Power Metering Market Size 2024-2028

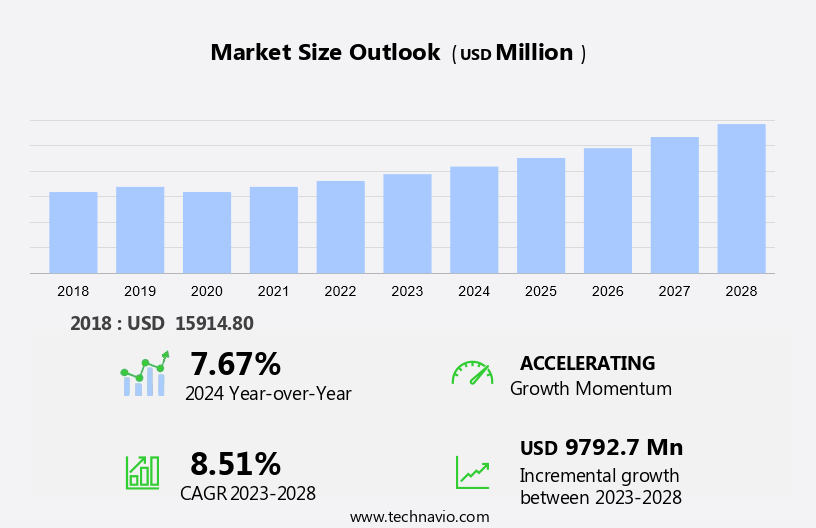

The power metering market size is forecast to increase by USD 9.79 billion at a CAGR of 8.51% between 2023 and 2028.

- In the market, utility companies and city infrastructure are driving the adoption of advanced technologies to monitor and manage electricity consumption more efficiently. Smart City initiatives and environmental concerns are key trends propelling market growth. Technological upgrades, such as AI technology and data metrics, enable real-time monitoring and analysis of energy consumption, enhancing grid stability and reducing wastage.

- Moreover, the construction sector is also embracing wireless smart power meters to optimize energy usage in new buildings. Despite these opportunities, high costs remain a challenge for widespread market penetration. Overall, the market is evolving to meet the demands of a more connected and sustainable energy landscape.

What will be the Size of the Market During the Forecast Period?

- The market in North America is witnessing significant advancements driven by the increasing demand for energy management and the integration of renewable infrastructure. Power metering systems enable accurate measurement and monitoring of electricity consumption, which is essential for effective energy management. User interfaces have become increasingly important in power metering systems, providing real-time data metrics for energy consumption and facilitating two-way communication between utilities and consumers. This allows for the implementation of multi-rate tariffs, which incentivize energy efficiency and promote the use of renewable energy sources. Renewable energy systems, such as solar and wind, are becoming more prevalent in North America, necessitating the installation of power metering systems to monitor their output and ensure efficient energy management.

- Moreover, the construction of renewable infrastructure, including charging stations for electric vehicles, also requires the integration of power metering systems to ensure optimal performance and energy efficiency. Smart cities are another application of power metering systems, where they are used to monitor and manage energy consumption in urban areas. This includes residential and commercial usage, as well as urban applications such as street lighting and public transportation. Power metering systems are also essential in rural applications, where they help to optimize energy usage and reduce costs. Power meter manufacturers are focusing on technological upgrades to enhance the capabilities of power metering systems. These upgrades include the integration of load balancing and remote reading features, which enable utilities to optimize energy distribution and reduce the need for manual inspections. Environmental concerns are also driving the development of more efficient and eco-friendly power metering systems. Single phase and three phase meters are the two main types of power meters used in North America. Single phase meters are suitable for residential and small commercial applications, while three phase meters are used for larger commercial and industrial applications. The market for power meters is expected to grow as the demand for energy management and renewable energy integration continues to increase.

- In conclusion, the market in North America is experiencing significant growth due to the increasing demand for energy management and the integration of renewable infrastructure. Power metering systems enable accurate measurement and monitoring of electricity consumption, facilitating effective energy management and the integration of renewable energy sources. The market is expected to continue growing as technological upgrades and the integration of smart city applications drive demand for more advanced power metering systems.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

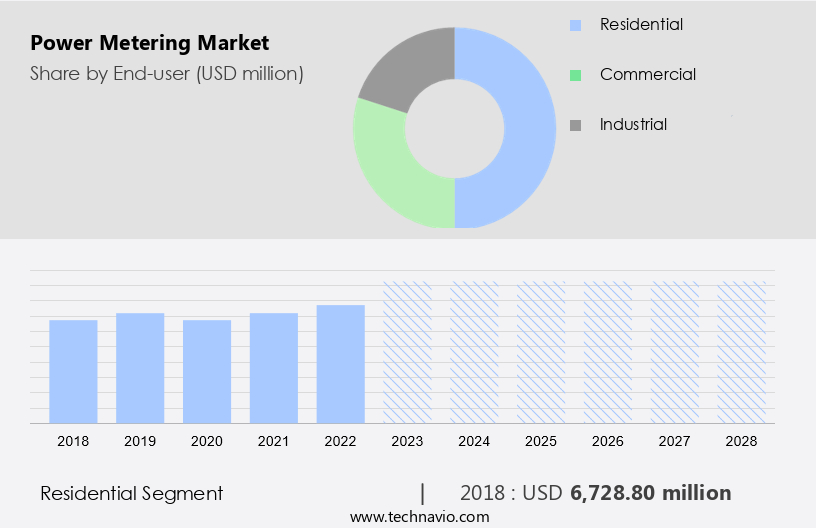

- End-user

- Residential

- Commercial

- Industrial

- Geography

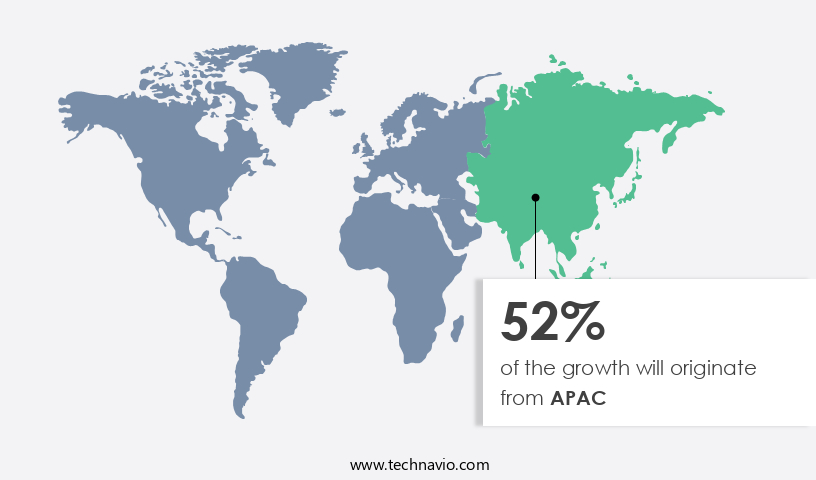

- APAC

- China

- Japan

- Europe

- Germany

- UK

- North America

- US

- South America

- Middle East and Africa

- APAC

By End-user Insights

- The residential segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant growth due to the increasing demand for electricity worldwide. Factors such as population growth, urbanization, and rising employment levels are driving this need. In the residential sector, governments in various countries are offering incentives for the installation of advanced power meters, leading to a growth in demand. Additionally, the implementation of smart grids on a global scale is fueling the demand for power meters among utility companies. Power meter manufacturers are responding to this demand by offering innovative solutions with high accuracy. For instance, some companies provide chainring options for bicycle power meters, while others use Ultra-Torque Titanium Axles for enhanced durability.

Furthermore, power meters are available in single-phase and three-phase versions to cater to both residential and commercial applications. Power meters find extensive usage in urban applications due to the high energy consumption in densely populated areas. However, they are also essential in rural areas where electricity is often generated on-site, requiring precise measurement for efficient energy management. Overall, the market is poised for continued growth as the world's energy needs evolve.

Get a glance at the market report of share of various segments Request Free Sample

The residential segment was valued at USD 6.73 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

- APAC is estimated to contribute 52% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market in Asia Pacific (APAC) is experiencing significant growth due to the increasing commercial and urban developments in countries like China and India. Factors driving this growth include the burgeoning population, increasing urbanization, and the growth of manufacturing industries. Moreover, supportive regulatory actions are further fueling the adoption of power meters in the region. The electric power demand in APAC has been on a steady rise over the past decade, primarily due to industrialization and urbanization. Key countries contributing to this growth include China, India, South Korea, and Japan.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Power Metering Market?

Growing investment in smart grid projects is the key driver of the market.

- In the global energy sector, power metering systems have gained significant attention due to the increasing adoption of renewable infrastructure. These systems play a crucial role in managing energy consumption and distribution, particularly in the context of renewable energy systems and charging stations for electric vehicles. Power metering systems offer advanced features such as user interfaces, energy management, load balancing, and remote reading. Multi-rate tariffs are becoming increasingly common, requiring sophisticated metering systems to accurately measure and bill consumers.

