Orthopedic 3D Printed Devices Market Size 2025-2029

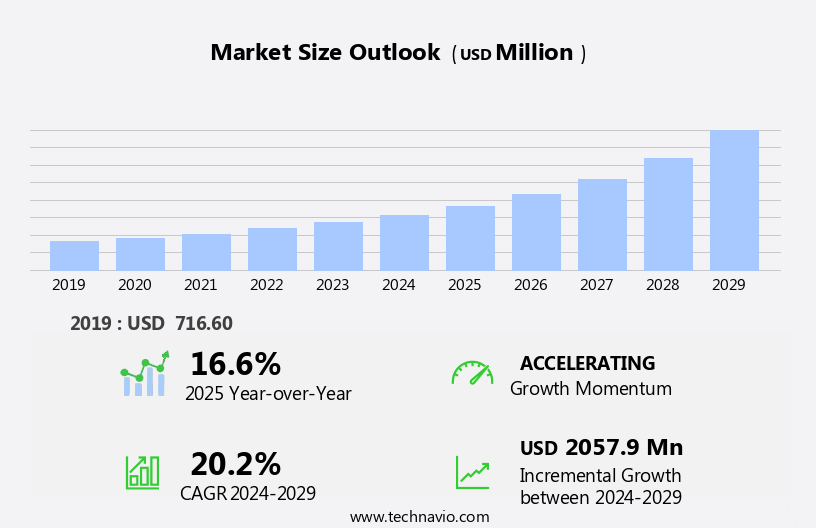

The orthopedic 3D printed devices market size is forecast to increase by USD 2.06 billion at a CAGR of 20.2% between 2024 and 2029.

- The market is experiencing significant growth due to the increasing demand for personalized orthopedic solutions. The ability of 3D printing technology to create customized devices tailored to individual patient needs is a key driver in this market. Medical professionals are increasingly adopting this technology to improve patient outcomes and enhance the overall patient experience. These trends are primarily driven by the increasing demand for innovative solutions, advancements in medical technology, and changing consumer preferences. However, high initial costs associated with setting up a 3D printing facility pose a significant challenge for market entrants. Despite this hurdle, the potential for innovation and the ability to address unmet clinical needs make the market an attractive proposition for companies seeking to capitalize on emerging opportunities.

- By focusing on cost reduction strategies and collaborative partnerships, market players can navigate the challenges and seize the potential of this dynamic and evolving market. The market's growth in the coming years will be fueled by the increasing number of elective orthopedic operations, advancements in implant materials and surgical techniques, and the integration of telemedicine and robotic operation assistants.

What will be the Size of the Orthopedic 3D Printed Devices Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The market is experiencing significant advancements, particularly in trauma operations and sports medicine. Artificial intelligence (AI) and machine learning algorithms are revolutionizing design optimization and software solutions, enabling reverse engineering and 3D scanning for personalized implants. Polylactic acid (PLA), polyurethane (PU), polypropylene (PP), and bioabsorbable polymers are popular materials for functional restoration, while ceramic materials and composite structures cater to spinal disorders and bone cancer patients.

- Orthopedic operation and physical therapy are benefiting from AI-assisted pain management and data analytics. Surgical robotics and PEEK polymers are transforming complex procedures, while bioactive glasses and PE enhance implant integration. These trends are improving the quality of life for patients and driving market growth.

How is this Orthopedic 3D Printed Devices Industry segmented?

The orthopedic 3D printed devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Orthopedic implants

- Surgical planning

- Surgical instruments

- Type

- Plastics

- Nylon

- Biomaterials

- Others

- Technology

- Stereolithography (SLA)

- Fused deposition modeling (FDM)

- Selective laser sintering (SLS)

- Electron beam melting (EBM)

