Real Estate Software Market Size 2024-2028

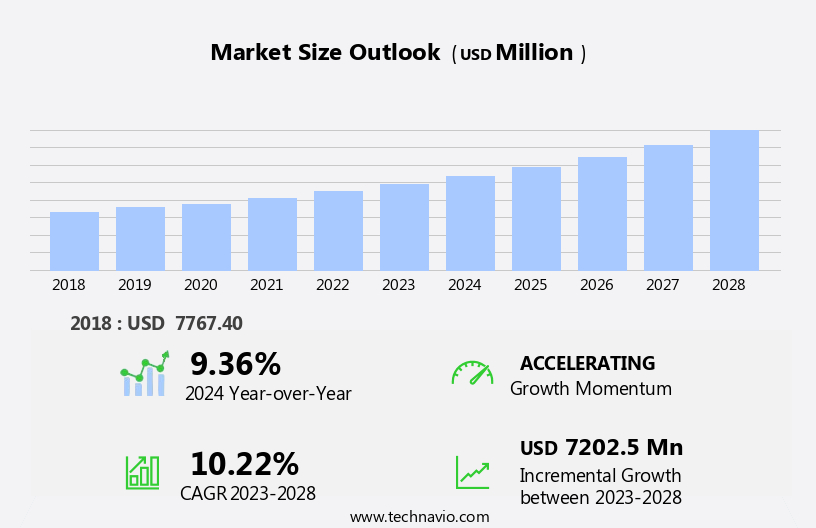

The real estate software market size is forecast to increase by USD 7.2 billion, at a CAGR of 10.22% between 2023 and 2028.

- The market is experiencing significant growth, driven primarily by the expanding middle-class population. This demographic shift is fueling increased demand for advanced real estate management solutions, as more individuals and families seek to purchase and manage properties. Another key trend shaping the market is the adoption of blockchain technology in real estate management software. This innovative solution offers enhanced security, transparency, and efficiency, making it an attractive option for both property owners and service providers. However, the market also faces challenges, including the increasing threat of open-source real estate management software.

- These free alternatives can undercut the pricing of proprietary software, putting pressure on market players to differentiate through value-added services and superior functionality. To capitalize on opportunities and navigate challenges effectively, companies must stay abreast of market trends and consumer needs, continuously innovating to deliver solutions that meet evolving demands.

What will be the Size of the Real Estate Software Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, with dynamic market activities shaping the industry's landscape. Property management solutions are increasingly incorporating advanced features to streamline operations and enhance user experience. These include maintenance management, CRM integration, data security, contract management, rent collection, data analytics, user interface, real-time data, document management, budgeting tools, training and documentation, company management, property tax management, workflow automation, online payment processing, compliance management, security features, 3D modeling, property listing, applicant tracking, legal compliance, expense tracking, on-premise solutions, virtual tours, customizable dashboards, and more. Integration of insurance and accounting systems, property valuation, property search, mobile accessibility, task management, automated emails, performance monitoring, lease management, cloud-based solutions, vacancy management, lease renewals, API integrations, inspection management, eviction management, marketing automation, customer support, tenant screening, communication tools, financial forecasting, reporting and analytics, and predictive analytics are becoming essential components of comprehensive property management software.

The market's continuous evolution reflects the industry's growing need for efficient, data-driven, and secure solutions. These tools enable real estate professionals to manage their properties effectively, ensuring optimal performance and profitability. The integration of various features allows for seamless workflows, improved communication, and enhanced data security. As the market continues to unfold, the focus on user experience, real-time data, and customization will remain key drivers of innovation.

How is this Real Estate Software Industry segmented?

