RAID Controller Card Market Size 2026-2030

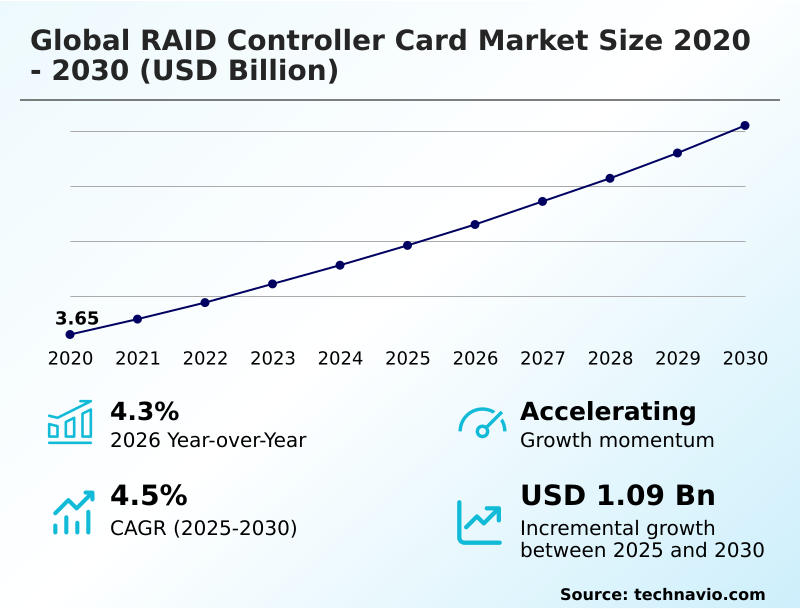

The raid controller card market size is valued to increase by USD 1.09 billion, at a CAGR of 4.5% from 2025 to 2030. Proliferation of NVMe storage will drive the raid controller card market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 38.9% growth during the forecast period.

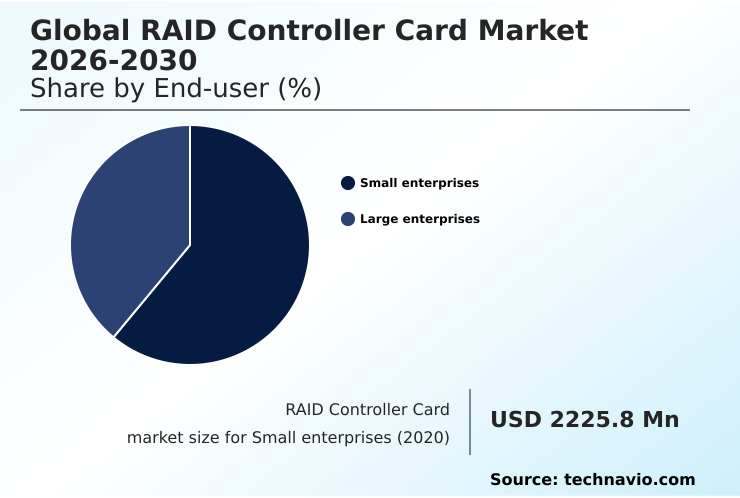

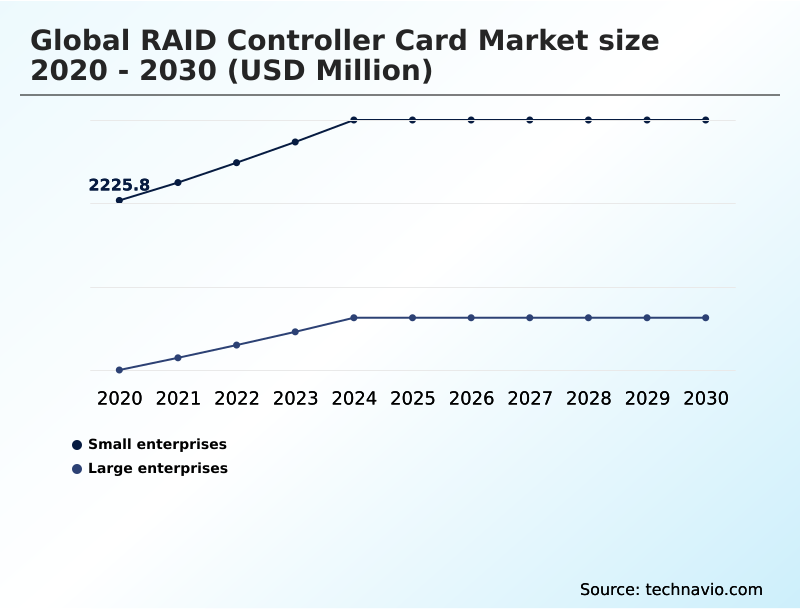

- By End-user - Small enterprises segment was valued at USD 2.61 billion in 2024

- By Product - Hardware RAID segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.90 billion

- Market Future Opportunities: USD 1.09 billion

- CAGR from 2025 to 2030 : 4.5%

Market Summary

- The RAID Controller Card Market is central to modern digital infrastructure, tasked with managing data integrity and performance as data volumes expand exponentially. The core function of a hardware RAID controller is to provide fault tolerance and accelerate storage, which remains critical even with the advent of high-speed NVMe drives.

- A key dynamic is the transition toward architectures that can eliminate storage bottlenecks in data-intensive applications like AI and machine learning. For instance, a financial services firm running real-time fraud detection analytics relies on the low latency and high IOPS of an NVMe array, managed by a powerful controller, to process transactions without delay.

- This scenario highlights the ongoing need for advanced hardware solutions. While software defined storage offers flexibility and scalability, dedicated controllers maintain an edge in mission-critical deployments where guaranteed performance and offloading RAID processing from the host CPU are paramount. The market's evolution is shaped by this balance between hardware-centric performance and software-defined agility.

What will be the Size of the RAID Controller Card Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the RAID Controller Card Market Segmented?

The raid controller card industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Small enterprises

- Large enterprises

- Product

- Hardware RAID

- Software RAID

- Application

- Data centers

- Cloud computing

- Enterprise storage

- SMEs

- Personal computers

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By End-user Insights

The small enterprises segment is estimated to witness significant growth during the forecast period.

The small enterprises segment is driven by the need for dependable data protection and improved storage performance in cost-sensitive environments.

These businesses require fault tolerance to ensure business continuity, making hardware RAID controller adoption crucial for mitigating data loss from drive failures.

A typical setup involves a RAID 1 mirror for operating system data integrity and a RAID 6 configuration for application data.

For these organizations, a dedicated RAID-on-Chip processor is essential, as it handles all parity calculations without impacting the host server's CPU.

This approach offers a significant advantage over integrated solutions, improving operational efficiency by ensuring that primary business applications are not slowed down by storage I/O bottlenecks, with some firms reporting a 15% improvement in application responsiveness.

The Small enterprises segment was valued at USD 2.61 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 38.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How RAID Controller Card Market Demand is Rising in APAC Get Free Sample

The geographic landscape is led by North America, which accounts for over 24% of the market opportunity, driven by its high concentration of hyperscale data centers requiring advanced storage virtualization and data management solutions.

APAC is the fastest-growing region, with a 5.9% growth rate, fueled by rapid digitalization and investment in new storage area networks and network attached storage.

In Europe, stringent regulations emphasize the need for robust data mirroring and data striping solutions for compliance.

Across all regions, the core need for storage performance acceleration and disaster recovery remains a constant, with direct attached storage configurations using techniques like parity generation and write-back caching with a battery backup unit being essential for RAID 0 striping and serial attached SCSI setups.

Market Dynamics

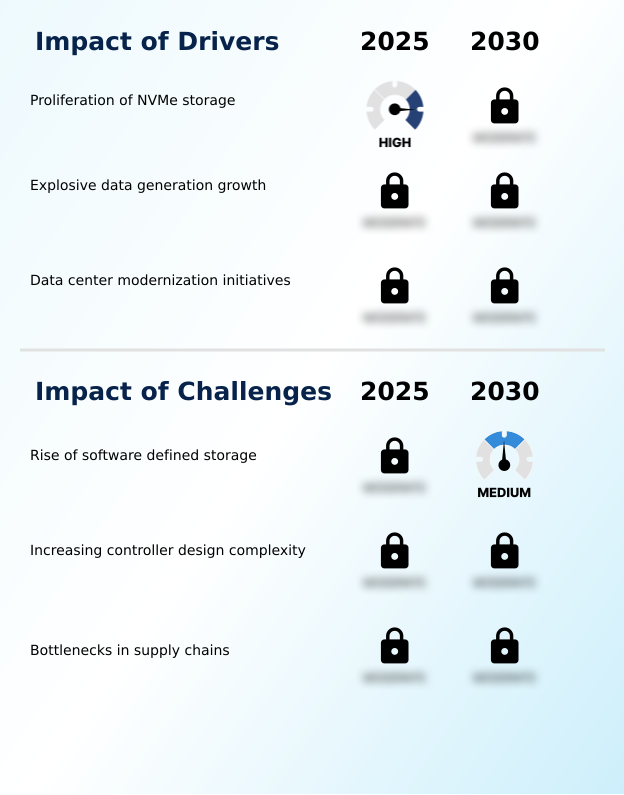

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the global raid controller card market 2026-2030 is defined by a significant architectural pivot away from legacy storage interfaces toward next-generation technologies. The transition is not merely about speed but about building a more efficient and flexible storage ecosystem.

- Tri-Mode controllers featuring robust SerDes technology have emerged as a critical bridge, allowing enterprises to manage existing SAS and SATA investments while progressively integrating high-performance NVMe drives. This future-proofs infrastructure and reduces total cost of ownership.

- Concurrently, the industry is moving toward the widespread adoption of the PCIe 5.0 standard, a necessary step to prevent the interconnect from becoming a bottleneck for arrays of ultra-fast SSDs. This shift also sets the stage for the next major trend: computational storage.

- By integrating processing capabilities directly onto the controller, these devices can offload tasks like compression and encryption, reducing host CPU load and data movement. For example, modern controllers can accelerate RAID rebuild times by more than 50% compared to previous generations, significantly minimizing the vulnerability window after a drive failure and enhancing overall data resilience.

- This transforms the controller from a simple I/O device into an active participant in the compute infrastructure, creating new value for data-intensive workloads.

What are the key market drivers leading to the rise in the adoption of RAID Controller Card Industry?

- The global RAID controller card market is being fundamentally driven by the rapid and widespread proliferation of NVMe-based solid-state storage, rooted in the demand for higher performance and lower latency.

- Key market drivers center on data center modernization and the explosive growth in data generation, which mandate scalable enterprise storage solutions.

- The proliferation of high-speed PCIe 4.0 NVMe SSD technology is compelling organizations to upgrade their storage array infrastructure to maximize I/O performance and achieve higher data availability.

- Modern PCIe 5.0 RAID controllers are instrumental in this transition, providing the necessary throughput for mission-critical applications and supporting advanced architectures like NVMe over Fabrics.

- The focus on performance is yielding tangible results, with deployments leveraging these technologies reporting over 2x improvement in input/output operations and a significant reduction in IOPS and latency, which is critical for high-performance computing.

What are the market trends shaping the RAID Controller Card Industry?

- The widespread adoption of Tri-Mode SerDes technology in next-generation controllers represents a significant and transformative market trend. This evolution in storage interface flexibility unifies connectivity for SAS, SATA, and NVMe drives from a single port.

- The market is rapidly evolving with the adoption of Tri-Mode SerDes technology, which unifies connectivity for SAS and SATA protocols and NVMe-based solid state storage within a single storage subsystem. This trend simplifies storage infrastructure and is foundational for creating a versatile tiered storage solution.

- Simultaneously, the emergence of computational storage integration is shifting processing tasks closer to data, enhancing workload optimization. The standardization of the PCIe Gen 5.0 interface is another key development, doubling bandwidth to support data-intensive workloads and prevent bottlenecks, enabling some users to achieve a 40% reduction in data transfer times for real-time data analytics and improving overall system reliability.

What challenges does the RAID Controller Card Industry face during its growth?

- The market faces a significant challenge from the rise of software-defined storage solutions, which represent a fundamental architectural shift in how storage is managed.

- A primary challenge is the increasing adoption of software defined storage, which handles data redundancy through methods like erasure coding and replication across multiple nodes, often using a simple host bus adapter instead of a full-featured controller. This architectural shift can cap the market for advanced cards in certain hyperscale environments.

- Concurrently, the increasing complexity of designing controllers with hot-swapping capability and data-at-rest encryption presents significant R&D hurdles. Supply chain volatility for components like universal flash storage and chips for advanced host controller interface creates further constraints, affecting system uptime and complicating efforts to ensure data loss prevention and data security without impacting cost structures negatively.

Exclusive Technavio Analysis on Customer Landscape

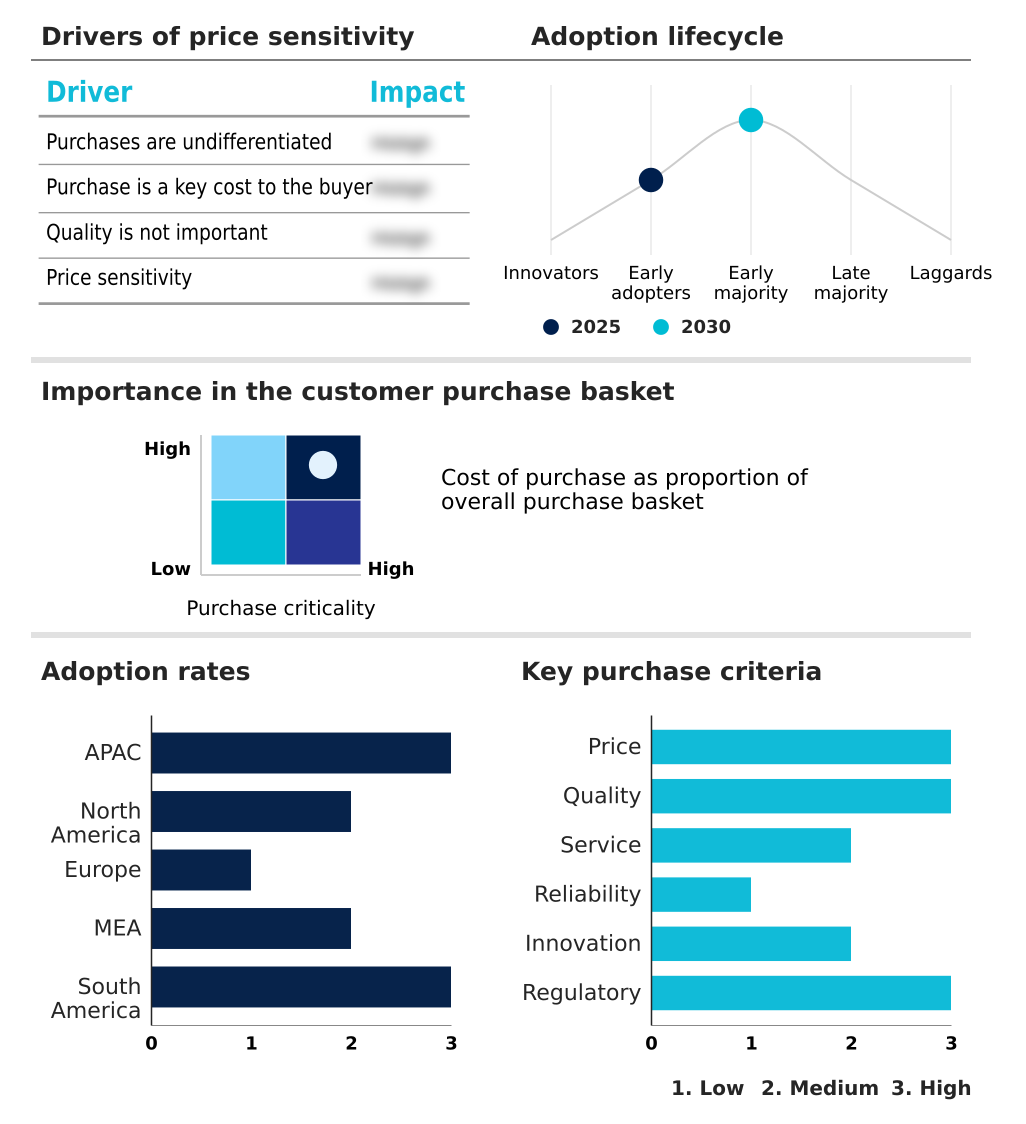

The raid controller card market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the raid controller card market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of RAID Controller Card Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, raid controller card market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced HPC Inc. - Provides specialized storage connectivity and infrastructure solutions, enabling high-performance data management and delivery for enterprise IT.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced HPC Inc.

- Advantech Co. Ltd.

- Areca Technology Corp.

- ATTO Technology Inc.

- Broadcom Inc.

- Dell Technologies Inc.

- Fujitsu Ltd.

- Hewlett Packard Enterprise Co.

- HighPoint Inc.

- Huawei Technologies Co. Ltd.

- IBM Corp.

- Intel Corp.

- Lenovo Group Ltd.

- Silicon Motion Technology Corp.

- Marvell Technology Inc.

- Microchip Technology Inc.

- NEC Corp.

- StarTech.com Ltd.

- Super Micro Computer Inc.

- Vantec Thermal Technologies Inc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Raid controller card market

- In August, 2024, Scala Data Centers initiated a partnership with Serena to source renewable energy for its hyperscale data centers in Brazil, beginning in January 2025.

- In January, 2025, CloudHQ and ESR announced a partnership to develop a $2 billion data center campus in Japan to meet the increasing demand for high-quality data capacity in the region.

- In January, 2025, Microsoft announced an ambitious plan to invest approximately $80 billion in the construction of new data centers to address the escalating demand for data processing and storage capabilities.

- In February, 2025, Brookfield Infrastructure Partners and Data4 announced a landmark investment of over $20.7 billion to develop artificial intelligence infrastructure in France, aiming to enhance the region's data infrastructure.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled RAID Controller Card Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 315 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.5% |

| Market growth 2026-2030 | USD 1091.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.3% |

| Key countries | China, India, Japan, South Korea, Singapore, Indonesia, US, Canada, Mexico, Germany, UK, France, The Netherlands, Italy, Spain, UAE, Saudi Arabia, South Africa, Israel, Egypt, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The RAID controller card market is undergoing a fundamental transformation, driven by the dual needs for extreme performance and architectural flexibility. In boardroom-level strategy discussions, the selection of a hardware RAID controller is no longer a simple procurement decision but a strategic choice impacting overall data center efficiency and readiness for future workloads.

- The industry is rapidly advancing with the adoption of the PCIe Gen 5.0 interface and the integration of Tri-Mode SerDes technology, which allows a single card to manage a heterogeneous environment of SAS and SATA protocols alongside NVMe-based solid state storage. This is crucial for creating a tiered storage solution.

- Advanced features like data striping, data mirroring, data-at-rest encryption, and support for RAID 0 striping and RAID 6 configuration are now standard. The evolution includes the emergence of computational storage integration, where the RAID-on-Chip processor, supported by a battery backup unit for its write-back caching, handles not just parity generation and parity calculations but also application-specific tasks.

- While software defined storage and simple host bus adapters using erasure coding are prevalent in some scale-out scenarios, the need for high-availability storage with guaranteed I/O performance and fault tolerance in direct attached storage, storage area networks, and network attached storage ensures continued demand.

- The latest PCIe 5.0 RAID controllers are engineered to manage PCIe 4.0 NVMe SSDs and future drives, supporting innovations like universal flash storage, hot-swapping capability, and architectures like NVMe over Fabrics, all built on standards like serial attached SCSI and the advanced host controller interface to provide robust data redundancy.

What are the Key Data Covered in this RAID Controller Card Market Research and Growth Report?

-

What is the expected growth of the RAID Controller Card Market between 2026 and 2030?

-

USD 1.09 billion, at a CAGR of 4.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Small enterprises, and Large enterprises), Product (Hardware RAID, and Software RAID), Application (Data centers, Cloud computing, Enterprise storage, SMEs, and Personal computers) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of NVMe storage, Rise of software defined storage

-

-

Who are the major players in the RAID Controller Card Market?

-

Advanced HPC Inc., Advantech Co. Ltd., Areca Technology Corp., ATTO Technology Inc., Broadcom Inc., Dell Technologies Inc., Fujitsu Ltd., Hewlett Packard Enterprise Co., HighPoint Inc., Huawei Technologies Co. Ltd., IBM Corp., Intel Corp., Lenovo Group Ltd., Silicon Motion Technology Corp., Marvell Technology Inc., Microchip Technology Inc., NEC Corp., StarTech.com Ltd., Super Micro Computer Inc. and Vantec Thermal Technologies Inc

-

Market Research Insights

- Market dynamics are increasingly shaped by the need for enhanced storage performance acceleration and workload optimization in data-intensive environments. The shift to advanced storage infrastructure is evident, with organizations that adopt all-flash NVMe storage for mission-critical applications reporting performance improvements of over 300%.

- This is coupled with a more than 50% reduction in application response times, a critical factor for maintaining system reliability and business continuity. Such gains are driving technology refresh cycles focused on eliminating storage I/O bottlenecks.

- Effective data management and robust data protection strategies are integral to this modernization, ensuring that the benefits of speed do not compromise data security or availability, thereby improving overall operational efficiency.

We can help! Our analysts can customize this raid controller card market research report to meet your requirements.

RIA -

RIA -