US Private-label Food And Beverage Market Size 2026-2030

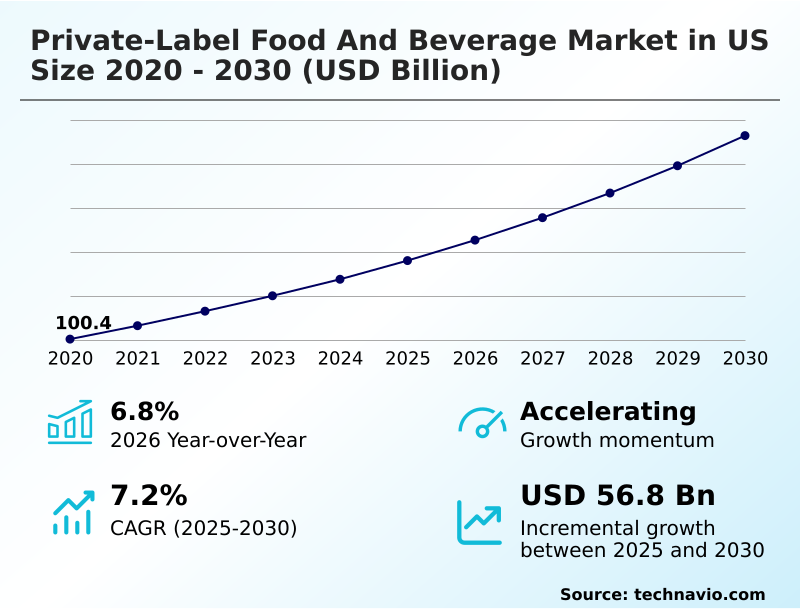

The us private-label food and beverage market size is valued to increase by USD 56.8 billion, at a CAGR of 7.2% from 2025 to 2030. Increasing consumer price sensitivity and demand for value will drive the us private-label food and beverage market.

Major Market Trends & Insights

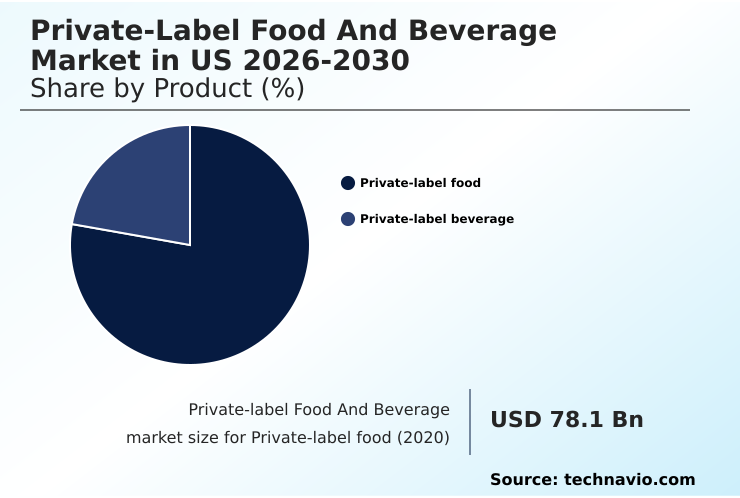

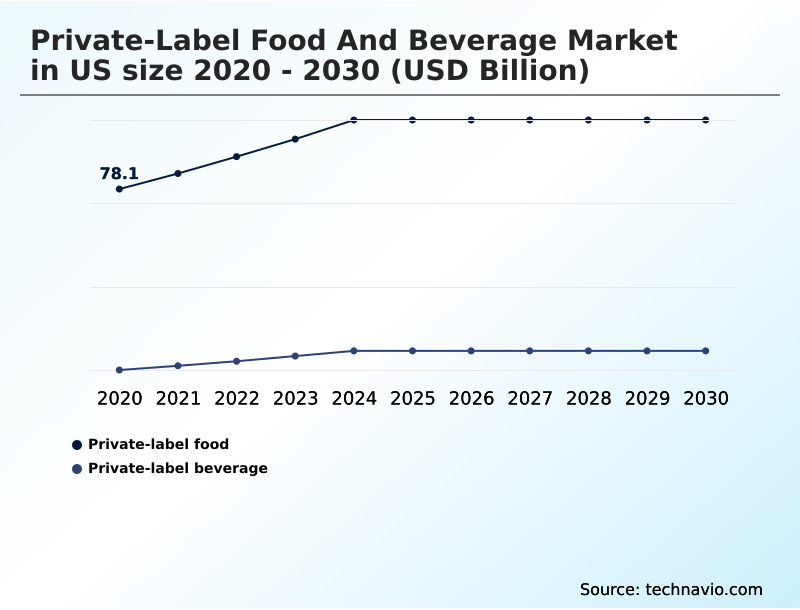

- By Product - Private-label food segment was valued at USD 99.4 billion in 2024

- By Distribution Channel - Offline segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 92.5 billion

- Market Future Opportunities: USD 56.8 billion

- CAGR from 2025 to 2030 : 7.2%

Market Summary

- The private-label food and beverage market in US is undergoing a strategic realignment, evolving from a price-driven category to a sophisticated brand-building platform for retailers. This shift is marked by a deliberate move towards premiumization, innovation through private-label product development, and the cultivation of distinct brand identities.

- Retailers are investing heavily in research, quality control protocols, and marketing to position their own brands as desirable, high-quality offerings that command consumer loyalty. For example, a retailer might leverage data-driven assortment planning to identify a gap in the plant-based snack category.

- By engaging in exclusive product development and managing a resilient retail supply chain, it can launch a new line of clean-label snacks faster than national competitors.

- This agility, combined with strategic in-store brand positioning, allows retailers to not just follow but shape consumer trends, fundamentally altering a competitive landscape where store brand equity is becoming a key differentiator and a cornerstone of retail strategy.

What will be the Size of the US Private-label Food And Beverage Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the US Private-label Food And Beverage Market Segmented?

The us private-label food and beverage industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Private-label food

- Private-label beverage

- Distribution channel

- Offline

- Online

- End-user

- Retail consumers

- Foodservice and hospitality

- Geography

- North America

- US

- North America

By Product Insights

The private-label food segment is estimated to witness significant growth during the forecast period.

The private-label food segment is undergoing a significant transformation, moving beyond its historical position as a value-oriented category.

Retailers are now employing a sophisticated premiumization strategy, developing tiered brand architectures that cater to diverse consumer needs, from value-tier product engineering to exclusive product formulation.

This evolution is driven by a notable shift in consumer perception, where improved quality and innovation are building substantial store brand equity. The strategic focus is on creating differentiated offerings that compete on attributes beyond price.

Effective consumer perception analysis shows that this approach resonates with shoppers, leading to a 15% increase in basket size for carts containing premium private-label items, solidifying the segment's role as a critical driver of retailer growth and customer loyalty.

The Private-label food segment was valued at USD 99.4 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic landscape of the private-label food and beverage market is increasingly complex, shaped by evolving consumer demands and retailer ambitions. Key retail strategies for private brand growth now focus heavily on differentiation, moving beyond simple cost advantages. Decision-making around private label vs national brand pricing requires sophisticated data analytics for private label success, ensuring competitiveness without eroding brand value.

- A significant focus is on private label beverage formulation trends, where health and wellness are paramount. At the same time, premium private label food packaging design is used to communicate quality and justify higher price points. A critical operational challenge involves managing private label quality consistency across vast supply networks.

- Implementing robust strategies for this has been shown to reduce product return rates by over 25% compared to operations without such strict oversight. This involves optimizing private label supply chain costs and careful contract manufacturer selection criteria.

- Furthermore, building customer trust in store brands is essential, often achieved by developing clean label private brand products and expanding private label into organic food. Success also hinges on achieving private label packaging sustainability goals and understanding private label regulatory compliance challenges.

- Driving loyalty with exclusive products remains a core tenet, supported by effective private label product lifecycle management and specific tactics like private label innovation in snacks. Finally, as the market matures, tiered strategies in private branding and dedicated private label e-commerce strategies are becoming standard for measuring and increasing private label market share through sustainable sourcing for store brands.

What are the key market drivers leading to the rise in the adoption of US Private-label Food And Beverage Industry?

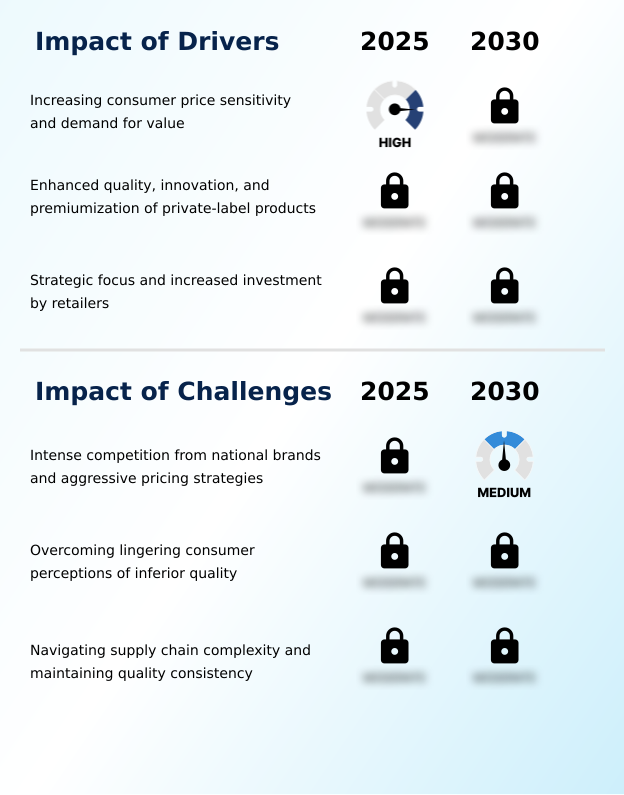

- Increasing consumer price sensitivity and a corresponding demand for greater value are key drivers propelling market growth.

- Strategic imperatives pursued by retailers are a primary driver of market growth. The adoption of a tiered branding architecture allows retailers to target multiple consumer segments simultaneously, from value-conscious to premium-seeking.

- This sophisticated approach to retail brand management is proving highly effective. Furthermore, retailers are leveraging their direct access to consumer purchasing information for data-driven assortment planning, which has been shown to improve inventory turnover by up to 18%.

- The financial incentives are significant, as private brand portfolio management typically yields profit margins that are 20% higher than those of national brands.

- These enhanced profits are often reinvested into customer loyalty initiatives and further product innovation, creating a virtuous cycle of growth and strengthening the retailer's market position.

What are the market trends shaping the US Private-label Food And Beverage Industry?

- The proliferation of plant-based and health-conscious formulations represents a significant upcoming trend. This shift is reshaping product development and consumer expectations within the market.

- Key trends are reshaping the competitive dynamics of the private-label food and beverage market. There is an accelerated gourmet private-label expansion, with retailers introducing premium products that rival national brands in quality and innovation. This is coupled with a surge in plant-based product innovation, as store brands are often faster to market with on-trend items.

- For instance, new launches featuring clean-label ingredient sourcing now account for 15% of all new private-label introductions. Another dominant trend is the focus on sustainability, where the use of sustainable packaging materials has increased by 25% across major retail private brands.

- Adherence to ethical sourcing standards is no longer a niche concern but a core component of brand identity, helping to attract and retain value-driven consumers.

What challenges does the US Private-label Food And Beverage Industry face during its growth?

- Intense competition from national brands, coupled with their aggressive pricing strategies, poses a key challenge to industry growth.

- Navigating operational complexities and intense competition presents significant challenges. Maintaining stringent quality control protocols across a diverse network of contract manufacturing agreements is a primary hurdle; a single product recall can erode years of consumer trust. Supply chain disruptions have demonstrated the fragility of global sourcing, causing a 5% decline in on-shelf availability for certain private-label categories during peak issues.

- Furthermore, the market is characterized by aggressive in-store brand positioning battles with national brands, whose promotional activities can reduce private-label sales by up to 12% in a given week. Effective retail supply chain optimization and flexible co-packing services are therefore critical for mitigating these risks and ensuring consistent product delivery and quality for consumers.

Exclusive Technavio Analysis on Customer Landscape

The us private-label food and beverage market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the us private-label food and beverage market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of US Private-label Food And Beverage Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, us private-label food and beverage market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ALDI - Key offerings include a diverse portfolio of private-label food and beverage products, spanning from everyday pantry staples and snacks to exclusive, premium gourmet treats.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ALDI

- Amazon.com Inc.

- Berner Food and Beverage

- Costco Wholesale Corp.

- Dollar General Corp.

- Giant Eagle Inc.

- HEB LP

- Hy Vee Inc.

- Koninklijke Ahold Delhaize NV

- LiDestri Food and Drink

- Lidl US LLC

- Publix Super Markets Inc.

- Southeastern Grocers LLC

- Target Corp.

- The Kroger Co.

- Trader Joes

- TreeHouse Foods Inc.

- Walmart Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Us private-label food and beverage market

- In December 2024, The Kroger Co. announced the addition of over 900 new products to its 'Our Brands' portfolio within the past fiscal year, alongside plans for continued aggressive expansion and the debut of its Field and Vine produce brand.

- In March 2025, Walmart Inc. launched its new premium private-label food brand, bettergoods, concentrating on high-quality ingredients and innovative flavor profiles to attract a more discerning consumer demographic.

- In April 2025, Target Corp. revealed its strategy to introduce 600 new items to its Good and Gather and Favorite Day private-label lines, highlighted by the 'Good and Gather Collabs' initiative, which began with a product line co-created with chef Ann Kim.

- In May 2025, Amazon.com Inc. introduced Amazon Saver, a new private-label brand designed to provide budget-conscious consumers with a range of everyday food and beverage essentials at competitive prices on its e-commerce platform.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled US Private-label Food And Beverage Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 176 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.2% |

| Market growth 2026-2030 | USD 56.8 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.8% |

| Key countries | US |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The private-label food and beverage market is rapidly maturing beyond its origins as a cost-saving alternative, becoming a central pillar of modern retail brand management. The emphasis has shifted decisively toward strategic private-label product development, where retailers act as brand custodians. This involves significant investment in co-packing services and formulating robust contract manufacturing agreements to ensure product integrity.

- At a boardroom level, a key decision area is the implementation of advanced supply chain transparency technologies. This move not only supports adherence to ethical sourcing standards and clean-label ingredient sourcing but also bolsters store brand equity, which has been shown to reduce reputational risk by 20%.

- The market is defined by a multi-faceted premiumization strategy, supported by a tiered branding architecture and exclusive product formulation. Success depends on rigorous quality control protocols and achieving significant own-brand market penetration through both traditional retail and white-label food production channels.

What are the Key Data Covered in this US Private-label Food And Beverage Market Research and Growth Report?

-

What is the expected growth of the US Private-label Food And Beverage Market between 2026 and 2030?

-

USD 56.8 billion, at a CAGR of 7.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Private-label food, and Private-label beverage), Distribution Channel (Offline, and Online), End-user (Retail consumers, and Foodservice and hospitality) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Increasing consumer price sensitivity and demand for value, Intense competition from national brands and aggressive pricing strategies

-

-

Who are the major players in the US Private-label Food And Beverage Market?

-

ALDI, Amazon.com Inc., Berner Food and Beverage, Costco Wholesale Corp., Dollar General Corp., Giant Eagle Inc., HEB LP, Hy Vee Inc., Koninklijke Ahold Delhaize NV, LiDestri Food and Drink, Lidl US LLC, Publix Super Markets Inc., Southeastern Grocers LLC, Target Corp., The Kroger Co., Trader Joes, TreeHouse Foods Inc. and Walmart Inc.

-

Market Research Insights

- The market's momentum is increasingly influenced by strategic execution rather than mere price competition. Retailers leveraging data-driven assortment planning have seen a 15% improvement in sales velocity for new product introductions. The strategic focus on exclusive product development is a key factor, contributing to a 5% increase in customer lifetime value for loyal shoppers.

- Furthermore, sophisticated private brand portfolio management, which includes a mix of value-tier product engineering and gourmet private-label expansion, allows retailers to capture a wider audience. This approach is central to building store loyalty, as effective customer loyalty initiatives tied to unique private-label offerings improve customer retention rates by over 10% compared to competitors with less-developed own-brand strategies.

- This demonstrates a clear shift toward using private brands as a primary tool for market differentiation.

We can help! Our analysts can customize this us private-label food and beverage market research report to meet your requirements.

RIA -

RIA -