Concurrently, the push for energy efficiency has yielded devices with a low quiescent current, with some components consuming 60% less power than standard parts. This is critical for any single-supply system operation, where maximizing battery life is paramount.

- Innovations like the chopper-stabilized amplifier and designs with a low 1/f noise corner cater to the high-impedance sensor interface market, including professional audio preamplifier and photodiode amplifier circuit designs. This trend toward rail-to-rail input output capability is now standard in portable diagnostic tool and ultrasound imaging system applications.

What challenges does the Operational Amplifier Industry face during its growth?

- Persistent supply chain volatility, compounded by geopolitical risks, presents a formidable challenge to the stability and growth of the operational amplifier market.

- Persistent supply chain vulnerabilities and the inexorable trend toward digital integration present significant hurdles. Component lead times have surged by over 200% for certain device families, disrupting production schedules for systems requiring a radiation-hardened component for avionics flight control or a specialized part for an electronic warfare platform.

- Concurrently, the advancement of system-on-chip integration, which can reduce bill-of-materials costs by 15% in high-volume applications like in-vehicle infotainment systems, threatens the market for discrete components.

- While a mixed-signal integrated circuit cannot replicate the performance of a specialized programmable gain amplifier or a component in hermetic packaging for a satellite telemetry system, it does erode the market for standard parts, including those in a simple voltage follower configuration.

- This pressures manufacturers to innovate in areas like low voltage noise density for a digital multimeter (DMM) front-end and arbitrary waveform generator applications.

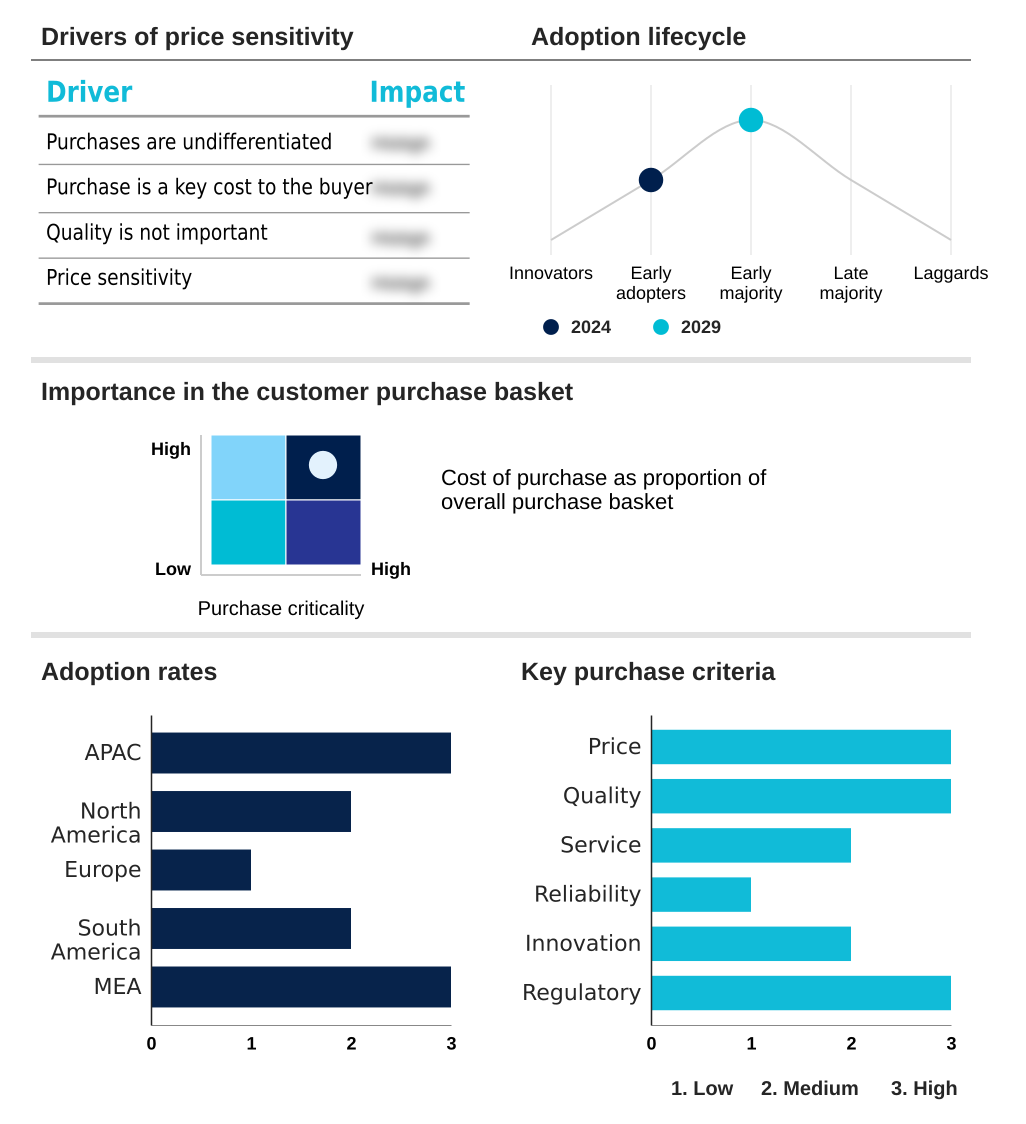

Exclusive Technavio Analysis on Customer Landscape

The operational amplifier market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the operational amplifier market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Operational Amplifier Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, operational amplifier market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABLIC Inc. - Specializes in zero-drift, rail-to-rail input/output operational amplifiers, engineered for low-power applications demanding high precision and stability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABLIC Inc.

- Advanced Linear Devices Inc.

- Analog Devices Inc.

- Apex Microtechnology

- Cirrus Logic Inc.

- Diodes Inc.

- Infineon Technologies AG

- KEC Holdings

- Microchip Technology Inc.

- Monolithic Power Systems Inc.

- Nisshinbo Holdings Inc.

- ON Semiconductor Corp.

- Renesas Electronics Corp.

- Richtek Technology Corp.

- ROHM Co. Ltd.

- STMicroelectronics NV

- Texas Instruments Inc.

- Toshiba Electronic Devices and Storage Corp.

- UTC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Operational amplifier market

- In September 2024, STMicroelectronics announced its new line of high-voltage operational amplifiers, capable of operating on 48V rails for industrial automation and mild-hybrid vehicle systems, enhancing its portfolio for robust applications.

- In November 2024, Texas Instruments Inc. launched its OPAx99-Q1 family of automotive-grade operational amplifiers, featuring high-speed performance and AEC-Q100 qualification for advanced driver-assistance systems (ADAS) sensor signal conditioning.

- In February 2025, Analog Devices Inc. unveiled a new series of micropower operational amplifiers with rail-to-rail input/output, specifically designed to extend battery life in wearable health monitors and IoT endpoint devices.

- In May 2025, Renesas Electronics highlighted the ISL28134, a chopper-stabilized, zero-drift operational amplifier designed for ultra-low noise and offset voltage, targeting biopotential signal amplification in medical applications.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Operational Amplifier Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 325 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.6% |

| Market growth 2025-2029 | USD 1450.2 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 4.5% |

| Key countries | China, Japan, South Korea, India, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, South Africa, UAE, Saudi Arabia, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The operational amplifier market is a complex ecosystem defined by a push for higher performance across multiple vectors. Strategic boardroom decisions on R&D investment are directly influenced by this specialization, weighing the development of a high gain-bandwidth product for communications against a precision current sensing device for automotive.

- Core technologies like the chopper-stabilized amplifier and zero-drift amplifier are crucial for achieving the ultra-low input offset voltage required in scientific instruments. The market's foundational technology, differential voltage amplification, is executed through an inverting input terminal and non-inverting input terminal, controlled via a negative feedback network.

- For battery-powered systems, achieving a low quiescent current is a primary design goal, while high-speed applications prioritize a fast slew rate and short settling time. Implementing advanced analog front-end design with components offering high common-mode rejection has improved signal fidelity by over 30% in critical systems.

- Further diversification is seen in a programmable gain amplifier, radiation-hardened component, and devices with a low 1/f noise corner, showcasing the industry's granular focus on application-specific performance and reliability.

What are the Key Data Covered in this Operational Amplifier Market Research and Growth Report?

-

What is the expected growth of the Operational Amplifier Market between 2025 and 2029?

-

USD 1.45 billion, at a CAGR of 4.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Automatic control system, Test and measurement, Vehicle electronics), Type (General-purpose, Precision, High-speed, Low-noise, Others), End-user (Consumer electronics, Automotive, Healthcare, Aerospace and defense, Others), Product Type (Open-loop, Closed-loop) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation of Internet of Things and connected devices , Persistent supply chain volatility and geopolitical risks

-

-

Who are the major players in the Operational Amplifier Market?

-

ABLIC Inc., Advanced Linear Devices Inc., Analog Devices Inc., Apex Microtechnology, Cirrus Logic Inc., Diodes Inc., Infineon Technologies AG, KEC Holdings, Microchip Technology Inc., Monolithic Power Systems Inc., Nisshinbo Holdings Inc., ON Semiconductor Corp., Renesas Electronics Corp., Richtek Technology Corp., ROHM Co. Ltd., STMicroelectronics NV, Texas Instruments Inc., Toshiba Electronic Devices and Storage Corp. and UTC

-

Market Research Insights

- Market dynamics are increasingly shaped by the demand for specialized analog components in high-value sectors. The adoption of high-performance amplifiers in smart factory automation has improved process stability by over 15%, while their integration into medical imaging front-end designs has reduced diagnostic signal acquisition time by 20% compared to previous-generation systems.

- The expansion of 5G telecommunications infrastructure relies on amplifiers capable of handling high-frequency signals. Concurrently, the growth in battery-powered devices, from a wearable health monitor to an electric vehicle powertrain, intensifies the need for power-efficient components.

- This is especially critical in battery management system (BMS) applications, where efficiency gains of just a few percentage points translate directly to extended operational life and reliability, underscoring the strategic importance of advanced analog design in modern electronic systems.

We can help! Our analysts can customize this operational amplifier market research report to meet your requirements.

RIA -

RIA -