Severe Duty Motors Market Size 2024-2028

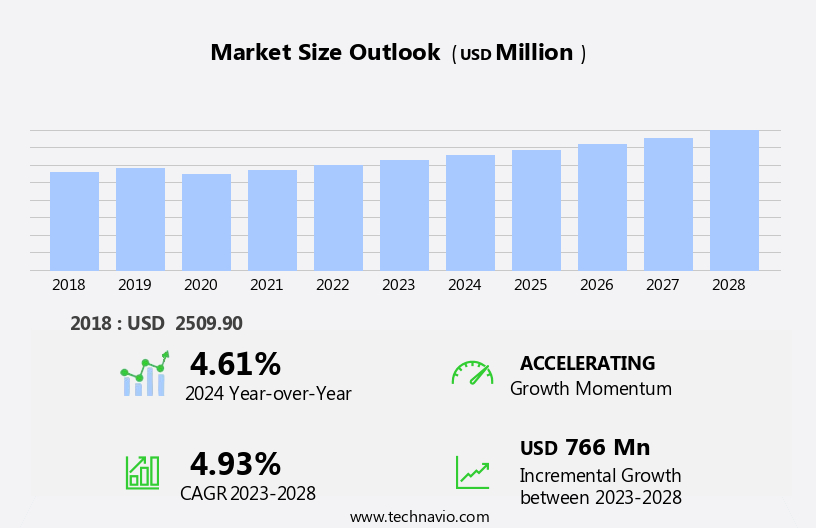

The severe duty motors market size is forecast to increase by USD 766 million, at a CAGR of 4.93% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing demand for energy-efficient motor solutions. This trend is driven by stringent energy regulations and the rising awareness of energy savings among industries. Additionally, the market is witnessing an uptick in upgrades of existing severe duty motors to more efficient models, further fueling market growth. Severe duty motors, including those used in pumps and compressors, also experience significant demand in various industries such as salt production, pulp and paper, and waste management. However, the market faces challenges as well. The gray market poses a significant threat with its offerings of low-quality and cheaper products, which can negatively impact the reputation and sales of legitimate market players.

- Companies in the market must focus on offering high-quality, reliable, and energy-efficient products to differentiate themselves from the competition and maintain customer loyalty. To capitalize on the growth opportunities and navigate the challenges effectively, market participants should closely monitor regulatory developments, invest in research and development, and adopt effective marketing strategies to reach their target audience.

What will be the Size of the Severe Duty Motors Market during the forecast period?

The market is characterized by its continuous evolution and dynamic nature, with various sectors relying on these motors for their heavy-duty applications. Permanent magnet motors, low-speed motors, high-torque motors, and synchronous motors, among others, are integral components in industries such as oil and gas, material handling, and construction equipment. The demand for these motors is driven by the need for high power density, efficiency, and durability in harsh operating conditions. Motor performance is a critical factor, with considerations including torque output, operating life, temperature resistance, and vibration resistance. In the oil and gas sector, severe duty motors are essential for powering drilling equipment and production facilities.

In material handling applications, these motors are used to move heavy loads, requiring high torque and shock resistance. In construction equipment, they provide the power needed for excavation, crushing, and pumping applications. Motor diagnostics, repair, and maintenance are crucial aspects of ensuring optimal performance and longevity. Motor selection, sizing, and commissioning are also essential steps in the process, with various IP ratings and efficiency ratings playing a role in determining the best fit for specific applications. Variable speed drives and motor control systems are increasingly being used to improve motor performance and energy efficiency. Custom motor designs and brushless motors offer solutions for specific applications, while motor protection systems ensure the safety and reliability of the overall system.

The mining machinery and power generation industries also rely on severe duty motors for their heavy-duty applications. Corrosion resistance and power density are critical factors in these industries, where motors are subjected to extreme conditions and high loads. The market is a complex and evolving landscape, with ongoing research and development efforts focused on improving motor performance, efficiency, and durability. Motor testing and maintenance requirements are essential components of ensuring the longevity and reliability of these critical components.

How is this Severe Duty Motors Industry segmented?

