Organic Chocolate Market Size 2024-2028

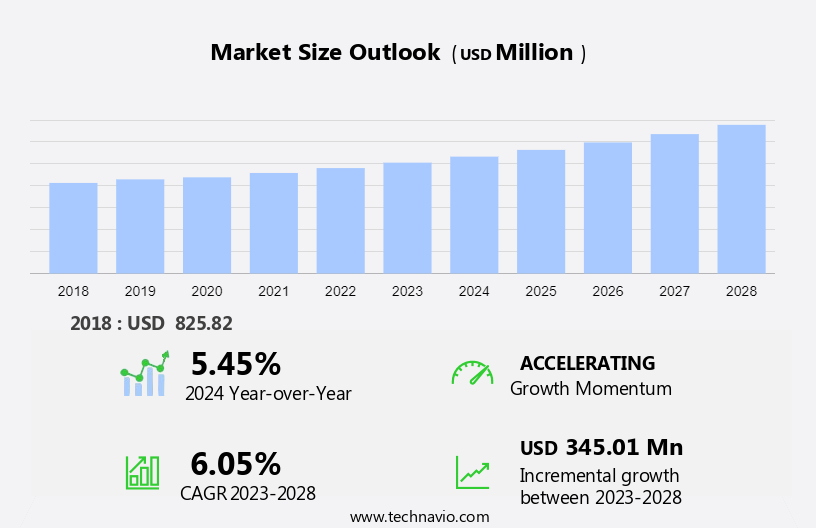

The organic chocolate market size is forecast to increase by USD 345.01 million at a CAGR of 6.05% between 2023 and 2028. The market is experiencing significant growth due to the increasing demand for organic food products in the United States. Premiumization of organic chocolates, particularly in the hazelnut segment, is a notable trend driving market expansion. The organic chocolate industry is witnessing innovative developments, such as the creation of new fruit spread, jam, and marmalade-infused chocolate products. However, the high production costs associated with organic farming and processing remain challenges for market participants. Despite these hurdles, the market is expected to continue its growth trajectory, offering opportunities for businesses in the chocolate confectionery sector.

What will be the Size of the Market During the Forecast Period?

The market is experiencing significant growth within the confectionery industry. Consumers' increasing awareness of health and wellness, coupled with a desire for ethically sourced and sustainably produced goods, has led to a surge in demand for organic chocolate products. Organic chocolate is produced using organic cocoa beans, which are grown without the use of artificial fertilizers or pesticides. This approach to farming not only benefits the environment by preserving soil health and promoting biodiversity, but also ensures the absence of harmful chemicals in the final product. The organic farming practices employed in the production of organic chocolate align with the broader trend towards organic goods in various sectors.

Consumers are increasingly seeking out organic food products, including chocolate spreads, as they perceive them to be healthier and more sustainable alternatives to conventional products. Dark, milk, and hazelnut chocolate spreads are popular choices within the organic chocolate spread segment. These spreads offer consumers a delicious and versatile way to enjoy the rich flavors of organic chocolate in their daily lives. Valeo Foods, Chocobee, and other organic chocolate confectioneries are capitalizing on this trend by introducing innovative and high-quality organic chocolate spreads to the market. The organic cocoa industry is also gaining traction, with a focus on sustainable and ethical production practices.

The use of organic farming methods ensures that cocoa farmers receive fair wages and work in safe conditions, while also minimizing the environmental impact of cocoa production. The market is not limited to spreads, however. Organic chocolate confectioneries, including chocolates, beverages, and cocoa powder, are also experiencing growth. These products cater to consumers who seek the health benefits and ethical production practices associated with organic chocolate. The fruit spread, jam, and marmalade segments are also seeing an increase in demand for organic options, as consumers look for healthier alternatives to traditional sweet spreads. Organic chocolate spreads, with their rich chocolate flavor and health benefits, are gaining popularity as a natural and delicious alternative to these conventional products.

Moreover, the market is poised for continued growth, as consumers become more conscious of their health and the environmental impact of their food choices. Organic chocolate confectioneries and chocolate spreads, in particular, offer a delicious and sustainable way for consumers to indulge in their sweet tooth while supporting ethical and sustainable farming practices. In conclusion, the market is a growing trend within the confectionery industry, driven by consumers' increasing awareness of health and sustainability. Organic chocolate spreads, made from organic cocoa beans grown using sustainable farming practices, are a popular choice for consumers seeking healthier and more ethically produced alternatives to conventional chocolate spreads. The market is expected to continue growing, as consumers increasingly demand transparency and sustainability in their food choices.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

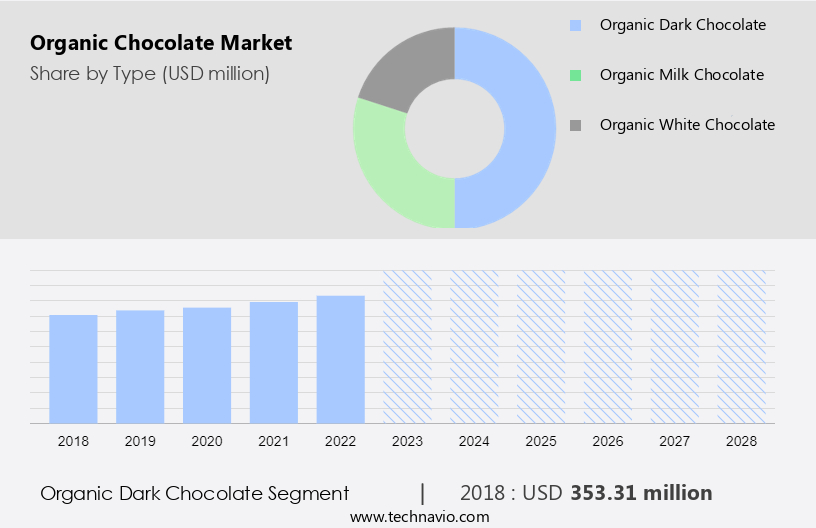

- Organic dark chocolate

- Organic milk chocolate

- Organic white chocolate

- Distribution Channel

- Offline

- Online

- Geography

- Europe

- Germany

- UK

- North America

- Canada

- US

- APAC

- China

- South America

- Middle East and Africa

- Europe

By Type Insights

The organic dark chocolate segment is estimated to witness significant growth during the forecast period. Organic dark chocolate is a popular product in the cocoa industry, derived primarily from the seeds of the cocoa tree that are organically produced. This type of chocolate is gaining traction among health-conscious consumers due to its higher nutrient content compared to other chocolate varieties. Organic dark chocolate is rich in antioxidants and flavonoids, which promote cardiovascular health by stimulating the production of nitric oxide in the blood vessels. Major companies in The market include Barry Callebaut AG and Divine Chocolate, a subsidiary of Ludwig Weinrich GmbH and Co. The demand for clean-label products, including organic chocolate, is on the rise as consumers seek healthier options. Organic cocoa powder is also used in the production of various beverages, further expanding the market for this product. As the trend towards healthy eating continues, the market is expected to grow steadily.

Get a glance at the market share of various segments Request Free Sample

The organic dark chocolate segment accounted for USD 353.31 million in 2018 and showed a gradual increase during the forecast period.

Regional Insights

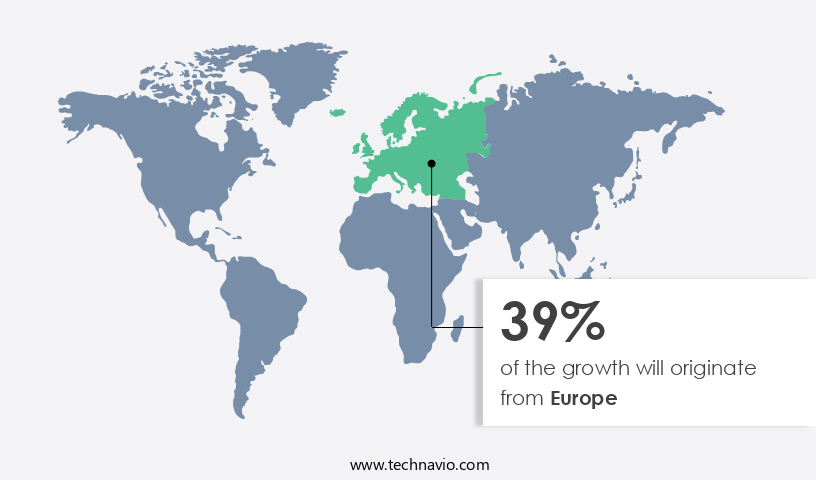

Europe is estimated to contribute 39% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

Organic chocolate has gained significant popularity in the confectionery industry, particularly in Europe, where the preference for organic goods is on the rise. The European market for organic chocolate, including organic dark, milk, and white varieties, is witnessing substantial growth due to the increasing demand for fine-flavored cocoa. The region's organic chocolate manufacturing industry requires large quantities of cocoa beans, leading to a surge in demand for these beans from countries practicing organic farming. Organic farming practices, which exclude the use of artificial fertilizers and pesticides, are essential for soil preservation and sustainable farming. The European Union (EU) has strict regulations regarding organic farming, ensuring the highest standards for organic products.

These regulations have made Europe a prominent region in The market. Major markets for organic chocolate in Europe include France, Switzerland, Germany, and the UK. The increasing number of product innovations and launches is expected to drive the growth of the highly competitive market in Europe during the forecast period. As consumers become more health-conscious and environmentally aware, the demand for organic chocolate is likely to continue increasing in the region.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Increasing premiumization of organic chocolates is the key driver of the market. The market in the confectionery industry is experiencing significant growth, with a focus on organic farming practices and the production of clean-label, health-conscious chocolate products. companies, such as Divine Chocolate and ChocoBee, are prioritizing soil preservation and plant protection, avoiding the use of artificial fertilizers and pesticides. This approach resonates with consumers seeking premium, high-quality organic chocolate, including dark, white, and milk varieties. The demand for organic chocolate spreads, such as dark chocolate and milk chocolate spreads, as well as hazelnut chocolate spread, is also increasing. Valeo Foods and other market players are responding by expanding their organic product offerings and emphasizing the benefits of organically produced cocoa.

Moreover, the cocoa industry, including chocolate confectioneries, cocoa liquor, chocolate couverture, cocoa butter, and cocoa powder, is benefiting from this trend. Consumers are increasingly seeking healthy eating options and are willing to pay a premium for organic and clean-label products. The organic cocoa industry is expected to continue growing, with an emphasis on transparency and sustainability. The market is not limited to traditional chocolate products. It also includes organic fruit spreads, jams, and marmalades, as well as dairy beverages and cocoa beverages. As consumers continue to prioritize health and wellness, the demand for organic chocolate and related products is expected to remain strong.

Market Trends

Growing developments in organic chocolate industry is the upcoming trend in the market. The market in the confectionery industry is witnessing significant growth due to increasing consumer demand for organic and ethically sourced products. Organic chocolate manufacturers are focusing on initiatives that promote fair trade and sustainable farming practices. For instance, some companies are ensuring that cocoa farmers receive fair compensation and are implementing organic farming methods that avoid the use of artificial fertilizers and pesticides for soil preservation and plant protection. Recent developments in the market include Hu Kitchen's launch of dairy milk chocolate options sourced from grass-fed cows, catering to consumers seeking ethical and sustainable dairy products.

Additionally, Theobroma Chocolat introduced "Yummy Zero Sugar," a groundbreaking innovation in organic chocolate, providing consumers with a sugar-free option. Valeo Foods, ChocoBee, and other players in the market are also focusing on clean-label products, using organically produced cocoa and organic cocoa industry ingredients such as cocoa butter, cocoa liquor, chocolate couverture, and cocoa butter blocks. The market also includes organic chocolate spreads like dark chocolate spread, milk chocolate spread, and hazelnut chocolate spread. The organic food fair is another platform showcasing a range of organic food products, including fruit spread, jam, marmalade, and hazelnut segment, highlighting the growing popularity of organic products in the chocolate confectionery and cocoa industry. The trend towards healthy eating and clean-label products is driving the demand for organic chocolate, beverages, cocoa powder, and other chocolate confectioneries.

Market Challenge

High production costs associated with organic farming and processing is a key challenge affecting the market growth. The market in the confectionery industry is characterized by higher production costs due to the requirements of organic farming. In contrast to conventional chocolate production, organic farming adheres to stringent regulations, prohibiting synthetic pesticides, herbicides, and fertilizers. These regulations can lead to lower yields and increased production expenses for organic cocoa farmers. Organic farming practices, such as crop rotation, natural pest control, and soil conservation, necessitate additional labor and resources compared to conventional farming methods. Farmers must also invest in organic certifications and compliance measures to meet regulatory standards, further increasing production costs.

However, organic chocolate offerings include Dark, White, and Milk varieties from companies like Divine Chocolate and ChocoBee. The Organic Cocoa Industry also produces organic cocoa powder, cocoa liquor, chocolate couverture, cocoa butter blocks, chips, and liquid cocoa butter for use in chocolate confectioneries, cakes, pastries, biscuits, dairy beverages, and healthy eating products. Organic Food Fairs showcase a range of organic food products, including organic chocolate spreads like Dark, Milk, and Hazelnut, as well as fruit spreads, jams, and marmalades. Valeo Foods and other market players offer clean-label, organically produced cocoa and chocolate products. The market is a niche segment of the chocolate confectionery and cocoa industry, with a focus on sustainable farming practices and health-conscious consumers.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Alter Eco: The company offers organic chocolate such as super blackout, dark salted brown butter, dark salted burnt caramel, deep dark sea salt, deep dark classic blackout, mint blackout organic dark chocolate, and others.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alter Eco

- American Licorice Co.

- Barry Callebaut AG

- Chocolat Bernrain AG

- Compartes Chocolatier

- Endangered Species Chocolate LLC

- Fortissimo Chocolates Ltd.

- Giddy Yoyo Inc.

- HOFER KG

- Ludwig Weinrich GmbH and Co. KG

- Mason and Co.

- Mondelez International Inc.

- Montezumas Direct Ltd.

- Newmans Own Inc.

- Nibmor Inc.

- Pronatec AG

- Rococo Chocolates London Ltd.

- Stern Wywiol Gruppe GmbH and Co. KG

- Taza Chocolate

- The Grenada Chocolate Co. Ltd.

- The Hershey Co.

- Theobroma Chocolat

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Organic chocolate is a popular choice in the confectionery industry for those seeking healthier and ethically sourced treats. Unlike conventional chocolate, organic chocolate is produced using organic farming methods, avoiding artificial fertilizers and pesticides. This results in better soil preservation and plant protection, ensuring high-quality cocoa beans. Organic chocolate comes in various forms, including dark, white, and milk varieties. Brands like Divine Chocolate and Valeo Foods offer organic dark chocolate, vegan/paleo options, and organic chocolate spreads. These spreads include dark chocolate spread, milk chocolate spread, and hazelnut chocolate spread. The organic cocoa industry focuses on clean-label products, with organic cocoa powder, cocoa liquor, chocolate couverture, cocoa butter blocks, and cocoa butter used in chocolates, beverages, and baked goods like cakes, pastries, biscuits, and dairy beverages. Organic food fairs showcase a wide range of organic food products, including fruit spreads, jams, and marmalades in the hazelnut segment. Organic chocolate production supports cocoa farmers, ensuring fair wages and sustainable farming practices. The organic cocoa industry's commitment to organic farming and clean-label products caters to consumers' growing demand for healthy eating and ethically sourced products.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

162 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.05% |

|

Market growth 2024-2028 |

USD 345.01 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.45 |

|

Regional analysis |

Europe, North America, APAC, South America, and Middle East and Africa |

|

Performing market contribution |

Europe at 39% |

|

Key countries |

US, Canada, China, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Alter Eco, American Licorice Co., Barry Callebaut AG, Chocolat Bernrain AG, Compartes Chocolatier, Endangered Species Chocolate LLC, Fortissimo Chocolates Ltd., Giddy Yoyo Inc., HOFER KG, Ludwig Weinrich GmbH and Co. KG, Mason and Co., Mondelez International Inc., Montezumas Direct Ltd., Newmans Own Inc., Nibmor Inc., Pronatec AG, Rococo Chocolates London Ltd., Stern Wywiol Gruppe GmbH and Co. KG, Taza Chocolate, The Grenada Chocolate Co. Ltd., The Hershey Co., and Theobroma Chocolat |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -