Solid State Drive (SSD) Market Size 2025-2029

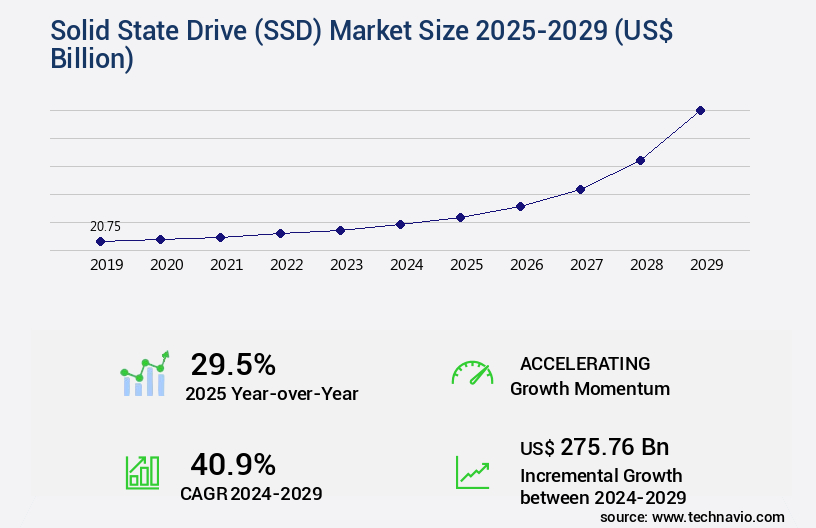

The solid state drive (ssd) market size is valued to increase USD 275.76 billion, at a CAGR of 40.9% from 2024 to 2029. Enhanced performance and durability will drive the solid state drive (ssd) market.

Major Market Trends & Insights

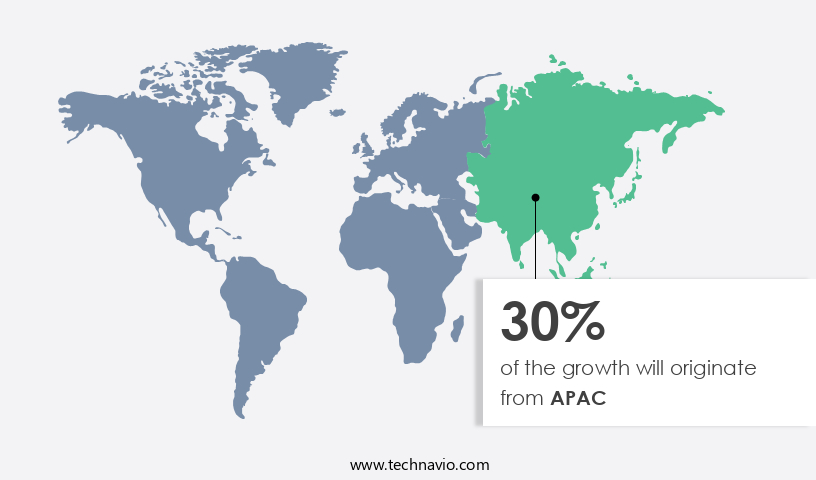

- APAC dominated the market and accounted for a 30% growth during the forecast period.

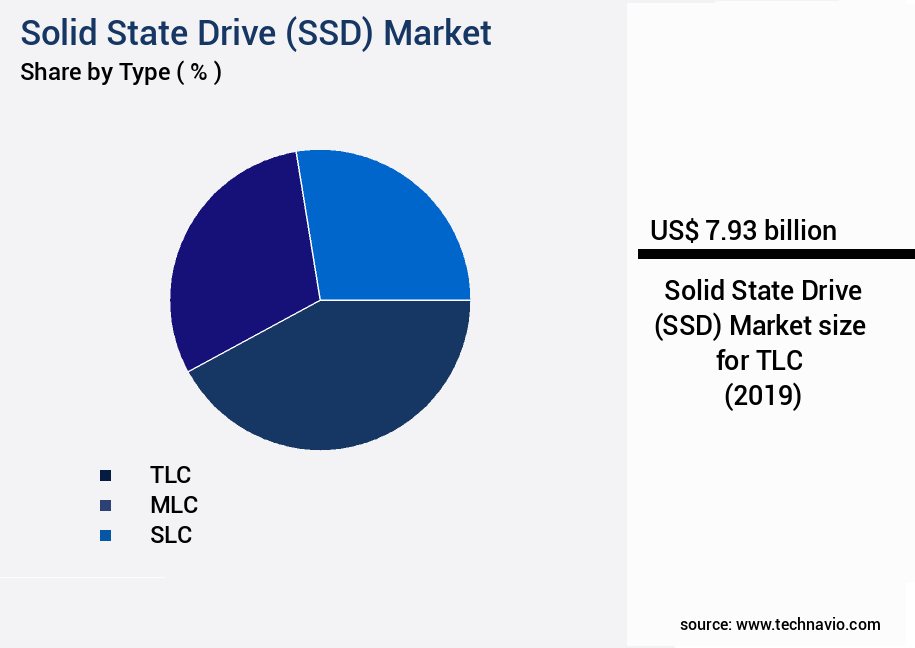

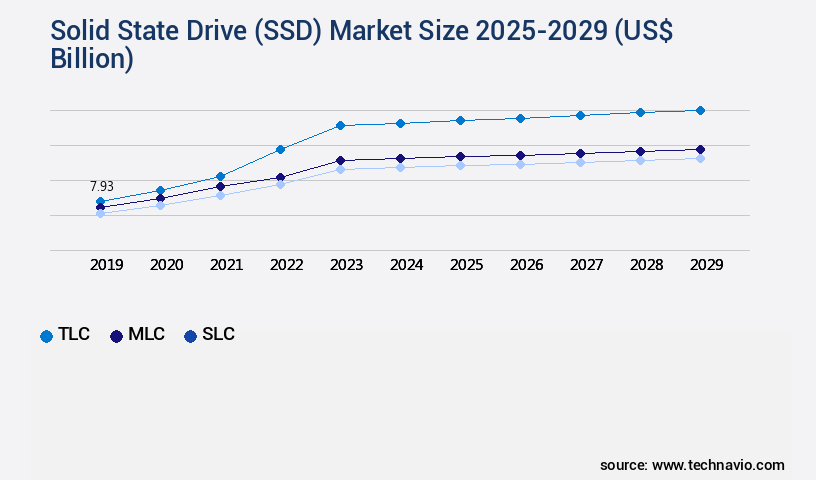

- By Type - TLC segment was valued at USD 7.93 billion in 2023

- By End-user - Laptops segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.00 billion

- Market Future Opportunities: USD 275.76 billion

- CAGR from 2024 to 2029 : 40.9%

Market Summary

- The market represents a dynamic and evolving sector in the technology industry, driven by advancements in core technologies and applications. SSDs, which offer enhanced performance and durability compared to traditional Hard Disk Drives (HDDs), have gained significant market traction. According to recent reports, SSDs accounted for over 30% of the total global hard drive market share in 2020, with this figure projected to grow further. Key drivers for the SSD Market include the emergence of portable SSDs, which cater to the increasing demand for data storage solutions that are compact, lightweight, and offer fast data transfer rates.

- Additionally, the poor latency and endurance of HDDs have made SSDs an attractive alternative for businesses and consumers alike. However, challenges such as high production costs and limited production capacity pose obstacles to market growth. Despite these challenges, opportunities abound, particularly in the data center and enterprise sectors, where the need for high-performance storage solutions is paramount.

What will be the Size of the Solid State Drive (SSD) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Solid State Drive (SSD) Market Segmented ?

The solid state drive (ssd) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- TLC

- MLC

- SLC

- End-user

- Laptops

- PCs

- Form Factor

- 2.5 Inch

- M.2

- U.2

- AIC (Add-in Card)

- Storage Capacity

- Under 250 GB

- 250 GB - 500 GB

- 500 GB - 1 TB

- 1 TB - 2 TB

- Above 2 TB

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Type Insights

The tlc segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with ongoing advancements in technology driving improvements in performance and capacity. TLC NAND flash, the most affordable form of NAND, is an emerging segment with high potential due to its high storage density and low cost. However, it only stores three bits per cell, requiring more error correction codes and resulting in shorter read/write life cycles compared to SLC and MLC. This makes TLC ideal for consumer applications with lower write requirements, such as memory cards. SSDs come in various form factors, including 2.5-inch and M.2, and interface standards like SATA, NVMe, and PCIe.

Firmware updates and power management features, such as read amplification and garbage collection, help optimize performance and extend SSD lifespan. With advancements in cell technology, SSDs offer increased storage capacity, faster latency performance, and higher data transfer rates. Despite these advancements, power consumption and thermal throttling remain considerations, as does data encryption and data integrity. Overall, SSDs offer significant benefits over traditional hard drives, including faster read/write speeds, improved power efficiency, and enhanced reliability.

The TLC segment was valued at USD 7.93 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 30% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Solid State Drive (SSD) Market Demand is Rising in APAC Request Free Sample

The market in APAC is experiencing significant growth, driven by the expanding use of SSDs in data centers and enterprises. South Korea and Japan are leading contributors to this burgeoning market. During the forecast period, Taiwan, China, and India are anticipated to emerge as substantial contributors to the SSD market in APAC. Government initiatives, such as the National Policy on Electronics (NPE 2019) in India, aim to expand the electronic industry, creating clusters for the entire value chain and employing over 10 million people, contributing to the industry's growth.

The APAC SSD market's expansion is a testament to the region's commitment to technological advancement and digital transformation.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is witnessing significant growth due to the increasing demand for high-performance storage solutions in various industries. NAND flash memory, the primary technology behind SSDs, is available in multiple cell types, including Multi-Level Cell (MLC), Triple-Level Cell (TLC), and Quad-Level Cell (QLC), each offering different performance and cost trade-offs. SSDs come with various interfaces, such as Serial Advanced Technology Attachment (SATA) and Non-Volatile Memory Express (NVMe), with NVMe offering faster data transfer rates and lower latency. SSD controller architecture designs play a crucial role in determining the overall performance of these drives. Write amplification, a common issue in SSDs, significantly impacts their lifespan.

Data encryption techniques, such as AES and XOR, are increasingly being adopted to enhance data security in SSDs. Trim and other optimizations help improve SSD performance by managing unused space and reducing write amplification. Managing thermal throttling and power consumption are essential considerations for SSDs, with thermal throttling limiting performance when temperatures exceed safe levels. SSDs employ wear leveling techniques, firmware updates, and data recovery methods to ensure data integrity and reliability. High-performance SSD configurations, such as RAID and JBOD, are popular choices for systems requiring large storage capacities and high data transfer rates. Choosing the right SSD for specific system needs involves considering factors like interface compatibility, capacity, performance, and cost.

SSD failure prediction and prevention techniques, including self-monitoring, analysis, and reporting technology (SMART), are gaining importance to minimize downtime and data loss. M.2 and 2.5-inch SSDs cater to different form factor requirements, with M.2 offering smaller dimensions and 2.5-inch drives providing larger capacities. Advanced SSD data compression methods, such as lossless and lossless-compressible data compression, help optimize storage capacity and improve overall system performance. Understanding SSD garbage collection and over-provisioning strategies is crucial for maximizing the lifespan and efficiency of these drives. Despite the growing competition, a few players dominate the high-end SSD market, accounting for over 40% of the market share.

Market information suggests that the industrial sector is adopting SSDs at a significantly faster pace than the academic sector, with adoption rates nearly doubling in the former.

What are the key market drivers leading to the rise in the adoption of Solid State Drive (SSD) Industry?

- The market's growth is driven primarily by enhanced performance and durability, making it a compelling choice for consumers seeking reliable and efficient solutions.

- Solid-state drives (SSDs) and hard disk drives (HDDs) are two primary storage technologies that cater to varying data access requirements. SSDs, devoid of moving parts, ensure data stability even in turbulent conditions. In contrast, HDDs rely on physical scanning for reads and writes, making them susceptible to performance issues in high-intensity environments. SSDs' architecture, without physical tracks or sectors, grants swift access to memory addresses.

- This attribute is particularly advantageous in Tier 0 and Tier 1 databases and caching technologies. The absence of mechanical components in SSDs significantly expedites input/output (I/O) requests, providing a notable edge over HDDs. By eliminating the need for physical seek limits, SSDs cater to the increasing demand for high-speed data access in modern businesses.

What are the market trends shaping the Solid State Drive (SSD) Industry?

- Portable solid-state drives (SSDs) represent the latest market trend, gaining increasing popularity due to their compact size and high-speed data transfer capabilities.

- Portable Solid State Drives (SSDs) have significantly transformed the data storage landscape, providing a multitude of advantages over conventional Hard Disk Drives (HDDs). One of the most notable benefits is their enhanced speed. SSDs process data much quicker than HDDs, resulting in reduced time for file transfers and system initialization. This is primarily due to the absence of moving parts in SSDs, which eliminates the latency associated with HDDs. Moreover, the durability of portable SSDs is another significant advantage. Their solid-state design renders them less susceptible to physical damage from drops or shocks, ensuring data security. Furthermore, their compact size and lightweight construction make them highly portable, enabling users to transport large volumes of data effortlessly.

- Recent innovations in portable SSD technology include the Samsung T9, released in October 2023, which boasts a USB 3.2 Gen 2 interface, offering impressive data transfer speeds. These advancements underscore the continuous evolution of portable SSDs and their expanding applications across various sectors.

What challenges does the Solid State Drive (SSD) Industry face during its growth?

- The issue of poor latency and endurance poses a significant challenge to the industry's growth, as these factors negatively impact performance and efficiency.

- The inconsistent performance of Input/Output (I/O) operations in storage systems remains a significant challenge for businesses. While write latency can be masked with write-back caching, read latency cannot be hidden. SSD latencies typically range from a few hundred microseconds to several milliseconds, but can exceed seconds when access is disrupted by internal tasks. The unpredictability of IO performance is further compounded by the lack of coordination across an array of devices. Endurance is another hurdle, as SSDs have fewer write cycles than hard disks. These challenges necessitate ongoing research and innovation to improve I/O performance and reliability.

- For instance, advancements in flash memory technology, such as 3D NAND and QLC, aim to enhance endurance and reduce latency. Additionally, the integration of AI and machine learning algorithms in storage systems is expected to optimize I/O operations and improve overall system performance. These evolving trends underscore the importance of addressing I/O challenges in an increasingly data-driven business landscape.

Exclusive Technavio Analysis on Customer Landscape

The solid state drive (ssd) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the solid state drive (ssd) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Solid State Drive (SSD) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, solid state drive (ssd) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ADATA Technology Co. Ltd. - The company specializes in manufacturing solid state drives, including the Legend 800 gold, Legend 700 gold, and Legend 850 Lite models. These drives offer reliable storage solutions with advanced technology and high performance, making them a top choice for consumers seeking efficient data management.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ADATA Technology Co. Ltd.

- Corsair Gaming Inc.

- DataDirect Networks Inc.

- International Business Machines Corp.

- Kingston Technology Co. Inc.

- Kioxia Corp.

- LITE ON Technology Corp.

- Maxta Inc.

- Micron Technology Inc.

- NetApp Inc.

- Pure Storage Inc.

- Samsung Electronics Co. Ltd.

- Sandisk Corp.

- Seagate Technology LLC

- Simms International plc

- SK hynix Co. Ltd.

- Solidigm

- Sony Group Corp.

- Toshiba Corp.

- Transcend Information Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Solid State Drive (SSD) Market

- In January 2024, Intel Corporation announced the launch of its new 700p Series SSD, featuring PCIe 4.0 technology and up to 1TB capacity (Intel press release). This release marked Intel's entry into the high-performance SSD market, intensifying competition with industry leaders like Samsung and Micron.

- In March 2024, Western Digital Corporation and Kioxia Corporation, two major SSD manufacturers, announced a strategic partnership to co-develop next-generation SSD solutions (Western Digital press release). This collaboration aimed to combine Western Digital's expertise in HDDs and Kioxia's strength in flash memory technology, potentially leading to innovative SSD products and improved market competitiveness.

- In April 2025, Seagate Technology completed the acquisition of Samsung's SSD business for approximately USD1.37 billion (Bloomberg). This acquisition significantly expanded Seagate's SSD portfolio and market share, making it a formidable competitor in the SSD market.

- In May 2025, Samsung Electronics unveiled its 16TB SSD, the world's largest capacity SSD for data centers (Samsung press release). This technological advancement demonstrated Samsung's commitment to pushing the boundaries of SSD capacity, potentially revolutionizing data center storage solutions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Solid State Drive (SSD) Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

199 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 40.9% |

|

Market growth 2025-2029 |

USD 275.76 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

29.5 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, with key trends shaping its dynamics. One significant development is the increasing focus on drive endurance, as manufacturers strive to enhance read/write speeds and extend SSD lifespan. Host interfaces, such as M.2 and NVMe, are gaining popularity due to their faster data transfer rates. Firmware updates play a crucial role in optimizing SSD performance, with improvements in read amplification and power management contributing to enhanced controller performance. The 2.5-inch form factor remains common, but the M.2 form factor's compact size and NVMe interface's high bandwidth are driving adoption. Power consumption is another critical factor, with SSDs increasingly offering energy efficiency.

- Data encryption is also a priority, with interface standards like PCIe and SATA supporting encryption to ensure data integrity. SSDs employ various technologies, including NAND flash memory, error correction codes, and wear leveling, to improve latency performance and data transfer rates. Thermal throttling and data retention are ongoing challenges, with manufacturers addressing these issues through advanced cooling systems and improved firmware. The SSD market's continuous evolution is driven by the pursuit of higher storage capacity, improved cell technology, and advanced interface standards. As the market adapts to these trends, SSDs are becoming an essential component of modern computing systems, offering significant performance advantages over traditional hard disk drives.

What are the Key Data Covered in this Solid State Drive (SSD) Market Research and Growth Report?

-

What is the expected growth of the Solid State Drive (SSD) Market between 2025 and 2029?

-

USD 275.76 billion, at a CAGR of 40.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (TLC, MLC, and SLC), End-user (Laptops and PCs), Geography (APAC, North America, Europe, South America, and Middle East and Africa), Form Factor (2.5 Inch, M.2, U.2, and AIC (Add-in Card)), and Storage Capacity (Under 250 GB, 250 GB - 500 GB, 500 GB - 1 TB, 1 TB - 2 TB, and Above 2 TB)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Enhanced performance and durability, Poor latency and endurance

-

-

Who are the major players in the Solid State Drive (SSD) Market?

-

ADATA Technology Co. Ltd., Corsair Gaming Inc., DataDirect Networks Inc., International Business Machines Corp., Kingston Technology Co. Inc., Kioxia Corp., LITE ON Technology Corp., Maxta Inc., Micron Technology Inc., NetApp Inc., Pure Storage Inc., Samsung Electronics Co. Ltd., Sandisk Corp., Seagate Technology LLC, Simms International plc, SK hynix Co. Ltd., Solidigm, Sony Group Corp., Toshiba Corp., and Transcend Information Inc.

-

Market Research Insights

- The market continues to evolve, with advancements in technology driving increased adoption. SSDs utilize memory chips instead of traditional spinning disks, resulting in faster read and write speeds and improved power efficiency. According to industry estimates, the global SSD market size is projected to reach USD126.8 billion by 2027, growing at a CAGR of 21.3% from 2020. One key factor contributing to this growth is the ongoing development of wear-leveling algorithms, which enhance SSD endurance and extend drive reliability. For instance, SSDs with advanced error correction and data security features, such as those using NVMe protocol, offer superior performance and data protection compared to their SATA counterparts.

- Additionally, the emergence of form factors like PCIe and M.2, along with RAID configurations and data migration tools, provide flexible storage solutions for businesses and consumers alike. Despite these advancements, challenges remain. Power efficiency and interface compatibility are crucial considerations for organizations seeking to optimize system performance. Furthermore, data storage solutions must also address data recovery, data compression, data deduplication, and data virtualization to meet the evolving demands of modern businesses. Ultimately, the SSD market will continue to innovate, driven by the need for faster, more efficient, and more secure data storage solutions.

We can help! Our analysts can customize this solid state drive (ssd) market research report to meet your requirements.

RIA -

RIA -