US Premature Ejaculation Disorder Market Size 2024-2028

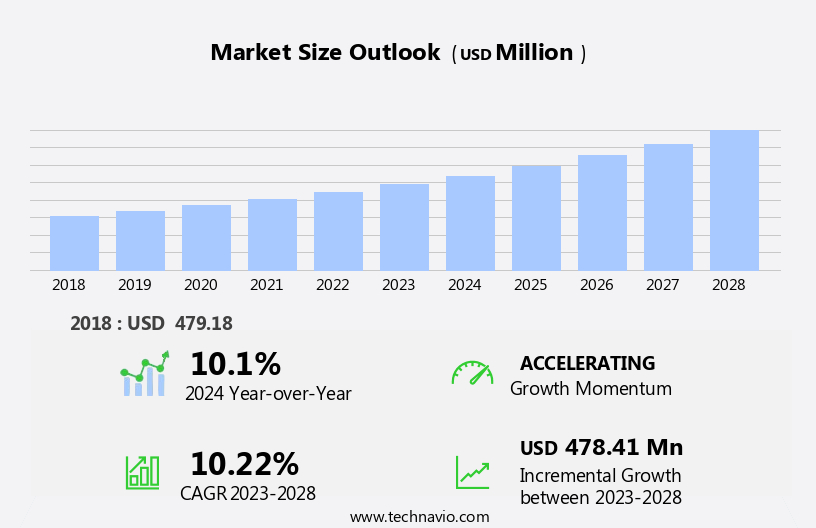

The US premature ejaculation disorder market size is forecast to increase by USD 478.41 million at a CAGR of 10.22% between 2023 and 2028. The premature ejaculation disorder market in the US is experiencing significant growth due to the high efficacy of off-label drugs, leading to increased usage by individuals seeking treatment. This trend is driven by the availability of effective medications, such as selective serotonin reuptake inhibitors (SSRIs), which offer prolonged intercourse and improved sexual satisfaction. Another key trend is the use of nanotechnology in drug delivery systems, enabling targeted and controlled release of drugs for enhanced efficacy and reduced side effects.

However, the market faces challenges related to the side effects of available treatments, including dizziness, headaches, and gastrointestinal issues, which may limit their widespread adoption. Additionally, the stigma surrounding premature ejaculation and the lack of awareness about the disorder hinder market growth. Despite these challenges, the US Premature Ejaculation Disorder market growth is steady due to the increasing demand for effective treatments and the ongoing research and development efforts in the field.

What will be the US Premature Ejaculation Disorder Market Size During the Forecast Period?

Premature ejaculation (PE) is a common issue affecting many men, marked by the inability to control ejaculation during intercourse, leading to distress and a reduced quality of life. The growing demand for PE therapeutics has led to the development of innovative drug therapies, including topical amide anesthetics and selective serotonin reuptake inhibitors (SSRIs), with OTC (Over-the-Counter) options becoming more accessible. Product diversification, such as combination therapies and telemedicine services, is a key trend in the market, while off-label drugs are also being explored for their effectiveness.

Diagnostic methods include self-reporting and clinical assessments, with digital platforms providing easy access to resources. Non-pharmacological interventions, such as pelvic floor exercises and mindfulness practices, are gaining popularity as well. Vendor analysis shows that the PE market is expected to grow significantly, driven by increasing awareness of PE causes, risk factors, and the demand for effective treatments..

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018 - 2022 for the following segments.

- Route Of Administration

- Oral

- Topical

- Drug Class

- SSRIs

- PDE5 inhibitors

- Amide anesthetics

- Others

- Distribution Channel

- Prescription

- OTC

- Geography

- US

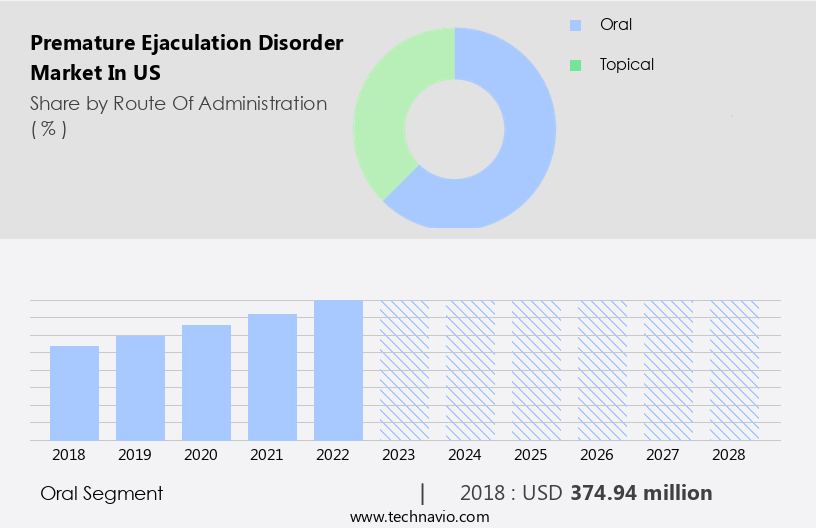

By Route Of Administration Insights

The Oral segment is estimated to witness significant growth during the forecast period The significant market share of the oral route segment can be attributed to the popularity and high preference for oral medication as the first line of treatment for premature ejaculation, owing to its ease of use and wide availability. These drugs are available in different forms, such as tablets, capsules, and liquids.

Furthermore, The significant premature ejaculation disorder market share of the oral route segment can be attributed to the popularity and high preference for oral medication as the first line of treatment for premature ejaculation, owing to its ease of use and wide availability. These drugs are available in different forms, such as tablets, capsules, and liquids. The traditional agents to prolong coitus were alpha amino benzoate and phenoxybenzamine, both of which were associated with severe side effects. Tricyclic antidepressants and, finally, SSRIs were used due to their sustained efficacy on ejaculatory latency and tolerable side effect profile. The mechanism for delayed ejaculation with SSRIs is generally related to the inhibition of various descending pathways linked with the ejaculatory reflex. This is supported by studies that show significant variations in cortical serotonergic function between patients with premature ejaculation in males. Such factors are expected to fuel the segment growth which in turn drives the market growth during the forecast period.

Get a glance at the market share of various segments Request Free Sample

The oral segment was valued at USD 374.94 million in 2018 and showed a gradual increase during the forecast period.

Our market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

US Premature Ejaculation Disorder Market Driver

The high efficacy of off-label drugs leading to high usage by people is the key driver of the market. The premature ejaculation (PE) disorder market in the US is primarily driven by the widespread use of off-label drugs, generic versions of patent-expired medicines, and over-the-counter (OTC) formulations. Men seeking treatment for PE often consult healthcare professionals for various therapeutic options. In the US, only one approved product exists for PE treatment. However, the dominance of off-label drugs, particularly those from the selective serotonin reuptake inhibitors (SSRIs) and phosphodiesterase-5 inhibitors (PDE5i) classes, has significantly influenced the market's growth. These drugs, used off-label, have shown promising results in managing PE, with improved drug delivery systems, such as nanotechnology, enhancing bioavailability and drug release rates.

Anxiety, depression, abnormal hormone levels, inherited traits, psychological factors, early sexual experiences, and sexual abuse are some common factors contributing to PE. Treatment approaches include anesthetic agents like lidocaine-based sprays, behavioral techniques, and medical interventions. The ongoing research in PE therapeutics, including the development of new drugs and delivery systems, is expected to further expand the market.

US Premature Ejaculation Disorder Market Trends

The use of nanotechnology in drug delivery is the upcoming trend in the market. Premature ejaculation (PE), a common condition affecting men, has been a subject of interest for healthcare professionals due to its significant impact on sexual health and well-being. PE is characterized by the incapability to control ejaculation during sexual intercourse, leading to a rapid climax or early ejaculation. The causes of PE are multifactorial, with both psychological and biological factors contributing. These include early sexual experiences, sexual abuse, poor body image, depression, anxiety, abnormal hormone levels, inherited traits, inflammation, infection, prostate issues, and urethral irritation. Nanotechnology, introduced in the 1980s, has emerged as a promising solution to enhance the efficacy and safety of PE therapeutics.

Furthermore, this advanced technology offers new approaches to medicine delivery, improving drug absorption and bioavailability, as well as controlling drug release rate. Off-label use of PDE-5 inhibitors, such as tadalafil, sildenafil, and vardenafil, has gained popularity due to their ability to inhibit the PDE-5 isoenzyme competitively. These drugs, which are orally administered, have shown significant improvement in PE symptoms. However, the development of nanotechnology-based PE therapeutics, such as Lidocaine-based sprays, offers a more targeted and effective approach to treating PE. Behavioral techniques and medical interventions remain essential components of PE management, and diagnostic methods continue to evolve to better identify and assess this condition as per Premature Ejaculation Disorder Market Trends

US Premature Ejaculation Disorder Market Challenge

The side effects of available drugs is a key challenge affecting the market growth. The premature ejaculation (PE) disorder market in the US comprises various therapeutic options, including over-the-counter (OTC) drugs and off-label use of certain medications. Men seeking treatment for PE face challenges due to the side effects associated with some therapeutics. For instance, Phosphodiesterase-5 (PDE5) inhibitors, which are FDA-approved for erectile dysfunction, are sometimes used off-label for PE. However, these drugs carry potential risks such as prolonged erections lasting over four hours and priapism, a serious condition characterized by a painful erection that persists for more than six hours. Nanotechnology offers promising solutions for PE therapeutics by enhancing medicine delivery, bioavailability, and drug release rate.

Furthermore, anesthetic agents like lidocaine-based sprays have gained popularity as a behavioral technique for PE treatment. These sprays are applied to the penis prior to sexual intercourse to desensitize the penis and delay ejaculation. PE is a complex condition influenced by both psychological and biological factors. Early sexual experiences, sexual abuse, poor body image, depression, anxiety, abnormal hormone levels, inherited traits, inflammation, infection, prostate issues, and urethral irritation are some of the factors contributing to PE. Diagnostic methods include self-reporting, clinical interviews, and physical examinations. Behavioral techniques, medical interventions, and pharmacological therapies are the primary treatment modalities for PE.

Moreover, behavioral techniques include the stop-start method, the squeeze technique, and the use of anesthetic agents. Medical interventions include the use of selective serotonin reuptake inhibitors (SSRIs) and tricyclic antidepressants (TCAs). Pharmacological therapies include PDE5 inhibitors, topical anesthetics, and local anesthetics. In conclusion, the PE disorder market in the US presents significant opportunities for the development of novel therapeutics that address the underlying causes of PE while minimizing side effects. Nanotechnology and anesthetic agents are promising areas of research for the development of effective PE therapeutics. Collaboration between healthcare professionals, researchers, and industry players is essential to improve the understanding of PE and develop effective, safe, and accessible treatment options for men.

Exclusive Customer Landscape

As per US Premature Ejaculation Disorder Market Analysis, the market forecast report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Absorption Pharmaceuticals LLC - The company offers premature ejaculation disorder therapeutics such as delay spray, home and away, and threesome.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Absorption Pharmaceuticals LLC

- Alembic Pharmaceuticals Ltd.

- Amneal Pharmaceuticals Inc.

- Bayer AG

- Cipla Ltd.

- Eli Lilly and Co.

- Johnson and Johnson

- Lupin Ltd.

- NeuroHealing Pharmaceuticals Inc.

- Novartis AG

- Pfizer Inc.

- Prinston Pharmaceutical Inc.

- Teva Pharmaceutical Industries Ltd.

- Veru Inc.

- VIVUS LLC

- Aytu BioPharma Inc.

- Royalty Pharma plc

- Sebela Pharmaceuticals Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Premature ejaculation (PE) is a common sexual health issue among men, characterized by the incapability to control ejaculation during sexual intercourse, resulting in rapid or early ejaculation. PE can be caused by both psychological and biological factors, including early sexual experiences, sexual abuse, poor body image, depression, anxiety, abnormal hormone levels, inherited traits, inflammation, infection, prostate issues, and urethral irritation.

Furthermore, healthcare professionals estimate that up to 30% of men experience PE at some point in their lives. PE therapeutics include over-the-counter (OTC) drugs, off-label use of certain medications, anesthetic agents, and PE-specific treatments like Promescent, a lidocaine-based spray. Nanotechnology is being explored for improving medicine delivery, bioavailability, and drug release rate to enhance the efficacy of PE treatments. Behavioral techniques and medical interventions are also used to manage PE. Diagnostic methods include self-reporting, physical examinations, and sexual function assessments. PE is a significant concern for men's sexual health, and ongoing research aims to develop more effective and accessible treatment options.

|

Premature Ejaculation Disorder Market Scope

|

|

|

Report Coverage |

Details |

|

Page number |

152 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.22% |

|

Market growth 2024-2028 |

USD 478.41 million |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

10.1 |

|

Key companies profiled |

Absorption Pharmaceuticals LLC, Alembic Pharmaceuticals Ltd., Amneal Pharmaceuticals Inc., Bayer AG, Cipla Ltd., Eli Lilly and Co., Johnson and Johnson, Lupin Ltd., NeuroHealing Pharmaceuticals Inc., Novartis AG, Pfizer Inc., Prinston Pharmaceutical Inc., Teva Pharmaceutical Industries Ltd., Veru Inc., VIVUS LLC, Aytu BioPharma Inc., Royalty Pharma plc, and Sebela Pharmaceuticals Inc. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles,market forecast , fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across US

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -