Rheology Modifiers Market Size 2024-2028

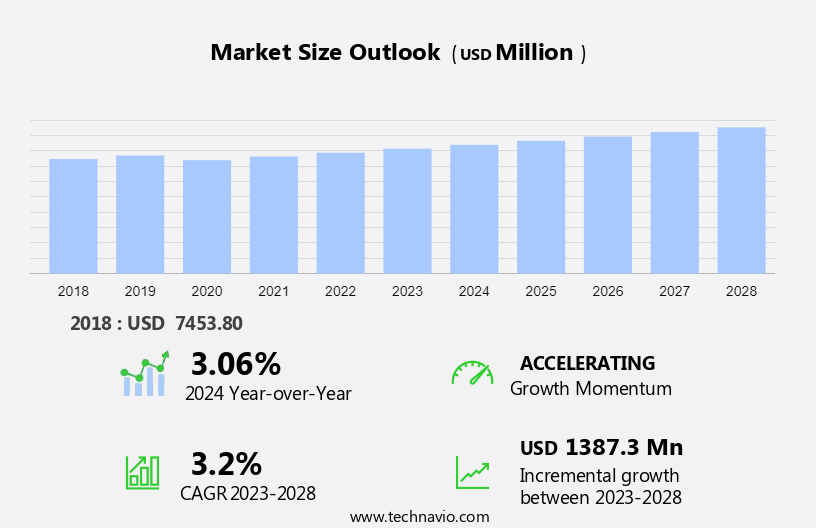

The rheology modifiers market size is forecast to increase by USD 1.39 billion at a CAGR of 3.2% between 2023 and 2028. The market is experiencing significant growth, driven by the increasing demand for efficient and high-performance additives in the paint and coating industry. This sector's expansion is fueled by the need for improved product quality, durability, and application properties. Another trend in the market is the growing utilization of nanoparticles in rheology modifiers, which offer enhanced performance and functionality. Additionally, the shift from print to digital media is impacting the market, as the demand for digital printing inks is on the rise, necessitating the use of rheology modifiers to ensure optimal ink flow and consistency. Overall, these factors are contributing to the market's growth and innovation.

The market is a significant industry that caters to various sectors, including Construction, Paints & Coatings, Cosmetics Personal Care, Adhesives & Sealants, Home Care, I&I Products, Inks, Oil & Gas, and others. Rheology modifiers, also known as viscosity control additives, play a crucial role in managing the flow characteristics of different materials. In construction, they are used as concrete admixtures to enhance the workability and durability of concrete in structures such as dams, roads, bridges, commercial buildings, and housing complexes. Organic and inorganic rheology modifiers, including clays, fumed silica, thickeners, viscofiers, and additives, are widely used to modify the viscosity and flow properties of these materials.

The market for rheology modifiers is driven by the increasing demand for high-performance and eco-friendly products in various end-use industries. The market is expected to grow at a steady pace due to the rising construction activities, increasing demand for cosmetics and personal care products, and the expanding oil & gas industry. The use of rheology modifiers in paints & coatings, adhesives & sealants, and home care products is also on the rise due to their ability to improve the product's consistency, texture, and stability.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD Billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product Type

- Organic

- Inorganic

- Application

- Paints and coatings

- Personal care

- Adhesives and sealants

- Household products

- Others

- Geography

- APAC

- China

- Japan

- South Korea

- Europe

- Germany

- North America

- US

- Middle East and Africa

- South America

- APAC

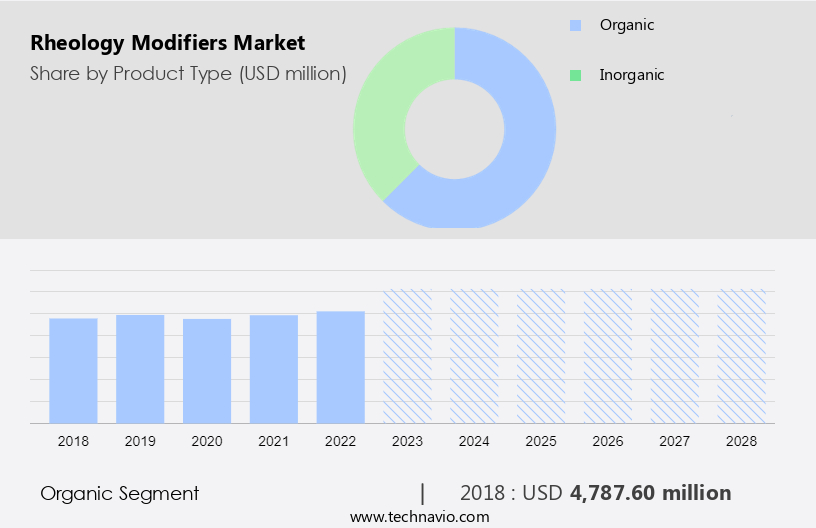

By Product Type Insights

The organic segment is estimated to witness significant growth during the forecast period. The market encompasses a wide range of additives used to manipulate the viscosity and flow characteristics of various industrial applications. Thickeners and viscosities, including inorganic matter like clays such as Bentonite, Hectorite, Organoclays, and Attapulgite, and organic matter like guar gum, xanthan gum, cellulose, and synthetic polymers such as polyamides, polyurethanes, alkali acrylics, and water-based or solvent-based systems, play a crucial role in this market. These rheology modifiers are extensively used in industries like agrochemicals, chemical manufacturing, adhesives, sealants, paints, dyes, drilling, extraction of oil, and mud industries. Additionally, they find significant applications in consumer products such as creams, lotions, shampoos, and personal care items.

In the housing transaction sector, rheology modifiers are used in plastics and electric vehicle markets to enhance their properties. Fumed silica is a commonly used rheology modifier in various industries due to its ability to improve the viscosity and flow properties of materials.

Get a glance at the market share of various segments Request Free Sample

The organic segment accounted for USD 4787.60 million in 2018 and showed a gradual increase during the forecast period.

Regional Insights

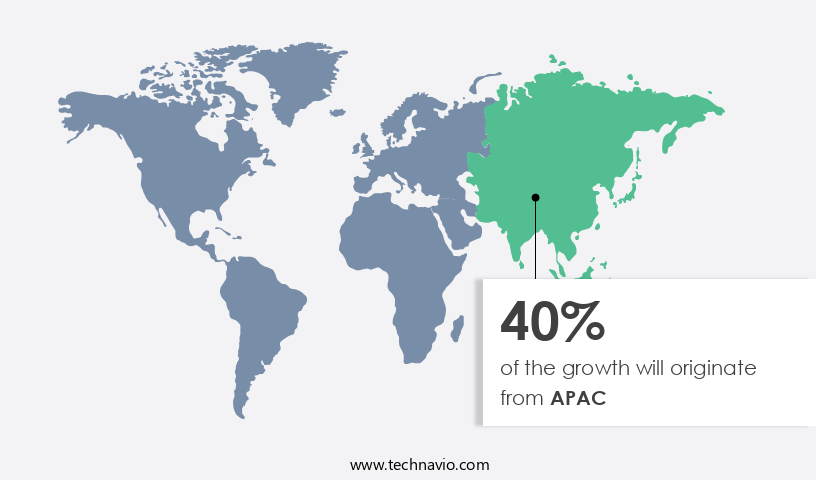

APAC is estimated to contribute 40% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market encompasses a wide range of thickeners, viscosifiers, and additives used to manipulate the viscosity and flow characteristics of various industries' products. Inorganic matter, such as clays like Bentonite, Hectorite, Organoclays, Attapulgite, and diatomaceous earth, as well as Fumed silica, serve as essential rheology modifiers. Organic matter, including Cellulose, Guar Gum, Xanthan Gum, Synthetic polymer, Polyamides, Polyurethanes, Alkali acrylics, and Water-based or Solvent-based systems, also plays a significant role. These modifiers find extensive applications in diverse sectors, including Agrochemical industries, Chemical industries, Adhesives, Sealants, Paints, Dyes, Drilling, Extraction of oil, Mud, Housing transactions, Plastics, and the Electric vehicle market.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Growing demand for efficient and high-performance additives in paint and coating industry is the key driver of the market. The market is witnessing significant growth due to the increasing demand for efficient and high-performance additives in various industries. In the paint and coating sector, there is a rising focus on sustainability and environmental regulations, leading to the development of low-volatile organic compound (VOC) coatings. These coatings require rheology modifiers to maintain the desired flow properties despite the reduced VOC content. For instance, the popularity of water-based coatings, which have a lower environmental impact than solvent-based coatings, is on the rise. Rheology modifiers are essential in various industries, including adhesives and sealants, cement and concrete, cleaners and disinfectants, coolants, rubber products, fermentation, lubricants and greases, and the agricultural and textiles industries, among others.

Some common types of rheology modifiers include Gellan gum, hydrogenated castor oil, powder, and granules. These additives function as leveling agents, pour point depressants, flow promoters/thinners, thickener/gelling agents, and thixotropic agents. In the electronics industry, rheology modifiers are used to improve the flow and leveling of electronic coatings, while in the water treatment industry, they help to optimize the rheological properties of water treatment chemicals.

Market Trends

Growing use of nanoparticles in rheology modifiers is the upcoming trend in the market. The market witnesses an ongoing trend toward the utilization of nanoparticles for enhancing the functionality of these additives. Rheology modifiers serve the purpose of enhancing the flow properties, stability, and overall performance of diverse materials. Nanoparticles, characterized by their dimensions in the nanometer range, offer distinct advantages due to their unique properties. One significant advantage of integrating nanoparticles into rheology modifiers is their ability to induce shear-thinning behavior. Shear-thinning is a phenomenon where a material's viscosity decreases under the influence of shear stress, thereby facilitating easier flow. Nanoparticles can be integrated into rheology modifiers to generate a network structure that disintegrates under shear stress, enabling improved flow characteristics.

Applications of rheology modifiers span across various industries, including Adhesives and Sealants, Cement and Concrete, Cleaners and Disinfectants, Coolants, Rubber products, Fermentation, Lubricants and greases, Agricultural Industry, Textiles Industry, and Electronics Industry. Incorporation of nanoparticles into rheology modifiers can lead to the production of Gellan gum, Hydrogenated Castor Oil, Powder, Granules, Leveling Agents, Pour Point Depressants, Flow Promoters/Thinners, Thickener/Gelling Agents, and Thixotropic Agents.

Market Challenge

Rise in shift from print to digital media is a key challenge affecting market growth. The market encompasses a range of additives used to modify the flow properties of various industrial applications. Key products in this market include Gellan gum, Hydrogenated Castor Oil, Powder, and Granules. These modifiers serve diverse functions such as Leveling Agents, Pour Point Depressants, Flow Promoters/Thinners, Thickener/Gelling Agents, and Thixotropic Agents. Industries utilizing rheology modifiers span from Adhesives and Sealants in construction, to Cement and Concrete, Cleaners and Disinfectants, Coolants, Rubber products, and Fermentation processes in the Food and Beverage Industry. Additionally, the market reaches industries such as Lubricants and greases in the Automotive Industry, Agricultural Industry, Textiles Industry, Electronics Industry, and Water treatment Industry.

The global demand for rheology modifiers is influenced by the technological advancements in these sectors, enabling the production of innovative and high-performance products. For instance, the Agricultural Industry benefits from the use of rheology modifiers in fertilizers and pesticides, while the Textiles Industry utilizes these additives to enhance the viscosity and texture of textile products. The Electronics Industry relies on rheology modifiers in the production of semiconductors and printed circuit boards, while the Water treatment Industry uses these additives to improve the performance and stability of water treatment chemicals. Overall, The market is experiencing significant growth due to the increasing demand for high-performance and cost-effective solutions in various industries.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

- Akzo Nobel NV: The company offers rheology modifiers such as AkzoNobel Dry Effects Rheology Modifier in 1 US Gallon amount.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Altana AG

- Archer Daniels Midland Co.

- Arkema SA

- Ashland Inc.

- BASF SE

- Berkshire Hathaway Inc.

- Cargill Inc.

- Clariant International Ltd.

- Croda International Plc

- Dow Inc.

- Eastman Chemical Co.

- Elementis Plc

- Evonik Industries AG

- Ingredion Inc.

- Kerry Group Plc

- Nouryon

- PPG Industries Inc.

- RPM International Inc.

- Solvay SA

- Tate and Lyle PLC

- The SNF Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a wide range of additives used to control the flow properties of various industrial applications. These additives play a crucial role in industries such as construction, cosmetics, personal care, household products, and more. In the construction sector, rheology modifiers are used as concrete admixtures and viscosity control additives for dams, roads, bridges, commercial buildings, and housing complexes. Bio-based rheology modifiers, derived from natural raw materials like plant extracts, polysaccharides, proteins, and synthetic polymers, are gaining popularity due to their eco-friendly nature. The organic segment of the market, which includes organic rheology modifiers, is expected to grow significantly due to the increasing demand for sustainable and biodegradable products.

Inorganic rheology modifiers, on the other hand, are widely used in industries such as paints & coatings, adhesives & sealants, inks, oil & gas, power generation, and waterborne systems. Synthetic rheology modifiers are also widely used due to their superior quality and ability to provide texture optimization. Rheology modifiers are also used in household products such as cleaners, detergents, and homecare sectors. In the cosmetics and personal care industry, rheology modifiers are used to improve the texture and consistency of various products, including creams, lotions, and gels. Overall, the market is expected to grow significantly due to the increasing demand for superior quality products in various industries.

The market is segmented into organic and inorganic rheology modifiers, and natural and synthetic rheology modifiers. The market is also segmented by application, including construction, household products, cosmetics personal care, paints & coatings, adhesives & sealants, home care, I&I products, inks, oil & gas, power generation, and others.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

200 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.2% |

|

Market growth 2024-2028 |

USD 1.39 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.06 |

|

Regional analysis |

APAC, Europe, North America, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 40% |

|

Key countries |

US, China, Germany, Japan, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Akzo Nobel NV, Altana AG, Archer Daniels Midland Co., Arkema SA, Ashland Inc., BASF SE, Berkshire Hathaway Inc., Cargill Inc., Clariant International Ltd., Croda International Plc, Dow Inc., Eastman Chemical Co., Elementis Plc, Evonik Industries AG, Ingredion Inc., Kerry Group Plc, Nouryon, PPG Industries Inc., RPM International Inc., Solvay SA, Tate and Lyle PLC, and The SNF Group |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -