Polyisocyanates Market Size 2024-2028

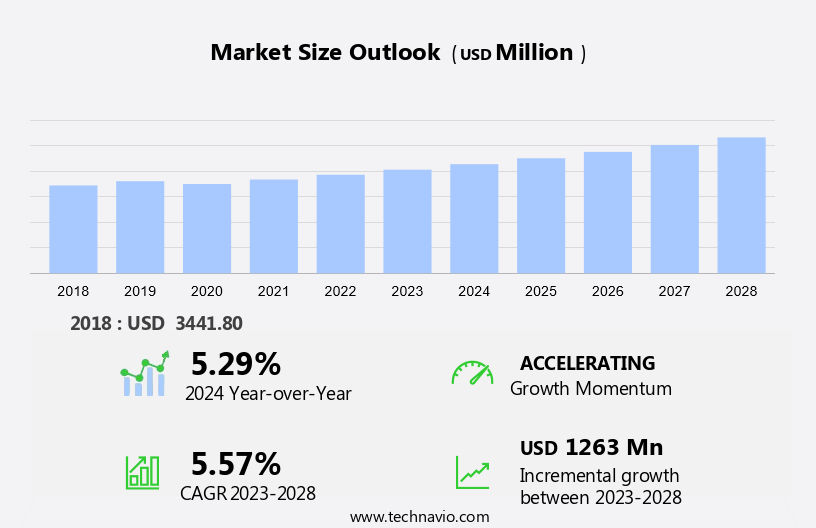

The polyisocyanates market size is forecast to increase by USD 1.26 billion at a CAGR of 5.57% between 2023 and 2028. The market is experiencing significant growth due to the expanding construction industry and the increasing demand for sustainable solutions. One trend driving market growth is the adoption of bio-based polyisocyanates, which offer improved sustainability and reduced environmental impact. However, fluctuations in the prices of raw materials, particularly aromatic diisocyanates, pose a challenge to market growth. Rigid and flexible foams remain the primary applications for polyisocyanates, with pipeline construction also presenting opportunities for market expansion. Strategic activities, such as mergers and acquisitions, and regulatory actions are shaping the competitive landscape. Understanding these trends and challenges is crucial for businesses looking to capitalize on the growth potential of the market. However, the market faces challenges due to the fluctuations in raw material prices, particularly those of toluene diisocyanate (TDI) and methylene diphenyl diisocyanate (MDI), which are key raw materials for polyisocyanates production.

What will be the Size of the Market During the Forecast Period?

The market encompasses the production and distribution of isocyanates, a crucial chemical intermediate used in the manufacturing of various polyurethane products. This market holds significant importance in industries such as adhesives, coatings, automotive, construction, and insulation materials. Isocyanates, specifically toluene diisocyanate (TDI) and polymeric MDI, serve as the foundation for producing polyurethane products. These include adhesives, coatings, automotive interiors and seats, insulation materials, sealants, and various types of foams, such as rigid and flexible. In the automotive sector, polyisocyanates contribute to the production of lightweight and durable components, including cushions and seats, which are essential for weight reduction and improved fuel efficiency.

Furthermore, in the construction industry, polyisocyanates are used in the manufacturing of insulation materials, contributing to energy efficiency and thermal insulation. The market faces various challenges, including health and safety concerns related to the production and handling of phosgene, a byproduct of isocyanate manufacturing. OSHA (Occupational Safety and Health Administration) has set strict regulations to minimize exposure to phosgene and ensure a safe working environment. Crude oil prices and capacity reductions can significantly impact the market. High crude oil prices increase the cost of raw materials, leading to increased production costs. Additionally, capacity reductions due to plant shutdowns or maintenance can lead to supply shortages and price fluctuations.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

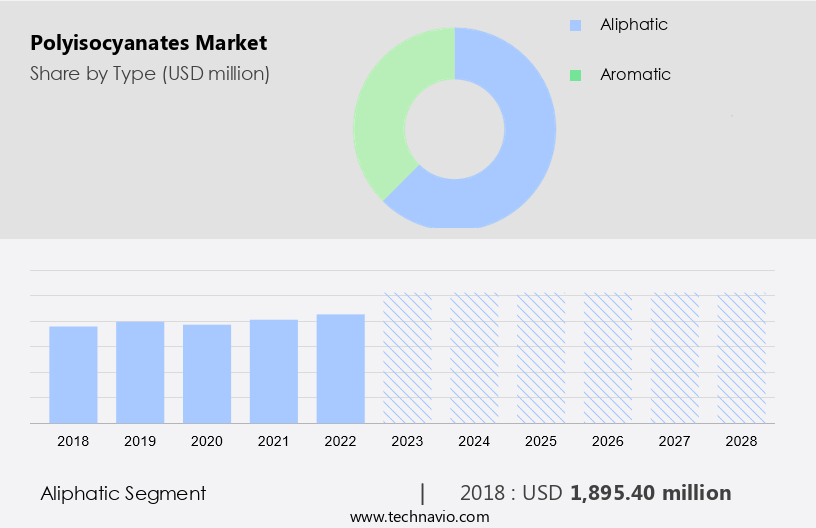

- Type

- Aliphatic

- Aromatic

- Application

- Coating

- Foam

- Adhesive

- Geography

- APAC

- China

- India

- North America

- US

- Europe

- Germany

- UK

- Middle East and Africa

- South America

- APAC

By Type Insights

The aliphatic segment is estimated to witness significant growth during the forecast period. Polyisocyanates are essential compounds utilized in the manufacturing process of various products, including paints, rigid foam, and flexible foam. In the realm of polyurethane (PU) production, polyisocyanates serve as crucial building blocks. These compounds are employed in creating PU coatings, sealants, adhesives, and elastomers. Furthermore, they find applications in textile treatment and finishing formulations. The expansion of the aliphatic segment within the market can be linked to the escalating demand for coatings across numerous industries, such as automotive, construction, and manufacturing. Aliphatic polyisocyanates offer remarkable durability, chemical resistance, and resistance to weather conditions, making them highly sought-after for safeguarding surfaces in challenging environments.

Furthermore, in coatings applications, aliphatic polyisocyanates outperform their aromatic counterparts due to their superior performance in varying weather conditions. As a result, their utilization is increasingly popular in industries where durability and resistance to harsh conditions are vital.

Get a glance at the market share of various segments Request Free Sample

The aliphatic segment accounted for USD 1.89 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

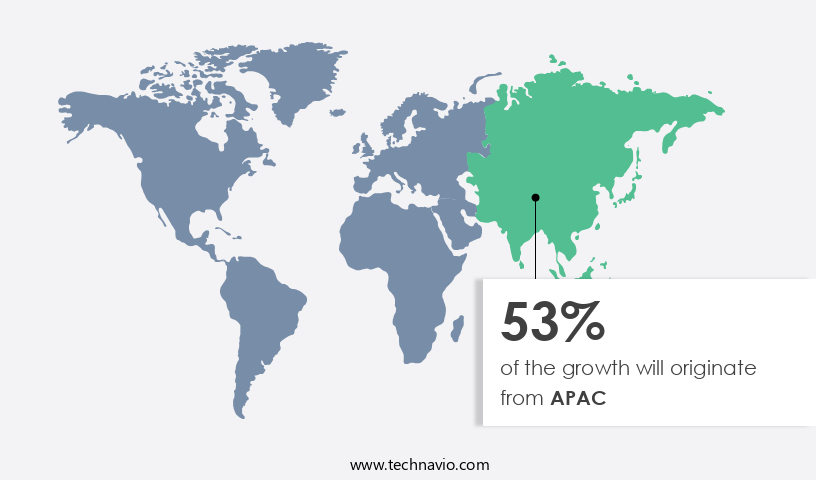

APAC is estimated to contribute 53% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market is experiencing substantial growth in the North American region due to expanding industries, particularly in China, Malaysia, Indonesia, Vietnam, Japan, South Korea, and India. This growth can be attributed to the rapid industrialization and construction sector development in these countries. The demand for polyisocyanates is primarily driven by the increasing usage of foam as an insulation material, which is backed by government initiatives. Additionally, many companies have relocated their production facilities to this region to take advantage of reduced production costs. As a result, the demand for polyisocyanates is expected to continue growing in the region, particularly in the coatings market and for the production of Polyurethane foam in various applications such as insulation for residential and commercial buildings, and Rigid PU foam for insulation in Zero-energy buildings. This trend is expected to continue as the market for insulation and energy-efficient construction gains momentum.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Growth in the construction industry is the key driver of the market. Polyisocyanates serve a significant function in the manufacture of polyurethane foam, a multifunctional material extensively utilized in the building sector. This foam offers exceptional thermal insulation capabilities, making it a preferred choice for various construction applications, such as insulation panels, roofing systems, and spray foam insulation. With the growing trend of energy efficiency and increasing urbanization in emerging economies, the need for insulation materials, including polyurethane foam, is experiencing a rise. Authorities worldwide are investing in energy-efficient structures, with the US Department of Energy (DOE) recently announcing program guidelines and inviting states and territories to apply for USD400 million in funding to implement energy codes.

Moreover, the demand for polyisocyanates extends beyond construction, with applications in various industries, including furniture, Footwear, electronics, and shared mobility. For instance, in the furniture industry, these materials are used to produce foam cushions and upholstery. In the footwear industry, they are applied as adhesives and coatings. In the electronics sector, they are used in the production of high-performance materials. Lastly, in the shared mobility and Electric vehicles sectors, polyisocyanates are utilized to manufacture lightweight and insulating components. As the market for greenhouse gas-neutral isocyanates continues to expand, companies are focusing on developing sustainable production methods. This trend is expected to drive the growth of the market in the coming years.

