Physical AI And Robotics-as-a-service Market Size 2026-2030

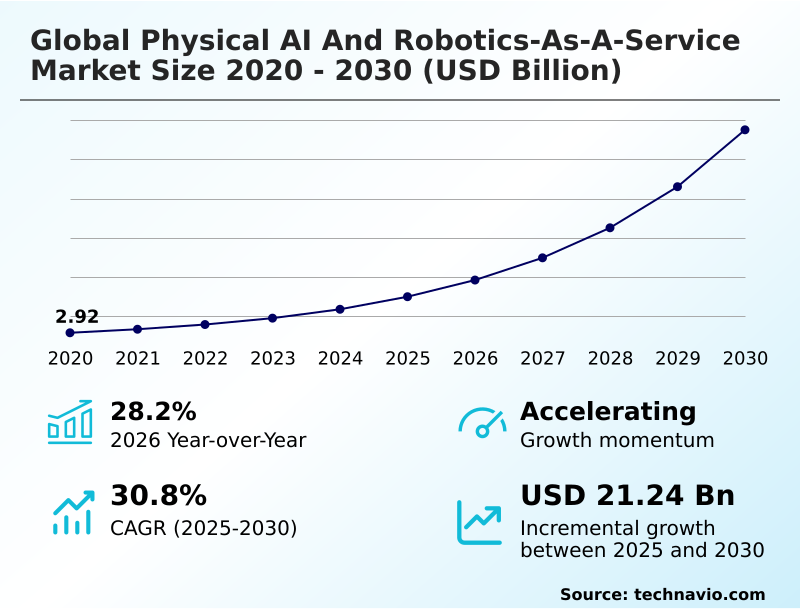

The physical ai and robotics-as-a-service market size is valued to increase by USD 21.24 billion, at a CAGR of 30.8% from 2025 to 2030. Proliferation of generative physical intelligence will drive the physical ai and robotics-as-a-service market.

Major Market Trends & Insights

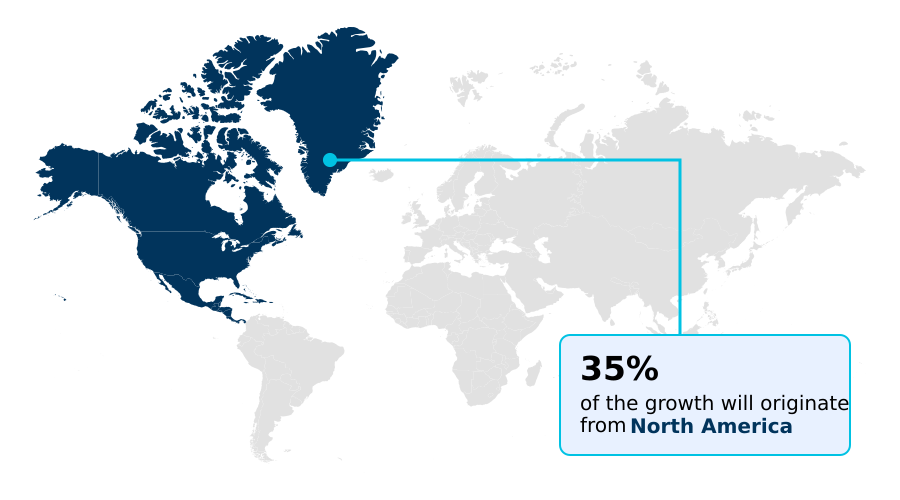

- North America dominated the market and accounted for a 35.2% growth during the forecast period.

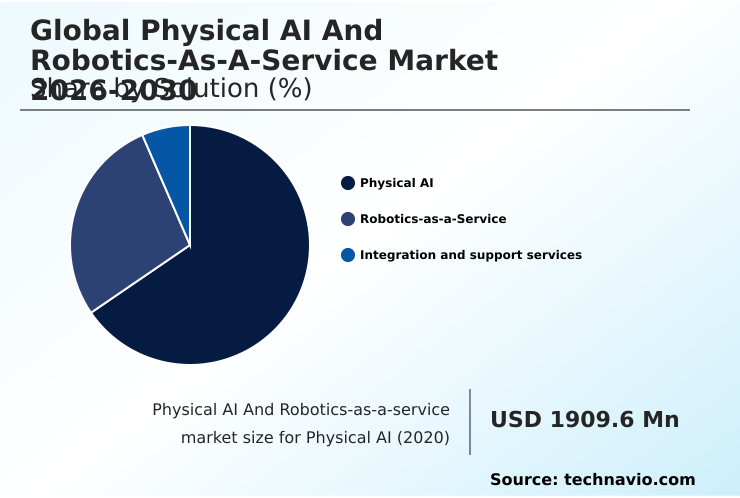

- By Solution - Physical AI segment was valued at USD 3.99 billion in 2024

- By Application - Logistics and warehousing segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 25.83 billion

- Market Future Opportunities: USD 21.24 billion

- CAGR from 2025 to 2030 : 30.8%

Market Summary

- The physical AI and robotics-as-a-service market is defined by the shift from capital-intensive hardware ownership to flexible, subscription-based robotics models. This evolution is propelled by the integration of advanced physical AI algorithms that enable autonomous mobile robots to perceive, learn, and navigate complex, real-world environments.

- Key trends include the push for interoperability standards to allow for seamless human-robot collaboration and the use of AI for supply chain resilience. For instance, a logistics company can leverage robotics-as-a-service for SMEs to dynamically scale its fleet during peak seasons, deploying additional robotic picking and sorting units to meet demand without long-term capital commitment, thus improving operational efficiency.

- However, the industry grapples with challenges such as high initial integration costs and a persistent talent deficit for managing these sophisticated systems. The convergence of cloud robotics platforms and edge computing is essential for enabling real-time decision-making, which is critical for applications in manufacturing and healthcare.

What will be the Size of the Physical AI And Robotics-as-a-service Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Physical AI And Robotics-as-a-service Market Segmented?

The physical ai and robotics-as-a-service industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

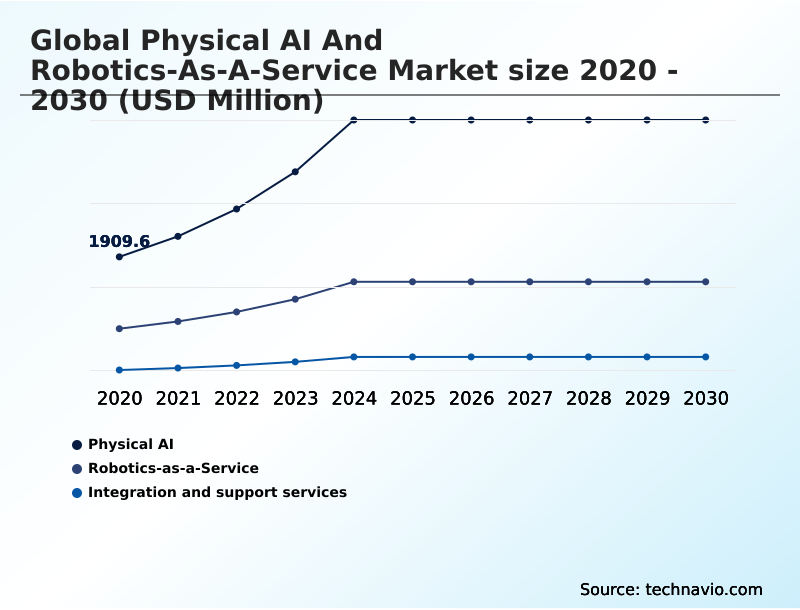

- Solution

- Physical AI

- Robotics-as-a-Service

- Integration and support services

- Application

- Logistics and warehousing

- Manufacturing and assembly

- Service and healthcare

- End-user

- Large enterprises

- SMEs

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Solution Insights

The physical ai segment is estimated to witness significant growth during the forecast period.

The physical AI segment is defined by the integration of advanced neural networks and proprietary physical ai algorithms directly into robotic hardware, creating intelligent hardware systems capable of autonomous operation.

This includes ai-enabled robotic solutions with sophisticated components such as high-performance neural processing units, advanced actuators, and specialized tactile sensing capabilities that facilitate real-time environmental perception.

The evolution of ai-orchestrated robotic systems is driven by the need for machines to navigate unstructured environments, using technologies like visual simultaneous localization and mapping to enable fluid interaction.

These collaborative robotic arms and mobile platforms utilize end-to-end neural network control for responsive decision-making.

As a result, deployments of this technology have demonstrated an 18% improvement in task completion rates in dynamic settings, pushing the boundaries of multi-robot fleet management and robotic perception technology.

The Physical AI segment was valued at USD 3.99 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Physical AI And Robotics-as-a-service Market Demand is Rising in North America Request Free Sample

The geographic landscape of the physical AI market is dynamic, with North America and APAC emerging as the two dominant regions, collectively accounting for nearly 70% of the market's incremental growth.

North America, contributing 35.2% of this growth, leverages its mature venture capital ecosystem to pioneer advanced applications. In contrast, APAC's expansion is fueled by large-scale manufacturing and government-led automation initiatives.

Key applications driving adoption include autonomous mobile robots and robotic piece-picking solutions in logistics, where cloud robotics platforms enable sophisticated robot fleet orchestration.

In healthcare, the use of raas in healthcare for tasks like autonomous cleaning machines is growing, improving sanitation efficiency by over 40%.

The deployment of autonomous service robots, supported by cobot integration services and advanced robotic manipulation systems, is becoming standard in high-growth areas, with physical intelligence systems providing the necessary adaptability.

Market Dynamics

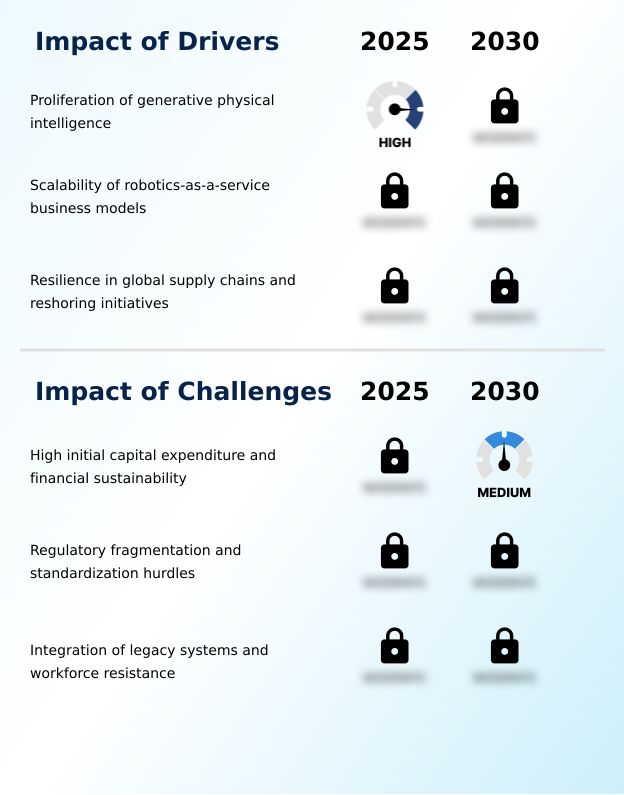

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The practical implementation of robotics-as-a-service for warehouse fulfillment is revolutionizing logistics, where subscription-based automation for smes allows smaller players to compete with established giants. The benefits of raas in supply chain management are clear, though organizations must still analyze the total cost of robotics-as-a-service implementation.

- For instance, deploying ai-driven inventory scanning robots and solutions for autonomous mobile picking and sorting can increase order accuracy by over 98%. In manufacturing, the use of ai-enabled robotic systems for manufacturing, particularly collaborative robots in assembly lines, enhances precision and throughput.

- The development of physical ai for unstructured environments and physical ai for last-mile delivery is expanding the technology's reach beyond controlled settings. This expansion relies on robust cloud management for autonomous mobile robots and advanced edge computing in physical ai to ensure low-latency performance. Key challenges include addressing physical ai and robotics-as-a-service security and solving the interoperability of mixed-fleet robotics.

- As the technology matures, general-purpose humanoid robot applications are moving from pilot stages to active deployment, especially with humanoid robots for logistics automation and robotics-as-a-service for healthcare logistics, driven by sophisticated end-to-end neural network for control and addressing robotics-as-a-service market challenges.

What are the key market drivers leading to the rise in the adoption of Physical AI And Robotics-as-a-service Industry?

- The proliferation of generative physical intelligence, which enables machines to interpret and execute complex tasks in unstructured environments, is the primary driver for market growth.

- The market's primary driver is the proliferation of generative physical intelligence, which enables embodied artificial intelligence to perform complex, non-repetitive tasks. This technological leap makes advanced physical AI applications viable across industries.

- The robotics-as-a-service model is a powerful accelerator, as its subscription-based robotics framework and flexible raas business models can lower market entry costs by over 50% for SMEs.

- This financial accessibility drives the adoption of ai-powered fulfillment solutions, autonomous warehouse automation, and specialized humanoid robots in manufacturing, where industrial robot subscriptions provide scalability. The ability of these systems to facilitate real-time decision-making allows for unprecedented operational agility.

- As a result, companies leveraging raas for SMEs report productivity gains of up to 30% within the first year of deployment, cementing the model's role in democratizing access to high-end automation.

What are the market trends shaping the Physical AI And Robotics-as-a-service Industry?

- The market is increasingly shaped by the emergence of edge-native orchestration, reflecting a broader trend toward decentralized robot intelligence.

- Key trends are reshaping the market, led by the shift toward edge-native orchestration and decentralized robot intelligence. This move to edge AI for robotics addresses critical latency issues in high-speed environments, reducing data processing delays by over 60% compared to purely cloud-based systems.

- Concurrently, the push for open-ecosystem orchestration and robust robotics middleware solutions is breaking down proprietary barriers, allowing for greater interoperability. This evolution toward software-defined manufacturing supports mixed-fleet deployments, which can improve overall operational efficiency by 20%. Furthermore, the integration of robot lifecycle management and stringent raas security frameworks is becoming standard.

- Innovations in generative AI in robotics are enhancing human-robot interaction safety, while the use of AI for supply chain resilience and ai-driven data capture provides businesses with unprecedented visibility and predictive capabilities, ensuring more sustainable and secure automated operations.

What challenges does the Physical AI And Robotics-as-a-service Industry face during its growth?

- High initial capital expenditure for advanced hardware and the challenge of ensuring long-term financial sustainability remain significant barriers to market adoption.

- Despite strong drivers, the market faces significant challenges, primarily the high initial capital expenditure and raas deployment challenges associated with hardware and integration. Integrating new platforms with legacy systems often results in technical debt and requires extensive enterprise resource planning integration, which can increase project timelines by up to 40%. A growing talent deficit for robotics management further complicates adoption.

- Another major hurdle is regulatory fragmentation; the lack of universal interoperability standards creates compliance burdens and hinders scalability, as providers must navigate disparate rules across key jurisdictions. This uncertainty, coupled with concerns over hardware obsolescence and the rapid cash-burn rates of startups, creates a challenging investment landscape that can slow the pace of innovation and widespread market adoption.

Exclusive Technavio Analysis on Customer Landscape

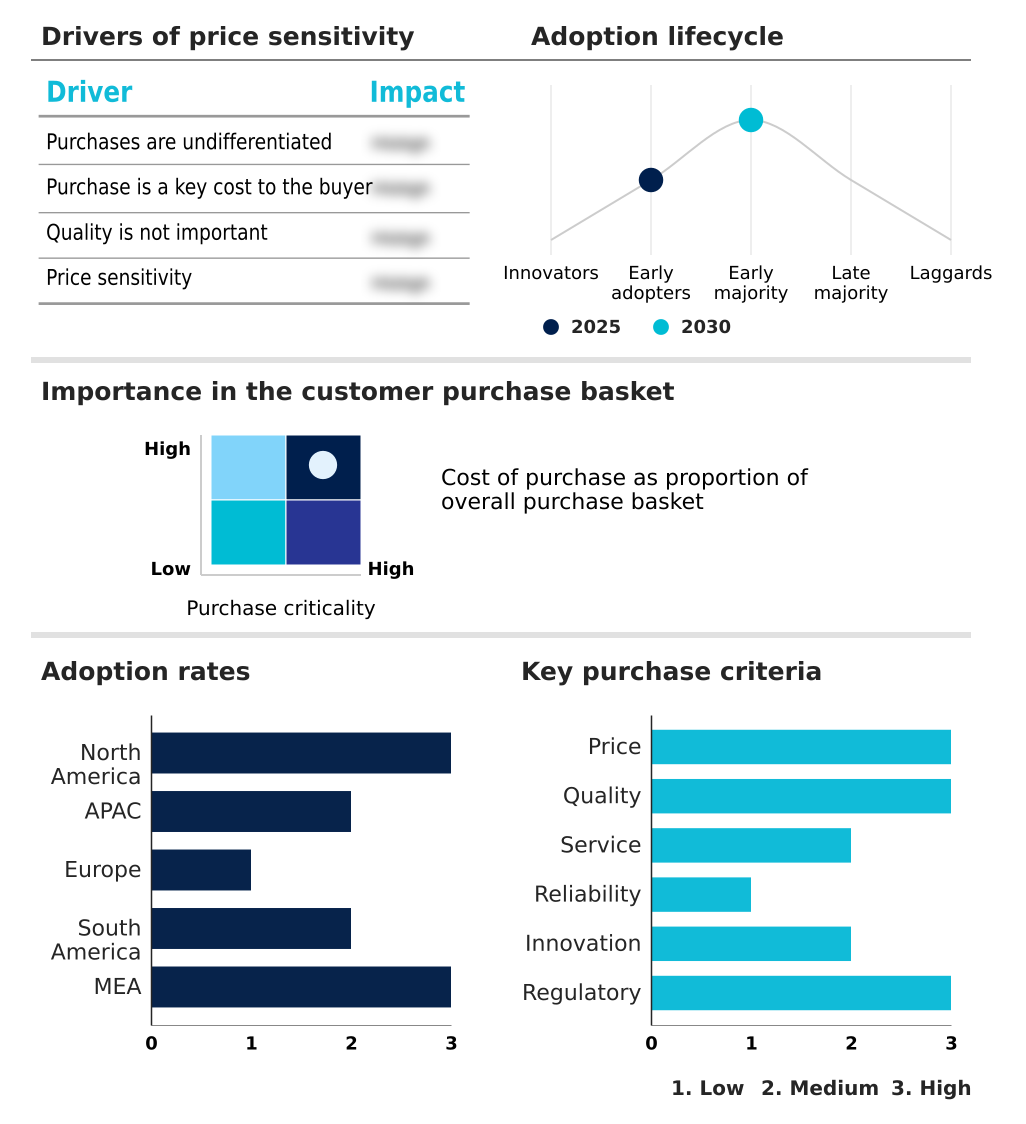

The physical ai and robotics-as-a-service market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the physical ai and robotics-as-a-service market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Physical AI And Robotics-as-a-service Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, physical ai and robotics-as-a-service market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agility Robotics Inc. - Offers advanced Isaac simulation platforms and edge AI hardware to train embodied agents, accelerating development in physical AI and robotics-as-a-service.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agility Robotics Inc.

- Bear Robotics, Inc.

- Berkshire Grey

- Boston Dynamics Inc.

- Brain Corp.

- Covariant

- Figure AI

- Formant

- Geekplus Technology Co. Ltd.

- IFS

- inVia Robotics Inc.

- Locus Robotics Corp.

- NVIDIA Corp.

- Qualcomm Inc.

- RightHand Robotics Inc.

- Symbotic Inc.

- Tesla Inc.

- UBTECH ROBOTICS CORP LTD

- Universal Robots AS

- Zebra Technologies Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Physical ai and robotics-as-a-service market

- In October 2024, SoftBank Group announced a definitive agreement to acquire the industrial robotics division of ABB for approximately USD 5.4 billion, signaling a major consolidation in the physical AI ecosystem.

