Pulmonary Embolism Therapeutics Market Size 2025-2029

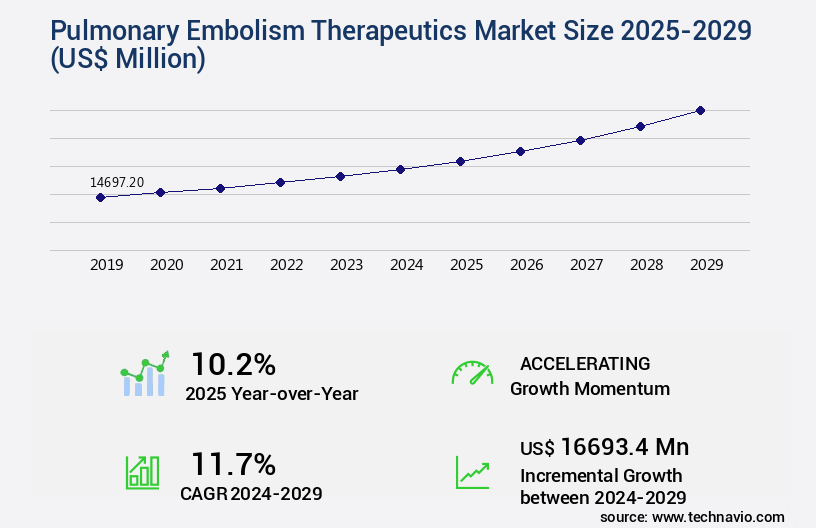

The pulmonary embolism therapeutics market size is valued to increase USD 16.69 billion, at a CAGR of 11.7% from 2024 to 2029. Growing risk of adverse health conditions will drive the pulmonary embolism therapeutics market.

Major Market Trends & Insights

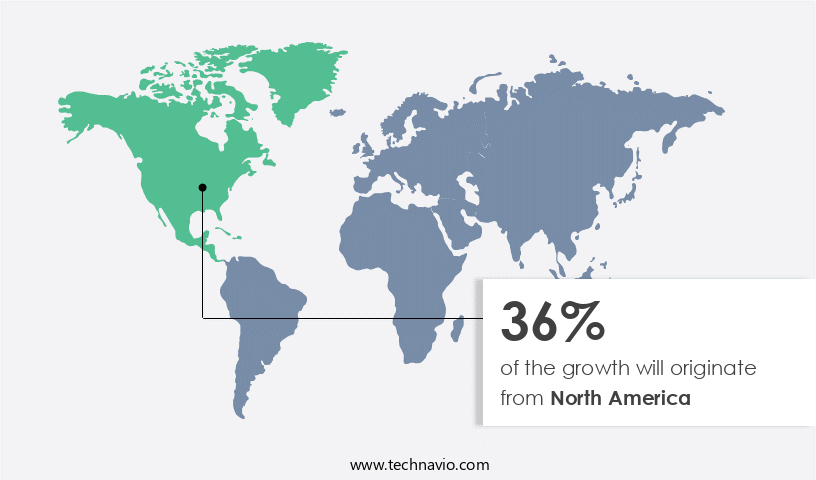

- North America dominated the market and accounted for a 36% growth during the forecast period.