Market Trends

Increasing demand for bio-based polyisocyanates is the upcoming trend in the market. The market is witnessing an upward trend due to the rising demand for corrosion protection solutions derived from this chemical compound. Bio-based polyisocyanates, a segment of this market, are gaining popularity due to their eco-friendly attributes. These polyisocyanates are produced using renewable feedstocks, such as vegetable oils, soybeans, corn, and biomass sources, including algae and lignocellulosic materials. The shift towards bio-based polyisocyanates is influenced by increasing environmental concerns, sustainability initiatives, and regulatory pressures to decrease carbon emissions and reliance on non-renewable resources. Bio-based polyisocyanates provide several benefits over their petrochemical counterparts. They have a reduced environmental impact, as they contribute less to greenhouse gas emissions and decrease the dependence on finite fossil resources.

Moreover, bio-based polyisocyanates offer comparable or even superior performance characteristics, including enhanced thermal stability, flame retardancy, and biodegradability. As a professional assistant, it is essential to maintain a formal and knowledgeable tone when discussing market trends. The market is an emerging area of interest due to its potential to address environmental concerns and offer competitive performance characteristics. This trend is expected to continue as more companies adopt sustainable business practices and regulatory bodies encourage the use of renewable resources.

Market Challenge

Fluctuations in raw material prices of polyisocyanates is a key challenge affecting the market growth. The market is impacted by the volatility in the pricing of crude oil and natural gas, which serve as the primary feedstocks for producing essential raw materials such as propylene and benzene. The production of polyisocyanates relies heavily on these petroleum-based materials.

Furthermore, fluctuations in their prices directly influence the cost structure and profitability of manufacturers. The price instability of these raw materials poses a significant challenge for the industry, as it can impact production costs and profit margins. Specialty chemicals, including polyisocyanates, are manufactured using polymers, resins, and additives as primary ingredients. The cost of these raw materials is contingent upon the price of crude oil.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

BASF SE - The company offers Polylisocyanates such as Isocyanates and Polyols, which can be used as tough automotive coatings, dampening pads, elastomers, shoe soles, sealants, binders or cables.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Anhui Sinograce Chemical Co. Ltd.

- Asahi Kasei Corp.

- BASF SE

- Bogao Synthetic Material Co. Ltd.

- BorsodChem

- China National Bluestar (Group) Co.Ltd.

- Covestro AG

- DIC Corp.

- Dow Inc.

- Doxu Group

- Evonik Industries AG

- Huntsman Corp.

- JIAHUA CHEMICALS INC.

- Merck KGaA

- Mitsui Chemicals Inc.

- N Shashikant and Co.

- Shandong INOV Polyurethane Co. Ltd.

- Super Urecoat Industries

- Tosoh Corp.

- Vencorex

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The global isocyanates market is witnessing significant growth due to the rising demand for polyurethane products in various industries. Isocyanates, specifically diisocyanates such as toluene diisocyanate and polymeric MDI, play a crucial role in the production of polyurethane products, including adhesives, coatings, automotive seats, interiors, and insulation materials. The market, particularly for PU coatings, is a major consumer of isocyanates. The automotive industry, construction sector, and furniture industry are key contributors to the demand for isocyanates.

Furthermore, the demand for isocyanates in insulation materials, sealants, and zero-energy buildings is increasing due to the focus on energy efficiency and sustainability. The use of isocyanates in rigid and flexible foam for insulation, cushions, bedding, and furniture is also growing. The market is also witnessing the emergence of bio-based isocyanates and greenhouse gas-neutral isocyanate for household applications. Regulatory actions and concerns over the toxic properties of isocyanates are posing challenges to the market. However, strategic activities such as pipeline construction for corrosion protection and the development of high-performance materials are expected to offer growth opportunities. The market is also witnessing trends in the electronics industry, shared mobility, and electric vehicles.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

205 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.57% |

|

Market Growth 2024-2028 |

USD 1.26 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.29 |

|

Regional analysis |

APAC, North America, Europe, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 53% |

|

Key countries |

China, US, Germany, India, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Anhui Sinograce Chemical Co. Ltd., Asahi Kasei Corp., BASF SE, Bogao Synthetic Material Co. Ltd., BorsodChem, China National Bluestar (Group) Co.Ltd., Covestro AG, DIC Corp., Dow Inc., Doxu Group, Evonik Industries AG, Huntsman Corp., JIAHUA CHEMICALS INC., Merck KGaA, Mitsui Chemicals Inc., N Shashikant and Co., Shandong INOV Polyurethane Co. Ltd., Super Urecoat Industries, Tosoh Corp., and Vencorex |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -