Retail Media Networks Market Size 2025-2029

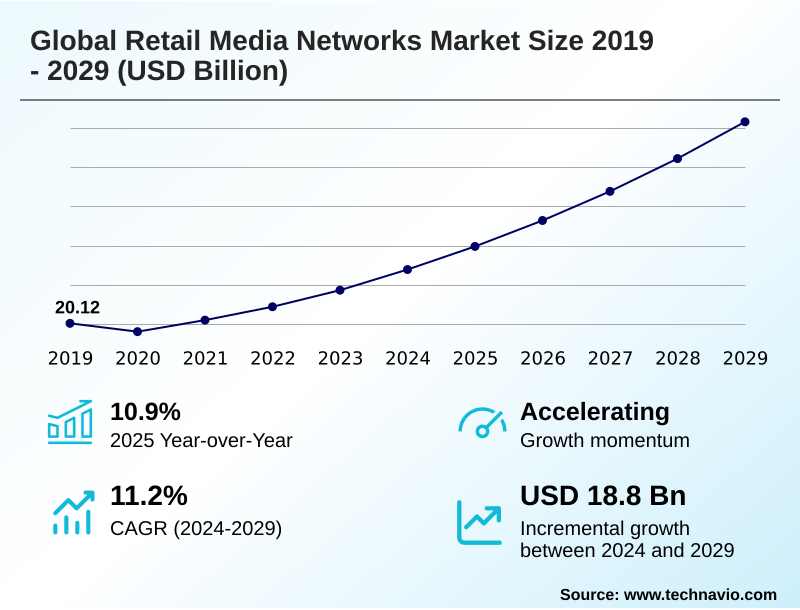

The retail media networks market size is valued to increase by USD 18.80 billion, at a CAGR of 11.2% from 2024 to 2029. Proliferation of first-party data amidst third-party cookie depreciation will drive the retail media networks market.

Major Market Trends & Insights

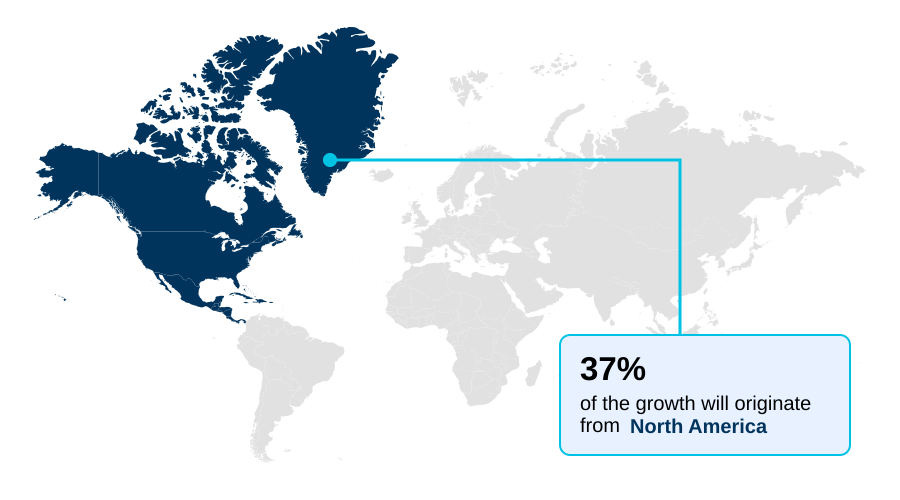

- North America dominated the market and accounted for a 36.9% growth during the forecast period.

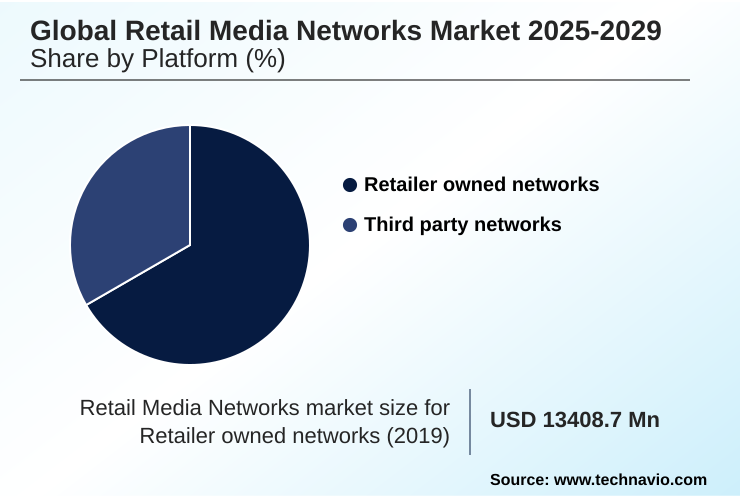

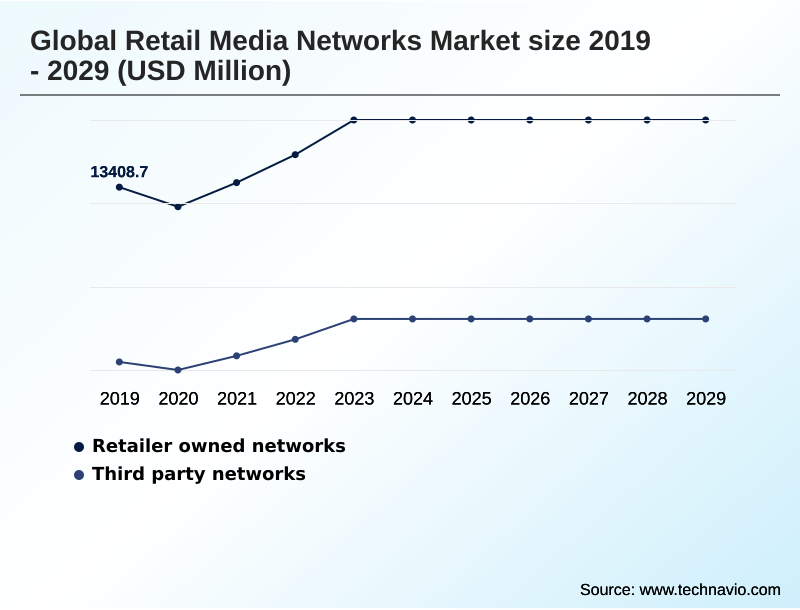

- By Platform - Retailer owned networks segment was valued at USD 15.98 billion in 2023

- By Type - Display ads segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 25.66 billion

- Market Future Opportunities: USD 18.80 billion

- CAGR from 2024 to 2029 : 11.2%

Market Summary

- The retail media networks market is undergoing a significant transformation, moving from a niche advertising channel to a central pillar of digital marketing strategy. This shift is primarily fueled by the diminishing effectiveness of traditional tracking methods, making retailer-owned first-party data a highly valuable asset.

- Advertisers are increasingly turning to these networks to achieve closed-loop attribution, directly linking media spend to sales outcomes. Key trends include the expansion of advertising capabilities beyond retailers' owned websites to include connected TV and social media, alongside the digitization of the in-store experience.

- For example, a consumer packaged goods company can now launch a new product using a retailer's self-service ad platform, targeting specific shopper segments with personalized video ads, and subsequently use in-store attribution data to measure how those digital campaigns influenced physical purchases.

- However, the industry grapples with challenges such as measurement standardization and the need to balance ad load with a positive customer experience. Success in the retail media networks market requires navigating this complex ecosystem to deliver relevant, performance-driven campaigns.

What will be the Size of the Retail Media Networks Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Retail Media Networks Market Segmented?

The retail media networks industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Platform

- Retailer owned networks

- Third party networks

- Type

- Display ads

- Sponsored products

- Video ads

- Others

- End-user

- Consumer packaged goods

- Electronics and technology

- Apparel and fashion

- Grocery and food delivery

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Platform Insights

The retailer owned networks segment is estimated to witness significant growth during the forecast period.

Retailer-owned networks are a dominant force, characterized by proprietary advertising platforms that grant operators full control over first-party data activation and the overall advertiser experience. These networks are built on significant infrastructure investments to enable sophisticated shopper data monetization.

This model, which now accounts for over 65% of total market activity, leverages loyalty program data to offer advanced capabilities like programmatic display ads and detailed omnichannel measurement.

As third-party cookie depreciation continues, the value of these walled-garden ecosystems increases, providing a competitive edge through superior cookieless audience targeting.

Effective ad load management is critical to balance this advertising revenue stream with a positive shopping journey, ensuring long-term platform viability and delivering strong return on ad spend for partners.

The Retailer owned networks segment was valued at USD 15.98 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Retail Media Networks Market Demand is Rising in North America Get Free Sample

The market's geographic landscape is led by North America, which is projected to contribute nearly 37% of the total incremental growth, underscoring its maturity and high adoption rate of full-funnel marketing solutions.

In this region, advanced commerce media platforms have demonstrated up to a 20% increase in campaign efficiency through superior data-driven optimization. Following closely, APAC and Europe represent dynamic growth fronts, together accounting for over 53% of the market opportunity.

The APAC market is characterized by mobile-first ecosystems and the integration of AI-powered recommendations. Europe's development is shaped by strict data privacy regulations, which has accelerated the demand for consent-based supplier-funded advertising and effective technology stack integration.

The remaining regions, including South America and the Middle East and Africa, are emerging markets focused on building foundational retail media APIs and infrastructure.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Successfully navigating the evolving digital advertising landscape requires a deep understanding of how to execute a full-funnel retail media strategy, particularly for consumer packaged goods (CPG) brands. A central challenge is connecting digital ads to in-store sales, a task that demands robust omnichannel attribution for sponsored search ads.

- The solution often involves leveraging loyalty data for programmatic advertising, which allows for precise targeting. However, this approach highlights the persistent challenges of retail media network standardization, making it difficult to compare performance across different platforms. Accurately measuring incremental lift in retail media is therefore paramount, as it distinguishes true advertising impact from sales that would have occurred anyway.

- Advanced strategies are now integrating retail data with connected TV targeting, creating a powerful combination of reach and relevance. The future of in-store retail media technology and the role of AI in retail media personalization will further enhance these capabilities. Moreover, the industry is exploring how to effectively target non-endemic brands on retail sites.

- Firms that master the art of managing campaign fragmentation across networks and can prove a clear return on investment by enhancing ROAS with first-party shopper data will gain a significant competitive advantage. As programmatic buying in walled garden environments becomes more sophisticated, analyzing shoppable video ad performance measurement will be key to optimizing media budgets.

- Ultimately, the ability to balance ad revenue with customer experience will define long-term success.

What are the key market drivers leading to the rise in the adoption of Retail Media Networks Industry?

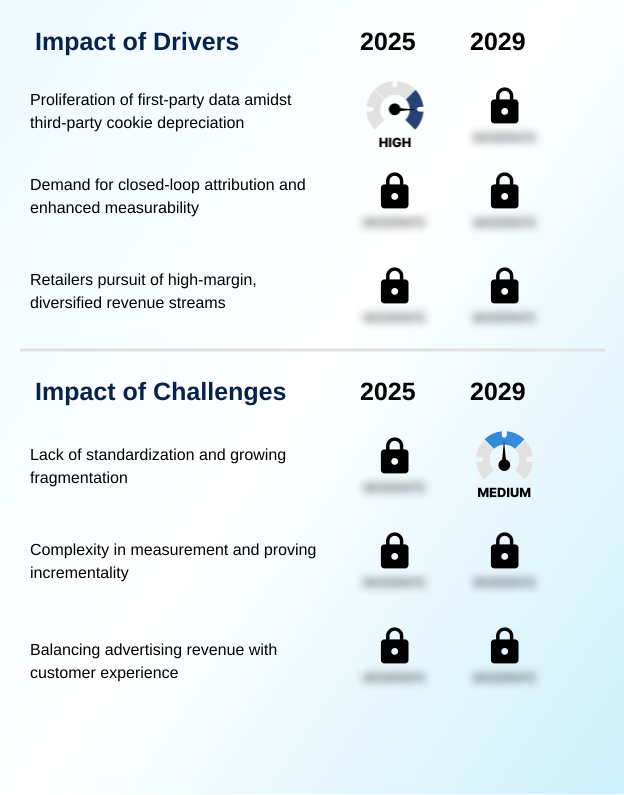

- The proliferation of retailer-owned first-party data, spurred by the depreciation of third-party cookies, is a primary driver of market growth.

- Market growth is primarily driven by the high demand for measurable advertising outcomes and new revenue streams for retailers.

- The deprecation of third-party cookies has made first-party data the cornerstone of digital advertising, with platforms leveraging loyalty program data improving audience targeting accuracy by over 50%.

- This enables precise, performance-based campaigns and robust closed-loop attribution, allowing brands to justify trade marketing budgets with concrete sales data.

- For retailers, the development of an advertising revenue stream provides a high-margin business that improves overall profitability, with advertising contributing up to 5% of total EBIT in mature operations.

- This dynamic is shifting budgets toward channels that offer clear marketing mix optimization and shopper marketing insights.

What are the market trends shaping the Retail Media Networks Industry?

- A defining market trend involves the strategic expansion of advertising capabilities beyond retailers' owned digital properties. This evolution transforms retail media into a full-funnel marketing tool by leveraging first-party data across the open internet.

- Key market trends are redefining advertising effectiveness, with a notable shift toward off-site media extension and omnichannel retail strategy. The strategic push to activate shopper data beyond a retailer’s own properties through connected TV advertising and other channels is expanding the scope of performance-based campaigns.

- This integration is delivering measurable results, with campaigns that span online and in-store digital media showing up to a 20% uplift in customer lifetime value. Concurrently, the proliferation of self-service ad platforms is democratizing access, enabling smaller brands to reduce campaign setup times by over 40%.

- This trend toward campaign automation and media network consolidation fosters a more agile and competitive environment, allowing for more dynamic creative optimization.

What challenges does the Retail Media Networks Industry face during its growth?

- The lack of standardization across a rapidly fragmenting landscape of distinct retail media platforms presents a significant challenge to market scalability and efficiency.

- The market faces significant operational hurdles, primarily stemming from the lack of retail media standardization and the complexities of omnichannel measurement. The fragmentation across walled-garden ecosystems can increase operational overhead for agencies by up to 35% when managing campaigns across multiple retailers.

- Proving the true impact of spend is another issue, as default attribution models often fail to provide accurate incrementality measurement. Furthermore, retailers must carefully balance ad revenue with user experience optimization, as A/B testing reveals that excessive ad loads can decrease organic conversion rates by 10%.

- These factors necessitate a greater focus on media mix modeling and create challenges in achieving a holistic view of campaign performance metrics.

Exclusive Technavio Analysis on Customer Landscape

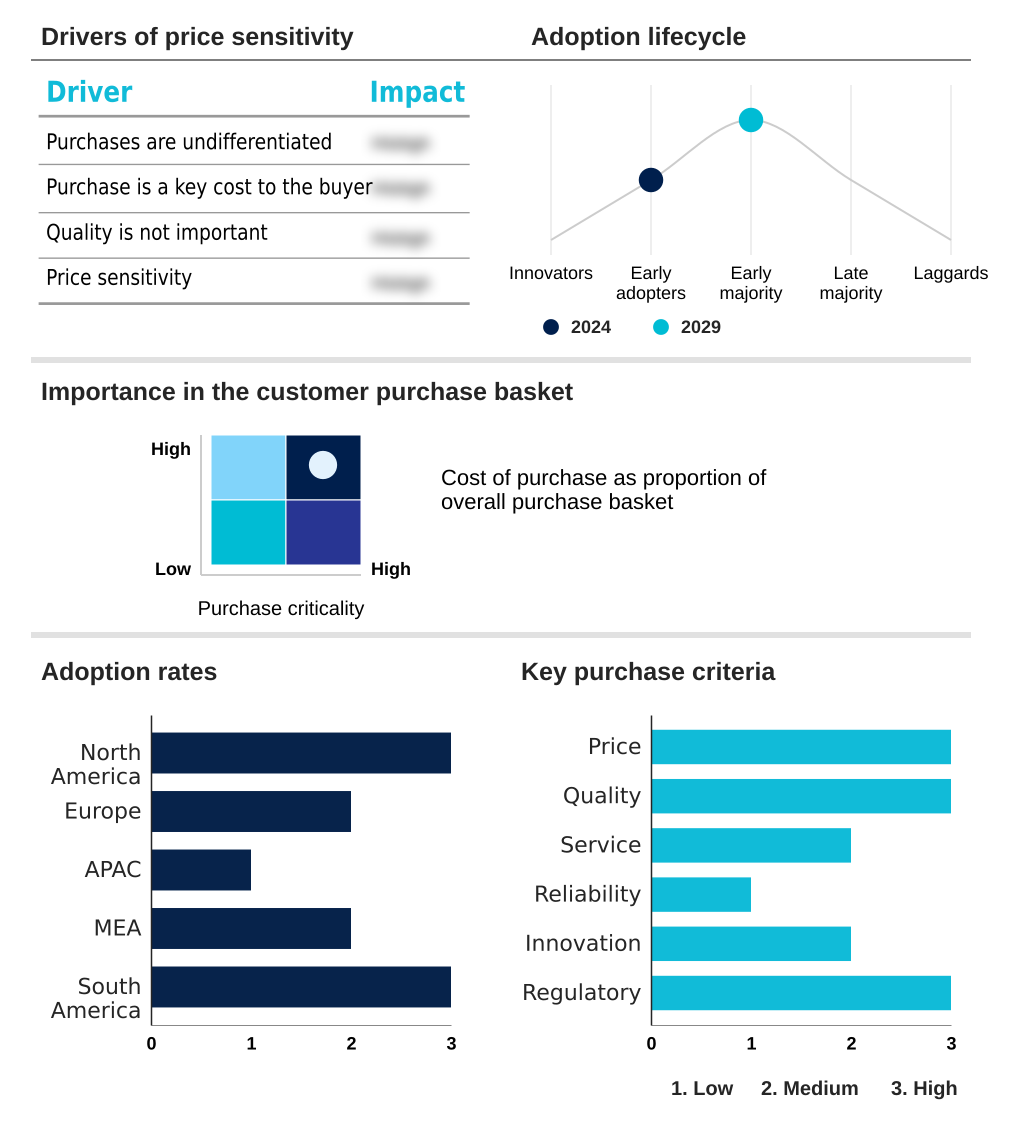

The retail media networks market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the retail media networks market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Retail Media Networks Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, retail media networks market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Albertsons Co. Inc - Offerings include integrated advertising platforms with sponsored products and display ads, designed to engage high-intent shoppers directly within a vast e-commerce ecosystem.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Albertsons Co. Inc

- Alibaba Group Holding Ltd.

- Amazon.com Inc.

- Best Buy Co. Inc.

- Carrefour SA

- CVS Health Corp.

- eBay Inc.

- JD.com Inc.

- Lowes Co. Inc.

- Macys Inc.

- Maplebear Inc.

- Target Corp.

- Tesco Plc

- The Home Depot Inc.

- The Kroger Co.

- Walmart Inc.

- Wayfair Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Retail media networks market

- In August 2024, Macy's Media Network expanded its partnership with marketing technology firm Rokt to utilize AI for personalizing the post-purchase customer journey.

- In September 2024, Tesco Media and Insight Platform extended its partnership with The Trade Desk to allow advertisers to use anonymized Tesco Clubcard data for targeting audiences on the open internet.

- In October 2024, The Home Depot launched Orange Access, a new self-service platform designed to simplify campaign planning and management for its supplier partners on the Orange Apron Media network.

- In May 2025, Unlimitail announced a partnership with Pacvue to enhance self-service capabilities for brands and agencies, starting with the Carrefour platform in France.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Retail Media Networks Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 308 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.2% |

| Market growth 2025-2029 | USD 18804.4 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 10.9% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, Australia, South Korea, Indonesia, Saudi Arabia, UAE, South Africa, Turkey, Israel, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The retail media networks market's trajectory is fundamentally shaped by the industry-wide third-party cookie depreciation, which has elevated the strategic value of first-party data activation. Retailer-owned networks are at the forefront, enabling sophisticated shopper data monetization through proprietary self-service ad platforms.

- Advertisers are deploying sponsored product ads and programmatic display ads to achieve closed-loop attribution and precisely measure return on ad spend. The critical boardroom decision now revolves around investment in omnichannel measurement, which is essential for bridging the digital and physical divide. Advanced platforms using cookieless audience targeting have already demonstrated a 30% greater efficiency in reaching qualified buyers.

- The pursuit of true incrementality measurement and the use of data clean rooms are becoming standard practice. As the landscape matures, the focus is shifting toward full-funnel marketing solutions, including shoppable video ads and connected TV advertising, creating a more cohesive and measurable advertising revenue stream for retailers.

What are the Key Data Covered in this Retail Media Networks Market Research and Growth Report?

-

What is the expected growth of the Retail Media Networks Market between 2025 and 2029?

-

USD 18.80 billion, at a CAGR of 11.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Platform (Retailer owned networks, and Third party networks), Type (Display ads, Sponsored products, Video ads, and Others), End-user (Consumer goods, Electronics and technology, Apparel and fashion, Grocery and food delivery, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of first-party data amidst third-party cookie depreciation, Lack of standardization and growing fragmentation

-

-

Who are the major players in the Retail Media Networks Market?

-

Albertsons Co. Inc, Alibaba Group Holding Ltd., Amazon.com Inc., Best Buy Co. Inc., Carrefour SA, CVS Health Corp., eBay Inc., JD.com Inc., Lowes Co. Inc., Macys Inc., Maplebear Inc., Target Corp., Tesco Plc, The Home Depot Inc., The Kroger Co., Walmart Inc. and Wayfair Inc.

-

Market Research Insights

- The market's dynamics are driven by a strategic shift toward performance-based campaigns and data-driven optimization, where advertisers demand tangible results. This focus on efficiency is reshaping shopper marketing insights, with leading platforms showing that advanced audience segmentation can improve click-through rates by up to 30%.

- Digital shelf optimization is also critical, as premium ad placements have been linked to a 20% lift in product consideration. As competition intensifies, advertisers are using brand term targeting and other sophisticated tactics to protect and grow market share. Furthermore, the push for advertiser self-service is accelerating, with self-managed campaigns achieving a 15% faster route to market compared to managed services.

- These shifts underscore a move toward greater transparency, control, and accountability in advertising spend.

We can help! Our analysts can customize this retail media networks market research report to meet your requirements.

RIA -

RIA -