- In November 2024, CynLr, a robotics startup, successfully closed a USD 10 million Series A funding round to advance its visual object-intelligence systems for robotic perception and manipulation.

- In February 2025, Apptronik secured USD 350 million in a funding round to scale up the production of its Apollo humanoid robot, designed for material handling and manufacturing assistance.

- In March 2025, Dexterity AI raised approximately USD 95 million in funding to scale its robotic manipulation systems for complex warehouse automation tasks, reaching a valuation of nearly USD 1.65 billion.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Physical AI And Robotics-as-a-service Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 291 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 30.8% |

| Market growth 2026-2030 | USD 21239.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 28.2% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, The Netherlands, Spain, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The physical AI and robotics-as-a-service market is fundamentally reshaping industrial automation through embodied artificial intelligence. At its core, the robotics-as-a-service model leverages subscription-based robotics to deploy intelligent hardware systems powered by advanced physical ai algorithms. This is enabled by technologies like autonomous navigation software and cloud-based robot management, allowing for sophisticated multi-robot fleet management.

- The hardware itself, from collaborative robotic arms to fully autonomous mobile robots and autonomous ground vehicles, relies on neural processing units and tactile sensing capabilities for real-time decision-making and human-robot collaboration. The trend toward open-ecosystem orchestration is a critical boardroom consideration, as it mitigates vendor lock-in and can improve integration efficiency by 40% when connecting heterogeneous robotic ecosystems.

- Innovations in ai-enabled robotic solutions, including humanoid robot development and ai-orchestrated robotic systems, are driven by deep learning techniques such as sim-to-real transfer learning and reinforcement learning for robotics.

- This convergence of software-defined manufacturing and advanced robotic perception technology, which uses visual simultaneous localization and mapping and proprioceptive feedback systems, is creating a new paradigm of operational efficiency, supported by ai-driven predictive maintenance and end-to-end neural network control.

What are the Key Data Covered in this Physical AI And Robotics-as-a-service Market Research and Growth Report?

-

What is the expected growth of the Physical AI And Robotics-as-a-service Market between 2026 and 2030?

-

USD 21.24 billion, at a CAGR of 30.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Solution (Physical AI, Robotics-as-a-Service, and Integration and support services), Application (Logistics and warehousing, Manufacturing and assembly, and Service and healthcare), End-user (Large enterprises, and SMEs) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation of generative physical intelligence, High initial capital expenditure and financial sustainability

-

-

Who are the major players in the Physical AI And Robotics-as-a-service Market?

-

Agility Robotics Inc., Bear Robotics, Inc., Berkshire Grey, Boston Dynamics Inc., Brain Corp., Covariant, Figure AI, Formant, Geekplus Technology Co. Ltd., IFS, inVia Robotics Inc., Locus Robotics Corp., NVIDIA Corp., Qualcomm Inc., RightHand Robotics Inc., Symbotic Inc., Tesla Inc., UBTECH ROBOTICS CORP LTD, Universal Robots AS and Zebra Technologies Corp.

-

Market Research Insights

- The physical AI and robotics-as-a-service market is driven by flexible raas business models that democratize access to advanced automation, with robotics-as-a-service pricing structures that reduce total cost of ownership by up to 35% for many organizations, especially raas for smes.

- Key physical ai applications in logistics and autonomous warehouse automation are being transformed by ai-powered fulfillment solutions and specialized humanoid robots in manufacturing. The use of cobot integration services and advanced robotic manipulation systems enables ai-based quality control, which can decrease defect rates by over 50%.

- The sector's expansion into raas in healthcare and industrial robot subscriptions is supported by developments in cloud robotics platforms, edge ai for robotics, and robust robot fleet orchestration. Managing raas deployment challenges and ensuring human-robot interaction safety are critical, as are innovations in robotic piece-picking solutions, autonomous cleaning machines, and comprehensive robot lifecycle management through sophisticated robotics middleware solutions.

We can help! Our analysts can customize this physical ai and robotics-as-a-service market research report to meet your requirements.

RIA -

RIA -