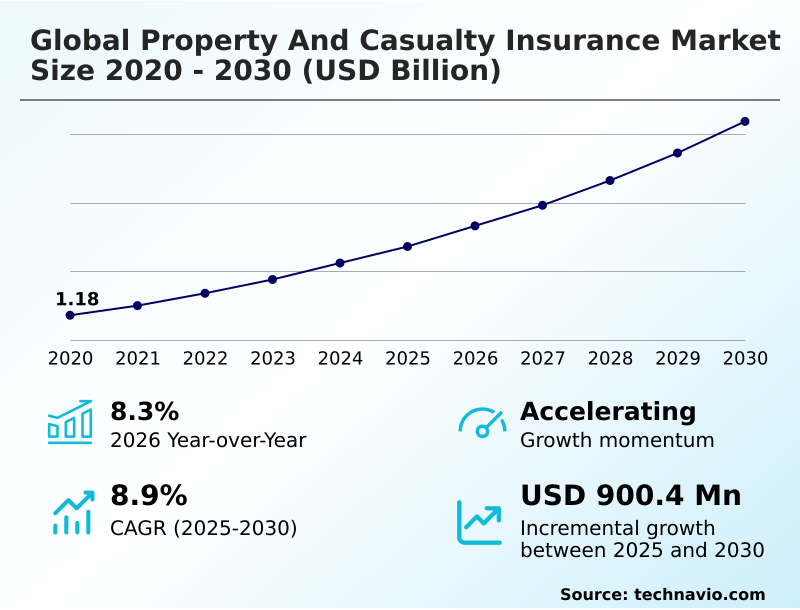

Property And Casualty Insurance Market Size 2026-2030

The property and casualty insurance market size is valued to increase by USD 900.4 million, at a CAGR of 8.9% from 2025 to 2030. Implementation of intelligent insurance and agentic artificial intelligence integration will drive the property and casualty insurance market.

Major Market Trends & Insights

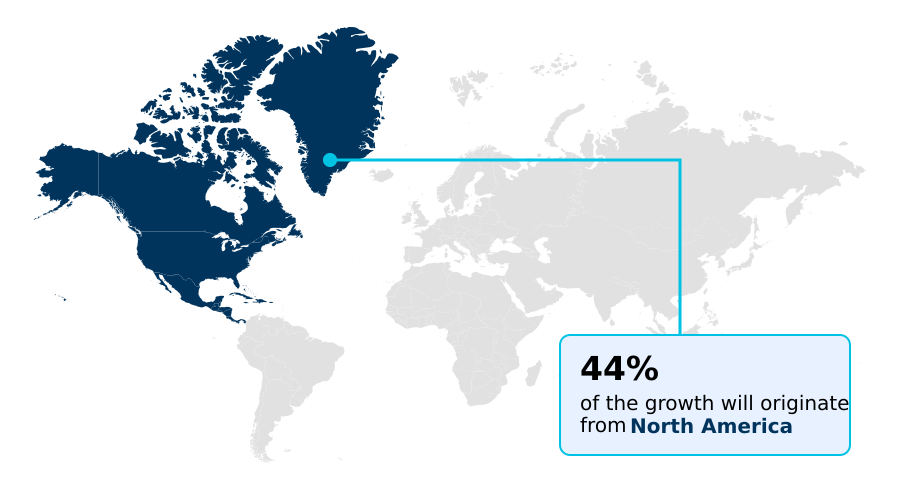

- North America dominated the market and accounted for a 43.7% growth during the forecast period.

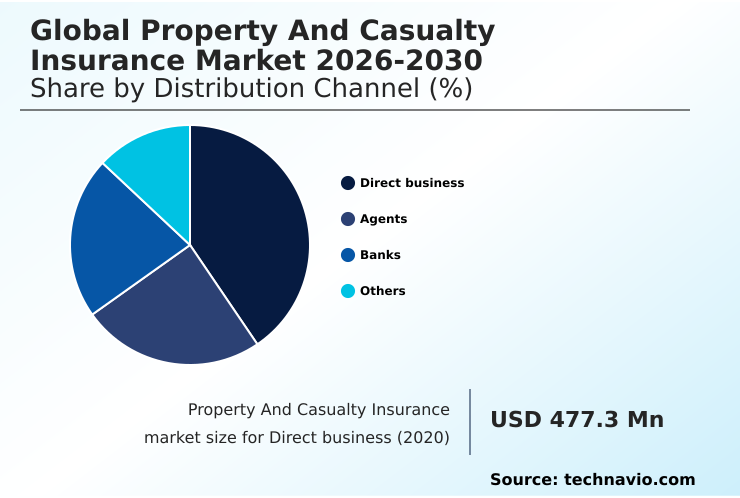

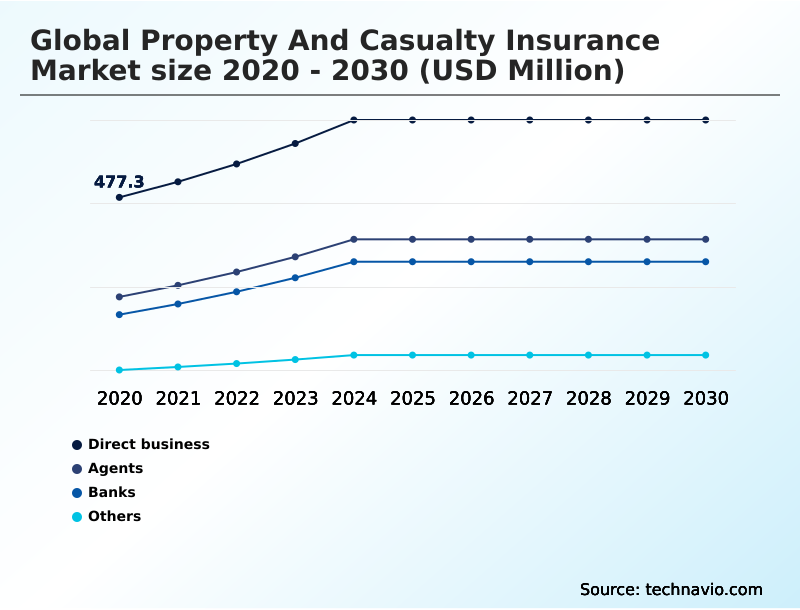

- By Distribution Channel - Direct business segment was valued at USD 622.5 million in 2024

- By Product Type - Fire insurance segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.41 billion

- Market Future Opportunities: USD 900.4 million

- CAGR from 2025 to 2030 : 8.9%

Market Summary

- The property and casualty insurance market is undergoing a significant transformation, driven by technological integration and shifting risk landscapes. Insurers are moving from traditional indemnity-based policies toward dynamic models incorporating real-time data for precision underwriting. A key trend is the growth of parametric insurance, where automated payouts are triggered by predefined environmental indices, bypassing lengthy claims processing.

- For instance, an agricultural enterprise can secure coverage that pays out automatically when satellite data confirms a drought, ensuring immediate liquidity. This shift is enabled by agentic artificial intelligence and advanced catastrophe modeling, which allows for more accurate risk-pooling mechanism design.

- However, the industry faces challenges from social inflation and the rise of deepfake-enabled fraud, which complicate actuarial modeling and increase loss-adjustment expenses. Simultaneously, embedded distribution models that integrate insurance into third-party platforms are creating frictionless customer journeys, expanding market reach and redefining policyholder engagement through seamless ecosystem integration.

What will be the Size of the Property And Casualty Insurance Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Property And Casualty Insurance Market Segmented?

The property and casualty insurance industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Direct business

- Agents

- Banks

- Others

- Product type

- Fire insurance

- Motor insurance

- Marine insurance

- Aviation insurance

- Others

- Type

- Short-term policies

- Long-term policies

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- South Korea

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- North America

By Distribution Channel Insights

The direct business segment is estimated to witness significant growth during the forecast period.

The direct business segment is evolving beyond simple direct-to-consumer (D2C) channels into a sophisticated intelligent insurance operating model. Carriers leverage API-first products and insurtech partnerships for seamless embedded distribution within non-insurance digital ecosystems, creating a frictionless customer journey.

This approach, supported by advanced actuarial modeling and customer relationship management (CRM) tools, enables a level of precision underwriting previously unattainable. Through API-driven distribution and open insurance initiatives, insurers are also enhancing bancassurance models to target high-net-worth individuals more effectively.

The focus is on automating workflows, with automated claims processing improving efficiency by over 25% for standard personal line claims, thereby strengthening the direct-to-policyholder relationship without intermediaries.

The Direct business segment was valued at USD 622.5 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 43.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Property And Casualty Insurance Market Demand is Rising in North America Get Free Sample

The geographic landscape is marked by distinct regional dynamics, with North America leading in the adoption of advanced litigation analytics to counter social inflation.

In APAC, rapid urbanization and regulatory support for open insurance initiatives are driving growth, with a focus on sharia-compliant insurance products in markets like Indonesia.

European insurers, guided by the Digital Operational Resilience Act (DORA), are focused on enhancing cyber-physical resilience and integrating ESG metrics. Bancassurance models remain a key distribution channel in Europe and Latin America.

Across regions, there's a rise in specialized commercial lines to cover risks like business interruption, with some carriers leveraging digital twin technology for complex asset underwriting.

This regional specialization, combined with global trends like unmanned aerial vehicles (UAVs) insurance, is creating diverse opportunities, with top-quartile firms in APAC achieving a net combined ratio that is 5% better than regional averages.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the sector are increasingly shaped by the impact of social inflation on casualty insurance lines, forcing a re-evaluation of long-tail liability risks. To maintain profitability, carriers are focusing on how to optimize the P&C net combined ratio with AI, using machine learning for AI-driven precision underwriting in property insurance.

- This involves sophisticated actuarial modeling for long-tail liability risks to price coverage for unpredictable litigation more accurately. The rise of usage-based motor insurance premium calculation models, powered by telematics, exemplifies the shift toward personalized pricing. In commercial fleet risk management, the role of telematics is crucial for monitoring driver behavior and reducing claims.

- For catastrophic events, reinsurance strategies for managing secondary perils are being revamped, while parametric insurance solutions for natural catastrophes offer faster payouts. At the corporate level, alternative risk transfer structures for corporate self-insurance are gaining traction. Operationally, digital transformation of automated claims processing is a priority, alongside advanced methods for detecting fraud in claims using litigation analytics.

- The market structure is also evolving, with managing general underwriter models for specialty lines and embedded insurance integration in automotive OEM sales becoming more common. These shifts occur within a framework of strict solvency mandates and capital adequacy requirements, ensuring stability.

What are the key market drivers leading to the rise in the adoption of Property And Casualty Insurance Industry?

- A key market driver is the implementation of intelligent insurance models, which integrate agentic artificial intelligence to automate complex decision-making processes.

- Core market drivers are centered on the industrialization of data and intelligence. The implementation of agentic artificial intelligence within a cloud-native architecture is enabling a new intelligent insurance operating model, with some carriers reporting a 30% gain in operational efficiency.

- This is complemented by the widespread adoption of telematics and usage-based insurance (UBI), which leverage real-time behavioral data from sources like advanced driver-assistance systems (ADAS) to personalize premiums, reducing claims frequency by up to 25%.

- Furthermore, as market volatility persists, large enterprises are turning to alternative risk transfer (ART) structures, including captive insurance companies and multi-year casualty programs.

- These loss-sensitive mechanisms, often managed by a managing general agent (MGA), provide greater control over long-tail liabilities and offer stability against unpredictable reinsurance pricing.

What are the market trends shaping the Property And Casualty Insurance Industry?

- The market is shaped by the expansion of parametric insurance solutions, which are increasingly coupled with real-time climate data for proactive risk orchestration.

- Market trends are coalescing around data-driven, automated risk management. The growth of parametric insurance, which abandons traditional indemnity-based policies for payouts based on predefined environmental indices, has reduced loss-adjustment expenses by up to 40% in certain catastrophe scenarios. This is enabled by real-time risk orchestration using satellite telemetry and climate data.

- Concurrently, the industry is combatting the effects of social inflation with advanced litigation analytics. These tools analyze regional juror sentiment and historical court data, improving the accuracy of claims triage processes by 15%. This allows carriers to more effectively manage nuclear verdicts fueled by third-party litigation financing.

- These trends, supported by sophisticated catastrophe modeling and the use of structured risk solutions, are reshaping how insurers price risk and interact with policyholders.

What challenges does the Property And Casualty Insurance Industry face during its growth?

- A primary challenge for the industry is the rise of systemic cyber-physical vulnerabilities, compounded by the escalation of sophisticated, deepfake-enabled fraud.

- The industry is confronting a triad of systemic challenges that test traditional risk-pooling mechanisms. The escalation of cyber-physical threats, particularly deepfake-enabled fraud targeting claims, has forced insurers to invest in advanced biometric and cryptographic tools, increasing compliance costs associated with principle-based regulations by an estimated 10-15%.

- Concurrently, social inflation continues to pressure the net combined ratio on liability lines, with nuclear verdicts making actuarial modeling for long-tail risks exceedingly difficult. Climate volatility presents the third major hurdle, as the rising frequency of secondary perils strains reinsurance capacity and forces a reliance on state-backed insurers in high-risk zones.

- This has led to a recalibration of property-catastrophe reinsurance strategies and a greater emphasis on catastrophe bonds to manage exposures within tightening solvency mandates.

Exclusive Technavio Analysis on Customer Landscape

The property and casualty insurance market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the property and casualty insurance market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Property And Casualty Insurance Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, property and casualty insurance market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Allianz SE - Delivers property and casualty insurance, including commercial liability and motor coverage, backed by extensive global risk management and digital platform support.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Allianz SE

- American International Group

- AXA Group

- BHHC

- Chubb Ltd.

- CNA Financial Corp.

- ICICI Lombard Insurance Co.

- Liberty Mutual Holding Co. Inc.

- Munich Reinsurance Co.

- Nationwide Mutual Insurance Co.

- Sompo Holdings Inc.

- State Farm Insurance Co.

- Swiss Re Ltd.

- The Allstate Corp.

- The Progressive Corp.

- The Travelers Co. Inc.

- Tokio Marine Holdings Inc.

- Universal Insurance Holdings

- USAA

- Zurich Insurance Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Property and casualty insurance market

- In March 2025, digital financial services platform PhonePe launched a comprehensive suite of vehicle insurance products, enabling users to compare and purchase policies directly within its application environment.

- In January 2025, Allianz SE announced a global partnership with Anthropic to accelerate the integration of responsible artificial intelligence into its insurance operations, automating complex claims processing and enhancing underwriting speed.

- In November 2024, Chubb Limited reported record full-year net income, driven by a record-low property and casualty combined ratio, highlighting a trend where operational excellence is a primary driver of profitability.

- In February 2025, the Indian Department for Promotion of Industry and Internal Trade formally liberalized the national insurance sector, permitting up to 100% foreign direct investment to attract global capital and technical expertise.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Property And Casualty Insurance Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 308 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.9% |

| Market growth 2026-2030 | USD 900.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.3% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, South Korea, India, Australia, Indonesia, Brazil, Argentina, Colombia, South Africa, Saudi Arabia, UAE, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is rapidly transitioning toward a model where technological proficiency dictates leadership. The integration of agentic artificial intelligence and telematics is no longer optional, enabling advanced usage-based insurance (UBI) models and real-time risk orchestration. This shift is critical for managing emerging challenges like deepfake-enabled fraud and systemic cyber-physical threats.

- Insurers are leveraging cloud-native architecture to deploy API-first products for embedded distribution, moving beyond traditional bancassurance models. In parallel, the industry is grappling with social inflation, using advanced litigation analytics to refine precision underwriting. The adoption of alternative risk transfer (ART) and captive insurance companies reflects a strategic move to manage volatility from secondary perils.

- This tech-driven evolution is validated by performance metrics, as firms implementing automated claims processing have achieved a 30% reduction in processing time. This operational gain directly informs boardroom budgeting for digital transformation, as it proves the ROI on investments in platforms that support sophisticated catastrophe modeling, actuarial modeling, and reinsurance capacity management.

What are the Key Data Covered in this Property And Casualty Insurance Market Research and Growth Report?

-

What is the expected growth of the Property And Casualty Insurance Market between 2026 and 2030?

-

USD 900.4 million, at a CAGR of 8.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Direct business, Agents, Banks, and Others), Product Type (Fire insurance, Motor insurance, Marine insurance, Aviation insurance, and Others), Type (Short-term policies, and Long-term policies) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Implementation of intelligent insurance and agentic artificial intelligence integration, Systemic cyber-physical vulnerabilities and escalation of deepfake-enabled fraud

-

-

Who are the major players in the Property And Casualty Insurance Market?

-

Allianz SE, American International Group, AXA Group, BHHC, Chubb Ltd., CNA Financial Corp., ICICI Lombard Insurance Co., Liberty Mutual Holding Co. Inc., Munich Reinsurance Co., Nationwide Mutual Insurance Co., Sompo Holdings Inc., State Farm Insurance Co., Swiss Re Ltd., The Allstate Corp., The Progressive Corp., The Travelers Co. Inc., Tokio Marine Holdings Inc., Universal Insurance Holdings, USAA and Zurich Insurance Co. Ltd.

-

Market Research Insights

- The market is defined by a rapid pivot toward an intelligent insurance operating model, where technology drives competitive advantage. The integration of high-fidelity predictive analytics and generative AI in claims has enabled leading firms to reduce claims frequency by up to 25% through proactive risk mitigation.

- This shift is supported by frictionless ecosystem integration and the growth of insurtech partnerships, creating direct-to-consumer (D2C) channels that offer a frictionless customer journey. As carriers adopt structured risk solutions and catastrophe bonds to manage volatility, they are also leveraging real-time climate data to refine underwriting.

- The industrialization of telematics allows for hyper-personalized policies, contributing to operational efficiency gains of up to 30% in automated workflows, fundamentally reshaping the relationship between insurers and policyholders.

We can help! Our analysts can customize this property and casualty insurance market research report to meet your requirements.

RIA -

RIA -