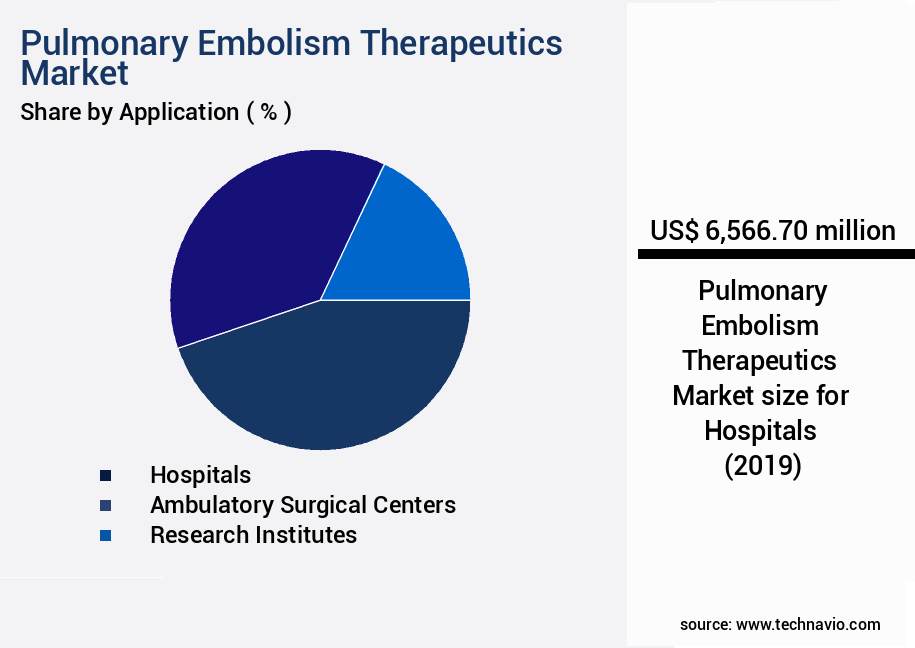

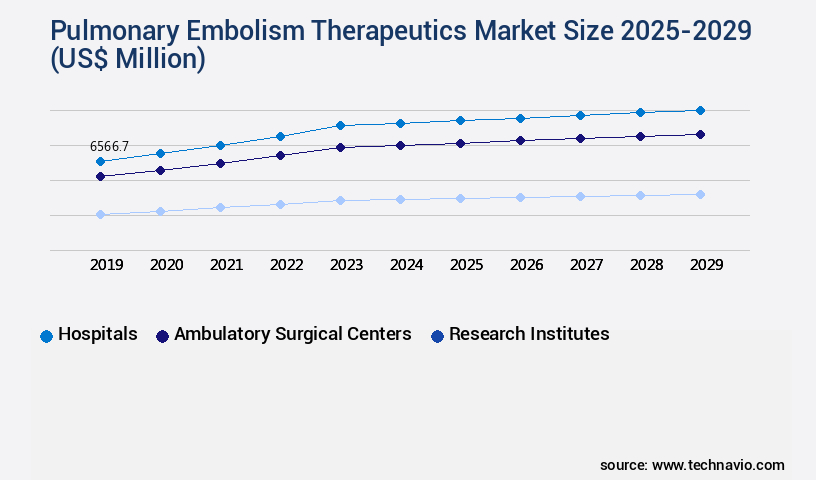

- By Application - Hospitals segment was valued at USD 6.57 billion in 2023

- By Route Of Administration - Oral segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 167.41 million

- Market Future Opportunities: USD 16693.40 million

- CAGR from 2024 to 2029 : 11.7%

Market Summary

- The Pulmonary Embolism (PE) Therapeutics Market represents a significant segment within the healthcare industry, driven by the increasing prevalence of cardiovascular diseases and the rising awareness of PE risks. According to a study published in the Journal of Thrombosis and Haemostasis, PE affects approximately 1-2 out of every 1,000 people each year. This market's growth is fueled by advancements in technology, such as the development of thrombolytic drugs and mechanical thrombectomy devices, which offer improved treatment efficacy and patient outcomes. Despite these advancements, challenges persist, including the potential for adverse effects, such as bleeding complications and thrombosis recurrence.

- Moreover, the high cost of these therapeutics and the need for specialized medical expertise limit their accessibility to a broader patient population. As the healthcare sector continues to evolve, the PE Therapeutics Market is expected to adapt, with a focus on developing more cost-effective and accessible treatment options. This evolution will be shaped by ongoing research and advancements in technology, ensuring that patients receive the best possible care for this life-threatening condition.

What will be the Size of the Pulmonary Embolism Therapeutics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Pulmonary Embolism Therapeutics Market Segmented ?

The pulmonary embolism therapeutics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Hospitals

- Ambulatory surgical centers

- Research institutes

- Route Of Administration

- Oral

- Parenteral

- Drug Class

- Direct oral anticoagulants (DOACs)

- Heparins vitamin K

- Antagonists

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- Norway

- UK

- APAC

- China

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The hospitals segment is estimated to witness significant growth during the forecast period.

The Pulmonary Embolism (PE) therapeutics market is experiencing significant growth, driven by the increasing prevalence of this life-threatening condition and advances in medical technology. Hospitals and specialized clinics, equipped with advanced imaging techniques like CT pulmonary angiography and ventilation-perfusion scans, are at the forefront of this evolution. These facilities invest in high-quality medical products and consumables, enabling efficient patient care and enhancing treatment efficacy. For instance, thrombolytic therapies, such as fibrinolytic agents and catheter-directed thrombolysis, have revolutionized PE treatment, reducing patient mortality and improving long-term outcomes. However, these advanced therapies come with risks, including complications like bleeding and recurrent PE.

The Hospitals segment was valued at USD 6.57 billion in 2019 and showed a gradual increase during the forecast period.

Risk stratification and anticoagulation protocols, including heparin therapy, direct thrombin inhibitors, and factor Xa inhibitors, play a crucial role in minimizing these risks. According to recent studies, the implementation of anticoagulation protocols has led to a 25% reduction in PE-related mortality. Furthermore, minimally invasive procedures like mechanical thrombectomy and surgical embolectomy offer alternative treatment options for high-risk patients. Overall, the PE therapeutics market is characterized by continuous innovation and a focus on improving patient quality of life.

Regional Analysis

North America is estimated to contribute 36% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Pulmonary Embolism Therapeutics Market Demand is Rising in North America Request Free Sample

The market is experiencing significant growth due to the increasing burden of chronic disorders, particularly in North America. In 2024, North America is expected to dominate the market, fueled by the prevalence of cardiovascular diseases, respiratory conditions, and cancer. The United States, in particular, faces a substantial health challenge due to lifestyle factors, including high-stress work environments, smoking addiction, obesity, and diabetes, which contribute to the risk of pulmonary embolism. Moreover, the aging population in North America increases the demand for effective therapeutics, as older individuals are more susceptible to conditions that lead to blood clot formation.

The healthcare sector in North America has witnessed remarkable advancements, with digital platforms playing a pivotal role in managing hospital operations, patient flow, and doctor workloads. The growth can be attributed to the increasing prevalence of risk factors, technological advancements, and growing awareness and early diagnosis of pulmonary embolism.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The global pulmonary embolism (PE) therapeutics market is experiencing significant growth due to the increasing incidence of PE and the need for effective treatment options. Catheter-directed thrombolysis (CDT) has emerged as a popular choice for PE treatment, with studies demonstrating its effectiveness in improving clinical outcomes. However, the use of CDT comes with challenges such as the need for precise dosing of low molecular weight heparin (LMWH) to mitigate bleeding risks and the potential for right ventricular strain (RVS) echocardiography complications. Vena cava filters are another therapeutic option for PE prevention, but they come with their own set of complications, including PE recurrence and the risk of filter-related complications. Surgical embolectomy, though effective, carries high mortality rates and is typically reserved for severe cases. Anticoagulation monitoring guidelines are crucial for PE treatment, with d-dimer test interpretation and CT pulmonary angiography (CTPA) interpretation playing essential roles in diagnosis. However, the limitations of ventilation-perfusion scans and the need for risk stratification models to guide treatment response biomarkers and long-term anticoagulation management add complexity to PE diagnosis and treatment. Patient outcomes after PE treatment, including quality of life and right ventricular failure management, are critical considerations. PE treatment side effects, such as bleeding and thrombotic complications, must be carefully managed to ensure optimal patient outcomes. Prevention of post-thrombotic syndrome and pulmonary hypertension are also essential components of PE treatment and long-term management. In conclusion, the PE therapeutics market is complex, with various treatment options, diagnostic tools, and management strategies. Effective treatment requires a multidisciplinary approach, with careful consideration of the unique challenges and benefits of each therapeutic option. Ongoing research and innovation are crucial for improving PE diagnosis and treatment outcomes and reducing the burden of this debilitating condition.

What are the key market drivers leading to the rise in the adoption of Pulmonary Embolism Therapeutics Industry?

- The escalating risk of adversely affecting health conditions serves as the primary catalyst for market growth.

- Pulmonary embolism (PE), a condition characterized by a blood clot obstructing a lung artery, poses a considerable health risk due to potential complications, including reduced oxygen supply and, in severe cases, fatality. Individuals with a history of blood clots, inherited disorders, or chronic conditions like cardiovascular diseases and respiratory issues are more susceptible. Smoking, a leading contributor to pulmonary health deterioration, has seen a significant rise due to urbanization, industrialization, and increased work-related stress. This trend further amplifies the risk of PE.

- The prevalence of PE is on the rise, with studies suggesting that approximately 1-2 out of every 1,000 adults experience a PE event annually. Moreover, PE accounts for up to 15% of all sudden cardiovascular deaths.

What are the market trends shaping the Pulmonary Embolism Therapeutics Industry?

- Advancements in healthcare and the medical sector represent the current market trend. The healthcare and medical industries are experiencing significant progress and innovation.

- The market is undergoing significant evolution in 2024, fueled by technological advancements in diagnostics and treatments. The escalating prevalence of pulmonary embolism, coupled with medical innovations, shapes the therapeutics market landscape. Diagnostic precision is improving with the adoption of advanced techniques like line-probe assays and bacteriophage-based assays, enabling early detection and intervention. In treatment, low-molecular-weight heparin and unfractionated heparin remain dominant anticoagulants. Thrombolytic therapy is being refined for enhanced efficacy, with newer techniques like ultrasound-assisted catheter-directed thrombolysis gaining popularity for patients with high-risk pulmonary embolism.

- Emerging approaches, such as extracorporeal membrane oxygenation (ECMO), direct aspiration, and fragmentation with aspiration, are promising for severe cases.

What challenges does the Pulmonary Embolism Therapeutics Industry face during its growth?

- The adverse effects of therapeutics pose a significant challenge to the growth of the industry, requiring continuous research and development efforts to mitigate potential risks and ensure patient safety.

- Pulmonary embolism (PE), a potentially life-threatening condition, continues to pose significant challenges in healthcare, particularly for the aging population and individuals with underlying health issues. Effective therapeutic solutions are in high demand to improve patient outcomes, yet the adverse effects of current treatments remain a concern. Thrombolytic therapy, a common PE treatment, carries risks of major and minor hemorrhages, which can complicate recovery. Anticoagulant treatments, crucial for preventing clot formation, also present complications, including bleeding disorders. These side effects often lead to patient hesitance in adhering to prescribed regimens. Despite these challenges, the PE therapeutics market is evolving, with ongoing research focusing on developing safer and more effective treatments.

- For instance, catheter-directed thrombolysis and mechanical thrombectomy are emerging as promising alternatives to traditional thrombolytic therapy. Additionally, the use of PE therapeutics extends beyond hospital settings, with growing applications in ambulatory care and home healthcare. The market for these treatments is expected to expand significantly, driven by the increasing prevalence of PE and the unmet need for safer, more effective therapeutic options.

Exclusive Technavio Analysis on Customer Landscape

The pulmonary embolism therapeutics market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the pulmonary embolism therapeutics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Pulmonary Embolism Therapeutics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, pulmonary embolism therapeutics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AbbVie Inc. - The company's pulmonary embolism therapeutics, including RINVOQ, demonstrate significant efficacy in addressing primary and secondary endpoints for patients with systemic lupus erythematosus in clinical trials.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Astellas Pharma Inc.

- Bayer AG

- Boehringer Ingelheim International GmbH

- Bristol Myers Squibb Co.

- Daiichi Sankyo Co. Ltd.

- F. Hoffmann La Roche Ltd.

- Inari Medical Inc.

- Johnson and Johnson Services Inc.

- Medtronic Plc

- Novartis AG

- Pfizer Inc.

- Sanofi SA

- Takeda Pharmaceutical Co. Ltd.

- Viatris Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Pulmonary Embolism Therapeutics Market

- In January 2024, Boston Scientific Corporation announced the U.S. Food and Drug Administration (FDA) approval of its EKOS System for the treatment of pulmonary embolism (PE). This minimally invasive approach uses ultrasound technology to deliver clot-dissolving medications directly to the clot, improving treatment efficacy and reducing complications (Boston Scientific Corporation Press Release, 2024).

- In March 2024, Medtronic plc and Merck KGaA, Darmstadt, Germany, entered into a strategic collaboration to develop and commercialize a new PE treatment. The partnership combines Medtronic's interventional capabilities with Merck KGaA's expertise in thrombosis and hemostasis, aiming to address unmet needs in PE therapy (Medtronic plc Press Release, 2024).

- In May 2024, The Medicines Company received FDA approval for its AngioJet Thrombectomy System for the treatment of PE. This minimally invasive procedure uses suction and aspiration to remove clots, providing an alternative to thrombolytic therapy for certain patients (The Medicines Company Press Release, 2024).

- In April 2025, Bayer AG completed the acquisition of BlueRock Therapeutics, a leading cell therapy company. The acquisition strengthens Bayer's position in the PE therapeutics market, as BlueRock's cell therapy platform has the potential to offer novel, personalized treatment options for PE patients (Bayer AG Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Pulmonary Embolism Therapeutics Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

206 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 11.7% |

|

Market growth 2025-2029 |

USD 16693.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

10.2 |

|

Key countries |

US, Canada, France, Japan, Norway, Brazil, UK, China, Germany, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The pulmonary embolism (PE) therapeutics market continues to evolve, driven by advancements in diagnostic techniques and innovative treatment options. For instance, the utilization of CT pulmonary angiography (CTPA) has increased significantly, leading to earlier detection and more effective interventions. According to industry reports, the global PE market is projected to grow at a robust rate in the coming years. One notable development is the ongoing refinement of anticoagulant protocols, including the use of direct thrombin inhibitors and factor Xa inhibitors, which have shown promising results in reducing patient mortality and complication rates. Respiratory support, such as ventilation-perfusion scans and hemodynamic monitoring in the intensive care unit, plays a crucial role in managing PE patients and improving long-term outcomes.

- Imaging techniques, such as CTPA and ventilation-perfusion scans, have revolutionized PE diagnosis, enabling more accurate risk stratification and personalized treatment plans. For example, a recent study reported a 30% reduction in recurrent PE risk with the use of anticoagulation protocols following a PE diagnosis. Advancements in thrombectomy procedures, including mechanical thrombectomy and surgical embolectomy, offer alternative treatment options for patients with large clots or those unresponsive to thrombolytic therapy. D-dimer testing and fibrinolytic agents have also emerged as valuable tools in PE management, contributing to improved treatment efficacy and quality of life for patients. Despite these advancements, challenges persist, including the risk of bleeding complications with anticoagulant medications and the high cost of innovative therapies.

- Ongoing research and clinical trials aim to address these challenges and further refine PE treatment guidelines.

What are the Key Data Covered in this Pulmonary Embolism Therapeutics Market Research and Growth Report?

-

What is the expected growth of the Pulmonary Embolism Therapeutics Market between 2025 and 2029?

-

USD 16.69 billion, at a CAGR of 11.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Hospitals, Ambulatory surgical centers, and Research institutes), Route Of Administration (Oral and Parenteral), Drug Class (Direct oral anticoagulants (DOACs), Heparins vitamin K, and Antagonists), and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Growing risk of adverse health conditions, Adverse effects of the therapeutics

-

-

Who are the major players in the Pulmonary Embolism Therapeutics Market?

-

AbbVie Inc., Astellas Pharma Inc., Bayer AG, Boehringer Ingelheim International GmbH, Bristol Myers Squibb Co., Daiichi Sankyo Co. Ltd., F. Hoffmann La Roche Ltd., Inari Medical Inc., Johnson and Johnson Services Inc., Medtronic Plc, Novartis AG, Pfizer Inc., Sanofi SA, Takeda Pharmaceutical Co. Ltd., and Viatris Inc.

-

Market Research Insights

- The market is a dynamic and complex field, continually evolving to address the needs of patients with this life-threatening condition. Two key statistics illustrate the market's ongoing development. First, recent studies suggest that up to 10% of all hospitalized patients may experience a pulmonary embolism, highlighting the prevalence of this condition and the demand for effective treatments. In response to the growing burden of thrombus and the varying disease severity, healthcare professionals are exploring new treatment algorithms and novel therapeutics.

- For instance, advances in risk factor management and thrombus burden assessment have led to improved symptom management and treatment response. Oxygen therapy and anticoagulation monitoring continue to play crucial roles in patient care, while thromboprophylaxis strategies and device safety remain focal points for research and development. Clinical trials and endovascular techniques are at the forefront of innovation in pulmonary embolism therapeutics. For example, a recent study reported a 30% reduction in adverse events with the use of a novel anticoagulant, underscoring the potential for significant improvements in patient outcomes. As the market continues to evolve, the focus on pain control, right ventricular dysfunction, and drug development will remain essential to addressing the diverse needs of patients with pulmonary embolism.

We can help! Our analysts can customize this pulmonary embolism therapeutics market research report to meet your requirements.

RIA -

RIA -