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

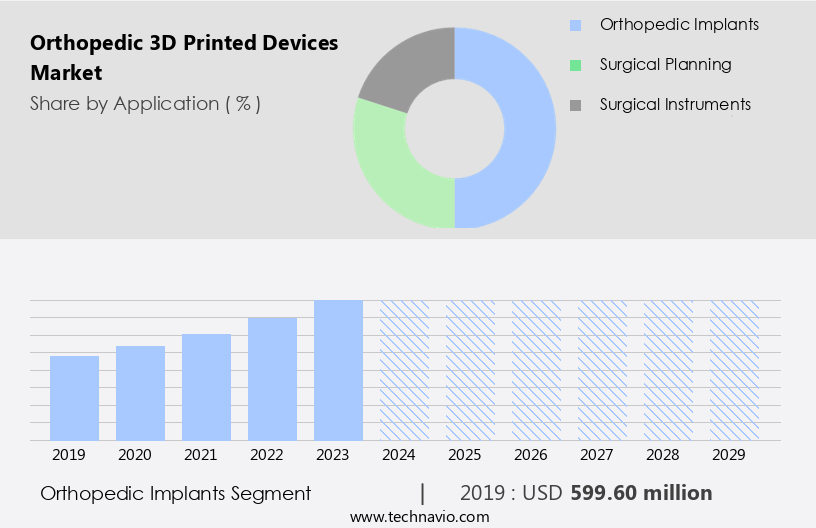

By Application Insights

The orthopedic implants segment is estimated to witness significant growth during the forecast period. The market encompasses surgical guides, mechanical strength medical devices, patient-specific designs, and various orthopedic implants. This sector leverages 3D printing and additive manufacturing to create complex structures, including bone implants, dental implants, and custom orthotics. Titanium alloys, with their high fracture toughness and biocompatibility, are commonly used materials in this field. Manufacturing automation through computer-aided design (CAD) and 3D printing technology enables the production of customized implants, addressing the unique needs of individual patients. Biocompatibility testing and biomechanical modeling ensure the safety and efficacy of these devices. 3D printing allows for the creation of intricate structures, unattainable through traditional manufacturing methods, and facilitates the production of patient-matched implants.

The technology's potential in personalized medicine reduces healthcare costs by minimizing the need for multiple implant sizes and types. Regulatory approvals, clinical trials, and patient outcomes are crucial factors driving the growth of the market. Advanced manufacturing techniques, such as stereolithography (SLA), powder bed fusion, and surface finishing, contribute to the development of high-quality, durable implants with improved wear resistance and fatigue strength. Bioresorbable materials and image-guided operation further expand the application scope of 3D printed orthopedic devices, enhancing patient care and surgical precision. Quality control measures ensure consistent product performance and reliability, making 3D printed orthopedic devices a promising solution for various orthopedic applications.

The Orthopedic implants segment was valued at USD 599.60 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

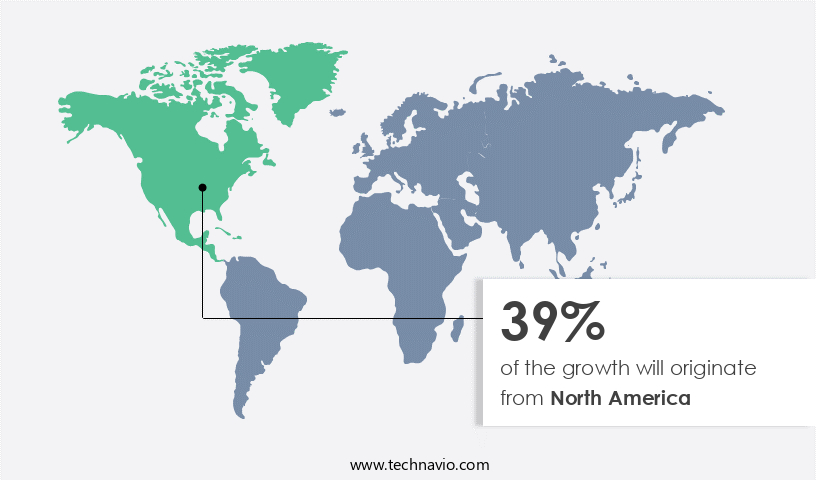

North America is estimated to contribute 39% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market experienced significant growth in 2024, with North America leading the revenue share. The US and Canada were the primary contributors to the market in the Americas, driven by enhanced healthcare infrastructure, increased adoption of 3D printing devices in healthcare facilities, and the presence of established companies. In Canada, around 59,000 hip replacements and over 70,000 knee replacements were performed between 2017 and 2018, according to the Canadian Joint Replacement Registry (CJRR). Additionally, over 9,700 hip and knee revision operations took place the previous year. The market's expansion can also be attributed to the advantages of patient-specific designs, mechanical strength from materials like titanium alloys and biocompatible materials, and the potential for tissue engineering and joint replacements.

