Smart Energy Market Size 2024-2028

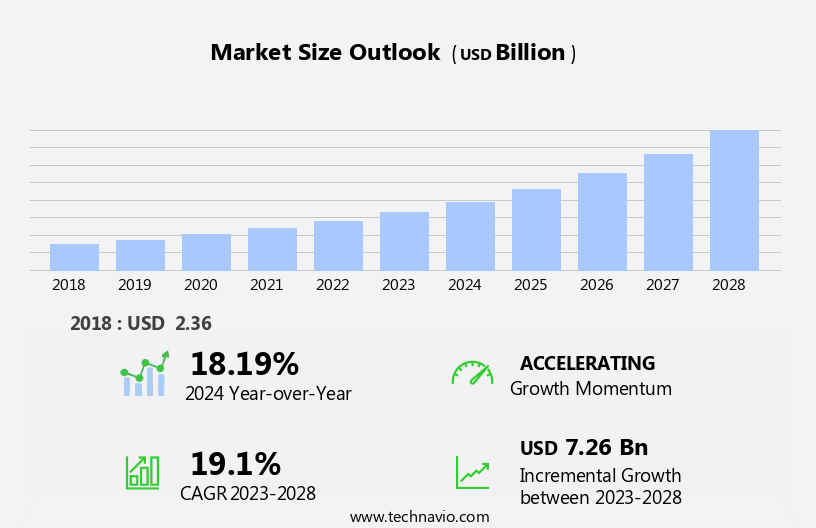

The smart energy market size is forecast to increase by USD 7.26 billion at a CAGR of 19.1% between 2023 and 2028.

- The market is experiencing significant growth, driven by the increasing adoption of smart grid technologies and the rising investment in smart cities and smart homes. These trends are transforming the energy sector by enabling more efficient energy management and consumption. However, the intermittency in solar energy remains a challenge, as renewable energy sources become an increasingly larger part of the energy mix. To capitalize on market opportunities and navigate challenges effectively, companies must stay abreast of technological advancements and regulatory developments.

- Strategic partnerships and collaborations can also help organizations expand their reach and enhance their offerings. By focusing on innovation and flexibility, companies can position themselves to thrive in this dynamic market.

What will be the Size of the Smart Energy Market during the forecast period?

- The market encompasses a range of technologies and services aimed at optimizing energy production and consumption, reducing carbon footprints, and integrating renewable energy sources into the grid. Key components include smart meters, distribution automation systems, and advanced metering devices for homes, offices, and industrial plants. Capital expenditures in this sector are driven by the adoption of smart grid technologies, such as solar energy, wind energy, and smart thermal grids. Consulting services play a crucial role in the development and implementation of these solutions, ensuring regulatory compliance and work management efficiency. The market's growth is fueled by the increasing importance of energy efficiency, the rise of renewable energy sources, and the integration of smart electricity grids.

- Hardware, including smart sensors and communication networks, are essential for enabling real-time monitoring and control of energy usage. Overall, the market is experiencing significant growth as businesses and consumers seek to minimize their carbon footprints and improve energy management.

How is this Smart Energy Industry segmented?

The smart energy industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

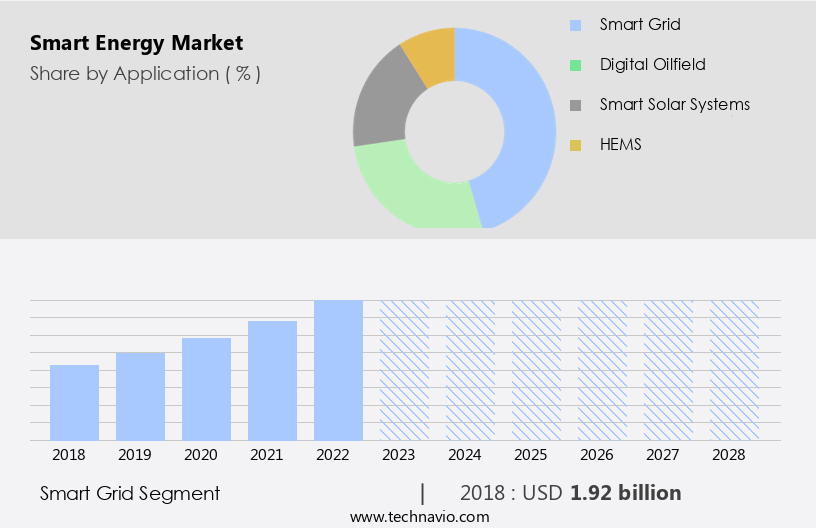

- Smart grid

- Digital oilfield

- Smart solar systems

- HEMS

- End-user

- Industrial

- Commercial

- Residential

- Component

- Solution

- Services

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- Rest of World (ROW)

- North America

By Application Insights

The smart grid segment is estimated to witness significant growth during the forecast period. The market encompasses the deployment of intelligent electricity meters, solar energy, and renewable energy sources in homes, offices, and industrial plants. Smart grids, a significant segment of this market, leverage advanced metering devices, network infrastructure, and system integration services to optimize energy supply security. The US is a pioneer in this field, with substantial investments in smart grid technology. In 2022, the US allocated USD 84 billion for grid investments, making it the global leader. China follows with USD 75 billion, and other countries invest USD 63 billion. The smart grid market consists of electric grid equipment and services, including distribution automation systems, network management software, and hardware.

This technology integration aids in the efficient management of renewable power sources, such as solar and wind, and reduces carbon footprints while adhering to regulatory standards. Smart thermal grids and work management systems further enhance industrial processes, ensuring energy efficiency and cost savings. Smart gas and steam turbines are also integral components of the market, contributing to the overall growth and development of renewable energy sources.

Get a glance at the market report of share of various segments Request Free Sample

The Smart grid segment was valued at USD 1.92 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

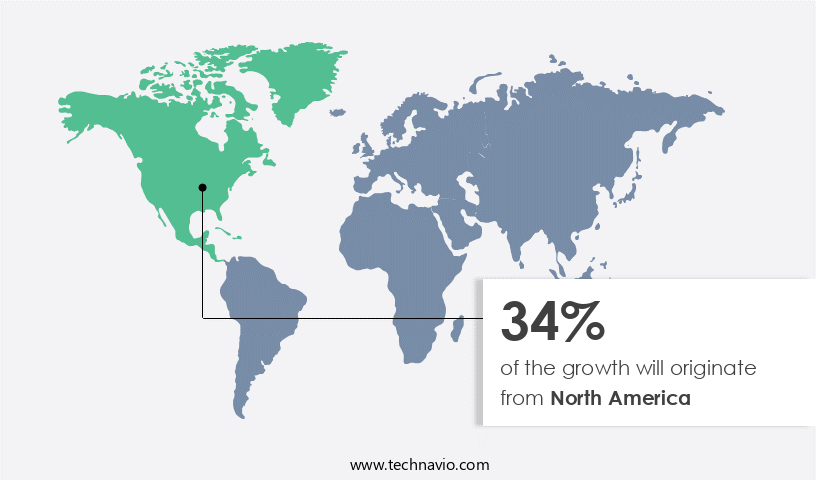

North America is estimated to contribute 34% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

In North America, the growing emphasis on smart electricity and the expansion of intelligent electricity meters in homes and offices are key drivers for the market. The region's smart grid technology development, including solar energy and renewable power sources, is a significant factor. Advanced metering devices, network management software, and distribution automation systems are integral components of this growth. Industrial plants and commercial establishments are also investing in smart grid technologies, such as steam turbines and smart thermal grids, to optimize energy supply security and reduce carbon footprints. Utility service providers are integrating hardware, system integration services, and consulting services to ensure regulatory standards are met.

The digital oilfield is also adopting smart grid technologies for improved efficiency. The US, as a leading investor in smart energy solutions, is poised for market growth due to extensive smart grid deployment. The region's smart grid projects, including large-scale deployments and smart solar initiatives, are expected to present attractive data analytics projections during the forecast period. Utility service providers are actively implementing these projects, having completed various pilot programs and initiating rollouts.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Smart Energy Industry?

- Rising adoption of smart grid technologies is the key driver of the market. The global adoption of smart grids is driving the demand for smart energy solutions. Utility providers are integrating advanced technologies, such as remote terminal units, intelligent electronic devices, and supervisory control and data acquisition systems, into their transmission and distribution networks. These technologies enhance grid reliability and promote energy efficiency. In addition, the installation of smart meters in consumer households is increasing. Smart meters serve as a bridge between utilities and homeowners, enabling real-time or near real-time energy consumption data exchange.

- This information empowers consumers to monitor their energy usage effectively. The integration of smart grids and smart meters is transforming the energy sector, offering numerous benefits to both utilities and consumers.

What are the market trends shaping the Smart Energy Industry?

- Growing investment in smart cities and smart homes is the upcoming market trend. The smart home market is experiencing significant growth as consumers increasingly prioritize convenience and efficiency in their daily lives. This trend is transforming the residential real estate sector, with the primary objective being to enhance comfort, convenience, security, entertainment, and sustainability. Advanced sensor technologies are making smart home solutions more accessible and affordable for the average household. Homeowners can now connect various appliances, including heating modules, lighting systems, air conditioning units, computers, television sets, entertainment systems, security devices, and camera systems, using their smartphones and tablets.

- Artificial intelligence is integrated into home appliances to accurately predict consumer preferences based on historical data, offering personalized experiences. The adoption of these technologies is driven by the desire for energy savings, improved security, and enhanced convenience.

What challenges does the Smart Energy Industry face during its growth?

- Intermittency in solar energy is a key challenge affecting the industry growth. Smart solar systems are gaining significance in the renewable energy market due to the intermittency associated with solar energy. Solar energy's dependence on weather and climatic conditions makes it an unreliable energy source, producing varying amounts of power. This volatility affects the entire power system and grid stability. To mitigate these issues, solar power plants require additional equipment to regulate power production and maintain grid stability. The demand for smart solar systems is driven by the need to address these challenges and optimize energy production.

- These systems use advanced technologies such as energy storage and predictive analytics to manage power generation and distribution effectively. The integration of smart solar systems can help ensure a consistent power supply, improve grid reliability, and enhance overall energy efficiency.

Exclusive Customer Landscape

The smart energy market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the smart energy market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, smart energy market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - ABB Electrification delivers advanced energy solutions, integrating technology and sustainability for optimized power management.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Cisco Systems Inc.

- Delta Electronics Inc.

- Enphase Energy Inc.

- General Electric Co.

- Honeywell International Inc.

- International Business Machines Corp.

- Itron Inc.

- Kontron AG

- Larsen and Toubro Ltd.

- Mitsubishi Electric Corp.

- Nextera Energy Inc.

- Robert Bosch GmbH

- Rockwell Automation Inc.

- SAP SE

- Schneider Electric SE

- Siemens AG

- SMART Energy Solutions

- Toshiba Corp.

- Xylem Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses the development, implementation, and management of intelligent electricity systems for various sectors, including homes and offices. These systems rely on advanced metering devices, network infrastructure, and software components to optimize energy consumption and distribution. The integration of renewable energy sources, such as solar energy, into smart grids is a significant trend in this market. Intelligent electricity meters play a crucial role in smart energy systems by providing real-time data on energy usage. This data enables network management software to optimize energy distribution and consumption, reducing overall energy waste and improving energy supply security. The residential sector is a major focus of smart energy development due to the growing importance of reducing carbon footprints and the increasing adoption of renewable power sources.

The industrial sector also benefits from smart energy systems, with steam turbines and other energy-intensive equipment being optimized through the use of advanced metering devices and distribution automation systems. The integration of smart grid technologies in industrial plants allows for more efficient energy management and reduces the reliance on fossil fuels. The development of smart energy systems requires significant capital expenditures for hardware and system integration services. Consulting services are also essential for ensuring technical expertise and regulatory compliance. The digital oilfield is another area where smart energy technologies are being applied to optimize energy production and reduce costs.

Smart thermal grids are another emerging trend in the market. These systems enable the efficient management of heating and cooling systems in commercial and residential buildings, reducing energy waste and improving overall energy efficiency. The integration of renewable energy sources into smart grids is a key challenge in the market. The intermittent nature of renewable energy sources requires advanced network management software to optimize energy distribution and ensure grid stability. The development of smart solar and other renewable power sources is a major focus of research and development efforts in the market. The market is characterized by the development and implementation of intelligent electricity systems for various sectors.

These systems rely on advanced metering devices, network infrastructure, and software components to optimize energy consumption and distribution. The integration of renewable energy sources and the optimization of industrial energy production are major trends in this market. The development of smart energy systems requires significant capital expenditures and technical expertise, making consulting services and system integration essential. The optimization of energy usage in commercial and residential buildings through smart thermal grids is another emerging trend in the market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

191 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 19.1% |

|

Market growth 2024-2028 |

USD 7.26 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

18.19 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Smart Energy Market Research and Growth Report?

- CAGR of the Smart Energy industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the smart energy market growth of industry companies

We can help! Our analysts can customize this smart energy market research report to meet your requirements.

RIA -

RIA -