Private 5g Market Size 2025-2029

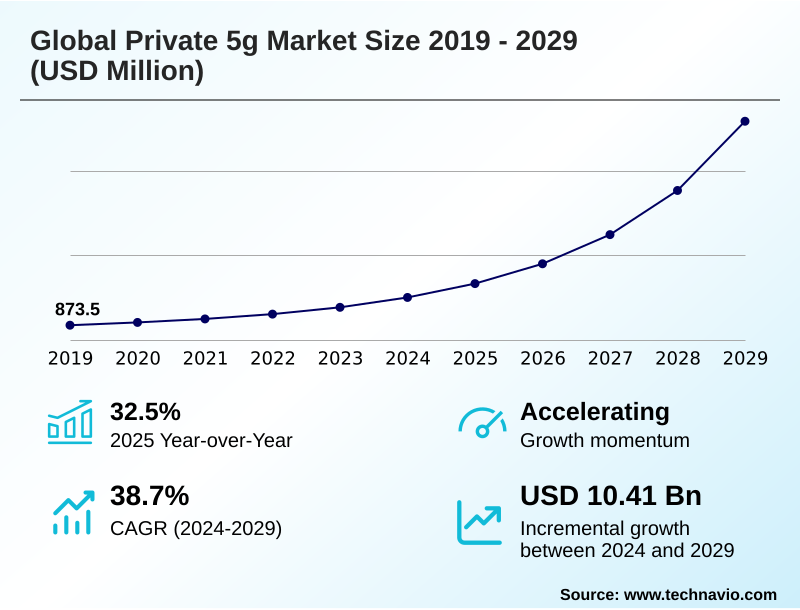

The private 5g market size is valued to increase by USD 10.41 billion, at a CAGR of 38.7% from 2024 to 2029. Growing demand for enhanced connectivity for industry 4.0 and mission-critical applications will drive the private 5g market.

Major Market Trends & Insights

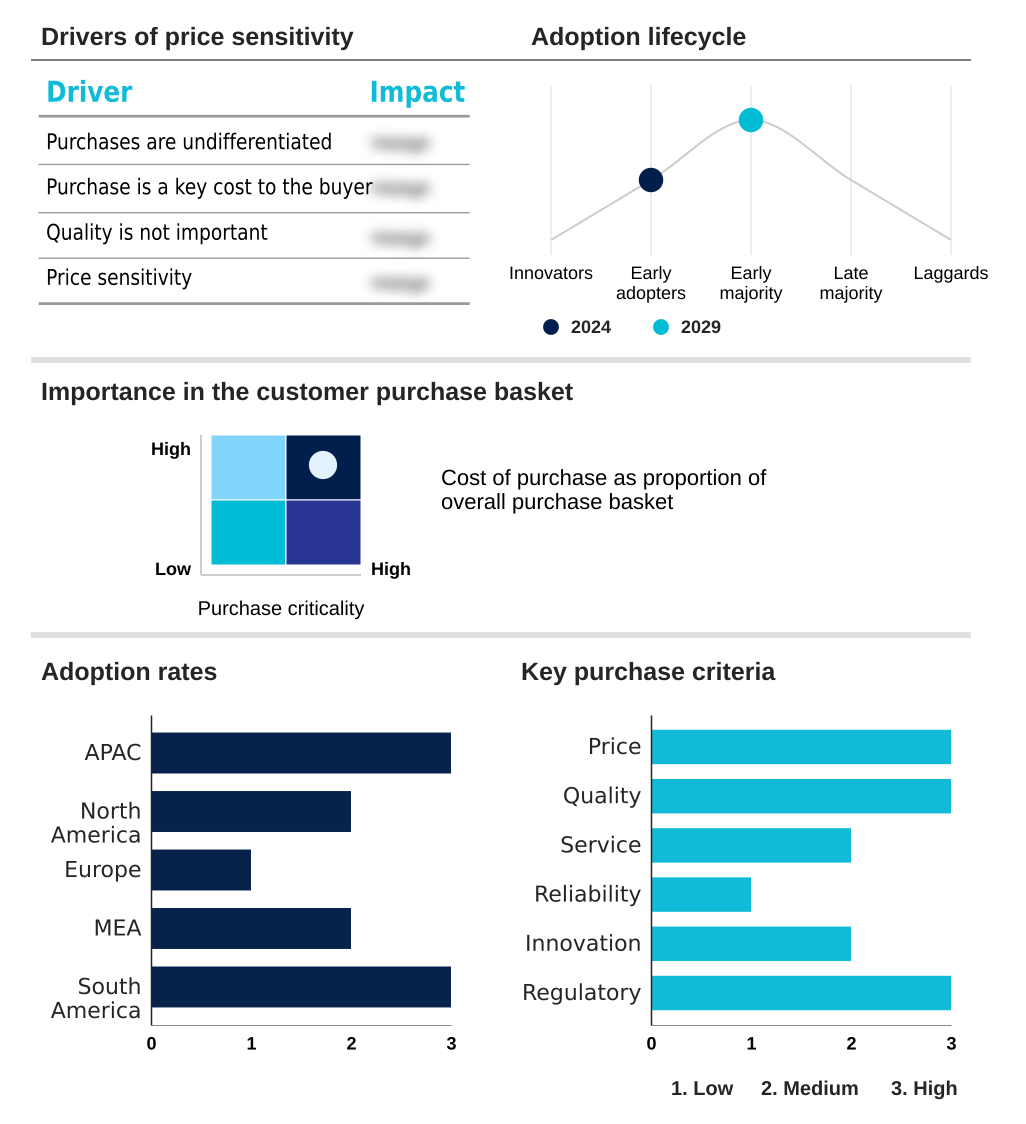

- APAC dominated the market and accounted for a 38.7% growth during the forecast period.

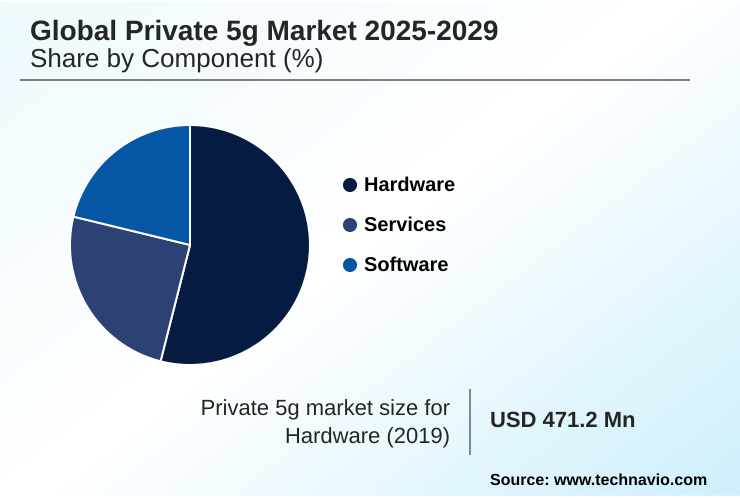

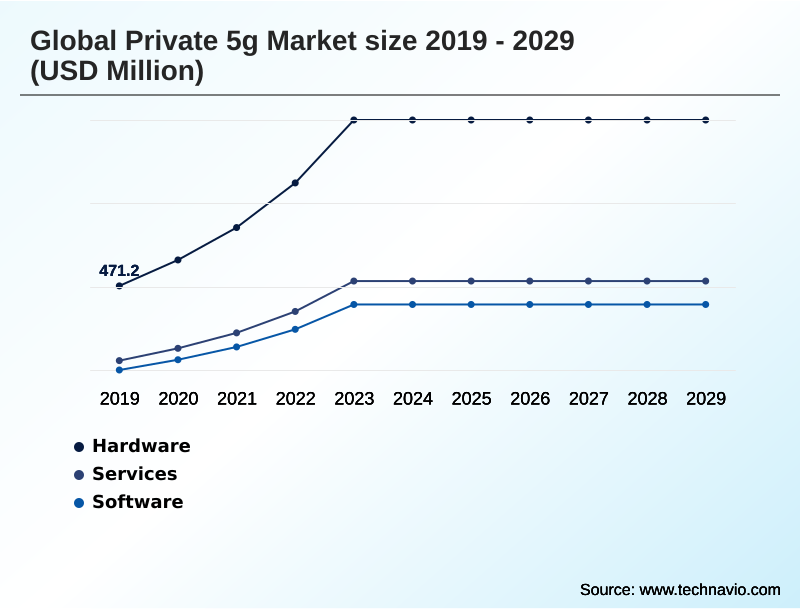

- By Component - Hardware segment was valued at USD 1.04 billion in 2023

- By Type - Licensed segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 12.05 billion

- Market Future Opportunities: USD 10.41 billion

- CAGR from 2024 to 2029 : 38.7%

Market Summary

- The private 5G market is transitioning from a niche concept to a cornerstone of enterprise digital transformation, driven by the stringent demands of Industry 4.0. Conventional wireless solutions often fail to provide the deterministic performance required for advanced operational technology (ot) integration. This technology offers a dedicated, enterprise-owned infrastructure that ensures ultra-reliable low-latency communication (urllc) and massive machine-type communication (mmtc).

- For instance, a smart factory can deploy a private network to guarantee sub-millisecond latency for industrial automation control loops and autonomous mobile robots, while simultaneously connecting thousands of sensors for predictive maintenance analytics. This level of control, inherent in a service-based architecture (sba), allows for customized private 5g network slicing to isolate critical traffic.

- However, adoption is tempered by the complexity of radio frequency (rf) planning and the need for specialized skills. The trend toward network-as-a-service (naas) models and open ran standards is mitigating these challenges, making deployments more financially and operationally viable for a wider range of industries seeking to secure a competitive edge through enhanced connectivity and on-premise data processing.

What will be the Size of the Private 5g Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Private 5g Market Segmented?

The private 5g industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Hardware

- Services

- Software

- Type

- Licensed

- Shared

- Frequency range

- Mid

- mmWave

- Low

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment is evolving beyond monolithic systems, driven by a strategic shift toward radio access network (ran) disaggregation.

This trend, underpinned by open ran standards, allows enterprises to build best-of-breed networks, improving system performance for high-resolution machine vision by up to 15%. The core network leverages a service-based architecture (sba), while new ran compute processors enhance edge capabilities.

Companies are moving toward a complete end-to-end network solution, utilizing software-defined networking (sdn) to manage quality of service (qos) parameters dynamically.

This supports demanding applications from augmented reality for remote assistance and automated port terminal operations to real-time asset tracking, ensuring secure campus-wide connectivity for use cases like live event production broadcasting.

The Hardware segment was valued at USD 1.04 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 38.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Private 5g Market Demand is Rising in APAC Get Free Sample

The global landscape is characterized by varied regional adoption strategies and regulatory environments. In North America, the citizens broadband radio service (cbrs) framework, governed by a spectrum access system (sas), has democratized access to spectrum, fueling a diverse ecosystem.

This has spurred deployments of non-public mobile networks built on a cloud-native 5g core with a distributed user plane function (upf) to support the industrial internet of things (iiot).

In contrast, APAC's market growth, which is expanding at a rate approximately 1% higher than North America's, is driven by manufacturing-led economies. These regions leverage enterprise-owned infrastructure to gain competitive advantages.

Deployments increasingly feature a mobile edge computing (mec) platform to enable real-time video analytics for predictive maintenance analytics, reducing equipment failures by up to 20%. This supports smart city infrastructure and high-density venue connectivity, ensuring a resilient communications network.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic implementation is increasingly focused on specialized use cases and architectures that deliver measurable business outcomes. The debate over private 5g vs wi-fi 6e performance comparison is settling, with enterprises recognizing the need for urllc for industrial robotics control, a domain where cellular technology excels.

- The roi calculation for private 5g in manufacturing is becoming clearer as deployments demonstrate tangible gains from reduced downtime and enhanced automation. Architecturally, a private 5g edge computing deployment architecture is standard for enabling mec integration for low-latency applications. Operationally, managing esim in private 5g networks is a key focus, simplified by naas models for private cellular networks.

- Security is paramount, with private 5g security for zero-trust models becoming a baseline requirement, governed by strict private 5g network security policy control. The cbrs shared spectrum for enterprise 5g in the US has created a blueprint for accessible deployments. Globally, firms are developing a private lte to 5g migration strategy to leverage existing investments.

- Key trends include network slicing for ot and it convergence, the rise of open ran benefits in private networks, and using private 5g for autonomous vehicle fleets. This is underpinned by a focus on data sovereignty with on-premise 5g core and creating a hybrid network for campus and public roaming.

- Firms leveraging these strategies report operational efficiencies that are often double those of legacy systems, particularly when automating private network operations with aiops for deployments like mmwave deployments for high-density venues and iiot connectivity with private 5g.

What are the key market drivers leading to the rise in the adoption of Private 5g Industry?

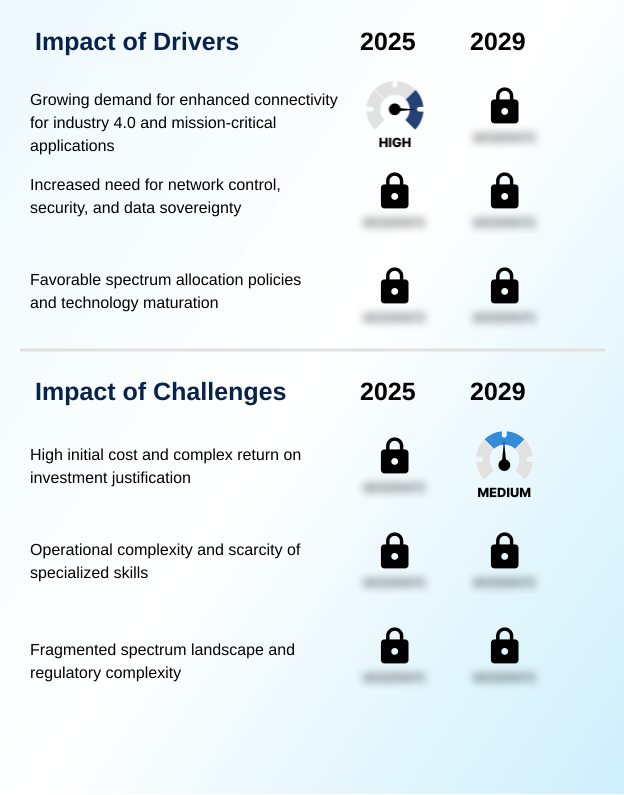

- The growing demand for enhanced connectivity to support Industry 4.0 and mission-critical applications serves as a primary driver for market adoption.

- The primary market drivers are the stringent performance requirements of modern industrial applications that legacy systems cannot meet.

- The need for ultra-reliable low-latency communication (urllc) is paramount for industrial automation control loops, with deployments achieving response times under 5 milliseconds for precise autonomous guided vehicle (agv) control.

- Concurrently, massive machine-type communication (mmtc) supports the connection of thousands of devices for critical infrastructure security, while enhanced mobile broadband (embb) facilitates data-intensive applications.

- Private 5g network slicing is crucial for operational technology (ot) integration, ensuring guaranteed performance for distinct processes. This is vital for autonomous mobile robots (amr), remote-controlled heavy equipment, and smart oilfield projects.

- The integration of time-sensitive networking (tsn) further enhances determinism, with implementations improving safety incident rates by up to 20% through reliable connected worker safety solutions.

What are the market trends shaping the Private 5g Industry?

- A pronounced shift toward network-as-a-service and managed service models is reshaping procurement, making private 5G more accessible to a broader range of enterprises.

- Market trends are centered on lowering adoption barriers and simplifying operational complexity. The shift to network-as-a-service (naas) models is significant, with some providers reporting this can reduce initial capital expenditures for enterprises by over 60% compared to traditional procurement. This trend is complemented by the rise of hybrid private-public network architectures, which offer seamless connectivity.

- On the operational front, ai for operations (aiops) is being integrated to automate management, decreasing network fault resolution times by an average of 30%. The technological underpinning involves a move to virtualized network functions (vnf) and containerized network functions (cnf), enabling agile deployments.

- Furthermore, dynamic spectrum sharing is gaining traction, providing more flexible and efficient spectrum use, while many organizations are initiating their journey with a private lte network as a stepping stone to full 5G, supporting smart factory initiatives and mission-critical communications.

What challenges does the Private 5g Industry face during its growth?

- The high initial cost of deployment, coupled with the complexity of justifying return on investment, presents a key challenge to widespread industry growth.

- Enterprises face significant challenges related to operational complexity and regulatory fragmentation. Managing a 3gpp-standardized 5g core requires specialized skills, and the complexity of radio frequency (rf) planning can extend project timelines by an average of 25%. Furthermore, esim lifecycle management introduces new operational workflows. The pursuit of data sovereignty compliance often mandates on-premise data processing, adding to infrastructure costs.

- The fragmented global landscape for local spectrum licensing means navigating different rules for mid-band and millimeter wave (mmwave) spectrum in each country, with the process of securing a license taking over six months in some regions. Implementing a robust zero-trust security architecture across this new network domain is non-trivial.

- These hurdles temper adoption, particularly for applications like remote surgical procedures, precision farming applications, industrial metaverse platforms, intelligent transportation systems, and large-scale unmanned aerial vehicle (uav) operation.

Exclusive Technavio Analysis on Customer Landscape

The private 5g market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the private 5g market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Private 5g Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, private 5g market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airspan Networks Inc. - Offerings include private 5G with multi-access edge computing, designed to deliver ultra-low latency and support localized data processing for mission-critical enterprise applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airspan Networks Inc.

- AT and T Inc.

- Celona Inc.

- Ciena Corp.

- Cisco Systems Inc.

- CommScope Holding

- Hewlett Packard

- Huawei Technologies Co. Ltd.

- Juniper Networks Inc.

- Mavenir Systems Inc.

- Microsoft Corp.

- NEC Corp.

- Nokia Corp.

- Qualcomm Inc.

- Samsung Electronics Co. Ltd.

- Telefonaktiebolaget Ericsson

- Verizon Communications Inc.

- ZTE Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Private 5g market

- In September, 2024, Samsung Electronics Co. Ltd. and NEC Corp. announced a partnership to deliver joint private 5G network solutions to enterprise customers, combining Samsung's 5G portfolio with NEC's system integration expertise.

- In November, 2024, Hewlett Packard Enterprise Co. enhanced its private networking offerings by integrating its Athonet core network software with its Aruba wireless technologies, creating a unified management interface for both Wi-Fi and private 5G.

- In January, 2025, Verizon Communications Inc. secured a contract to deploy a private 5G network for the U.S. Department of Energy Pacific Northwest National Laboratory, providing a secure communications platform for advanced research programs.

- In April, 2025, Nokia Corp. announced an expansion of its private 5G network for the City of Las Vegas, utilizing CBRS shared spectrum to support a wide range of smart city initiatives, including public safety and remote asset monitoring.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Private 5g Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 38.7% |

| Market growth 2025-2029 | USD 10411.5 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 32.5% |

| Key countries | China, Japan, South Korea, India, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is defined by a technological convergence aimed at delivering enterprise-owned infrastructure with carrier-grade performance. Deployments are increasingly leveraging a service-based architecture (sba) and a cloud-native 5g core, often managed via network-as-a-service (naas) models.

- Key enablers include radio access network (ran) disaggregation through open ran standards and dynamic spectrum sharing frameworks like citizens broadband radio service (cbrs), which is managed by a spectrum access system (sas).

- The technology delivers on three core principles: ultra-reliable low-latency communication (urllc) for applications like autonomous guided vehicle (agv) control, massive machine-type communication (mmtc) for industrial internet of things (iiot), and enhanced mobile broadband (embb). Functionality is enhanced by private 5g network slicing, mobile edge computing (mec) platforms, and time-sensitive networking (tsn).

- For enterprises, this translates to tangible benefits from operational technology (ot) integration and on-premise data processing, secured by a zero-trust security architecture. A focus on simplified operations is driving adoption of ai for operations (aiops), which has been shown to reduce network downtime by up to 40%.

- The ecosystem is delivering end-to-end network solutions featuring advanced ran compute processors and sophisticated software-defined networking (sdn) to manage quality of service (qos) parameters, moving beyond private lte networks.

- Managing a 3gpp-standardized 5g core, including esim lifecycle management and radio frequency (rf) planning, remains complex but essential for harnessing technologies like millimeter wave (mmwave) spectrum and containerized network functions (cnf) within a non-public mobile network.

What are the Key Data Covered in this Private 5g Market Research and Growth Report?

-

What is the expected growth of the Private 5g Market between 2025 and 2029?

-

USD 10.41 billion, at a CAGR of 38.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Services, and Software), Type (Licensed, and Shared), Frequency Range (Mid, mmWave, and Low) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Growing demand for enhanced connectivity for industry 4.0 and mission-critical applications, High initial cost and complex return on investment justification

-

-

Who are the major players in the Private 5g Market?

-

Airspan Networks Inc., AT and T Inc., Celona Inc., Ciena Corp., Cisco Systems Inc., CommScope Holding, Hewlett Packard, Huawei Technologies Co. Ltd., Juniper Networks Inc., Mavenir Systems Inc., Microsoft Corp., NEC Corp., Nokia Corp., Qualcomm Inc., Samsung Electronics Co. Ltd., Telefonaktiebolaget Ericsson, Verizon Communications Inc. and ZTE Corp.

-

Market Research Insights

- Enterprise adoption is accelerating, driven by the need for secure campus-wide connectivity and data sovereignty compliance. Smart factory initiatives are leveraging private networks to enable a 25% improvement in automated warehouse logistics, while smart city infrastructure projects utilize them for intelligent transportation systems.

- Use cases range from high-density venue connectivity and live event production broadcasting to critical infrastructure security for a smart grid management system. The technology supports remote-controlled heavy equipment in smart oilfield projects and provides the resilient communications network needed for tactical communications network deployments.

- This enables transformative applications like digital twin applications, remote surgical procedures, industrial metaverse platforms, and precision farming applications, with deployments showing real-time asset tracking accuracy improving by over 99.5%.

- It also underpins mission-critical communications for connected worker safety solutions, autonomous mobile robots (amr), high-resolution machine vision, augmented reality for remote assistance, industrial automation control loops, real-time video analytics, predictive maintenance analytics, and automated port terminal operations with unmanned aerial vehicle (uav) operation.

We can help! Our analysts can customize this private 5g market research report to meet your requirements.

RIA -

RIA -