Regulatory approvals, clinical trials, and quality control are crucial aspects of the market, ensuring the biocompatibility, fatigue strength, and wear resistance of these devices. Technological advancements, such as additive manufacturing, computer-aided design, stereolithography, and surface finishing, contribute to the market's evolution. The integration of medical imaging and image-guided operation further enhances the precision and customization of these devices. Manufacturing automation and biomechanical modeling enable efficient production and accurate design, while material extrusion and powder bed fusion are essential fabrication techniques. The market's trends include the development of bioresorbable materials and joint replacements, catering to the demand for personalized medicine and minimally invasive procedures.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Orthopedic 3D Printed Devices market drivers leading to the rise in the adoption of Industry?

- The increase in demand for personalized and customized orthopedic devices is the primary market driver, as patients increasingly seek individualized solutions to address their unique orthopedic needs. Three-dimensional (3D) printing technology is revolutionizing the orthopedic medical device industry by enabling the creation of patient-specific surgical guides and implants. This technology allows for the fabrication of customized devices using a patient's medical imaging data. The intricate shapes and geometric features possible with additive layer manufacturing are not achievable through traditional subtractive manufacturing techniques, regardless of cost. 3D printing is particularly valuable in the development of complex orthopedic applications, such as customized prosthetic limbs. The technology facilitates the creation of porous engineered structures, tortuous internal channels, and internal support structures, all of which enhance implant performance and patient outcomes.

- The use of 3D printing in orthopedics is not limited to complex cases. It also offers advantages in the production of standard implants, as it allows for the rapid prototyping and testing of new designs. Furthermore, the use of materials like titanium alloys ensures the required mechanical strength and fracture toughness for orthopedic applications. Personalized medicine is a growing trend in healthcare, and 3D printing plays a significant role in its implementation. The ability to create patient-specific devices using 3D printing technology reduces healthcare costs by minimizing the need for multiple surgical procedures and reducing the time and resources required for traditional manufacturing methods.

What are the Orthopedic 3D Printed Devices market trends shaping the Industry?

- Medical professionals are increasingly adopting 3D printing technology, marking a significant trend in the healthcare industry. This advanced technology enables the creation of customized medical devices and implants, improving patient outcomes and reducing costs. 3D printing, a cutting-edge technology, is revolutionizing the medical field, particularly in orthopedics. This additive manufacturing process enables the creation of intricately designed bone implants, dental implants, and other medical devices. The technology's integration into orthopedic procedures enhances manufacturing automation, leading to improved accuracy, efficiency, and cost savings. Biocompatibility testing and biomechanical modeling are crucial aspects of 3D printing in orthopedics. Material extrusion is a common 3D printing technique used to produce implants, ensuring they mimic the mechanical properties of natural bone. These advancements offer operations a more deep experience, enabling them to anticipate surgical challenges and optimize patient treatment.

- Pre-surgical planning, such as that for shoulder arthroplasty, benefits significantly from 3D printed anatomical models. These models provide a more comprehensive understanding of complex anatomy and pathology compared to traditional 2D representations.

How does Orthopedic 3D Printed Devices market face challenges during its growth?

- The high initial costs associated with establishing a 3D printing facility pose a significant challenge and hinder the industry's growth. The market is experiencing significant growth due to the advancements in biocompatible materials and tissue engineering. Regulatory approvals for these devices are increasing, enabling custom orthotics and prosthetics to become more accessible. Computer-aided design (CAD) technology plays a crucial role in the production process, ensuring precise and accurate designs. However, high capital costs are a barrier to widespread adoption. These costs include the expensive equipment required for 3D printing or outsourced print service contracts, as well as the advanced software used in post-processing activities. High-end additive manufacturing (AM) printers, such as SLS, material jetting, and metal printing, can cost from USD200,000 to USD850,000, and sometimes even several millions of dollars.

- End-users must also bear the costs of maintenance and repairs on the 3D printing machines. Additionally, the cost of proprietary raw materials sold by 3D printer manufacturers contributes to the high costs. Clinical trials and patient outcomes studies are essential to validate the effectiveness and safety of these devices, further increasing the overall costs. Despite these challenges, the potential benefits of 3D printed orthopedic devices, such as improved fatigue strength and customization, make them an attractive option for the healthcare industry.

Exclusive Customer Landscape

The orthopedic 3D printed devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the orthopedic 3D printed devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, orthopedic 3D printed devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3D Systems Corp. - This company provides orthopedic operations with advanced 3D visualization technology, enabling them to examine a patient's anatomy in detail and create customized surgical plans before procedures.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3D Systems Corp.

- Biomedical Modeling Inc.

- Dimension Inx.

- EOS GmbH

- Formlabs Inc.

- General Electric Co.

- Johnson and Johnson Services Inc.

- MATERIALISE NV

- Medtronic Plc

- Osteo3D

- Renishaw Plc

- SLM Solutions Group AG

- Smith and Nephew plc

- Stratasys Ltd.

- Ultimaker BV

- Zimmer Biomet Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Orthopedic 3D Printed Devices Market

- In February 2024, Stryker Corporation, a leading medical technology company, announced the FDA clearance and commercial launch of its 3D printed, custom-made titanium knee implants. This innovative product expansion marks a significant step forward in personalized orthopedic solutions (Stryker Corporation Press Release, 2024).

- In May 2025, Medtronic and GE Additive, a leading metal 3D printing company, announced a strategic partnership to develop and commercialize 3D-printed orthopedic implants. This collaboration combines Medtronic's clinical expertise and market reach with GE Additive's advanced 3D printing technology (Medtronic Press Release, 2025).

- In July 2024, Nano Dimension, a leading additive manufacturing solutions provider, raised USD120 million in a funding round to expand its production capacity and accelerate the development of its DragonFly LMD 3D printer for bioprinting orthopedic implants. This investment signifies a strong market demand and confidence in the potential of 3D-printed orthopedic devices (Nano Dimension Press Release, 2024).

Research Analyst Overview

The market continues to evolve, driven by advancements in biocompatible materials, tissue engineering, and regulatory approvals. The integration of computer-aided design (CAD) and medical imaging enables the creation of patient-specific designs, leading to improved fit and functionality. Titanium alloys, known for their mechanical strength and fracture toughness, remain popular choices for bone implants. Manufacturing automation through additive manufacturing techniques, such as material extrusion and powder bed fusion, streamlines production and reduces healthcare costs. Bone implants, dental implants, and custom orthotics are among the sectors benefiting from these innovations. Biocompatibility testing and biomechanical modeling ensure the durability and wear resistance of these devices.

Regulatory approvals continue to be granted, enabling wider market access. Ongoing clinical trials provide valuable insights into patient outcomes, further fueling market growth. The future of orthopedic devices lies in personalized medicine, with a focus on patient-specific designs and tissue engineering. Bioresorbable materials offer the potential for minimally invasive procedures and reduced recovery times. Image-guided operations and surface finishing techniques enhance precision and accuracy. Market dynamics remain fluid, with ongoing research and development shaping the landscape. The ongoing integration of technology and biology promises to unlock new possibilities in the orthopedic devices sector.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Orthopedic 3D Printed Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

235 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 20.2% |

|

Market growth 2025-2029 |

USD 2.06 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

16.6 |

|

Key countries |

US, Germany, China, UK, Canada, France, Italy, Japan, India, and Mexico |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Orthopedic 3D Printed Devices Market Research and Growth Report?

- CAGR of the Orthopedic 3D Printed Devices industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the orthopedic 3D printed devices market growth of industry companies

We can help! Our analysts can customize this orthopedic 3D printed devices market research report to meet your requirements.

RIA -

RIA -