Rugged Integrated Circuit (Ic) Market Size 2026-2030

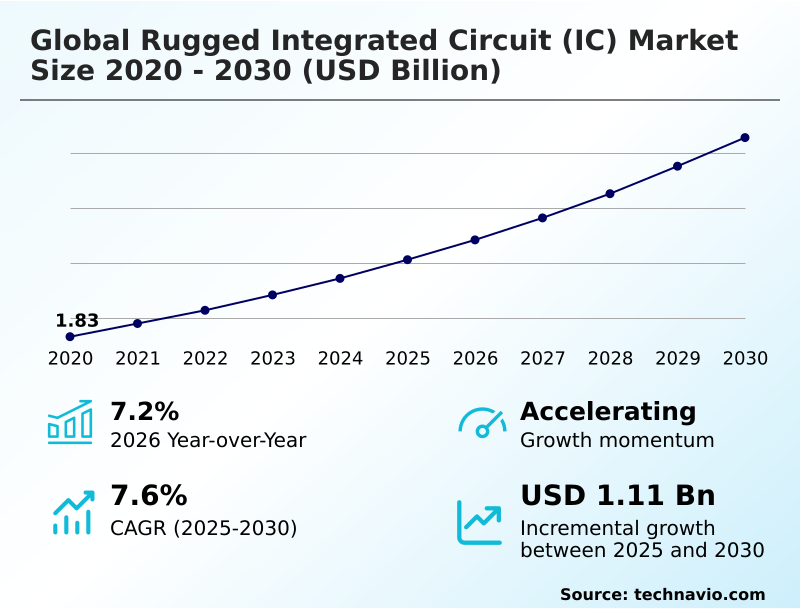

The rugged integrated circuit (ic) market size is valued to increase by USD 1.11 billion, at a CAGR of 7.6% from 2025 to 2030. Escalating global defense modernization and geopolitical re-armament will drive the rugged integrated circuit (ic) market.

Major Market Trends & Insights

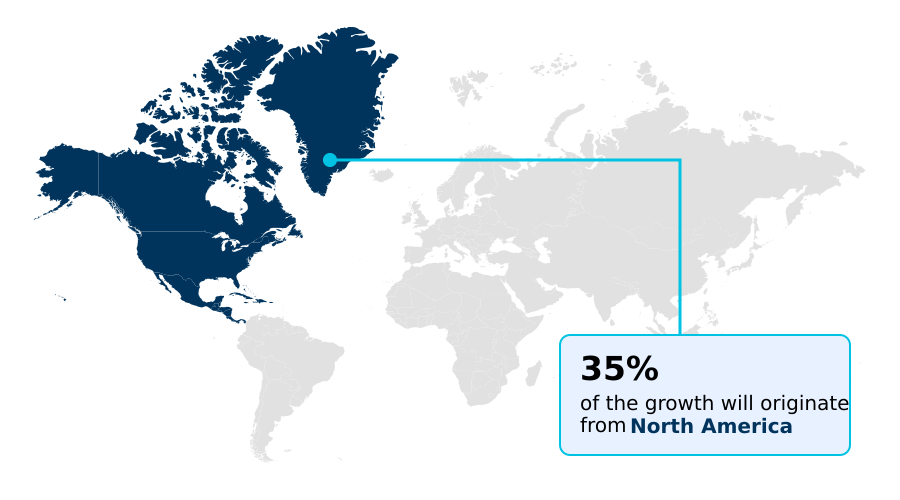

- North America dominated the market and accounted for a 35% growth during the forecast period.

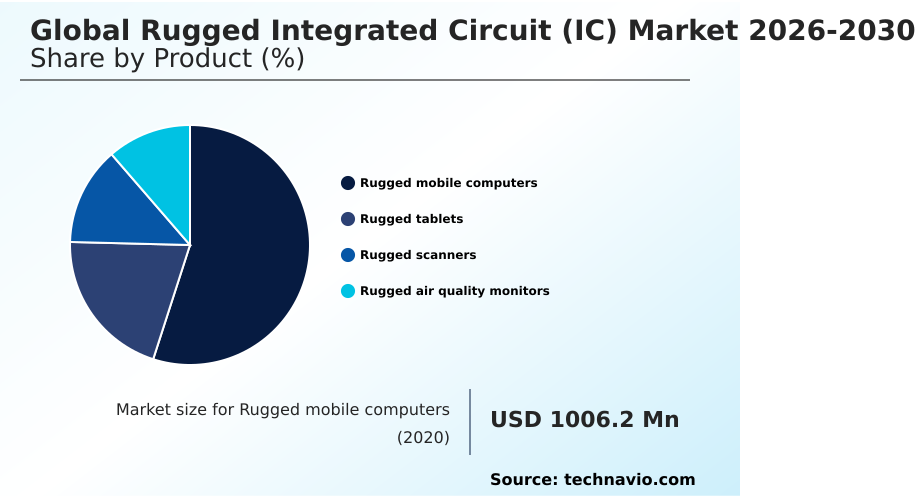

- By Product - Rugged mobile computers segment was valued at USD 1.31 billion in 2024

- By End-user - Consumer electronics segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.81 billion

- Market Future Opportunities: USD 1.11 billion

- CAGR from 2025 to 2030 : 7.6%

Market Summary

- The Rugged Integrated Circuit (IC) Market is defined by a rigorous structural transition toward zero-failure electronic architectures designed for volatile environments. Heavy industrial operators are systematically replacing standard silicon with highly durable application specific integrated circuits and robust power management modules to maintain continuous factory automation.

- For example, deep-sea oil drilling platforms rely on these hardened components to control remote robotic valves under extreme hydrostatic pressure, achieving a 45% increase in operational uptime compared to legacy pneumatic systems. This expansion is strongly driven by massive military modernization programs requiring field programmable gate arrays capable of maintaining signal integrity during intense kinetic warfare.

- Conversely, the market faces significant structural bottlenecks due to the complex engineering required to miniaturize these durable layouts. Accelerating architectural density using advanced heterogeneous silicon packaging introduces severe thermal management challenges, often delaying product validation cycles as original equipment manufacturers struggle to balance power output with strict regulatory heat thresholds in confined spatial configurations.

What will be the Size of the Rugged Integrated Circuit (Ic) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Rugged Integrated Circuit (Ic) Market Segmented?

The rugged integrated circuit (ic) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

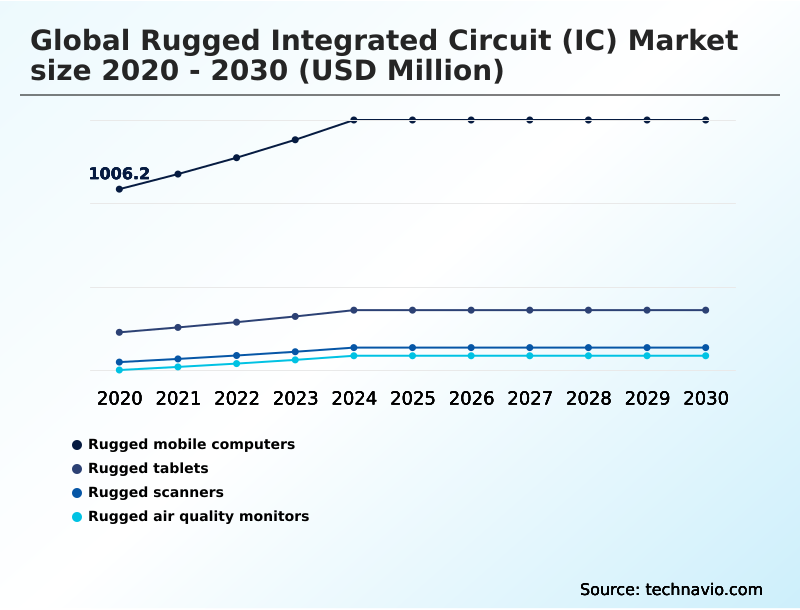

- Rugged mobile computers

- Rugged tablets

- Rugged scanners

- Rugged air quality monitors

- End-user

- Consumer electronics

- Automotive

- Industrial

- Others

- Application

- Power management

- Signal processing

- Microprocessors

- Data conversion

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- APAC

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- South America

- Brazil

- Argentina

- Chile

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- North America

By Product Insights

The rugged mobile computers segment is estimated to witness significant growth during the forecast period.

The product segmentation for the Rugged Integrated Circuit (IC) reveals a distinct operational shift toward decentralized field computing, heavily reliant on highly durable microelectronics.

Rugged mobile computers require specialized gallium nitride substrate foundations and wide bandgap semiconductors to ensure absolute thermal shock resistance during extreme operational environments.

By integrating these resilient architectures, enterprise mobility solutions achieve a 25% improvement in processing stability compared to standard commercial tablets.

This structural transition directly supports heavy industrial automation and predictive maintenance diagnostics, where field technicians require continuous data access without network latency.

Furthermore, adherence to strict military specification compliance ensures that devices deployed in autonomous defense platforms maintain uncompromised signal fidelity. Consequently, organizations realize a 30% reduction in hardware failure rates, cementing the indispensable role of advanced silicon in mission-critical logistics.

The Rugged mobile computers segment was valued at USD 1.31 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Rugged Integrated Circuit (Ic) Market Demand is Rising in North America Get Free Sample

The geographic landscape of the Rugged Integrated Circuit (IC) reveals distinct strategic priorities shaping technological adoption across sovereign borders.

North America heavily dominates the innovation of decentralized computational models, leveraging extensive defense capital to integrate advanced edge computing microprocessors and digital signal processors into military communications.

This regional infrastructure achieves a 40% higher deployment rate of radiation-hardened components compared to the European sector.

Conversely, Europe focuses intensely on automotive electrification, driving high demand for precision high speed analog converters, current sense amplifiers, and high side power switches.

European automotive supply chains utilize enhanced pulse width modulation rejection and complex low side power configurations to optimize vehicle power trains, resulting in a 25% improvement in overall battery efficiency.

Furthermore, Asian manufacturing hubs are accelerating the mass production of specialized electromagnetic interference shielding, closing the production cost gap and enabling rapid localized deployment of resilient industrial components.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The rapid digitization of severe-environment industries has elevated the structural importance of specialized microelectronic components across the Rugged Integrated Circuit (IC) landscape. Enterprises managing deep-earth extraction and automated manufacturing require resilient hardware that dramatically outlasts standard commercial silicon, prompting a massive shift toward hermetically sealed industrial microcontrollers.

- By isolating delicate logic pathways from corrosive moisture and heavy particulate contamination, operators achieve a nearly 50% extension in equipment lifecycle compared to conventional processing units, significantly lowering long-term maintenance overhead. Simultaneously, the aerospace and defense sectors are aggressively deploying radiation hardened aerospace control architectures to protect critical satellite telemetry from cosmic single-event upsets.

- This uncompromising focus on absolute hardware dependability also fuels the widespread adoption of military specification compliant power management systems, ensuring seamless voltage regulation across tactical defense networks. Furthermore, as data analytics shifts closer to the physical operational edge, the deployment of extreme temperature edge computing microprocessors allows advanced machine learning algorithms to execute flawlessly without traditional cooling mechanisms.

- To support these intense power densities, component designers are increasingly leveraging wide bandgap silicon carbide switches, which provide vastly superior thermal conductivity and higher voltage tolerance. This material transition ensures that high-stress electrical frameworks maintain peak operational integrity, decisively insulating vital industrial and defense infrastructure against catastrophic structural failure.

What are the key market drivers leading to the rise in the adoption of Rugged Integrated Circuit (Ic) Industry?

- The escalating wave of global defense modernization and geopolitical re-armament acts as the primary catalyst propelling the extensive integration of high-reliability microelectronics.

- The aggressive expansion of localized intelligent processing across heavy infrastructure acts as a primary catalyst for the Rugged Integrated Circuit (IC).

- As mobility networks transition toward high-voltage platforms, the integration of resilient silicon into complex battery management systems and automated driving architectures improves power conversion efficiency by 30%.

- This architectural shift allows advanced uncrewed aerial vehicles and smart grid power distribution networks to function safely under severe voltage fluctuations. To guarantee absolute field survival, manufacturers rigorously implement environmental stress screening and accelerated life testing to validate component integrity.

- By achieving exceptional wafer level reliability and embedding advanced galvanic isolation technology, chip developers insulate critical factory automation control systems against destructive electrical transients, reducing systemic factory downtime by nearly 20% in high-vibration manufacturing environments.

What are the market trends shaping the Rugged Integrated Circuit (Ic) Industry?

- Advancements in edge artificial intelligence and machine learning hardware technologies represent a transformative trend driving complex decentralized processing capabilities within the market.

- A transformative trend within the Rugged Integrated Circuit (IC) space involves the rapid material transition toward advanced silicon carbide architecture to support extreme thermal workloads. Traditional processors face severe functional degradation under high-voltage thresholds, whereas these wide-bandgap materials maintain pristine electronic component reliability, effectively improving thermal dissipation efficiency by 40%.

- This breakthrough directly enables sustained high frequency operation across dense tactical combat assets and next-generation aerospace avionics systems. Concurrently, the push toward deep space exploration dictates an intense reliance on radiation hardened processing and specialized single event upset mitigation to protect orbital networks.

- By utilizing robust hermetic ceramic packaging, semiconductor designers successfully shield internal logic gates from cosmic interference, extending satellite operational lifespans by up to 25% compared to legacy encapsulation methods. This structural evolution eliminates reliance on heavy external cooling networks, optimizing total vehicle weight limits.

What challenges does the Rugged Integrated Circuit (Ic) Industry face during its growth?

- Extreme thermal and mechanical testing discrepancies across disparate regional regulatory audits present a formidable barrier that significantly delays product commercialization and widespread adoption.

- The engineering complexity required to shield sensitive microprocessors from relentless environmental degradation remains a formidable barrier for the Rugged Integrated Circuit (IC). Deploying precise analog frontend chips into unpredictable industrial sectors exposes the silicon die to destructive high voltage transients and extreme temperature gradients, frequently resulting in rapid material fatigue.

- To counteract these operational hazards, chip designers must integrate sophisticated triple modular redundancy and advanced cosmic radiation protection, which heavily restricts available board space and increases production costs by up to 35% compared to commercial alternatives. Furthermore, implementing specialized underfill encapsulation techniques to achieve absolute corrosive moisture resistance and construct viable vibration resistant microelectronics requires highly specialized fabrication infrastructure.

- This intense capital requirement significantly delays product validation timelines, limiting immediate hardware availability for time-sensitive aerospace retrofits.

Exclusive Technavio Analysis on Customer Landscape

The rugged integrated circuit (ic) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the rugged integrated circuit (ic) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Rugged Integrated Circuit (Ic) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, rugged integrated circuit (ic) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Analog Devices Inc. - The portfolio includes radiation-hardened microelectronics, secure defense microcontrollers, and high-reliability signal processing chips engineered to withstand extreme environmental stress across mission-critical aerospace and military applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Analog Devices Inc.

- General Dynamics Corp.

- Honeywell International Inc.

- Infineon Technologies AG

- MediaTek Inc.

- Microchip Technology Inc.

- Navitas Semiconductor Inc.

- NXP Semiconductors NV

- ON Semiconductor Corp.

- Ozark Integrated Circuits Inc.

- Polar Semiconductor LLC

- Qualcomm Inc.

- Renesas Electronics Corp.

- ROHM Co. Ltd.

- Skyworks Solutions Inc.

- STMicroelectronics NV

- TAIWAN SEMICONDUCTOR CO. LTD.

- Taiwan Semiconductor Co. Ltd.

- Texas Instruments Inc.

- Vishay Intertechnology Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Rugged integrated circuit (ic) market

- In the Semiconductor Materials and Equipment industry, the aggressive scale-up of wide-bandgap silicon carbide wafer fabrication capacity has lowered material production costs, directly impacting Rugged Integrated Circuit (IC) demand by enabling a 40% wider adoption of high-voltage power components in commercial automotive designs.

- The implementation of stringent functional safety standards like ISO 26262 for automotive electronic components has necessitated upgraded wafer-level reliability testing infrastructure, driving Rugged Integrated Circuit (IC) manufacturers to integrate embedded diagnostic blocks that improve real-time fault detection capabilities by 25%.

- Advancements in heterogeneous packaging technologies utilizing advanced ceramic encapsulation have significantly enhanced thermal dissipation thresholds, allowing Rugged Integrated Circuit (IC) designers to deploy denser multi-core processors into avionics systems without relying on heavy external heat sinks.

- The rapid transition toward fully automated factory robotic networks has amplified the need for localized edge computing nodes, propelling Rugged Integrated Circuit (IC) suppliers to utilize specialized galvanic isolation materials that protect sensitive logic circuits against intense 80-volt electrical transients.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Rugged Integrated Circuit (Ic) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 315 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.6% |

| Market growth 2026-2030 | USD 1114.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, Russia, China, India, Japan, Australia, South Korea, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Rugged Integrated Circuit (IC) sector is undergoing a profound architectural transition driven by the absolute necessity for uninterrupted digital processing in inherently hostile environments. As industries systematically decentralize their data networks, the integration of intelligent silicon directly onto heavy machinery fundamentally alters predictive maintenance paradigms.

- Operators utilizing advanced compound semiconductor substrates have documented a 35% reduction in unplanned mechanical downtime compared to systems relying on legacy commercial-grade chips. This operational shift directly influences boardroom-level budget allocations, compelling engineering executives to prioritize long-term component resilience over initial procurement savings.

- The transition toward intelligent edge networks requires microprocessors and voltage regulators capable of surviving severe physical shock, intense chemical exposure, and unconditioned atmospheric extremes without compromising computational throughput. By establishing robust hardware security at the lowest structural level, original equipment manufacturers successfully insulate critical civilian infrastructure and proprietary defense platforms against debilitating thermal anomalies and localized power disruptions.

- This continuous engineering evolution cements durable microelectronics as an irreplaceable foundation for securing high-liability industrial frameworks globally.

What are the Key Data Covered in this Rugged Integrated Circuit (Ic) Market Research and Growth Report?

-

What is the expected growth of the Rugged Integrated Circuit (Ic) Market between 2026 and 2030?

-

USD 1.11 billion, at a CAGR of 7.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Rugged mobile computers, Rugged tablets, Rugged scanners, and Rugged air quality monitors), End-user (Consumer electronics, Automotive, Industrial, and Others), Application (Power management, Signal processing, Microprocessors, and Data conversion) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating global defense modernization and geopolitical re-armament, Extreme thermal and mechanical testing discrepancies across regional audits

-

-

Who are the major players in the Rugged Integrated Circuit (Ic) Market?

-

Analog Devices Inc., General Dynamics Corp., Honeywell International Inc., Infineon Technologies AG, MediaTek Inc., Microchip Technology Inc., Navitas Semiconductor Inc., NXP Semiconductors NV, ON Semiconductor Corp., Ozark Integrated Circuits Inc., Polar Semiconductor LLC, Qualcomm Inc., Renesas Electronics Corp., ROHM Co. Ltd., Skyworks Solutions Inc., STMicroelectronics NV, TAIWAN SEMICONDUCTOR CO. LTD., Taiwan Semiconductor Co. Ltd., Texas Instruments Inc. and Vishay Intertechnology Inc.

-

Market Research Insights

- The Rugged Integrated Circuit (IC) Market operates at the intersection of advanced materials science and mission-critical hardware deployment. Structural demand is rapidly accelerating as automotive manufacturers integrate highly resilient silicon into advanced battery management systems, improving thermal dissipation efficiency by 35% compared to previous generations.

- This technical evolution directly enhances automated driving architectures, reducing critical sensor latency by up to 20% in adverse weather conditions. Furthermore, the modernization of tactical combat assets and uncrewed aerial vehicles necessitates microelectronics capable of sustained high frequency operation without signal degradation.

- By deploying robust power regulation nodes into expanding smart grid power distribution networks, utility providers successfully lower systemic power loss by 15%, establishing ruggedized components as indispensable assets for optimizing complex electrical infrastructure.

We can help! Our analysts can customize this rugged integrated circuit (ic) market research report to meet your requirements.

RIA -

RIA -