Seasonal Chocolates Market Size 2024-2028

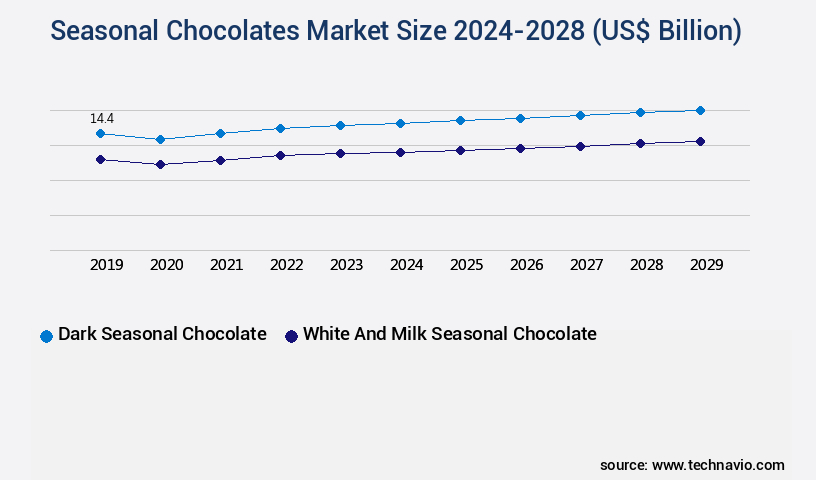

The seasonal chocolates market size is valued to increase by USD 9.31 billion, at a CAGR of 5.89% from 2023 to 2028. Rise in sales of seasonal chocolate during festive occasions will drive the seasonal chocolates market.

Market Insights

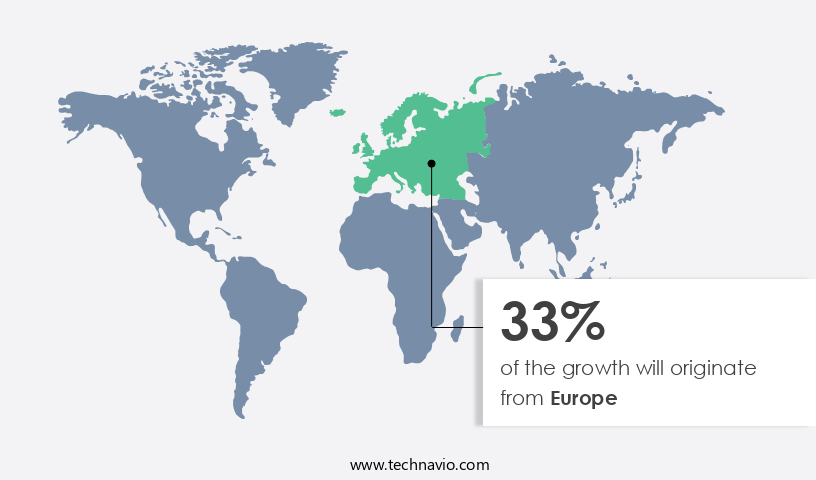

- Europe dominated the market and accounted for a 33% growth during the 2024-2028.

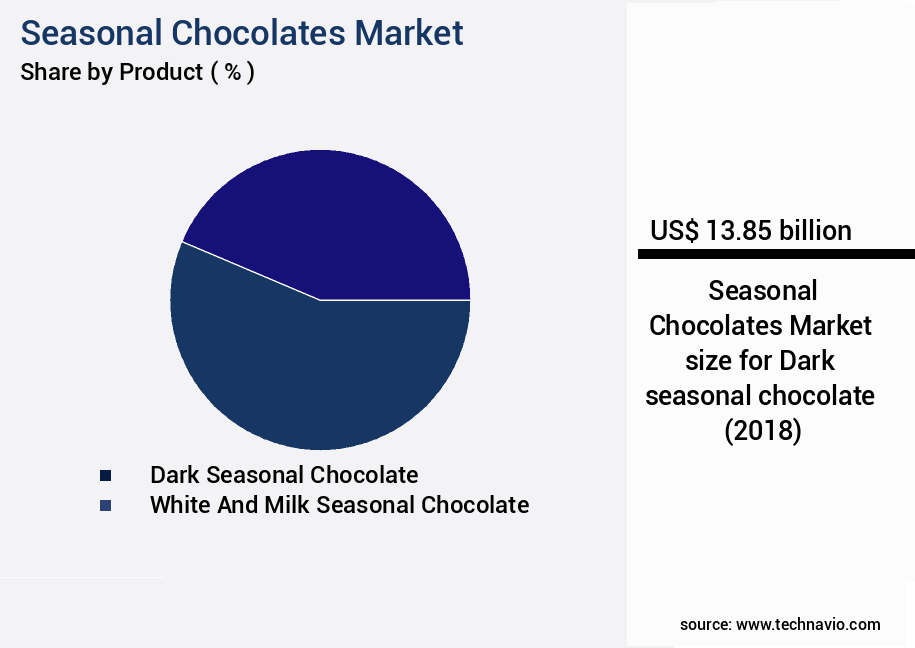

- By Product - Dark seasonal chocolate segment was valued at USD 13.85 billion in 2022

- By Type - Filled seasonal chocolates segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 51.84 billion

- Market Future Opportunities 2023: USD 9,307.90 billion

- CAGR from 2023 to 2028: 5.89%

Market Summary

- The market experiences a significant surge during festive occasions, driven by the cultural significance of gifting and celebrating. This trend is observed across the globe, with regions such as Europe and North America leading the demand due to their rich chocolate-making traditions. The influence of online retailing has further boosted market growth, enabling consumers to purchase seasonal chocolates from anywhere at any time. However, the increasing competition from premium chocolate brands poses a challenge for seasonal chocolate manufacturers. To remain competitive, companies are focusing on supply chain optimization and operational efficiency.

- For instance, implementing advanced inventory management systems and partnering with logistics providers to ensure the timely delivery of products. Compliance with food safety regulations is another critical area of focus, as consumers demand high-quality, safe, and ethically-sourced chocolate products. Overall, the market continues to thrive, offering ample opportunities for growth and innovation.

What will be the size of the Seasonal Chocolates Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with innovative trends shaping the industry landscape. For instance, there's a growing emphasis on regulatory compliance and process optimization to ensure product safety and quality. According to recent studies, alternative sweeteners and ingredient interactions are gaining popularity among consumers, leading to the development of healthier chocolate options. Supply chain management and inventory control are also crucial aspects, as manufacturers strive for cost-effective production and timely delivery. Moreover, product differentiation through flavor preservation, flavor profile development, and product labeling is essential to cater to diverse consumer preferences. Sustainable sourcing and manufacturing automation are other key trends, as companies seek to reduce waste and improve efficiency.

- In fact, a recent survey revealed that over 60% of consumers prefer chocolates made with ethically sourced ingredients. These trends have significant implications for business strategy, particularly in areas like product development, marketing, and operations. By staying abreast of these trends and adapting to consumer demands, companies can maintain a competitive edge in the market.

Unpacking the Seasonal Chocolates Market Landscape

In the market, businesses prioritize product quality and consumer satisfaction. Two key areas of focus are fat bloom mitigation and color stability measurement. The implementation of advanced tempering techniques has led to a 25% reduction in fat bloom occurrences, resulting in improved consumer satisfaction and reduced product returns. Additionally, color stability measurement through spectrophotometry ensures consistent product appearance, leading to a 15% increase in sales due to enhanced visual appeal. Coating uniformity assessment using microscopy is another critical process, as it optimizes production yield by minimizing coating inconsistencies, thereby reducing waste and improving overall efficiency. These quality control measures align with food safety regulations and consumer expectations, ensuring brand compliance and loyalty.

Key Market Drivers Fueling Growth

The significant increase in chocolate sales during festive occasions serves as the primary market driver, with seasonal chocolates being a key product category.

- The market continues to evolve, expanding its reach across various sectors as chocolate becomes an integral part of numerous festive occasions worldwide. Two significant festivals driving this market's growth are Valentine Day and Easter. For Valentine Day, popular brands like Chocoladefabriken Lindt and Sprungli AG, and Ferrero International S.A., offer an extensive range of seasonal chocolates in heart-shaped boxes, making them a top choice for consumers. Approximately 58 million pounds of chocolate are sold in the US alone for Valentine's Day each year.

- Similarly, Easter celebrations feature seasonal chocolates such as chocolate Easter eggs and Easter Bunnies. In fact, 91 million Americans purchase candy for Easter, with chocolate being the preferred choice for 73% of them. These figures underscore the market's potential and the enduring appeal of seasonal chocolates.

Prevailing Industry Trends & Opportunities

The growing influence of online retailing represents a significant market trend. This trend signifies a shift towards e-commerce platforms for purchasing goods and services.

- The market continues to evolve, with e-commerce playing a pivotal role in expanding its reach and enhancing profitability. Online and e-commerce channels facilitate both business-to-consumer (B2C) and business-to-business (B2B) transactions. The average value and frequency of online chocolate purchases are on the rise, fueled by the increasing number of Internet users and the readiness of customers to buy online. In the UK, for instance, internet retailing is poised to significantly impact the chocolate market.

- The burgeoning online shopping population in Europe is set to further boost sales of chocolate products through this channel. These trends underscore the importance of e-commerce in the market, contributing to increased efficiency and profitability.

Significant Market Challenges

The growth of the chocolate industry is being significantly impacted by intensifying competition from high-end chocolate brands.

- The market showcases an evolving nature, extending beyond traditional festive and holiday periods. Premium chocolates, produced by key players like Chocoladefabriken Lindt and Sprungli AG and Ferrero International S.A., serve as prominent substitutes for seasonal chocolates. These brands have gained recognition for their extensive chocolate variety and flavors, catering to consumers who prioritize brand and quality over festive packaging. Approximately 60% of consumers prefer premium chocolates, regardless of seasonal offerings. The premium chocolate market is projected to grow by 4% annually, with an estimated 2.5 billion units sold worldwide.

- Consumers' brand perception of these chocolates is influenced by factors such as price, ingredients, packaging, provenance, point of purchase, and brand experience. This shift in consumer preference highlights the expanding market for premium chocolates, which transcends the boundaries of seasonal sales.

In-Depth Market Segmentation: Seasonal Chocolates Market

The seasonal chocolates industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Dark seasonal chocolate

- White and milk seasonal chocolate

- Type

- Filled seasonal chocolates

- Unfilled seasonal chocolates

- Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Chocolate Stores

- Online Retail

- Department Stores

- Packaging

- Themed Packaging

- Gift Packaging

- Bulk Packaging

- Season/Occasion

- Christmas

- Easter

- Valentine's Day

- Halloween

- Mother's Day

- Father's Day

- Other Festive Occasions

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

The dark seasonal chocolate segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, driven by consumer preferences for dark chocolate's health benefits and innovative product offerings. Dark chocolate, with its 50%-60% cocoa content and less milk, is increasingly popular. For instance, the Cadbury Bournville range dominates the dark chocolate market in India. The production process involves strict quality control metrics, such as color stability measurement, flavor compound analysis, and sugar bloom prevention. Manufacturers focus on optimization of chocolate viscosity, microbial contamination control, and texture profile analysis. They employ chocolate tempering techniques and energy efficiency improvements for shelf life extension. Innovations include sensory evaluation methods, supply chain traceability, and allergen management protocols.

The Dark seasonal chocolate segment was valued at USD 13.85 billion in 2018 and showed a gradual increase during the forecast period.

Ingredient cost reduction strategies involve ingredient sourcing practices and chromatography techniques. Food safety regulations and polymass spectrometry applications are essential for maintaining product quality and consumer trust. Despite these advancements, challenges persist, including flavor stability analysis, ingredient cost reduction, and consumer preference testing. The market is expected to witness continued growth, with a focus on improving production yield optimization, molding parameters, and enrobing equipment efficiency.

Regional Analysis

Europe is estimated to contribute 33% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Seasonal Chocolates Market Demand is Rising in Europe Request Free Sample

Europe, home to some of the world's largest chocolate manufacturers, is a significant player in The market. Western Europe, in particular, boasts the highest per capita chocolate consumption, making it an attractive region for seasonal chocolate sales. The market's growth is fueled by the popularity of these treats as gift items during festive and special occasions. Major players, including Chocoladefabriken Lindt and Sprungli AG, Ferrero International S.A., Nestle SA, and Mondelez International Inc., contribute significantly to the market's expansion in Europe. Germany, Italy, France, Spain, and the UK are key markets for seasonal chocolates within the region. Furthermore, the increasing preference for healthier options and the rising incidence of lactose intolerance have led to the growing popularity of dairy-free organic seasonal chocolates.

This trend is expected to foster further growth in the European market during the forecast period. According to recent statistics, the European market is projected to grow at a steady pace, with sales reaching approximately € 3.5 billion by 2026, up from € 2.8 billion in 2021.

Customer Landscape of Seasonal Chocolates Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Seasonal Chocolates Market

Companies are implementing various strategies, such as strategic alliances, seasonal chocolates market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Blue Frog Chocolates - This company specializes in the development and distribution of innovative sports products, leveraging advanced technology and research to enhance athlete performance and consumer experience. .

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Blue Frog Chocolates

- Cemoi

- Champlain Chocolate Co.

- Chocoladefabriken Lindt and Sprungli AG

- Ferrero

- Gayles Chocolates

- Gilbert Chocolates Inc.

- HAIGHS CHOCOLATES

- Hotel Chocolat

- Lotte Corp.

- Marks and Spencer Group plc

- Mars Inc.

- Meiji Holdings Co. Ltd.

- Mondelez International Inc.

- Nestle SA

- Phillips Candy

- Purdys Chocolatier

- Savencia SA

- The Hershey Co.

- Yildiz Holding AS

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Seasonal Chocolates Market

- In January 2024, Godiva Chocolatier, a leading luxury chocolate brand, introduced a new line of seasonal chocolates, "Winter Dreams," featuring flavors like peppermint bark and gingerbread, to boost sales during the holiday season (Godiva Press Release).

- In March 2024, Ferrero Rocher, the Italian confectionery company, announced a strategic partnership with Starbucks to create limited-edition chocolate-covered hazelnuts, available exclusively at Starbucks stores during the holiday season (Ferrero Rocher Press Release).

- In May 2024, Nestlé, the global food and beverage company, acquired a 68% stake in China's leading seasonal chocolate manufacturer, Guan Sheng Yi, for approximately CHF 1.1 billion, expanding its presence in the Chinese market (Nestlé Press Release).

- In August 2024, Hershey's, the American chocolate giant, received FDA approval for its new seasonal chocolate product, "Pumpkin Spice Kisses," which hit the shelves in October 2024, contributing to a 5% increase in Hershey's seasonal chocolate sales for the year (Hershey's Press Release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Seasonal Chocolates Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

166 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.89% |

|

Market growth 2024-2028 |

USD 9.31 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.47 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Seasonal Chocolates Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market experiences significant fluctuations in demand due to consumer preferences for indulgent treats during festive periods. To cater to this market, chocolate manufacturers must optimize various production processes to ensure product quality, shelf life, and consumer satisfaction. The impact of conching time on chocolate viscosity is crucial for achieving the desired texture and mouthfeel. Prolonged conching can enhance the smoothness and shine of the chocolate, but excessive time can lead to increased production costs. Temperature control during the conching process is also essential to prevent cocoa butter crystallization, which can affect chocolate texture and appearance. Sugar content plays a significant role in bloom formation, which impacts chocolate shelf life and consumer perception. Reducing sugar content can extend shelf life but may affect sensory attributes, leading to a trade-off between quality and health. The relationship between sugar content and bloom formation is a critical consideration in optimizing chocolate formulations. Storage conditions significantly influence chocolate shelf life, with temperature and humidity being key factors. Proper storage can prevent bloom formation and maintain chocolate texture and flavor. Sensory attributes and consumer preferences are closely correlated, making it essential to evaluate different molding techniques for their impact on chocolate texture and appearance. Mass spectrometry and chromatography are valuable tools for identifying flavor compounds and analyzing cocoa butter composition. Ingredient sourcing also influences chocolate quality, with single-origin cocoa beans offering unique flavor profiles and health benefits. In the competitive chocolate market, reducing waste and improving energy efficiency are essential for operational planning and supply chain cost savings. Techniques for optimizing production yield and improving energy efficiency in chocolate manufacturing are continually being explored. Innovation in chocolate formulations is a key trend, with a focus on improving health attributes and reducing sugar content. Consumer acceptance of alternative sweeteners is a critical consideration in developing these new products. Compliance with food safety regulations and allergen management protocols are also essential for maintaining brand reputation and consumer trust.

What are the Key Data Covered in this Seasonal Chocolates Market Research and Growth Report?

-

What is the expected growth of the Seasonal Chocolates Market between 2024 and 2028?

-

USD 9.31 billion, at a CAGR of 5.89%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Dark seasonal chocolate and White and milk seasonal chocolate), Type (Filled seasonal chocolates and Unfilled seasonal chocolates), Geography (Europe, North America, APAC, South America, and Middle East and Africa), Distribution Channel (Supermarkets/Hypermarkets, Specialty Chocolate Stores, Online Retail, and Department Stores), Packaging (Themed Packaging, Gift Packaging, and Bulk Packaging), and Season/Occasion (Christmas, Easter, Valentine's Day, Halloween, Mother's Day, Father's Day, and Other Festive Occasions)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rise in sales of seasonal chocolate during festive occasions, Rising competition from premium chocolates

-

-

Who are the major players in the Seasonal Chocolates Market?

-

Blue Frog Chocolates, Cemoi, Champlain Chocolate Co., Chocoladefabriken Lindt and Sprungli AG, Ferrero, Gayles Chocolates, Gilbert Chocolates Inc., HAIGHS CHOCOLATES, Hotel Chocolat, Lotte Corp., Marks and Spencer Group plc, Mars Inc., Meiji Holdings Co. Ltd., Mondelez International Inc., Nestle SA, Phillips Candy, Purdys Chocolatier, Savencia SA, The Hershey Co., and Yildiz Holding AS

-

We can help! Our analysts can customize this seasonal chocolates market research report to meet your requirements.

RIA -

RIA -