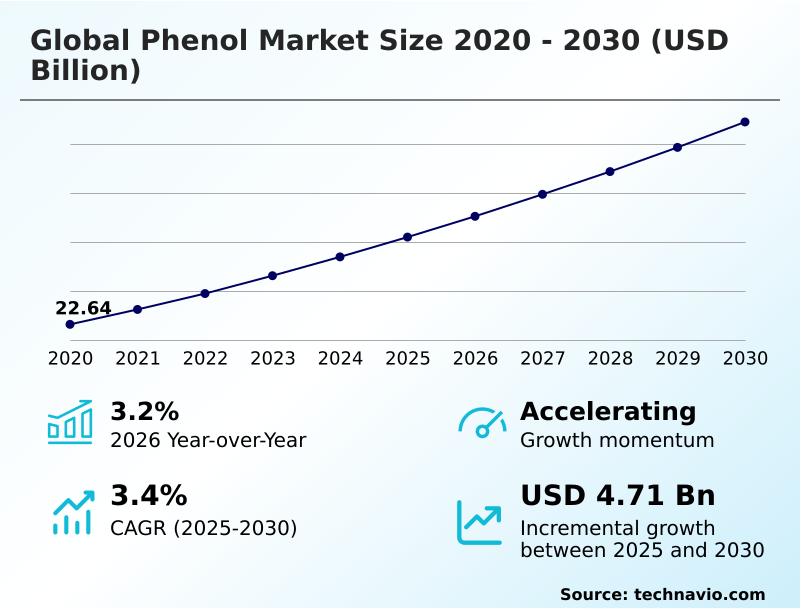

Phenol Market Size 2026-2030

The phenol market size is valued to increase by USD 4.71 billion, at a CAGR of 3.4% from 2025 to 2030. Robust demand for BPA as primary growth catalyst will drive the phenol market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 62.9% growth during the forecast period.

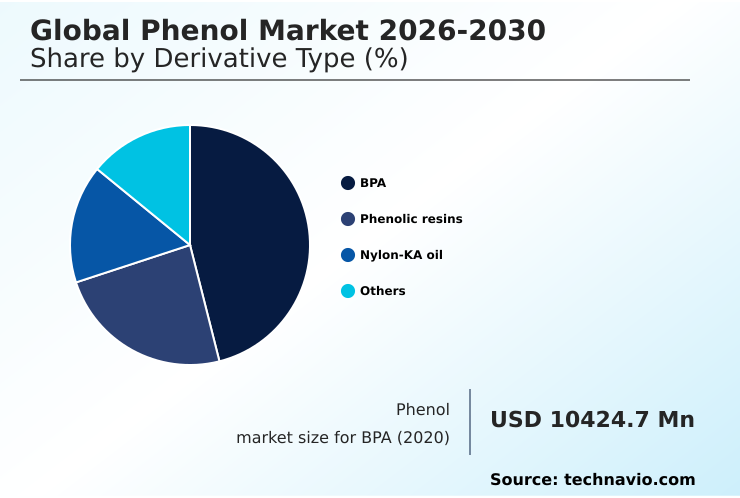

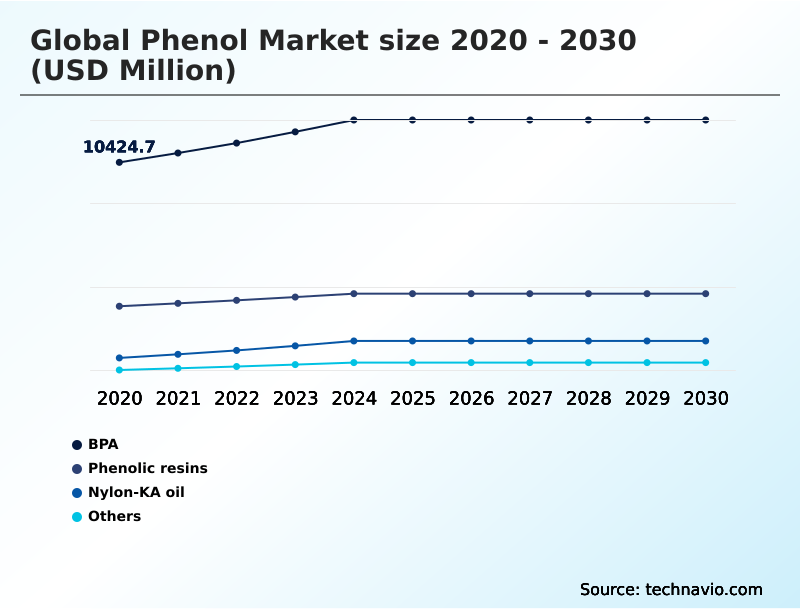

- By Derivative Type - BPA segment was valued at USD 11.90 billion in 2024

- By End-user - Chemical segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 8.28 billion

- Market Future Opportunities: USD 4.71 billion

- CAGR from 2025 to 2030 : 3.4%

Market Summary

- The phenol market is undergoing a significant transformation, shaped by the robust demand for its derivatives in high-performance applications and a strategic shift in global production capacities. Key drivers include the extensive use of polycarbonate and epoxy resins in the automotive and electronics sectors, which rely on phenol as a foundational chemical intermediate.

- Concurrently, the industry is navigating the trend toward sustainable manufacturing, with research into bio-based alternatives gaining traction to mitigate environmental impact. However, the market contends with challenges such as pronounced feedstock price volatility and structural oversupply in certain regions, which pressures profit margins.

- A typical business scenario involves a derivative manufacturer implementing advanced analytics to optimize its supply chain, enabling it to better forecast raw material price fluctuations and adjust production schedules, thereby improving operational efficiency and cost control in a competitive environment. This dynamic interplay of demand, innovation, and economic pressures defines the current landscape.

What will be the Size of the Phenol Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Phenol Market Segmented?

The phenol industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Derivative type

- BPA

- Phenolic resins

- Nylon-KA oil

- Others

- End-user

- Chemical

- Construction

- Automotive

- Electronic communication

- Others

- Channel

- Indirect sale

- Direct sale

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- France

- UK

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- Turkey

- UAE

- Rest of World (ROW)

- APAC

By Derivative Type Insights

The bpa segment is estimated to witness significant growth during the forecast period.

The global phenol market is segmented by derivative type, end-user, and geography. The bisphenol-a (bpa) segment is the largest, accounting for approximately 47% of phenol applications.

As a critical monomer, bpa is essential for producing high-performance materials like polycarbonate and epoxy resins, which are integral to numerous end-use industries.

The downstream demand for these phenol derivatives, including laminates, is driven by their use in automotive, electronics, and construction sectors. The synthesis of this aromatic organic compound through processes like hydrogenation underpins its role as a foundational industrial chemical.

This segmentation highlights the market's dependence on the performance of key industrial manufacturing outputs and the extensive reach of phenol's versatile applications.

The BPA segment was valued at USD 11.90 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 62.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Phenol Market Demand is Rising in APAC Get Free Sample

The global phenol market is experiencing a profound geographic realignment, driven by shifting regional dynamics. The APAC region, particularly China, has become the dominant force, with new petrochemical infrastructure investments leading to superior operational efficiency.

This expansion alters global trade flows and reshapes the commodity chemicals market. In contrast, producers in North America and Europe are focusing on high-value derivatives such as alkylphenols and materials for semiconductor encapsulation and printed circuit boards (PCBs).

This strategic pivot leverages advanced synthesis process capabilities and feedstock integration to enhance supply chain resilience. Navigating this evolving manufacturing footprint and ensuring regulatory compliance across jurisdictions is essential for maintaining a competitive edge.

This shift underscores a broader trend where operational footprint alignment with demand centers is critical.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global phenol market is navigating a complex environment defined by specific end-use demands and production challenges. The primary application remains bisphenol-a for polycarbonate manufacturing, a cornerstone for durable goods. Concurrently, the use of phenolic resins in construction materials provides a stable, high-volume demand stream.

- In specialty areas, caprolactam for nylon 6 synthesis and alkylphenols for industrial surfactants showcase the material's versatility. Key growth sectors include phenol applications in automotive components and epoxy resins for protective coatings, while phenol use in electronic communication is driven by miniaturization.

- The push for sustainability trends in phenol production is evident in the exploration of bio-based phenol production from lignin. Operationally, firms are focused on managing feedstock price volatility and the efficiency of the cumene process, which remains the dominant production route.

- The impact of regulations on phenol manufacturing is forcing investment in cleaner technologies, which can represent over 15% of new plant capital expenditure compared to older designs. The competitive landscape for phenol producers is intensifying due to phenol market oversupply challenges, making strategic sourcing of benzene and propylene critical.

- This has led to a regional shift in phenol consumption toward areas with lower production costs. Businesses are now focused on optimizing phenol plant utilization rates and leveraging phenol as a chemical intermediate for higher-margin products, including its role in pharmaceutical synthesis and for creating specialty polymers.

What are the key market drivers leading to the rise in the adoption of Phenol Industry?

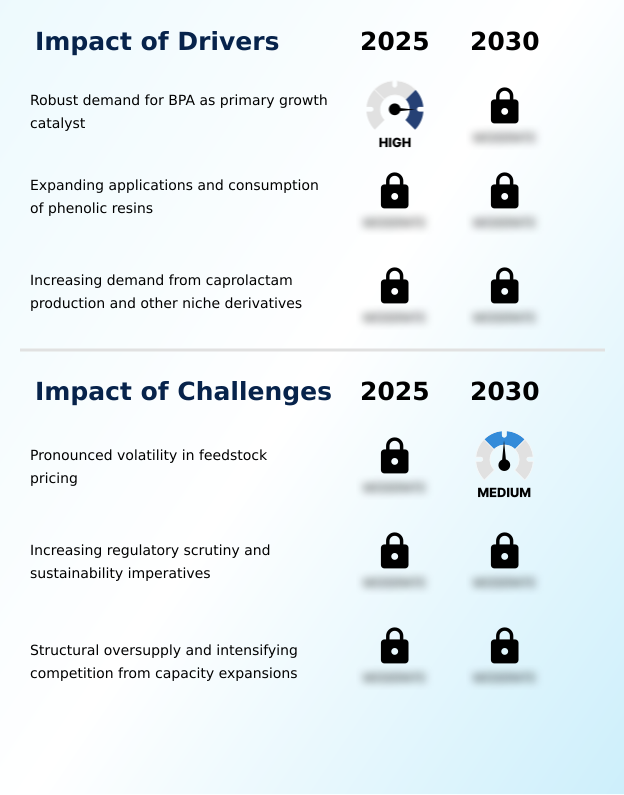

- Robust demand for bisphenol a (BPA) serves as a primary catalyst for growth in the phenol market.

- The phenol market's growth is fundamentally driven by sustained downstream demand across the petrochemical value chain.

- The cumene process remains the cornerstone of phenol production, supplying the essential chemical intermediate for derivatives like caprolactam, which undergoes polymerization to create nylon 6. This material's use in applications from textiles to automotive components highlights the market's reach.

- The demand for industrial additives and industrial lubricants also contributes steadily. Technological advancement in chemical synthesis and catalytic process optimization is boosting production capacity, with some modernized plants improving yields by up to 3%.

- This focus on efficiency in the synthesis process is crucial for producing high-performance materials and friction materials for various end-use industries.

What are the market trends shaping the Phenol Industry?

- The expansion of applications for phenolic resins reinforces foundational demand. This development is emerging as a significant market trend.

- Key trends are reshaping the global phenol market, driven by a strategic shift towards sustainability and value-added applications. The development of bio-based phenol from lignin feedstock is moving from niche research to a viable component of the circular economy framework.

- This push for sustainable manufacturing and green chemistry is influencing the asset portfolio of major producers, with some achieving a 5% reduction in carbon footprint through process innovations. Simultaneously, the expanding use of high-performance thermosetting polymers and wood adhesives in construction provides foundational demand.

- This strategic realignment allows producers to adjust their operational footprint away from commoditized segments toward specialty chemicals, enhancing market competitiveness. Such diversification within the value chain analysis is critical for long-term stability.

What challenges does the Phenol Industry face during its growth?

- Pronounced volatility in feedstock pricing presents a significant challenge to the growth of the phenol industry.

- Significant challenges in the phenol market stem from structural economic pressures and operational complexities. The primary issue is feedstock volatility, with unpredictable price instability for benzene and propylene creating severe margin compression. This forces a relentless focus on cost optimization and supply chain optimization to protect profitability.

- The reliance on petroleum derivatives for raw material sourcing exposes producers to geopolitical and market-driven price shocks. In response, some firms with strong vertical integration report a 10% greater stability in input costs compared to those without. However, widespread oversupply leads to low capacity utilization, sometimes falling below 80% during economic downturns, which intensifies competition and leads to asset rationalization.

- Managing this difficult balance of high operational expenditure and pricing pressure is a defining characteristic of the current market.

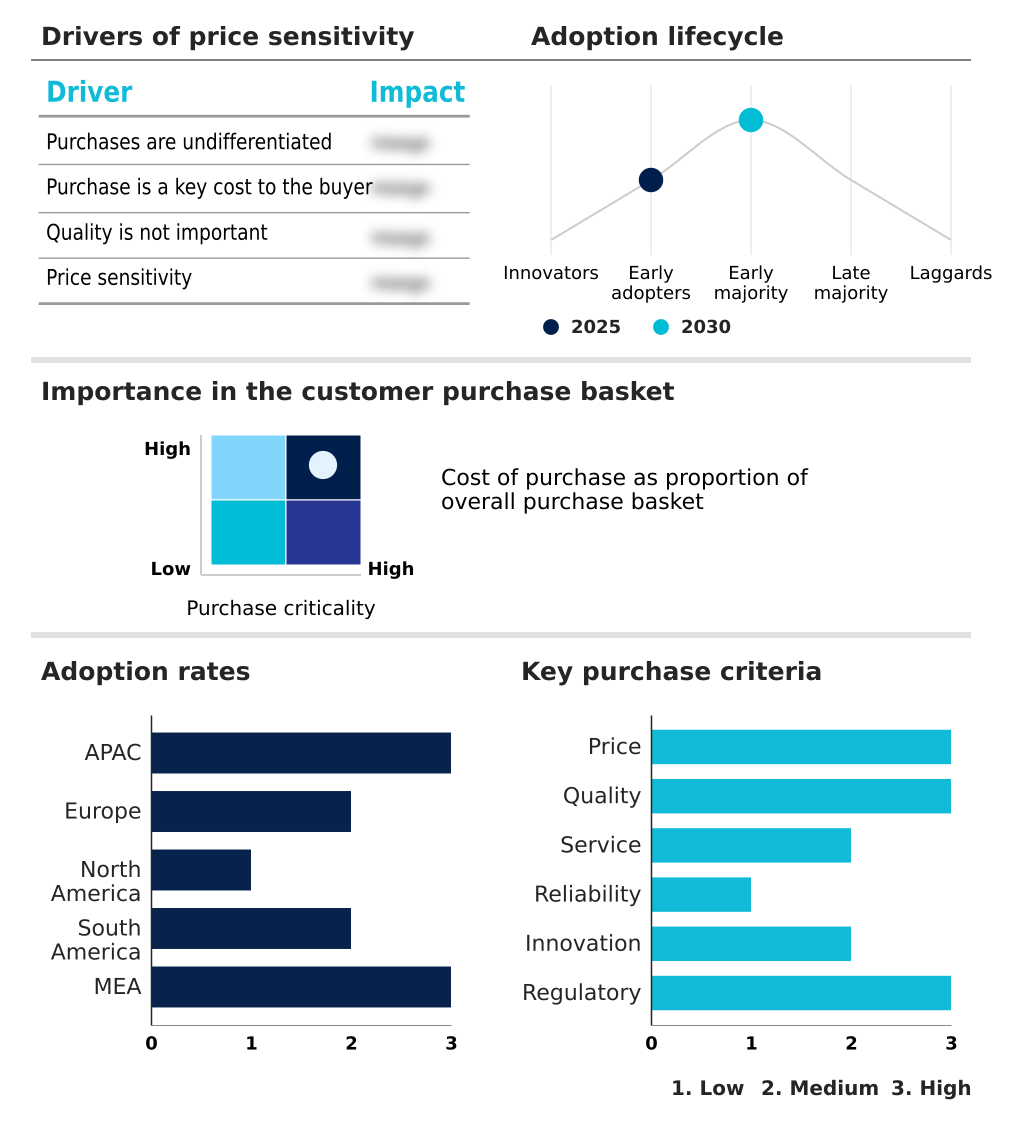

Exclusive Technavio Analysis on Customer Landscape

The phenol market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the phenol market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Phenol Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, phenol market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AdvanSix Inc. - Phenol offerings for bisphenol-a and phenolic resins are key to industrial applications, supporting diverse manufacturing of specialty chemicals and high-performance materials.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AdvanSix Inc.

- ALTIVIA

- BASF SE

- Chang Chun Group

- Deepak Nitrite Ltd.

- Domo Chemicals GmbH

- Formosa Chemicals and Fibre Corp

- Honeywell International Inc.

- INEOS Group Holdings S.A.

- Kumho Chemicals Inc.

- LG Chem Ltd.

- Mitsui Chemicals Inc.

- MOEVE S.A.

- Nanjing Chemical Material Corp

- PTT Global Chemical Public Co.

- Sasol Ltd.

- Shell plc

- Solvay SA

- The Mitsubishi Chemical Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Phenol market

- In November 2024, Haldia Petrochemicals Ltd. announced an additional investment to augment its Haldia facility's phenol production capacity, with completion expected in the first quarter of 2026.

- In January 2025, INEOS Phenol announced a significant capital investment to expand its production facility in Mobile, Alabama, to meet growing North American demand from the automotive and construction industries.

- In April 2025, Sinopec and INEOS confirmed their joint venture to construct China's largest phenol and acetone facility in Nanjing, with an annual capacity of at least 400,000 tons of phenol.

- In April 2025, Orlen declared its intention to discontinue phenol and acetone production at its Plock, Poland petrochemical site by the end of the year as part of a strategic realignment.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Phenol Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 314 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.4% |

| Market growth 2026-2030 | USD 4705.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.2% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, Germany, Russia, France, UK, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Colombia, Saudi Arabia, Turkey, UAE, South Africa and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The phenol market is defined by a strategic recalibration of global supply chains and a heightened focus on production economics. The industry is moving beyond its reliance on traditional end-use industries by advancing green chemistry initiatives, such as developing bio-based phenol from lignin feedstock.

- This transition toward sustainable manufacturing is creating a new competitive paradigm where the ability to innovate within a circular economy framework is as critical as cost optimization. This shift directly influences boardroom decisions on capital allocation, with investments in green technologies now a key part of long-term strategy to ensure market competitiveness and de-risk the asset portfolio from feedstock volatility.

- In this landscape, operational efficiency and a resilient manufacturing footprint are paramount. For instance, companies adopting advanced catalytic process technologies have reported improvements in yield and energy consumption, leading to a more favorable operational expenditure profile. The strategic realignment of production capacity toward high-growth regions reflects a fundamental adaptation to evolving downstream demand and global trade flows.

What are the Key Data Covered in this Phenol Market Research and Growth Report?

-

What is the expected growth of the Phenol Market between 2026 and 2030?

-

USD 4.71 billion, at a CAGR of 3.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Derivative Type (BPA, Phenolic resins, Nylon-KA oil, and Others), End-user (Chemical, Construction, Automotive, Electronic communication, and Others), Channel (Indirect sale, and Direct sale) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Robust demand for BPA as primary growth catalyst, Pronounced volatility in feedstock pricing

-

-

Who are the major players in the Phenol Market?

-

AdvanSix Inc., ALTIVIA, BASF SE, Chang Chun Group, Deepak Nitrite Ltd., Domo Chemicals GmbH, Formosa Chemicals and Fibre Corp, Honeywell International Inc., INEOS Group Holdings S.A., Kumho Chemicals Inc., LG Chem Ltd., Mitsui Chemicals Inc., MOEVE S.A., Nanjing Chemical Material Corp, PTT Global Chemical Public Co., Sasol Ltd., Shell plc, Solvay SA and The Mitsubishi Chemical Group

-

Market Research Insights

- The phenol market is characterized by complex dynamics where operational efficiency and strategic raw material sourcing are paramount. Within the petrochemical value chain, producers navigate significant price instability, with integrated firms often achieving a 10-15% cost advantage over non-integrated competitors.

- Adherence to stringent regulatory compliance for industrial chemical production has spurred technological advancement, leading to process optimizations that have reduced wastewater effluent by over 20% in modern facilities. The downstream demand for high-performance materials and phenol derivatives is reshaping global trade flows, forcing a strategic realignment of manufacturing footprints.

- Companies are increasingly focused on supply chain resilience to mitigate the effects of margin compression and ensure stable production capacity for diverse phenol applications across end-use industries.

We can help! Our analysts can customize this phenol market research report to meet your requirements.

RIA -

RIA -