Peripheral Guidewires Market Size 2025-2029

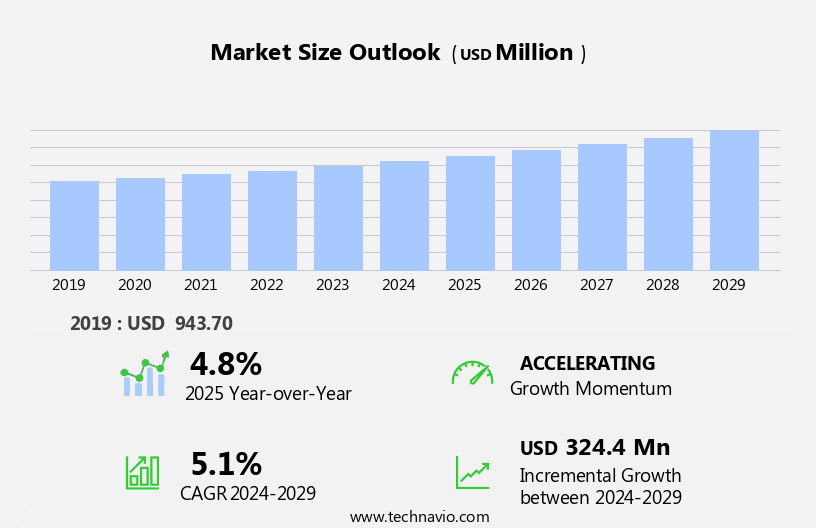

The peripheral guidewires market size is forecast to increase by USD 324.4 million, at a CAGR of 5.1% between 2024 and 2029.

- The market is experiencing significant growth, driven primarily by the increasing demand for Minimally Invasive (MI) procedures in various medical applications. The adoption of MI procedures is on the rise due to their numerous benefits, including reduced recovery time, minimal scarring, and improved patient outcomes. The advanced medical technologies used in these devices offer several advantages over traditional radial and femoral access methods, making them a preferred choice for hospitals and healthcare providers. Advances in guidewire technology are another key driver for market growth. Innovations such as shape memory alloys, hydrophilic coatings, and radiopaque materials are enhancing the functionality and performance of guidewires, making them increasingly indispensable in the medical field.

- Compliance with these regulations can be costly and time-consuming, potentially hindering the entry of new players and limiting product innovation. Companies seeking to capitalize on market opportunities must navigate these regulatory hurdles effectively while continuously innovating to meet the evolving needs of healthcare providers and patients. Regulations and standards govern their design, manufacturing, and sterilization to ensure patient safety and efficacy.

What will be the Size of the Peripheral Guidewires Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The market, a segment of medical technology, is experiencing significant growth due to the increasing prevalence of peripheral vascular disease and the demand for minimally invasive neurovascular and peripheral interventional procedures. Medical device design plays a crucial role in advancing neurovascular intervention, with innovations in medical imaging and image-guided interventions enabling more precise vascular access and procedure execution. Medical device manufacturers prioritize safety and efficacy in the development of vascular grafts, closure devices, and drug-eluting stents for peripheral vascular intervention. Regulatory compliance is essential, with medical device certification ensuring adherence to stringent safety standards.

- Cost-effective manufacturing processes are essential to maintaining competitiveness in the medical device market. Balloon angioplasty and endovascular procedures continue to be popular treatment options for peripheral vascular disease, with ongoing research focusing on improving medical device safety and efficacy. In the realm of interventional cardiology, medical innovation is driving advancements in vascular access techniques and bioresorbable stents, further expanding the scope of minimally invasive surgery. Medical imaging technology continues to play a pivotal role in guiding these procedures, ensuring optimal outcomes for patients.

How is this Peripheral Guidewires Industry segmented?

The peripheral guidewires industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

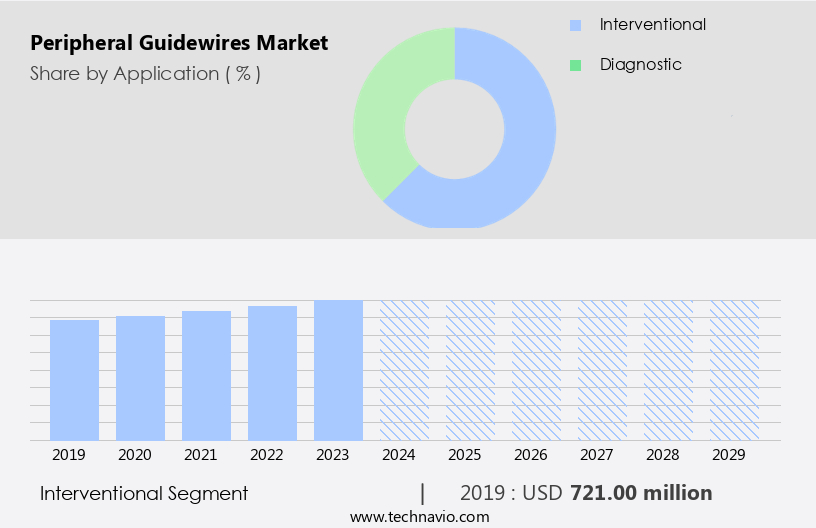

- Application

- Interventional

- Diagnostic

- End-user

- Cardiac catheterization laboratories

- Hospitals

- Others

- Material

- Stainless steel

- Nitinol

- Hybrid materials

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The interventional segment is estimated to witness significant growth during the forecast period. The market experienced significant growth in 2024, driven by the increasing prevalence of cardiovascular diseases and the rising demand for minimally invasive procedures. Peripheral guidewires play a crucial role in facilitating interventional procedures by providing access to target vessels and enabling the delivery of therapeutic devices. These guidewires are available in various sizes, with the most commonly used diameters being 0.014, 0.018, and 0.035 inches. The benefits of peripheral guidewires include improved navigation, enhanced tracking, and increased safety during interventions. Their strength and durability ensure smooth insertion and maneuverability, while their coatings provide lubrication and resistance to wear and tear.

Patents and ongoing research continue to drive innovation in guidewire technology, leading to advancements in tip design, material, and biocompatibility. Manufacturers prioritize safety and certification to ensure the highest standards in guidewire production. The market trends toward smaller, more flexible guidewires to accommodate complex procedures and anatomies. Alternatives, such as microcatheters and balloon-guided catheters, offer additional options for interventionalists. Peripheral guidewires are used in various applications, including peripheral arterial interventions, neurovascular interventions, and interventional oncology. Despite their advantages, limitations such as cost and potential complications persist, necessitating ongoing research and development. However, the market faces challenges from stringent regulatory frameworks governing medical devices.

The Interventional segment was valued at USD 721.00 million in 2019 and showed a gradual increase during the forecast period.

The peripheral guidewires market is advancing with innovations in guidewire strength, guidewire biocompatibility, and guidewire tracking to enhance precision in medical procedures. Improved guidewire lubrication and specialized guidewire coatings optimize performance while ensuring smooth guidewire insertion. Strict guidewire sterilization processes uphold safety standards, alongside variations in guidewire length, guidewire material, and guidewire shape tailored for specific applications. Enhanced guidewire resistance, guidewire durability, and guidewire performance drive reliability. Factors like guidewire cost, guidewire approval, and adherence to guidewire standards and guidewire regulations influence market adoption. Ongoing guidewire patents, guidewire innovation, guidewire research, and guidewire development fuel advancements. The growing focus on guidewire applications, guidewire uses, and guidewire benefits supports guidewire market growth, aligning with evolving guidewire market trends.

Regional Analysis

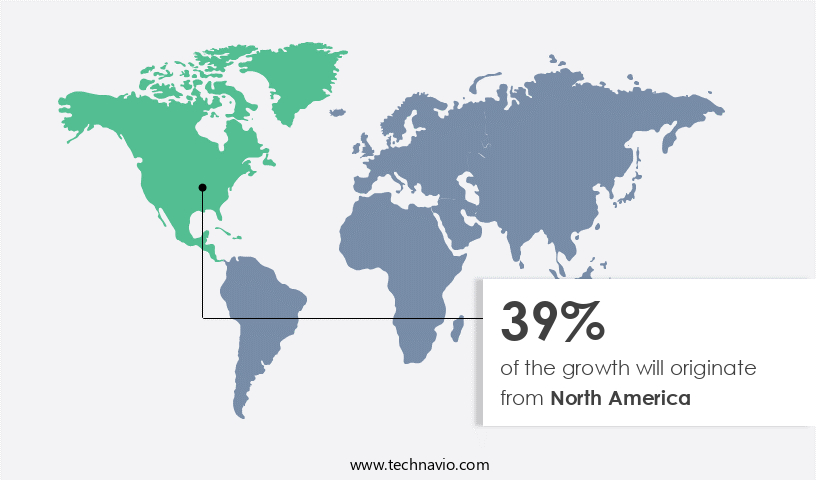

North America is estimated to contribute 39% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is experiencing significant growth due to the increasing prevalence of peripheral vascular diseases (PVD), including abdominal aortic aneurysms (AAA) and carotid artery stenosis (CAS). In 2024, North America led the market with the US being the major revenue contributor. Peripheral guidewires play a crucial role in interventional procedures for treating PVD. This trend is fueling the demand for advanced guidewires that enable efficient and precise navigation during these procedures. Factors such as high blood pressure, high cholesterol, atherosclerosis, and smoking contribute to the development of these conditions. In Canada, heart disease is the second-leading cause of death. Dedicated societies and associations, like the Canadian Society for Vascular Surgery, promote vascular health through research, education, advocacy, and collaboration, thereby increasing awareness about vascular diseases.

Guidewires offer benefits such as improved flexibility, enhanced performance, and precise navigation. Their strength and durability are crucial for successful interventions. Patents and ongoing research continue to drive innovation in guidewire design, resistance, lubrication, and biocompatibility. Manufacturers prioritize safety and cost-effectiveness while ensuring certification and sterilization. Guidewires come in various diameters, coatings, and lengths, catering to diverse applications. Despite advancements, limitations such as potential complications and resistance to certain materials remain. Market trends include the development of thinner, more flexible guidewires, as well as those with advanced coatings and tracking systems. Alternatives, such as catheters and drug-eluting stents, also impact the market.

Regulations and standards ensure the quality and safety of guidewires, while their shape and design continue to evolve to address specific clinical needs. Overall, the market is dynamic, driven by the growing need to address PVD and improve patient outcomes. Transradial access devices have gained significant traction in the market due to the increasing number of cardiovascular diseases (CVDs) and the subsequent rise in percutaneous coronary intervention (PCI) procedures.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Peripheral Guidewires market drivers leading to the rise in the adoption of Industry?

- The significant increase in demand for Minimally Invasive (MI) procedures serves as the primary growth driver for the market. Peripheral guidewires play a crucial role in minimally invasive (MI) procedures, which have gained significant traction due to their numerous advantages over traditional surgical methods. These advantages include reduced infection risks, fewer complications, shorter hospital stays, and faster recovery times. As MI procedures continue to replace conventional surgeries and laparoscopic techniques for various treatments, the demand for peripheral guidewires is poised for growth. The strength and durability of guidewires are essential factors in ensuring precision during interventional procedures. Innovations in guidewire technology have led to the development of advanced materials and designs, enhancing their performance and versatility.

- Furthermore, ongoing research and development efforts have led to the filing of numerous patents for guidewire technology, securing intellectual property and fostering competition in the market. Market trends indicate a growing emphasis on improving patient outcomes while reducing healthcare costs. Peripheral guidewires' ability to facilitate accurate and efficient access to peripheral vessels aligns with this trend, making them an essential component of the MI procedure toolkit. The benefits of MI procedures, coupled with the continuous advancements in guidewire technology, are expected to drive the growth of the peripheral guidewire market.

What are the Peripheral Guidewires market trends shaping the Industry?

- Advances in guidewire technology are currently shaping the market trend. This innovation is driven by professional developments in medical devices, ensuring improved patient care and outcomes. In the market, manufacturers are prioritizing innovation to enhance clinical outcomes and diagnostic experiences for end-users. New opportunities are arising due to the introduction of advanced guidewires boasting features such as super elasticity, customized shapes, and maximal deflection. One example of these advanced guidewires is Merit Medical Systems' Laureate Hydrophilic Guide Wires.

- Manufacturers' focus on guidewire safety, certification, and cost-effective manufacturing processes also contributes to market growth. The development of guidewire navigation and tracking systems further enhances the market's potential. This latest peripheral guidewire boasts a hydrophilic technology coating, which maintains a constant fluid layer on the wire surface for optimal lubrication and durability. The superior lubricity enables the guidewire to traverse even the most complex lesions, ensuring successful outcomes in challenging interventional and diagnostic procedures. Diagnostic angiography and peripheral vascular interventions are other areas where transradial access devices have gained popularity.

How does Peripheral Guidewires market face challenges during its growth?

- Lack of skilled vascular surgeons is the main challenge that the market is facing. Currently, shortage of vascular surgeons poses a potential threat to the adoption of vascular specialties in the management of vascular diseases. The excessive workload also compels many surgeons to retire even before they reach the age of retirement.Hence, a greater number of trainees are required to fill up the vacancies and take up the positions vacated by the retiring vascular surgeons to keep up with the demand for the treatment of vascular diseases. Also, though interventional cardiologists have the technical skills required to perform non-coronary vascular interventional procedures, they lack a comprehensive knowledge of vascular medicine.

-

Therefore, training programs should be carried out to fill this knowledge gap so that interventional cardiologists can also perform peripheral vascular procedures effectively.Therefore, the shortage of skilled vascular surgeons can be detrimental to the demand for peripheral guidewires, as, without surgeons, the number of vascular surgeries and procedures would fall significantly and ultimately hamper the growth of the global peripheral guidewires market during the forecast period.

Exclusive Customer Landscape

The peripheral guidewires market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the peripheral guidewires market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, peripheral guidewires market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - The company specializes in providing advanced guidewires for medical interventions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Asahi Intecc Co. Ltd.

- B.Braun SE

- Becton Dickinson and Co.

- BIOTRONIK SE and Co. KG

- Boston Scientific Corp.

- Conmed Corp.

- Cook Group Inc.

- Cordis Corp.

- EPflex Feinwerktechnik GmbH

- Haemonetics Corp.

- Heraeus Holding GmbH

- Integer Holdings Corp.

- Medtronic Plc

- Merit Medical Systems Inc.

- MicroPort Scientific Corp.

- Stryker Corp.

- Teleflex Inc.

- Terumo Corp.

- Tianjin Demax Medical Technology Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Peripheral Guidewires Market

- In February 2023, Medtronic, a leading medical technology company, announced the launch of its new Envision Peripheral Guidewire portfolio. This innovative product line includes five new guidewires designed to improve tracking and deliver precise lesion access in peripheral interventions (Medtronic Press Release, 2023).

- In May 2024, Boston Scientific and Merit Medical entered into a strategic collaboration to co-develop and commercialize a new generation of peripheral guidewires. This partnership aims to leverage Boston Scientific's interventional expertise and Merit Medical's guidewire manufacturing capabilities to create advanced guidewires for peripheral vascular procedures (Boston Scientific Press Release, 2024).

- In October 2024, Terumo Corporation completed the acquisition of Arterioscan, a leading manufacturer of intravascular imaging systems and peripheral guidewires. This acquisition will expand Terumo's product portfolio and strengthen its position in the peripheral interventions market (Terumo Press Release, 2024).

- In January 2025, Abbott Laboratories received FDA approval for its new Absolute Quadra Guidewire, a next-generation peripheral guidewire with advanced tip technologies for improved tracking and maneuverability. This approval marks a significant milestone in Abbott's efforts to expand its portfolio and enhance its presence in the peripheral interventions market (Abbott Laboratories Press Release, 2025).

Research Analyst Overview

The market continues to evolve, driven by advancements in technology and growing applications across various medical sectors. These thin, flexible tubes play a crucial role in guiding catheters and other medical devices through the body's vasculature. Guidewire diameter and coatings are essential considerations, with manufacturers constantly innovating to improve guidewire flexibility, performance, and biocompatibility. Guidewire certification ensures adherence to stringent safety and quality standards, while guidewire manufacturing processes continue to refine production methods for enhanced durability and resistance. Guidewire safety remains a top priority, with ongoing research focusing on reducing complications during insertion and navigation.

Cost-effective solutions are also in demand, as guidewires are an essential component in numerous medical procedures. Guidewire navigation and tracking technologies continue to advance, enabling more precise and efficient interventions. The guidewire tip, a critical component, is engineered for optimal performance and maneuverability. As the market landscape unfolds, guidewire alternatives and regulations emerge, shaping the competitive landscape. Ongoing research and development efforts aim to enhance guidewire design, lubrication, and material properties, further expanding their applications and benefits.

Peripheral guidewires are essential tools in the medical devices industry, used in various interventional procedures to access and navigate complex vascular structures. These Class II medical devices are subject to additional special controls under US regulations, ensuring their safety and effectiveness. The Food and Drug Administration (FDA) mandates compliance with various regulations, including registration and listing (21 CFR Part 807), medical device reporting (21 CFR 803), labeling (21 CFR Part 801), and Good Manufacturing Practices (GMP). Additionally, electronic product radiation control provisions apply if applicable. Guidance documents, device tracking, and post-market surveillance are also essential components of the control system. Guidewire design and development prioritize flexibility, resistance, and performance to cater to diverse clinical applications. The shape and material of guidewires vary based on the intended use, ensuring optimal maneuverability and compatibility with other medical devices. Adhering to these regulations and maintaining high-performance standards is crucial for the success and acceptance of peripheral guidewires in the medical industry. The FDA's regulatory framework encompasses performance standards, such as those set by the American Standards Association (ASA), International Organization for Standardization (ISO), and American Society for Testing and Materials (ASTM).

The Peripheral Guidewires Market is expanding as advancements in neurovascular procedures drive demand for precision and reliability. The integration of vascular closure devices enhances procedural outcomes, ensuring safety and efficiency. Innovations in medical device manufacturing improve guidewire quality and functionality, while strict medical device regulation maintains industry standards. Evaluating medical device efficacy ensures optimal performance, influencing adoption across healthcare settings. Cost-effectiveness remains crucial, with medical device cost shaping purchasing decisions. The growing role of healthcare technology supports intelligent solutions, enhancing guidewire tracking and usability.

Dive into Technavio's strong research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Peripheral Guidewires Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

221 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.1% |

|

Market growth 2025-2029 |

USD 324.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.8 |

|

Key countries |

US, Canada, Germany, China, UK, France, Japan, Brazil, Mexico, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Peripheral Guidewires Market Research and Growth Report?

- CAGR of the Peripheral Guidewires industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the peripheral guidewires market growth of industry companies

We can help! Our analysts can customize this peripheral guidewires market research report to meet your requirements.

RIA -

RIA -