Pipeline Processing And Pipeline Services Market Size 2024-2028

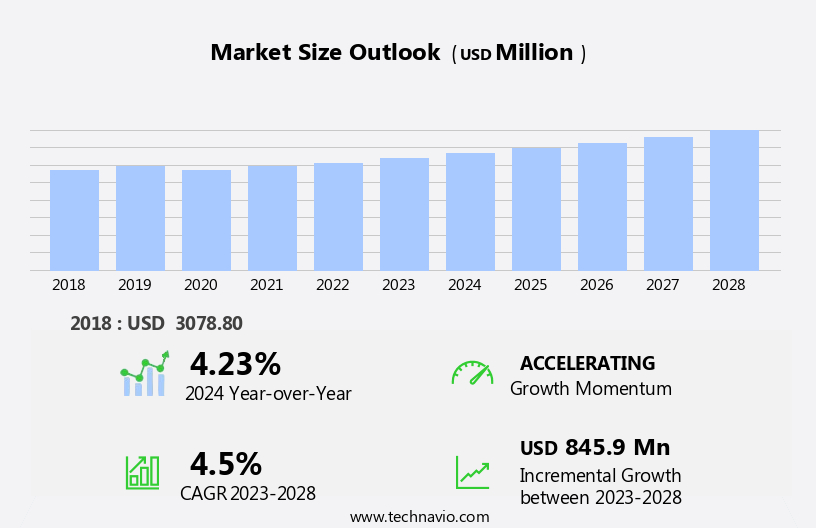

The pipeline processing and pipeline services market size is forecast to increase by USD 845.9 million, at a CAGR of 4.5% between 2023 and 2028.

- The market is experiencing significant growth, driven by the increasing preference for pipeline transportation as an efficient and cost-effective solution for transporting large volumes of oil and gas. This trend is further fueled by the advancements in pipeline inspection technologies, enabling more accurate and efficient detection of potential issues, thereby enhancing safety and reliability. However, the market faces challenges, including the stringent safety regulations that necessitate substantial investments in compliance and adherence to maintain operational excellence and mitigate potential risks.

- Companies in this market must navigate these challenges by continuously innovating and investing in technology to meet evolving regulatory requirements and customer demands, ultimately positioning themselves for long-term success in the dynamic pipeline processing and pipeline services landscape.

What will be the Size of the Pipeline Processing And Pipeline Services Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The pipeline processing and services market is characterized by its continuous evolution and dynamic nature, with ongoing activities and emerging patterns shaping the industry landscape. Pipeline integrity management plays a crucial role in ensuring the safety and reliability of these critical infrastructure assets. Pipeline simulation and modeling help optimize operations and enhance efficiency, while pipeline coating and corrosion monitoring protect against damage and extend asset life. Pipeline automation and pipeline asset management streamline processes and improve decision-making, with pipeline fittings and valves ensuring seamless flow and pressure control. Pipeline risk assessment and lifecycle management enable proactive maintenance and mitigate potential hazards.

Pipeline compressors and piping materials, such as high-density polyethylene (HDPE), support efficient transport of various commodities. Pipeline inspection, surveillance, and monitoring technologies enable early detection of leaks and anomalies, reducing environmental impact and minimizing downtime. Pipeline construction and project management, including directional drilling and pipeline permitting, require careful planning and execution. Pipeline emergency response, cybersecurity, and rehabilitation ensure business continuity and mitigate risks. Pipeline decommissioning and replacement are essential for end-of-life asset management. Pipeline regulations and safety standards continue to evolve, driving innovation and advancements in pipeline engineering, design, and construction management. The market's ongoing developments underscore the importance of pipeline integrity specialists and their role in maintaining the integrity and reliability of these essential infrastructure assets.

How is this Pipeline Processing And Pipeline Services Industry segmented?

The pipeline processing and pipeline services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

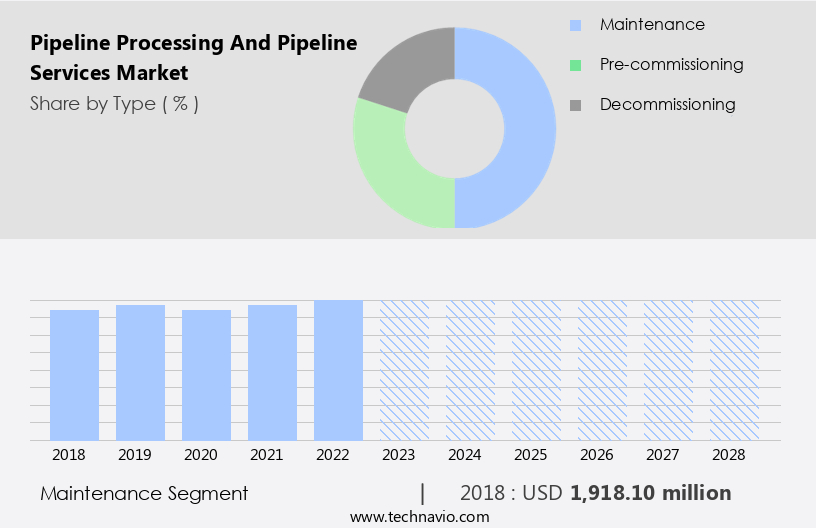

- Maintenance

- Pre-commissioning

- Decommissioning

- Geography

- North America

- US

- Canada

- Europe

- Russia

- APAC

- China

- Rest of World (ROW)

- North America

By Type Insights

The maintenance segment is estimated to witness significant growth during the forecast period.

In the oil and gas industry, pipeline processing and services play a pivotal role in ensuring the safe and efficient transportation of crude oil and natural gas. Pipeline maintenance, a critical aspect of this industry, encompasses pipeline integrity management, risk assessment, and lifecycle management. Pipeline integrity is maintained through various methods, including pipeline inspection using in-line inspection tools, corrosion monitoring, and cathodic protection. Pipeline materials, such as high-density polyethylene (HDPE) and steel pipes, require regular assessment and maintenance to prevent leaks and ensure safety. Pipeline construction, including directional drilling and hydraulic fracturing, necessitates the use of advanced pipeline design, engineering, and construction management techniques.

Pipeline automation and pipeline operations are optimized through the use of pipeline SCADA systems, pipeline pressure sensors, and pipeline flow meters. Pipeline safety regulations mandate regular pipeline safety inspections and emergency response plans. Pipeline rehabilitation and replacement are carried out using pipeline telemetry, pipeline pigging, and pipeline decommissioning. Pipeline fittings, pipeline valves, and pipeline compressors are essential components that require regular maintenance and replacement. Pipeline coating and pipeline anodic protection are used to prevent corrosion and extend the pipeline's lifespan. Pipeline cybersecurity is increasingly becoming a concern, with the integration of pipeline data acquisition and data analytics. Pipeline construction projects require extensive permitting and pipeline right-of-way acquisition.

Pipeline repair and maintenance are carried out by pipeline integrity specialists, using pipeline repair techniques such as composite wraps and steel repair sleeves. Pipeline replacement involves the use of pipeline replacement technologies, such as smart pigging and pipeline rehabilitation. The pipeline industry continues to evolve, with a focus on sustainability and reducing environmental impact.

The Maintenance segment was valued at USD 1918.10 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

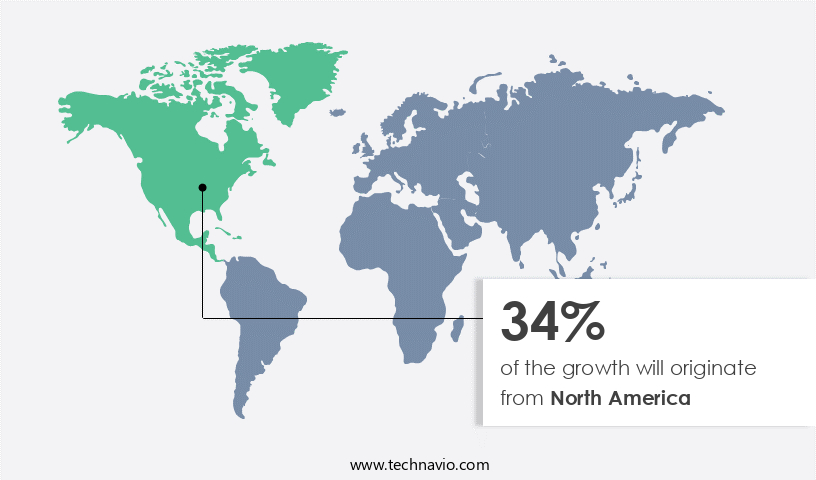

North America is estimated to contribute 34% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is experiencing moderate growth in the oil and gas industry, as the market recovers from the impact of COVID-19. North America, as the second-largest consumer of crude oil globally, is a significant contributor to the market's growth. The increasing demand for oil and gas production, coupled with the presence of numerous pipeline processing and pipeline services providers such as Halliburton Company and Baker Hughes Company, positions North America as a leading market. Pipeline integrity management, simulation, coating, automation, asset management, fittings, risk assessment, lifecycle management, compressors, abandonment, construction, safety regulations, inspection, materials, leak detection, pigging, environmental impact, modeling, high-density polyethylene (hdpe), emergency response, pressure sensors, operations, integrity specialists, repair, flow meters, design, construction management, hydraulic fracturing, anodic protection, integrity assessment, data analytics, directional drilling, data acquisition, cybersecurity, rehabilitation, telemetry, replacement, right-of-way, scada systems, steel pipes, corrosion monitoring, project management, welding, in-line inspection (ili), engineering, surveillance, valves, cathodic protection, maintenance, monitoring technologies, decommissioning, smart pigging, permitting, pumps, and remote monitoring are integral parts of the pipeline processing and pipeline services value chain.

Pipeline processing and pipeline services companies offer solutions for pipeline integrity management, ensuring the safe and efficient operation of pipelines. They provide pipeline simulation services to optimize pipeline performance and reduce operational costs. Pipeline coating services protect pipelines from external damage, while pipeline automation solutions enhance pipeline operations' efficiency and productivity. Pipeline asset management services help pipeline operators maintain their assets, ensuring their longevity and reliability. Pipeline risk assessment services identify potential threats and vulnerabilities, enabling pipeline operators to mitigate risks and prevent incidents. Pipeline lifecycle management services help pipeline operators manage the entire pipeline lifecycle, from design and construction to operations, maintenance, and decommissioning.

Pipeline compressors ensure the efficient transportation of natural gas and other hydrocarbons through pipelines. Pipeline abandonment services help pipeline operators safely decommission and remove pipelines at the end of their useful life. Pipeline construction services provide engineering, design, and construction expertise for new pipeline projects. Pipeline safety regulations ensure the safe and reliable operation of pipelines, while pipeline inspection services identify defects and anomalies, enabling timely repairs and maintenance. Pipeline materials, including high-density polyethylene (HDPE), are used in pipeline construction and rehabilitation to enhance pipeline performance and durability. Pipeline emergency response services help pipeline operators respond effectively to pipeline incidents, minimizing their impact on the environment and public safety.

Pipeline pressure sensors monitor pipeline pressure in real-time, enabling operators to detect anomalies and prevent potential incidents. Pipeline integrity specialists provide expertise in pipeline integrity assessment, data analytics, and monitoring technologies to help pipeline operators maintain pipeline integrity and prevent incidents. Pipeline repair services help operators repair pipeline damage and restore pipeline functionality. Pipeline flow meters measure pipeline flow rates, enabling operators to optimize pipeline operations and reduce costs. Pipeline design services provide engineering expertise for pipeline design and construction management. Hydraulic fracturing services help extract natural gas and oil from shale formations. Pipeline anodic protection services prevent pipeline corrosion, ensuring pipeline longevity and reliability.

Pipeline integrity assessment services use in-line inspection (ili) technology to identify pipeline defects and anomalies. Pipeline data analytics services help pipeline operators make data-driven decisions, optimizing pipeline operations and reducing costs. Directional drilling services enable the construction of pipelines in challenging terrain. Pipeline data acquisition services provide real-time pipeline data, enabling operators to monitor pipeline performance and prevent incidents. Pipeline cybersecurity services protect pipeline control systems from cyber attacks, ensuring pipeline safety and reliability. Pipeline rehabilitation services help pipeline operators extend pipeline life by repairing and upgrading existing pipelines. Pipeline telemetry services provide real-time pipeline data, enabling operators to monitor pipeline performance and prevent incidents.

Pipeline replacement services help pipeline operators replace aging pipelines with new ones, ensuring pipeline safety and reliability. Pipeline right-of-way services help pipeline operators acquire and manage pipeline right-of-way permits. Pipeline SCADA systems provide real-time pipeline data and control capabilities, enabling operators to optimize pipeline operations and prevent incidents. Steel pipes are a common material used in pipeline construction, while corrosion monitoring services help pipeline operators prevent pipeline corrosion. Pipeline project management services help pipeline operators manage pipeline projects from planning to execution. Pipeline welding services ensure pipeline integrity and reliability. In-line inspection (ILI) services help pipeline operators identify pipeline defects and anomalies.

Pipeline engineering services provide expertise in pipeline design and construction. Pipeline surveillance services monitor pipeline performance and prevent incidents. Pipeline valves ensure pipeline safety and reliability by controlling pipeline flow. Pipeline cathodic protection services prevent pipeline corrosion, ensuring pipeline longevity and reliability. Pipeline maintenance services help pipeline operators maintain pipeline functionality and prevent incidents. Pipeline monitoring technologies, including pipeline leak detection and smart pigging, help pipeline operators detect pipeline leaks and anomalies, enabling timely repairs and maintenance. Pipeline decommissioning services help pipeline operators safely remove and dispose of pipelines at the end of their useful life. Pipeline permitting services help pipeline operators acquire and manage pipeline permits.

Pipeline pumps ensure the efficient transportation of hydrocarbons through pipelines. Pipeline remote monitoring services enable operators to monitor pipeline performance and prevent incidents from a remote location.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Pipeline Processing And Pipeline Services Industry?

- The growing demand for pipeline transportation is the primary factor driving market growth in this sector.

- Pipeline processing and services play a crucial role in the midstream oil and gas industry. Pipelines are the preferred choice for transporting crude oil and natural gas over long distances due to their numerous advantages. These include low energy consumption, resulting in a smaller carbon footprint, high reliability, and the ability to operate continuously with minimal dependence on external factors. Additionally, pipelines can be laid through various terrains and underseas, making them versatile for transporting resources from remote production sites to refineries and end-users. Pipeline infrastructure encompasses various components such as pipeline welding, in-line inspection (ILI), pipeline engineering, pipeline surveillance, pipeline valves, pipeline cathodic protection, pipeline maintenance, pipeline monitoring technologies, pipeline decommissioning, smart pigging, pipeline permitting, pipeline pumps, and pipeline remote monitoring.

- These services ensure the efficient and safe operation of pipelines throughout their extended life cycle, which averages 20-30 years. Pipeline processing and services are essential for maintaining the integrity of pipelines, enhancing their performance, and ensuring the safe transportation of oil and gas. These services are continuously evolving with advancements in technology, enabling more efficient and cost-effective solutions for pipeline operators.

What are the market trends shaping the Pipeline Processing And Pipeline Services Industry?

- The trend in pipeline inspection markets is characterized by significant advancements in technology. Technological innovations continue to shape the industry, ensuring more efficient and effective inspections.

- In the oil and gas industry, ensuring pipeline safety is of paramount importance. Traditional methods for pipeline maintenance and inspection, such as using scrapers or pigs, have limitations. Smaller diameter pipelines or those with bends may not be accessible for pigging, leading to undetected issues like metal loss, corrosion, or cracks. However, research and development efforts have led to significant advancements in pipeline services. These innovations include pipeline integrity management, pipeline simulation, pipeline coating, pipeline automation, pipeline asset management, pipeline fittings, pipeline risk assessment, pipeline lifecycle management, pipeline compressors, and pipeline inspection using advanced technologies.

- These solutions enable remote monitoring and early detection of potential pipeline issues, reducing the risk of oil or gas spillage and leakage. Pipeline materials are also being improved to enhance durability and resistance to corrosion. The focus on pipeline safety regulations ensures the implementation of these advanced technologies and practices, maintaining the integrity and reliability of the pipeline infrastructure.

What challenges does the Pipeline Processing And Pipeline Services Industry face during its growth?

- Strict safety regulations pose a significant challenge to the industry's growth by increasing operational costs and complexifying compliance processes.

- The market is subject to stringent safety regulations, primarily enforced by organizations such as the Occupational Safety and Health Administration (OSHA). These regulations necessitate comprehensive health and safety plans (HASPs) for employers in industries utilizing pipelines, including oil and gas, mining, petrochemical, and chemical sectors. OSHA's mandates prioritize worker safety during pipeline operations, clean-up processes, and pipeline emergency response situations. Pipeline services encompass various applications, such as pipeline leak detection, pipeline pigging, pipeline modeling, pipeline pressure sensors, pipeline flow meters, pipeline repair, and pipeline design. Pipeline integrity specialists play a crucial role in maintaining pipeline operations, ensuring the structural integrity of pipelines and minimizing environmental impact.

- High-density polyethylene (HDPE) pipelines have gained popularity due to their durability and resistance to corrosion, contributing to the market's growth. Pipeline construction management and hydraulic fracturing are other significant factors driving market expansion. Despite these growth factors, regulatory compliance remains a critical challenge for market participants. Ensuring adherence to safety regulations and maintaining pipeline integrity are essential for market players to succeed in the pipeline processing and pipeline services industry.

Exclusive Customer Landscape

The pipeline processing and pipeline services market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the pipeline processing and pipeline services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, pipeline processing and pipeline services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Baker Hughes Co. - This company specializes in pipeline processing and services, encompassing crude processing, corrosion mitigation, desalination, fouling prevention, and foaming with process treatment chemicals.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Baker Hughes Co.

- BGS Energy Services

- Chenergy Services Ltd.

- CR Asia Pte Ltd.

- Cypress Pipeline and Process Services LLC

- EnerMech Group Ltd.

- Enerpac Tool Group Corp.

- Eunisell Chemicals

- GATE Energy

- Halliburton Co.

- Ideh Pouyan Energy Co.

- IKM Instrutek AS

- NiGen International LLC

- Offshore Construction Specialists Pte. Ltd.

- Saudi Arabian Oil Co.

- Schlumberger Ltd.

- STEP Energy Services Ltd.

- Techfem SpA

- Trans Asia Pipeline Services FZC

- Tucker Energy Solutions LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Pipeline Processing And Pipeline Services Market

- In January 2024, Schlumberger Limited, a leading provider of technology and integrated project management for the energy industry, announced the launch of its new pipeline processing solution, OptiFlo, designed to optimize pipeline throughput and efficiency. This innovative technology was showcased at the annual Oil & Gas Show in Calgary, Canada (Schlumberger press release, 2024).

- In March 2024, Halliburton Company and Baker Hughes, two major players in the pipeline services market, announced their merger, creating a leading provider of technology and services to the energy industry. The combined entity, Baker Hughes, a GE Company, aimed to enhance its pipeline services offerings through the integration of Halliburton's pipeline services business (Baker Hughes press release, 2024).

- In May 2024, the U.S. Department of Energy (DOE) granted approval for the construction of the Mountain Valley Pipeline, a 303-mile natural gas pipeline project in the Eastern United States. The project, valued at approximately USD5.3 billion, was expected to create jobs and strengthen the U.S. Energy infrastructure (DOE press release, 2024).

- In February 2025, Saipem S.P.A., an Italian multinational company specializing in engineering and construction, signed a contract with TotalEnergies for the engineering, procurement, and construction (EPC) of a natural gas processing plant in Mozambique. The project, valued at â¬3 billion, was expected to increase Mozambique's natural gas production capacity and contribute to the country's economic growth (Saipem press release, 2025).

Research Analyst Overview

- In the pipeline processing and services market, pipeline maintenance scheduling and pipeline safety management are critical focus areas. Pipeline regulatory compliance and pipeline integrity software ensure adherence to regulations, while pipeline fracture mechanics and pipeline failure analysis help prevent catastrophic incidents. Pipeline instrumentation, pipeline corrosion prevention, and pipeline coating technologies contribute to asset optimization. Pipeline construction software, pipeline cost optimization, and pipeline commissioning streamline project execution. Pipeline design software, pipeline fatigue analysis, pipeline stress analysis, and pipeline welding techniques ensure robust pipeline structures.

- Pipeline reliability analysis, pipeline safety management, and pipeline incident reporting facilitate proactive incident prevention. Pipeline GIS mapping, pipeline GPS tracking, and pipeline start-up/shutdown optimization enhance operational efficiency. Pipeline life extension and pipeline predictive maintenance enable prolonged asset utilization. Overall, these technologies and services play a pivotal role in ensuring pipeline reliability, safety, and cost-effectiveness.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Pipeline Processing And Pipeline Services Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

138 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2024-2028 |

USD 845.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Key countries |

US, Russia, China, Canada, and Saudi Arabia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Pipeline Processing And Pipeline Services Market Research and Growth Report?

- CAGR of the Pipeline Processing And Pipeline Services industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the pipeline processing and pipeline services market growth of industry companies

We can help! Our analysts can customize this pipeline processing and pipeline services market research report to meet your requirements.

RIA -

RIA -