Processed Red Meat Market Size 2026-2030

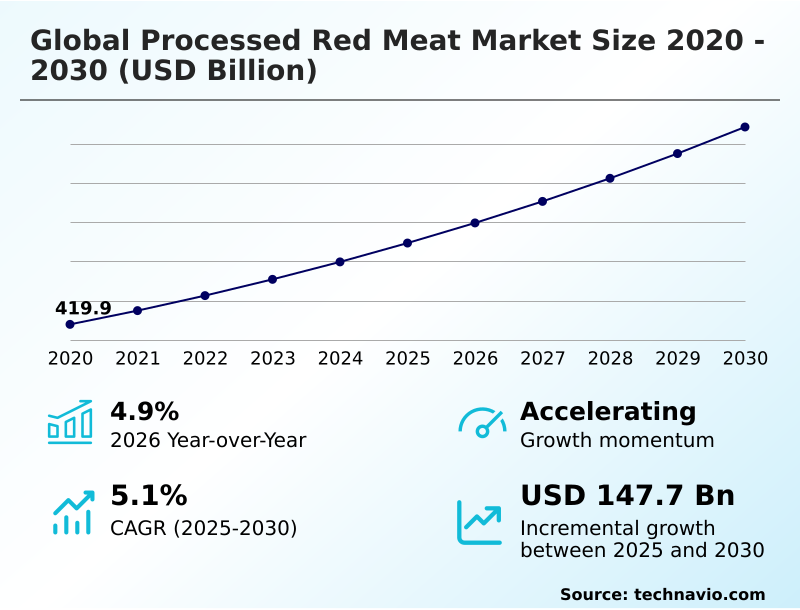

The processed red meat market size is valued to increase by USD 147.7 billion, at a CAGR of 5.1% from 2025 to 2030. Surging demand for convenience and ready-to-eat food products will drive the processed red meat market.

Major Market Trends & Insights

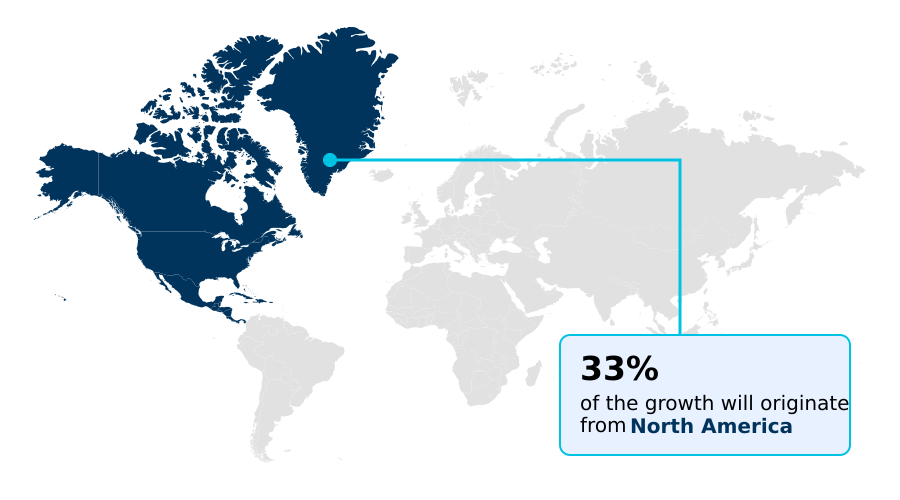

- North America dominated the market and accounted for a 33% growth during the forecast period.

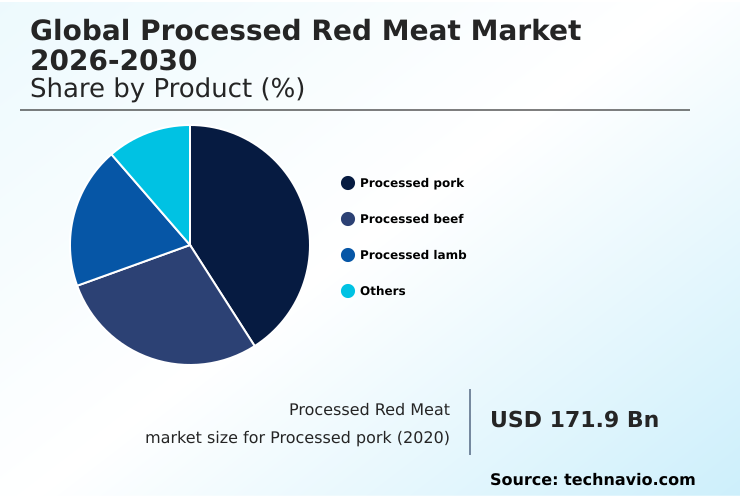

- By Product - Processed pork segment was valued at USD 209.4 billion in 2024

- By Type - Deli meats segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 251.2 billion

- Market Future Opportunities: USD 147.7 billion

- CAGR from 2025 to 2030 : 5.1%

Market Summary

- The processed red meat market is a dynamic industry shaped by the interplay of consumer convenience, technological innovation, and evolving health perceptions. A core driver is the global demand for ready-to-eat and easy-to-prepare food solutions, which aligns with modern, time-constrained lifestyles. Manufacturers leverage advanced techniques like modified atmosphere packaging and high-pressure processing to enhance shelf-life extension technologies and food safety.

- However, the sector faces headwinds from growing health consciousness, which has intensified scrutiny on ingredients like sodium nitrite and spurred a movement toward clean label meat formulation. For example, a mid-sized processor might pivot its strategy to focus on a line of nitrate-free processing products using natural preservative systems like celery powder, targeting a health-aware demographic.

- This involves significant R&D investment and navigating complex supply chains for ethically sourced livestock. Concurrently, the competitive threat from plant-based meat alternatives compels continuous innovation in flavor, texture, and product formats. The industry's trajectory depends on balancing traditional appeal with the demands for healthier, more sustainable, and transparently produced goods, using tools like livestock traceability systems to build consumer trust.

- The use of robotic processing automation is also becoming key for improving efficiency.

What will be the Size of the Processed Red Meat Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Processed Red Meat Market Segmented?

The processed red meat industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

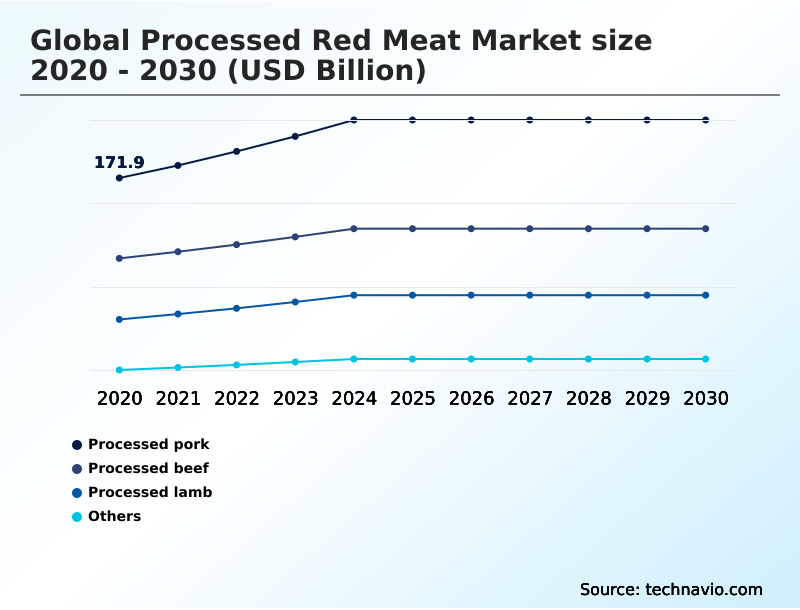

- Product

- Processed pork

- Processed beef

- Processed lamb

- Others

- Type

- Deli meats

- Sausages

- Bacon

- Others

- Distribution channel

- Supermarkets and hypermarkets

- Butcher shops

- Convenience stores

- Online retail

- Form factor

- Refrigerated

- Frozen

- Canned

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- Australia

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of World (ROW)

- North America

By Product Insights

The processed pork segment is estimated to witness significant growth during the forecast period.

The processed pork segment, representing a substantial portion of the market, is driven by its cultural acceptance and versatility. Innovation focuses on health-oriented reformulations, utilizing sodium reduction technology and alternatives like celery powder curing agent in place of traditional nitrates.

Advanced methods like bacterial culture fermentation and precise dry-curing process control are employed for artisanal products, while industrial-scale production relies on ensuring meat batter stability and maximizing protein extraction efficiency.

The rise of direct-to-consumer meat delivery services has increased access to specialty items. Growing consumer interest in sustainable meat production is also influencing sourcing decisions.

Packaging innovations, such as portion-controlled meat packs, cater to modern lifestyles, with processors utilizing advanced smoke generation technology to create unique flavor profiles. This segment is significant, with its market value having grown by over 5% annually.

The Processed pork segment was valued at USD 209.4 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Processed Red Meat Market Demand is Rising in North America Get Free Sample

The geographic landscape is defined by diverse regional preferences and regulatory standards. In mature markets like Europe, there is a strong emphasis on geographical indication labeling and animal welfare certification standards, driving demand for ethically sourced livestock.

Halal certified meat processing is non-negotiable in the Middle East and parts of Asia, while kosher meat processing standards are critical for specific segments. The demand for grass-fed beef processing and heritage breed pork products is rising globally.

Producers use advanced livestock traceability systems to verify claims related to antibiotic-free meat sourcing.

Processing techniques like meat grinding and emulsification and meat marination and injection are adapted to regional tastes, with texture profile analysis and sensory evaluation panels ensuring product quality.

Improving water-holding capacity remains a key technical goal to enhance yield, with some regions showing a 5.9% higher growth rate.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The future of the global processed red meat market 2026-2030 is increasingly tied to navigating complex consumer demands and technological shifts. A key area of focus is the impact of natural preservatives on shelf-life, as the industry moves away from synthetic additives. This directly addresses the growing consumer perception of clean label meats, which has become a primary purchasing driver.

- Operationally, the cost-benefit of robotic processing automation is a critical boardroom discussion, as firms seek to improve efficiency and mitigate labor shortages. For instance, facilities implementing automation have reported consistency improvements that reduce product rejects by over 20% compared to manual lines. The challenge of reducing sodium content in deli meats without compromising taste remains a significant R&D hurdle.

- Meanwhile, the strategic threat posed by plant-based alternatives vs traditional sausages is forcing innovation in both product formulation and marketing. Technological advancements such as high-pressure processing for pathogen reduction are becoming standard for ensuring food safety. Furthermore, traceability systems for grass-fed beef are essential for validating premium claims and building consumer trust.

- The logistical challenge of optimizing cold chain for refrigerated products continues to be a major operational focus. The role of heritage breeds in charcuterie is growing as producers seek differentiation through unique flavor profiles, even though it presents challenges of nitrate-free bacon production.

- Exploring the effectiveness of celery powder as cure and enhancing flavor development in dry-cured hams are central to this premiumization trend. Finally, packaging innovations for meat snacks are catering to on-the-go consumption, while the environmental footprint of meat processing and adherence to halal certification requirements for exporters are becoming critical for global market access.

- The market adoption of blended meat products and technical goals like improving water-holding capacity in ham and advances in sausage casing technology demonstrate the industry's multifaceted approach to future growth. Even the sensory analysis of reduced-fat sausages is now a key part of product development cycles.

What are the key market drivers leading to the rise in the adoption of Processed Red Meat Industry?

- The surging global demand for convenience and ready-to-eat food products, driven by profound socioeconomic shifts, is a key driver for market expansion.

- The relentless demand for convenience meal components and ready-to-eat protein solutions is a primary market driver.

- This is supported by advancements in shelf-life extension technologies, including modified atmosphere packaging and vacuum packaging systems, which are critical for private label meat programs and meal kit ingredient sourcing.

- Innovations like high-pressure processing improve food safety, while robotic processing automation enhances efficiency, reducing manual labor costs by up to 15%. The expansion of quick-service restaurant supply chains and foodservice meat applications further fuels growth.

- Effective cold chain logistics management ensures product integrity for these value-added meat preparations, while traditional curing and smoking methods continue to be refined for premium product lines, with some processors reporting a 25% improvement in throughput after automation.

What are the market trends shaping the Processed Red Meat Industry?

- A paradigm shift toward health-conscious product formulations is reshaping the industry. This trend reflects a growing consumer demand for cleaner ingredients and greater nutritional transparency.

- The market is witnessing a significant shift toward premiumization and health-conscious offerings. There is a growing demand for gourmet charcuterie products and premium artisanal offerings, driving innovation in artisanal meat processing and traditional fermentation processing techniques.

- Consumers are increasingly seeking nutritionally enhanced meats and reduced sodium formulations, pushing manufacturers toward clean label meat formulation and the adoption of natural preservative systems for nitrate-free processing. This trend has spurred development in casing technology for sausages and inspired new meat-based flavor profiles incorporating umami flavor enhancement and complex global cuisine flavor profiles.

- These changes are also creating opportunities for convenient high-protein snack formats that align with wellness trends, with some firms seeing a 20% increase in sales for products with cleaner ingredient decks.

What challenges does the Processed Red Meat Industry face during its growth?

- Intensifying public and regulatory scrutiny over the health and nutritional aspects of processed products presents a formidable challenge to industry growth.

- The industry faces significant challenges from intensifying competition and regulatory pressures. The rise of plant-based meat alternatives and blended meat-plant products is capturing market share, with alternative protein sales growing at twice the rate of traditional meat. This necessitates innovation in frozen meat product innovations and refrigerated meat packaging.

- Internally, processors are implementing stringent fat content reduction strategies and developing phosphate-free meat binders to meet health demands. Ensuring safety requires robust pathogen reduction interventions and comprehensive food safety HACCP plan implementation. Advanced technologies like x-ray inspection systems and metal detection in processing are now standard for mitigating contamination risks from foreign objects.

- The traditional use of sodium nitrite preservation is under scrutiny, pushing firms to explore alternatives for both fresh and shelf-stable meat products and monitor for microbial spoilage indicators to avoid recalls.

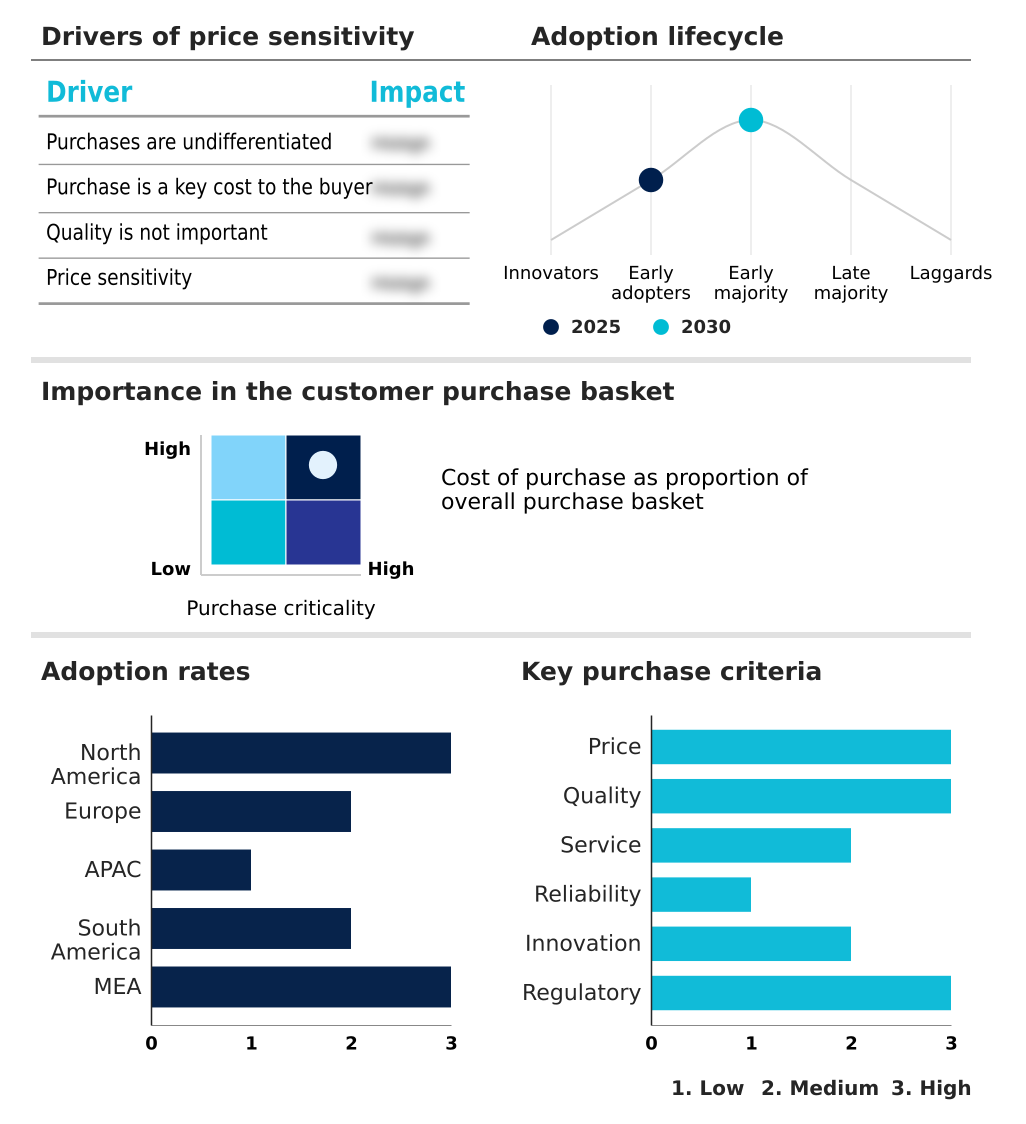

Exclusive Technavio Analysis on Customer Landscape

The processed red meat market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the processed red meat market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Processed Red Meat Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, processed red meat market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

American Foods Group LLC - Offerings include a range of beef and pork products, focusing on beef processing and value-added meat solutions for diverse market applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- American Foods Group LLC

- BRF SA

- Cargill Inc.

- Cherkizovo Group

- Clemens Food Group

- Cremonini SpA

- Danish Crown AS

- Dawn Farm Foods Ltd.

- Foyle Food Group Ltd.

- Hormel Foods Corp.

- Itoham Yonekyu Holdings Inc.

- JBS SA

- Maple Leaf Foods Inc.

- Marfrig Global Foods SA

- Minerva Foods SA

- NH Foods Ltd.

- OSI Group LLC

- Sunbulah Group

- Sysco Corp.

- Tyson Foods Inc.

- WH Group Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Processed red meat market

- In January, 2025, JBS SA expanded its portfolio by acquiring a 50 percent stake in South America's largest egg producer, Mantiqueira Brasil, signaling a strategic diversification into new protein segments.

- In February, 2025, JBS USA announced a $200 million investment to upgrade its beef production facilities in Texas and Colorado, aiming to enhance operational efficiency and increase output.

- In March, 2025, JBS SA allocated $100 million to establish two new meat processing plants in Vietnam, a strategic expansion to address the increasing demand for processed meat in Southeast Asia.

- In May, 2025, MBRF Global Foods, the entity formed by the merger of Marfrig and BRF, completed a major capacity expansion across its South American facilities to boost processed beef production for export.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Processed Red Meat Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 329 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.1% |

| Market growth 2026-2030 | USD 147.7 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.9% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, Russia, China, Japan, Australia, Indonesia, South Korea, India, Brazil, Argentina, Colombia, Saudi Arabia, South Africa, UAE, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The processed red meat market is navigating a complex transition, balancing high-volume production with demands for premium, healthier products. Key operational shifts include the adoption of robotic processing automation and advanced x-ray inspection systems to enhance safety and efficiency.

- A central focus is on product reformulation, involving fat content reduction strategies and the development of phosphate-free meat binders to create clean label meat formulation. Firms are utilizing natural preservative systems and celery powder curing agent for nitrate-free processing, moving away from traditional sodium nitrite preservation. This requires precise dry-curing process control and advancements in smoke generation technology.

- The entire supply chain is under review, from ensuring animal welfare certification standards to implementing robust food safety HACCP plan. Companies that have integrated comprehensive livestock traceability systems report a 30% reduction in time-to-traceability during mock recalls. This focus on transparency and quality, involving everything from meat batter stability to pathogen reduction interventions, defines the competitive landscape.

- Success depends on mastering curing and smoking methods, optimizing water-holding capacity, and leveraging technologies like high-pressure processing and modified atmosphere packaging for shelf-life extension technologies. The industry is also refining meat grinding and emulsification processes and using sensory evaluation panels to perfect meat-based flavor profiles.

What are the Key Data Covered in this Processed Red Meat Market Research and Growth Report?

-

What is the expected growth of the Processed Red Meat Market between 2026 and 2030?

-

USD 147.7 billion, at a CAGR of 5.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Processed pork, Processed beef, Processed lamb, and Others), Type (Deli meats, Sausages, Bacon, and Others), Distribution Channel (Supermarkets and hypermarkets, Butcher shops, Convenience stores, and Online retail), Form Factor (Refrigerated, Frozen, and Canned) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Surging demand for convenience and ready-to-eat food products, Intensifying public and regulatory scrutiny over health and nutrition

-

-

Who are the major players in the Processed Red Meat Market?

-

American Foods Group LLC, BRF SA, Cargill Inc., Cherkizovo Group, Clemens Food Group, Cremonini SpA, Danish Crown AS, Dawn Farm Foods Ltd., Foyle Food Group Ltd., Hormel Foods Corp., Itoham Yonekyu Holdings Inc., JBS SA, Maple Leaf Foods Inc., Marfrig Global Foods SA, Minerva Foods SA, NH Foods Ltd., OSI Group LLC, Sunbulah Group, Sysco Corp., Tyson Foods Inc. and WH Group Ltd.

-

Market Research Insights

- The market's dynamics are shaped by a push for both convenience and higher quality. The demand for ready-to-eat protein solutions and convenience meal components is expanding, with direct-to-consumer meat delivery models growing twice as fast as traditional retail channels.

- This is met with a concurrent trend toward premium artisanal offerings and gourmet charcuterie products, where attributes like ethically sourced livestock justify higher price points. Manufacturers are innovating with global cuisine flavor profiles and value-added meat preparations to capture consumer interest.

- For example, firms that have adopted reduced sodium formulations have seen a 15% increase in repeat purchases from health-conscious consumers. Meanwhile, the expansion of private label meat programs by major retailers is intensifying competition, often prioritizing cost-efficiency over premium attributes, leading to a bifurcated market strategy for many producers.

We can help! Our analysts can customize this processed red meat market research report to meet your requirements.

RIA -

RIA -