The real estate software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Deployment

- Cloud-based

- On-premises

- Application

- Residential

- Commercial

- Geography

- North America

- US

- Europe

- France

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

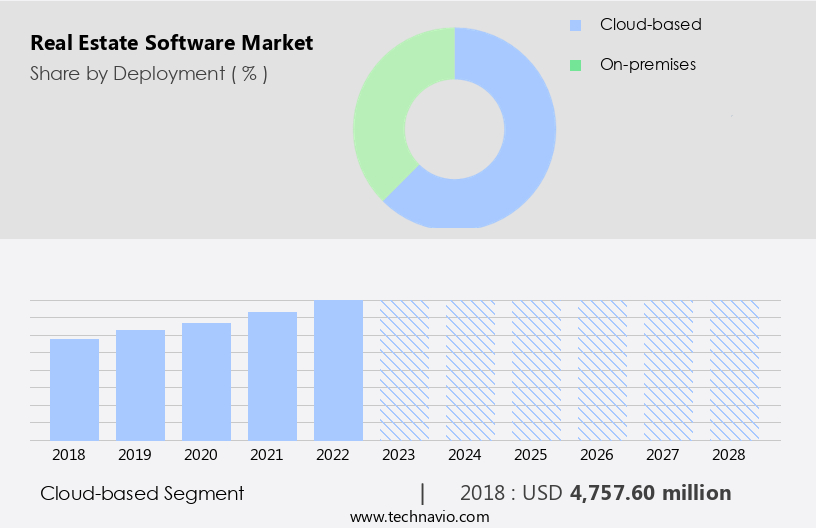

By Deployment Insights

The cloud-based segment is estimated to witness significant growth during the forecast period.

In the realm of real estate management, cloud-based solutions are gaining significant traction among businesses due to their affordability, ease of implementation, and low maintenance costs. These solutions offer various features such as maintenance management, CRM integration, data security, contract management, rent collection, data analytics, user-friendly interfaces, real-time data access, document management, budgeting tools, training and documentation, company management, property tax management, workflow automation, online payment processing, compliance management, security features, 3D modeling, property listing, applicant tracking, legal compliance, expense tracking, and more. Cloud-based property management software enables small and medium-sized enterprises (SMEs) and startups to avoid the high costs associated with on-premises solutions.

The software is accessible from anywhere, making it ideal for remote teams and those who need to access information on the go. It also offers customizable dashboards, accounting integration, lease management, and performance monitoring. Moreover, cloud-based solutions offer scalability, allowing businesses to add or remove features as needed. They also provide real-time data, enabling users to make informed decisions quickly. Security features, such as encryption and access controls, ensure data protection. Additionally, cloud-based solutions offer integration with other business applications, such as marketing automation, customer support, tenant screening, communication tools, financial forecasting, reporting and analytics, and predictive analytics.

The adoption of cloud-based real estate software is on the rise due to its numerous benefits. It eliminates the need for purchasing servers and offers easy accessibility from any electronic device. Its cost-effectiveness makes it an attractive option for businesses looking to streamline their operations and improve efficiency.

The Cloud-based segment was valued at USD 4.76 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

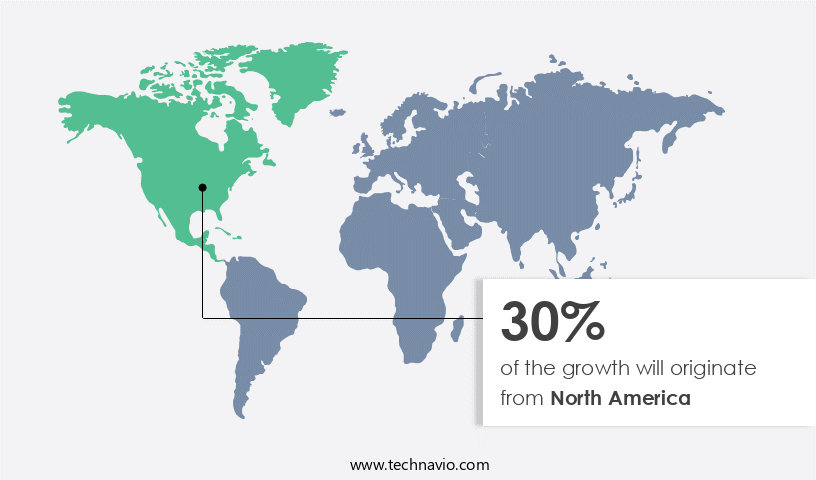

North America is estimated to contribute 30% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The US real estate market is experiencing steady growth, driven by a robust economy and low unemployment rates. This economic stability has fostered a positive outlook among citizens, leading to an increase in first-time homebuyers. However, population growth in the US remains moderate, but the number of immigrants is on the rise, contributing to a demand-supply imbalance in the housing sector. In response, construction activities are expected to increase, fueling the need for advanced property management solutions. These software systems offer various features such as maintenance management, CRM integration, data security, contract management, rent collection, data analytics, user interface, real-time data, document management, budgeting tools, training and documentation, company management, property tax management, workflow automation, online payment processing, compliance management, security features, 3D modeling, property listing, applicant tracking, legal compliance, expense tracking, on-premise solutions, virtual tours, customizable dashboards, property management software, insurance integration, property valuation, property search, mobile accessibility, task management, automated emails, performance monitoring, lease management, cloud-based solutions, vacancy management, accounting integration, lease renewals, API integrations, inspection management, eviction management, marketing automation, customer support, tenant screening, communication tools, financial forecasting, reporting and analytics, and predictive analytics.

These solutions streamline property management tasks, enhance security, improve communication, and provide valuable data insights, making them essential tools for real estate professionals and property managers in meeting the demands of the growing market.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

In the dynamic and competitive real estate industry, software solutions have become indispensable tools for brokers, agents, and property managers. The market caters to diverse needs, offering integrated platforms that streamline property listings, client management, and transaction processing. These solutions utilize advanced search algorithms, enabling users to find properties based on location, price range, and property type. Additionally, they offer features like virtual tours, document management, and marketing automation, enhancing the overall customer experience. Real-time data analytics and reporting capabilities provide valuable insights, while mobile applications ensure accessibility on the go. Security and compliance are paramount, with solutions offering data encryption, secure login, and regulatory compliance. Overall, real estate software empowers professionals to manage their businesses more efficiently and effectively, driving growth and success in the industry.

What are the key market drivers leading to the rise in the adoption of Real Estate Software Industry?

- The middle-class population, which continues to expand, serves as the primary catalyst for market growth.

- The market is experiencing significant growth due to the increasing middle-class population and rising disposable income in developing countries, particularly in Asia Pacific, South America, and the Middle East and Africa. These regions are witnessing robust economic activities, including industrialization, manufacturing, and urbanization, leading to an increased demand for long-term investment opportunities. Real estate software solutions are essential tools for property management companies to streamline their operations and enhance efficiency. These solutions offer features such as maintenance management, contract management, rent collection, data analytics, and budgeting tools. The integration of CRM systems and data security measures are also crucial for managing customer relationships and ensuring data privacy.

- Moreover, real-time data access, document management, and company management are essential functions that real estate software solutions provide to help businesses manage their properties effectively. Training and documentation are also vital to ensure that users can leverage the software's full potential. In conclusion, The market is poised for growth due to the increasing demand for efficient property management solutions in developing economies. The market offers various features, including maintenance management, CRM integration, data security, contract management, rent collection, data analytics, user interface, real-time data, document management, budgeting tools, training, and documentation, and company management, making it an indispensable tool for property management companies.

What are the market trends shaping the Real Estate Software Industry?

- The use of blockchain technology in real estate management software is an emerging market trend. This innovative approach enhances security, transparency, and efficiency in managing real estate transactions and records.

- The market is witnessing significant advancements, with technology playing a pivotal role in streamlining processes and enhancing transparency. One of the key areas of focus is property tax management, where workflow automation and online payment processing are becoming increasingly popular. Compliance management is another crucial aspect, with security features being prioritized to protect sensitive data. In addition to these functionalities, real estate software solutions are incorporating innovative features such as 3D modeling, property listing, applicant tracking, legal compliance, and expense tracking. These solutions are available both as on-premise and cloud-based options, catering to the varying needs of businesses.

- Moreover, the integration of blockchain technology in real estate software is revolutionizing the industry. This technology provides a secure and transparent platform for transactions by encrypting every record and making ledgers impenetrable to hackers. It eliminates the need for intermediaries, enabling seamless and quick transactions. With blockchain technology, real estate deals can be completed efficiently and securely, even outside of business hours. Overall, The market is witnessing rapid growth, driven by the need for automation, transparency, and security.

What challenges does the Real Estate Software Industry face during its growth?

- The expansion of open-source real estate management software poses a significant challenge to the industry's growth trajectory. This trend, driven by its accessibility and cost-effectiveness, may potentially disrupt traditional business models and market dynamics within the real estate sector.

- The market faces significant competition from the growing adoption of customizable open-source property management solutions. Open-source software, which is freely available online, offers several advantages, including transparency due to accessible source code, cost savings, and scalability. Popular open-source real estate software options include EspoCRM, Vtiger CRM, and Bitrix CRM. These solutions cater to organizations with limited budgets, providing functionality comparable to paid software. However, they offer flexibility for users to customize dashboards, integrate insurance, manage properties, search for new listings, and perform various tasks. Additionally, open-source software supports mobile accessibility, automated emails, lease management, vacancy management, and performance monitoring through cloud-based solutions.

- Despite the benefits, it is crucial for organizations to ensure the security and ongoing support for open-source software.

Exclusive Customer Landscape

The real estate software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the real estate software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, real estate software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Altus Group Ltd. - Utilizing advanced technology, our real estate software, Altus Valuation, streamlines property asset and tax management. This solution empowers users to effectively monitor and optimize their real estate portfolios. With features including automated data collection and robust reporting capabilities, Altus Valuation enhances operational efficiency and accuracy.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Altus Group Ltd.

- AppFolio Inc.

- Autodesk Inc.

- Bentley Systems Inc.

- CDK Global Inc.

- CoStar Group Inc.

- CREATIO EMEA Ltd.

- Dassault Systemes SE

- Fiserv Inc.

- Fortive Corp.

- IFCA MSC Berhad

- International Business Machines Corp.

- LanTrax Inc.

- MRI Software LLC

- Oracle Corp.

- Planon Shared Services BV

- RealPage Inc.

- SAP SE

- Trimble Inc.

- Yardi Systems Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Real Estate Software Market

- In January 2024, PropTech leader Yardi Systems announced the launch of Yardi Voyager 9S, an advanced real estate investment management solution, integrating AI and machine learning capabilities to streamline property management and investment analysis (Yardi Systems Press Release).

- In March 2024, CoStar Group, a leading commercial real estate information provider, entered into a strategic partnership with Microsoft to integrate CoStar's property data into Microsoft's Azure cloud platform, enhancing data accessibility and analytics capabilities for real estate professionals (CoStar Group Press Release).

- In May 2024, RE/MAX, a global real estate franchisor, completed a USD50 million Series C funding round, led by Blackstone, to accelerate the growth of its RE/MAX Cloud platform and expand its technology offerings (RE/MAX Press Release).

- In April 2025, the European Union's General Data Protection Regulation (GDPR) came into full effect, requiring real estate software companies to comply with stringent data privacy regulations, leading to increased investments in data security and privacy solutions (European Commission Press Release).

Research Analyst Overview

- In the dynamic real estate market, software solutions continue to evolve, integrating advanced technologies to enhance user experience (UX) and facilitate efficient asset management. Data visualization tools enable real estate professionals to gain insights from complex property data, while open data standards ensure seamless data integration. Financial modeling and portfolio management systems help in making informed investment decisions, and regulatory compliance tools assist in due diligence and legal review processes. Smart building technologies, such as augmented reality (AR) and virtual reality (VR), revolutionize space planning and facility management. Accessibility standards and sustainability reporting tools cater to the growing focus on environmental compliance and social responsibility.

- Machine learning (ML) and artificial intelligence (AI) applications streamline risk management, energy management, and competitive analysis. Market research tools and business intelligence (BI) platforms provide valuable insights into industry trends, while property data aggregators ensure access to comprehensive and up-to-date information. Blockchain technology offers enhanced security and transparency in asset management and regulatory compliance. Building management systems and regulatory compliance tools ensure efficient operations and adherence to legal requirements. Data integration and data modeling are essential for effective property assessment and investment analysis. Market research tools and competitive analysis software help stakeholders stay informed about market trends and competitors.

- Overall, these advanced technologies and software solutions continue to transform the real estate industry, offering significant benefits to businesses and professionals.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Real Estate Software Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.22% |

|

Market growth 2024-2028 |

USD 7202.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

9.36 |

|

Key countries |

US, China, UK, France, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Real Estate Software Market Research and Growth Report?

- CAGR of the Real Estate Software industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the real estate software market growth of industry companies

We can help! Our analysts can customize this real estate software market research report to meet your requirements.

RIA -

RIA -