- Moreover, the implementation of these systems enables utilities to analyze power consumption patterns, facilitating load forecasting, peak demand management, and risk assessment. The US, alongside countries like China, India, and European nations such as Spain, Germany, and France, have made substantial investments in smart grid projects, integrating power metering systems as part of comprehensive digital grid strategies. These networking systems offer utilities valuable insights into their customers' energy usage, promoting efficient energy management and optimizing grid performance.

What are the market trends shaping the Power Metering Market?

Growing demand for wireless smart power meters is the upcoming trend in the market.

- In the US market, utilities are embracing the adoption of advanced wireless power metering systems to enhance energy efficiency and optimize electricity consumption. The implementation of AI technology in these systems allows for real-time monitoring and analysis of energy usage patterns, providing utilities with valuable data metrics to address environmental concerns and improve overall grid performance. The shift from traditional manual meter checks to smart power meters enables consumers to access real-time pricing information, fostering energy conservation and demand response. The aging infrastructure of utilities calls for technological upgrades, leading to the construction of smart energy networks.

- Moreover, these networks consist of a cohesive set of systems, products, and solutions that facilitate remote and continuous monitoring and diagnosis of distribution-related issues. The integration of AI technology in power metering systems is a significant step towards creating a sustainable and efficient energy ecosystem in the US. The growing emphasis on energy efficiency and sustainability, coupled with the need for accurate and timely data, is driving the demand for advanced power metering solutions. The smart city initiative is also playing a crucial role in the market's growth, as cities aim to reduce their carbon footprint and improve energy management. The implementation of these systems not only benefits utilities but also empowers consumers to make informed decisions about their energy usage, ultimately contributing to a more sustainable energy future.

What challenges does Power Metering Market face during the growth?

The high cost of products is a key challenge affecting the market growth.

- Smart power meters, which include Digital meters, Multi-function meters, and Smart meters, offer advanced features such as real-time energy consumption data and remote monitoring capabilities. However, their higher installation costs compared to traditional Analog meters, Single-phase meters, and Three-phase meters, can be a significant barrier for smaller utilities. The investment in these meters typically yields a return on investment within a period of five to eight years. Yet, the initial expense may not be justifiable for utilities with limited resources.

- Furthermore, the installation of smart power meters necessitates investment in networking technology for seamless integration with utility networks. This integration is essential for the effective functioning of smart power meters. In the context of the United States, the large population and the need for extensive networking infrastructure add to the complexity and cost of implementing smart power meters. Nevertheless, the long-term benefits, including energy conservation and IoT integration, make it a worthwhile investment for utilities with the necessary resources.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Aichi Tokei Denki Co. Ltd.

- ALLETE Inc

- Eaton Corp. Plc

- General Electric Co.

- Holley Technology Ltd.

- Honeywell International Inc.

- Hubbell Inc.

- Itron Inc.

- Jabil Inc.

- Kamstrup AS

- Landis Gyr AG

- Networked Energy Services

- Ningbo Sanxing Medical and Electric Co. Ltd.

- Schneider Electric SE

- Shenzhen Kaifa Technology Co. Ltd

- Siemens AG

- Suntront Tech Co. Ltd

- Wasion Holdings Ltd.

- Xylem Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Power metering systems have gained significant traction in recent years due to the increasing focus on energy management and conservation. Renewable infrastructure, including renewable energy systems and charging stations for electric vehicles, has driven the demand for advanced power metering solutions. Multi-rate tariffs and energy management systems enable efficient load balancing and optimize energy consumption. User interfaces have evolved from analog meters to digital and multi-function meters, offering real-time data metrics and two-way communication. IoT and AI technology have revolutionized power metering, enabling predictive maintenance and energy conservation. Utilities and smart city construction projects are major applications for power metering systems.

Moreover, renewable energy systems and electrification projects require high operating efficiency and accurate sensors, including gyroscopes and strain gauges. Power meter manufacturers are investing in technological upgrades, such as AI algorithms and smart grid players, to meet the growing demand for advanced power metering solutions. Venture capital firms and investment banks are also investing in the sector, driving innovation and growth. Power metering systems are essential for residential, commercial, and urban applications, as well as rural areas. Single-phase and three-phase meters cater to various power consumption needs. Energy conservation and environmental concerns continue to be key drivers for the market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

144 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.51% |

|

Market growth 2024-2028 |

USD 9.79 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.67 |

|

Key countries |

China, US, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -