Outsourced Orthopedic Manufacturing Market Size 2025-2029

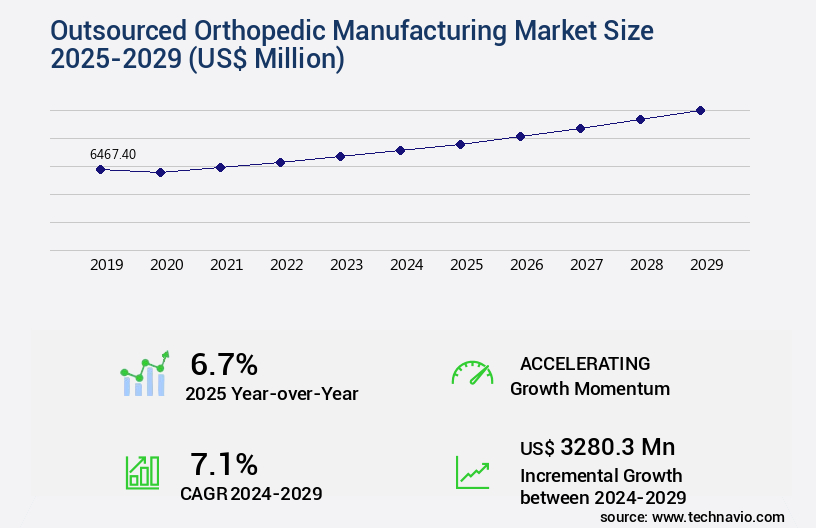

The outsourced orthopedic manufacturing market size is valued to increase USD 3.28 billion, at a CAGR of 7.1% from 2024 to 2029. Rising demand for orthopedic procedures will drive the outsourced orthopedic manufacturing market.

Major Market Trends & Insights

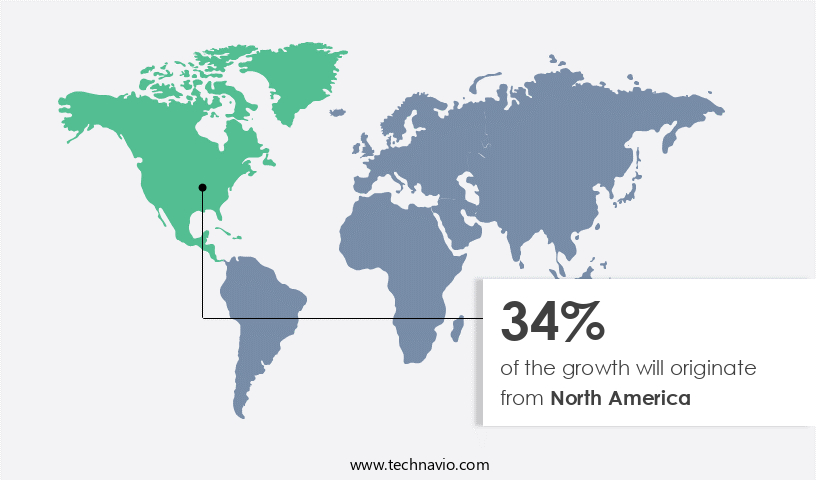

- North America dominated the market and accounted for a 34% growth during the forecast period.

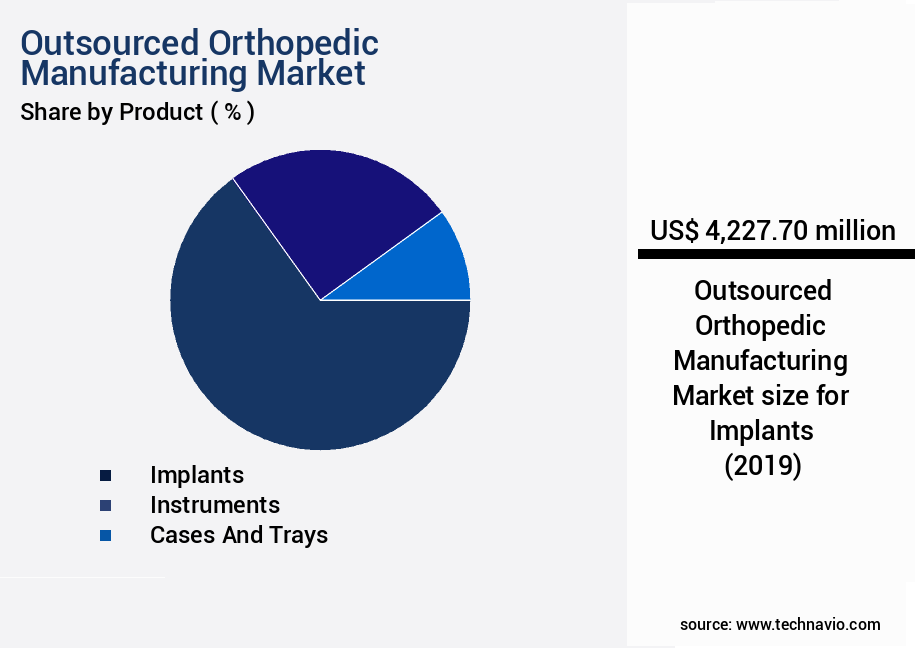

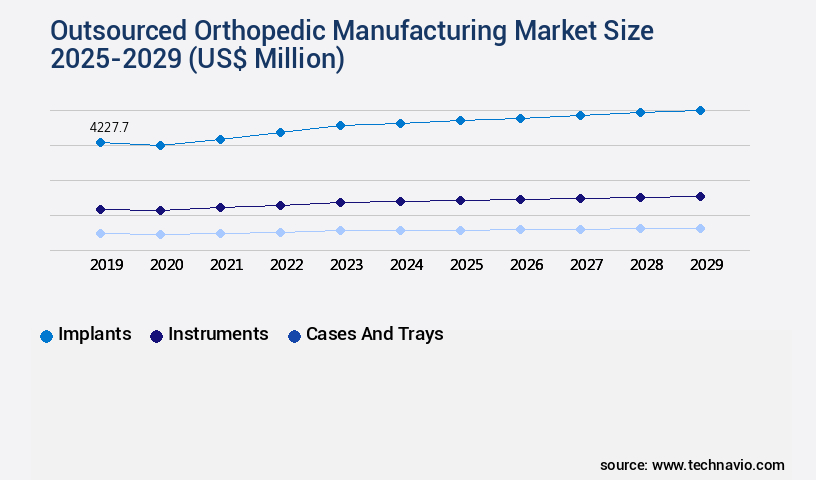

- By Product - Implants segment was valued at USD 4.23 billion in 2023

- By Material - Metal segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 74.50 million

- Market Future Opportunities: USD 3280.30 million

- CAGR from 2024 to 2029: 7.1%

Market Summary

- In the dynamic orthopedic industry, outsourced manufacturing has emerged as a strategic solution for companies seeking cost savings, improved efficiency, and access to specialized expertise. According to market intelligence, the market was valued at USD 14.2 billion in 2020, reflecting the significant demand for these services. Key drivers for this market include the rising prevalence of orthopedic conditions and the increasing adoption of advanced manufacturing technologies. These innovations, such as 3D printing and automation, enable the production of customized implants and devices, enhancing patient outcomes and reducing surgical time. However, the market faces challenges from stringent regulatory requirements.

- Compliance with various regulatory bodies, such as the US Food and Drug Administration (FDA), necessitates rigorous quality control measures and extensive documentation. This not only increases operational costs but also demands a high level of expertise from manufacturers. Despite these challenges, the future of outsourced orthopedic manufacturing looks promising. The integration of digital technologies, such as artificial intelligence and machine learning, is expected to streamline processes, improve accuracy, and reduce errors. Moreover, the growing trend towards personalized medicine will further fuel demand for customized orthopedic solutions, making outsourced manufacturing an indispensable part of the orthopedic value chain.

What will be the Size of the Outsourced Orthopedic Manufacturing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Outsourced Orthopedic Manufacturing Market Segmented ?

The outsourced orthopedic manufacturing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Implants

- Instruments

- Cases and trays

- Material

- Metal

- Polymers

- Ceramics

- Composites

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Product Insights

The implants segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with a significant focus on the production of orthopedic implants. These essential medical devices, which include joint implants for hips, knees, and other parts of the musculoskeletal system, are in high demand due to their role in restoring mobility, reducing pain, and improving patients' quality of life. The global market for outsourced orthopedic manufacturing is expected to reach USD 28.4 billion by 2027. Orthopedic implants are manufactured using various techniques, including 3D printing, forging titanium alloys, and precision machining.

The manufacturing process involves several stages, including design transfer, production planning, material engineering, and quality control systems. Component inspection, design verification, and process validation are crucial steps to ensure regulatory compliance and maintain high-quality standards. Surface treatments, such as hydroxyapatite coating, are used to enhance implant biocompatibility and promote bone growth. Sterile processing, inventory management, and risk management are also essential aspects of outsourced orthopedic manufacturing. Sterilization validation, packaging validation, and device traceability are critical to ensure patient safety and regulatory compliance. Medical device outsourcing companies offer contract manufacturing services for orthopedic implants, providing expertise in areas such as material certifications, regulatory submissions, and supply chain management.

The Implants segment was valued at USD 4.23 billion in 2019 and showed a gradual increase during the forecast period.

Precision machining, CNC machining implants, and additive manufacturing are used to produce implants with high accuracy and complexity. Failure analysis and quality assurance are ongoing activities to ensure product lifecycle management and maintain the highest standards of care for patients.

Regional Analysis

North America is estimated to contribute 34% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Outsourced Orthopedic Manufacturing Market Demand is Rising in North America Request Free Sample

The North American region holds a prominent position in the market, fueled by several influential factors. With the presence of major industry players, including Stryker, Zimmer Biomet, Medtronic, and Johnson & Johnson (DePuy Synthes), headquartered in the US, the demand for contract manufacturing services is significantly boosted. These companies, renowned for their industry expertise and advanced technologies, produce high-quality orthopedic implants and instruments, strengthening North America's leading role in the market.

Furthermore, the extensive healthcare infrastructure in North America, comprising approximately 6,100 hospitals in the US and around 1,010 hospitals in Canada, provides ample opportunities for market expansion.

Market Dynamics

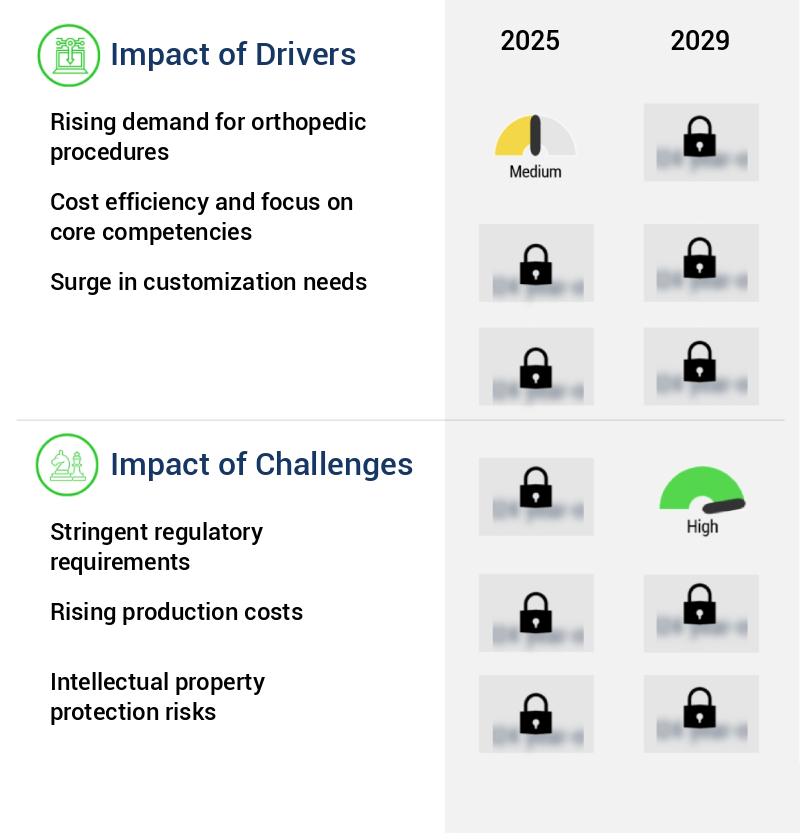

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to the increasing demand for advanced orthopedic devices. Orthopedic implant surface modification plays a crucial role in enhancing implant performance and biocompatibility. Titanium alloy, a popular material for orthopedic implants, undergoes rigorous fatigue strength testing to ensure durability and reliability. Precision machining of orthopedic components is essential for achieving the required accuracy and fit. Quality control in orthopedic device manufacturing is paramount to ensure regulatory compliance for medical devices. Sterilization validation for medical implants is another critical aspect, ensuring the elimination of microbial contamination and maintaining the integrity of the implant material. Additive manufacturing of custom implants is revolutionizing the industry, enabling the production of complex geometries and individualized solutions. Design verification orthopedic devices is a crucial step in the manufacturing process, ensuring that the final product meets the intended design specifications. Biocompatible material selection for implants is essential to minimize the risk of adverse reactions. Computer-aided design (CAD) is widely used in orthopedic implant production planning, enabling efficient and accurate design and manufacturing processes. Supply chain management for orthopedic implants is a complex process that requires effective risk management strategies and process validation to ensure the timely delivery of high-quality products. Regulatory compliance for medical devices is a continuous challenge, requiring ongoing efforts in design transfer, failure analysis, quality assurance, and surgical instrument sterilization validation. Packaging validation of medical devices is another critical aspect of the manufacturing process, ensuring that the packaging protects the implant during transportation and storage. Device traceability systems are essential to maintain a comprehensive record of each implant's production history, enabling effective recall management and improving patient safety.

What are the key market drivers leading to the rise in the adoption of Outsourced Orthopedic Manufacturing Industry?

- The surge in demand for orthopedic procedures serves as the primary catalyst for market growth in this sector.

- The market is undergoing substantial expansion due to the escalating demand for orthopedic treatments. This growth can be largely attributed to the increasing prevalence of conditions such as osteoporosis, osteoarthritis, and trauma-related injuries, leading to a higher requirement for orthopedic implants and instruments. The global population aged 60 years and above is projected to reach 2.1 billion by 2050, according to World Health Organization data.

- This demographic shift will significantly increase the demand for orthopedic solutions, as older adults are more susceptible to these conditions. The outsourcing of orthopedic manufacturing offers numerous advantages, including cost savings, improved efficiency, and enhanced product quality. This trend is expected to continue, making the market a robust and evolving sector.

What are the market trends shaping the Outsourced Orthopedic Manufacturing Industry?

- Advanced manufacturing technologies are increasingly being adopted as the market trend. Adoption of advanced manufacturing technologies is a significant trend in the current market.

- The market is undergoing a significant transformation due to the adoption of advanced technologies. Technologies such as 3D printing, robotics, and computer-aided design (CAD) are driving enhanced precision, improved efficiency, and greater product customization in the production of orthopedic devices. One of the most notable advancements is the increasing use of 3D printing, also known as additive manufacturing. This technology enables the creation of customized implants and surgical instruments with intricate designs and complex geometries, previously challenging to achieve with traditional methods. For instance, the Stryker Tritanium PL Cage, a 3D-printed spinal implant, boasts a porous structure that promotes better bone integration, leading to improved post-surgery outcomes.

- Robotics and computer-aided design are also playing a pivotal role in the evolution of the market. These technologies allow for increased automation and automation, reducing production time and errors, while also enabling greater product customization. The integration of these advanced technologies is leading to a more robust and competitive landscape in the outsourced orthopedic manufacturing industry.

What challenges does the Outsourced Orthopedic Manufacturing Industry face during its growth?

- The stringent regulatory requirements pose a significant challenge to the industry's growth, imposing mandatory compliance that professionals must adhere to in order to operate effectively.

- The market is subject to stringent regulatory requirements, necessitating adherence to rigorous safety, quality, and performance standards. In the US, the Food and Drug Administration (FDA) enforces comprehensive Quality System Regulations (QSR) under 21 CFR Part 820. These regulations mandate thorough design controls, risk management strategies, and documentation processes for contract manufacturers. Orthopedic implants, including hip replacements, knee implants, and spinal devices, undergo extensive clinical testing and validation before receiving FDA clearance or approval.

- The European Union's Medical Devices Regulation (MDR) and the International Organization for Standardization (ISO) 13485:2016 also set similar standards for orthopedic manufacturing. These regulations ensure that orthopedic devices meet stringent safety and efficacy requirements, ultimately benefiting patients and healthcare providers.

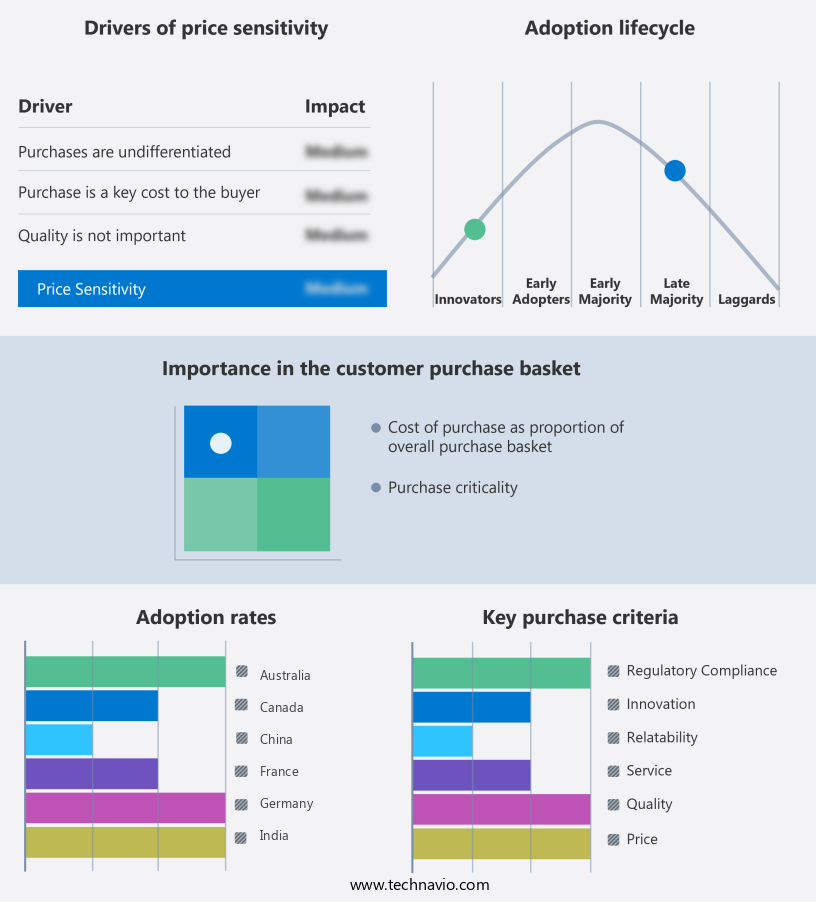

Exclusive Technavio Analysis on Customer Landscape

The outsourced orthopedic manufacturing market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the outsourced orthopedic manufacturing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Outsourced Orthopedic Manufacturing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, outsourced orthopedic manufacturing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Autocam Medical - This company specializes in providing outsourced manufacturing solutions for high-precision orthopedic implants, surgical instruments, and components, catering to orthopedic, spine, and cardiovascular applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Autocam Medical

- Avalign Technologies Inc.

- Cretex Companies Inc.

- intech Medical SAS

- LISI MEDICAL

- Marle Group

- Norman Noble Inc.

- Norwood Medical

- Orchid MPS Holdings LLC

- Paragon Medical

- Resolve Surgical Technologies

- SpiTrex Orthopedics

- Tecomet Inc.

- Tegra Medical

- Velocity Medtech

- Viant

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Outsourced Orthopedic Manufacturing Market

- In January 2024, Medtronic plc, a global leader in healthcare solutions, announced the launch of its new Orthopedic Innovation Lab in Ireland. This state-of-the-art facility is dedicated to the research, design, and manufacturing of orthopedic implants and instruments, expanding Medtronic's global footprint in outsourced orthopedic manufacturing (Medtronic Press Release, 2024).

- In March 2024, Stryker Corporation, a leading medical technology company, entered into a strategic partnership with 3D Systems, a provider of 3D printing technologies. The collaboration aimed to accelerate the development and production of 3D-printed orthopedic implants, demonstrating Stryker's commitment to technological advancements in the outsourced orthopedic manufacturing sector (3D Systems Press Release, 2024).

- In May 2024, Smith & Nephew, a global medical device manufacturer, completed the acquisition of Osactis, a French orthopedic implant manufacturer. This acquisition significantly expanded Smith & Nephew's presence in the European orthopedic market and added Osactis' advanced manufacturing capabilities to its portfolio (Smith & Nephew Press Release, 2024).

- In April 2025, the U.S. Food and Drug Administration (FDA) granted 510(k) clearance to Zimmer Biomet Holdings, Inc. For its new, advanced robotic-assisted surgical system for total knee arthroplasty. This approval marked a significant milestone in the adoption of robotics in outsourced orthopedic manufacturing and surgery, paving the way for more advanced and precise implant production (Zimmer Biomet Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Outsourced Orthopedic Manufacturing Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

208 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.1% |

|

Market growth 2025-2029 |

USD 3280.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.7 |

|

Key countries |

US, Germany, UK, China, Canada, India, France, Japan, South Korea, and Australia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by advancements in technologies such as 3D printing and additive manufacturing for implant manufacturing. Surface treatments and material certifications play a crucial role in ensuring the biocompatibility and durability of orthopedic components. Risk management and inventory management are essential components of medical device outsourcing, with sterile processing and sterilization validation ensuring the safety and efficacy of surgical instruments and implants. Forging titanium alloys and precision machining remain key processes in orthopedic implant manufacturing, while product lifecycle management and quality assurance ensure the smooth transition from design to production. Component inspection, design transfer, and regulatory compliance are critical aspects of the outsourcing process, with regulatory submissions and packaging validation ensuring the readiness of products for market.

- One example of market dynamics at play is a leading orthopedic manufacturer increasing sales by 15% through the adoption of advanced manufacturing technologies and improved supply chain management. The global orthopedic manufacturing market is expected to grow by over 5% annually, driven by the increasing demand for advanced orthopedic solutions and regulatory requirements. Quality control systems, contract manufacturing, process validation, and failure analysis are ongoing activities that ensure the continued success of outsourced orthopedic manufacturing partnerships. Biocompatible materials and materials engineering are at the forefront of innovation, driving the development of new and improved orthopedic implants and surgical instruments.

What are the Key Data Covered in this Outsourced Orthopedic Manufacturing Market Research and Growth Report?

-

What is the expected growth of the Outsourced Orthopedic Manufacturing Market between 2025 and 2029?

-

USD 3.28 billion, at a CAGR of 7.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Implants, Instruments, and Cases and trays), Material (Metal, Polymers, Ceramics, and Composites), and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Rising demand for orthopedic procedures, Stringent regulatory requirements

-

-

Who are the major players in the Outsourced Orthopedic Manufacturing Market?

-

Autocam Medical, Avalign Technologies Inc., Cretex Companies Inc., intech Medical SAS, LISI MEDICAL, Marle Group, Norman Noble Inc., Norwood Medical, Orchid MPS Holdings LLC, Paragon Medical, Resolve Surgical Technologies, SpiTrex Orthopedics, Tecomet Inc., Tegra Medical, Velocity Medtech, and Viant

-

Market Research Insights

- The market continues to evolve, with quality audits and supplier management playing crucial roles in ensuring compliance and cost reduction. According to industry reports, the market is expected to grow by 7% annually over the next decade. For instance, a leading orthopedic device manufacturer achieved a 10% increase in sales by optimizing its supply chain and implementing rigorous inspection protocols. This included computer-aided manufacturing techniques for yield improvement, wear testing, and biomechanical testing to enhance process capability and reduce defect rates.

- Furthermore, the adoption of advanced technologies such as statistical process control, investment casting, and powder metallurgy has led to significant improvements in production efficiency and corrosion resistance. Additionally, on-time delivery and implant fixation have become essential factors in maintaining customer satisfaction and market competitiveness.

We can help! Our analysts can customize this outsourced orthopedic manufacturing market research report to meet your requirements.

RIA -

RIA -