The severe duty motors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

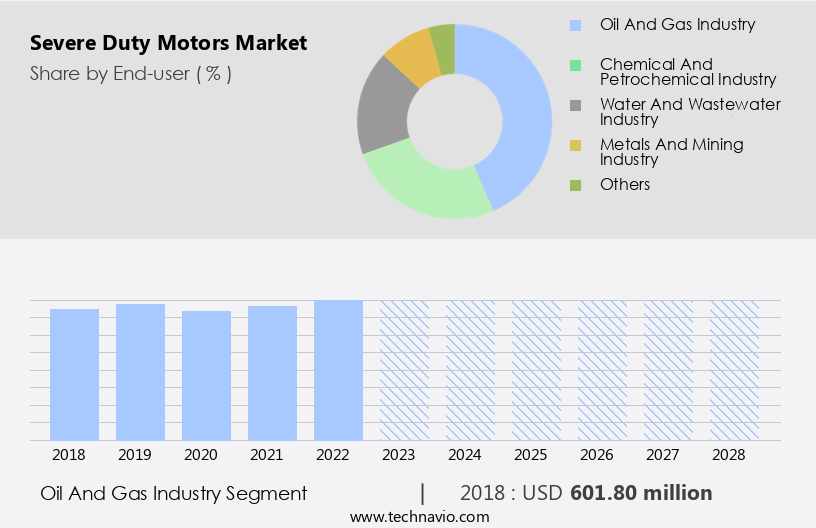

- End-user

- Oil and gas industry

- Chemical and petrochemical industry

- Water and wastewater industry

- Metals and mining industry

- Others

- Geography

- North America

- US

- Europe

- Germany

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By End-user Insights

The oil and gas industry segment is estimated to witness significant growth during the forecast period.

Severe duty motors cater to the unique demands of various industries, particularly oil and gas. These motors, with their robust design, are integral to the operation of oil rigs and refineries. In the oil and gas sector, severe duty motors power essential equipment such as cat crackers, sulfur recovery units, distillers, cooling facilities, water treatment systems, alkylation units, and reformers. Beyond production and refining, these motors are also extensively used in oil rig pumping applications. Permanent magnet motors, low-speed motors, high-torque motors, and synchronous motors are commonly used in severe duty applications. These motors are engineered to withstand harsh environments, offering shock resistance, temperature resistance, and vibration resistance.

Motor diagnostics and troubleshooting are crucial for maintaining optimal motor performance and extending their operating life. Heavy-duty applications, material handling, and power generation further expand the market for severe duty motors. Motor selection, sizing, and replacement are essential considerations for industries that rely on these motors. Variable speed drives and motor control systems enable efficient speed control and motor maintenance. Induction motors, custom motor designs, and brushless motors also find applications in severe duty environments. Hydraulic motors and pneumatic motors provide additional power transmission options. Motor protection systems ensure the safety and longevity of severe duty motors.

Mining machinery, construction equipment, off-highway vehicles, and power generation equipment are among the industries that benefit from severe duty motors. Energy efficiency and corrosion resistance are essential factors in the design and implementation of these motors. Motor commissioning and installation are crucial for ensuring optimal performance and reliability.

The Oil and gas industry segment was valued at USD 601.80 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

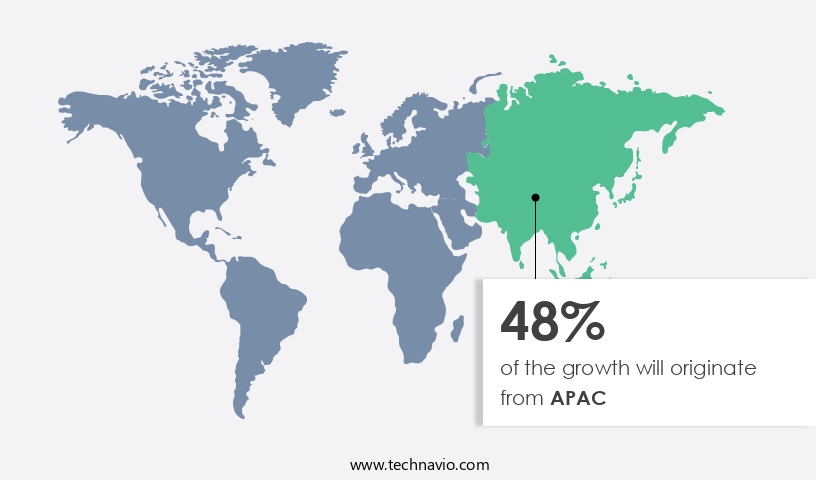

APAC is estimated to contribute 48% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

Severe duty motors, including those with NEMA ratings, permanent magnet motors, low-speed motors, high-torque motors, and synchronous motors, are in high demand across various industries. In the APAC region, heavy-duty applications, such as material handling, construction equipment, mining machinery, and power generation, are driving the market's growth. China and India are leading markets due to increasing industrialization and rising population, with improving per capita income. The oil and gas industry in APAC is also expanding, fueling the demand for severe duty motors in the region. Motor repair, motor diagnostics, and motor maintenance are essential services to ensure optimal motor performance.

Electric motors, including induction motors and brushless motors, as well as pneumatic motors, are commonly used. Motor selection, motor sizing, and motor installation are crucial aspects of motor implementation. Motor control systems, speed control, and variable speed drives are integral to efficient motor operation. Heavy-duty motors require high power density, temperature resistance, vibration resistance, and shock resistance to withstand harsh operating conditions. Motor protection systems are essential to prevent damage and ensure longevity. Motor efficiency ratings, maintenance requirements, and energy efficiency are critical factors in motor choice. Custom motor designs cater to specific application needs. The market is dynamic, with continuous innovation in motor technology and evolving industry demands.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Severe Duty Motors Industry?

- The increasing demand for energy-efficient severe duty motors serves as the primary market driver.

- The market is experiencing significant growth due to the increasing demand for high-efficiency motors in various end-user industries. These industries, including food and beverages, power, oil and gas, and chemical and petrochemicals, are striving to enhance their production capabilities to meet the rising global demand. Severe duty motors are an ideal solution, as they offer improved energy savings through high-speed performance. Moreover, the increasing energy consumption worldwide, coupled with the high cost of electricity, has compelled end-users to prioritize energy efficiency measures. Motor selection and sizing are critical factors in motor efficiency, and motor testing, speed control, and motor maintenance play essential roles in ensuring motor performance.

- Motor control systems, including IP ratings, are also vital for ensuring motor durability and protection against environmental conditions. Hydraulic motors, with their high power density, are increasingly popular in heavy-duty applications. Efficiency ratings are a significant consideration in motor selection, as they directly impact energy consumption and cost savings. The market is poised for continued growth as end-users seek to optimize energy usage and reduce operational costs.

What are the market trends shaping the Severe Duty Motors Industry?

- The trend in the severe duty motor market is shifting towards more frequent upgrades. This requirement for enhanced motor performance is becoming increasingly prominent.

- Severe duty motors are a robust solution for industries operating in challenging environments. These motors, which are modifications of standard TEFC motors, are characterized by their heavier construction and enhanced features. The demand for severe duty motors is on the rise due to their ability to deliver superior performance and operational benefits in harsh industrial conditions. Industries such as power generation, mining, and off-highway vehicles are increasingly adopting severe duty motors for their applications. These motors offer advantages like cooler operation, increased efficiency, corrosion resistance, and improved motor protection systems. The benefits of upgrading to severe duty motors are significant, leading industries to prioritize such upgrades.

- To identify the opportunity to upgrade to severe duty motors, industries can conduct an evaluation of their existing motor base. This evaluation will help identify the motors that can be upgraded to severe duty motors based on their application requirements and operating conditions. Severe duty motors come in various designs, including induction motors and brushless motors, catering to different industry needs. The custom motor designs offer tailored solutions for specific applications, ensuring optimal performance and reliability. Severe duty motors are a strategic investment for industries operating in harsh environments. Their rugged construction, enhanced features, and operational benefits make them an attractive alternative to conventional motors.

- By conducting an evaluation of their existing motor base, industries can identify the motors that can be upgraded to severe duty motors, thereby improving their overall operational efficiency and productivity.

What challenges does the Severe Duty Motors Industry face during its growth?

- The gray market poses a significant challenge to the industry's growth by providing lower-quality and cheaper products. This issue undermines the reputation of legitimate businesses and can result in decreased consumer trust and loyalty. Moreover, the sale of unauthorized goods can lead to intellectual property infringement and potential safety hazards, further complicating the situation. Consequently, addressing the gray market and ensuring the authenticity and quality of products remains a crucial priority for industry players.

- The market is experiencing significant growth due to the attractive investment environment in Asian countries. End-users in the region are prioritizing power-efficient machinery and solutions, leading to increased demand for severe duty motors. Price sensitivity from customers has driven motor companies to form relationships with cost-effective subcomponent suppliers. In recent years, low-cost imports from Asian manufacturers, including China, have flooded the American and European markets.

- The availability of low-cost labor and abundant resources in Asia enables these companies to manufacture severe duty motors at lower prices compared to their counterparts in other regions. This price advantage has made Asian manufacturers major players in The market.

Exclusive Customer Landscape

The severe duty motors market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the severe duty motors market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, severe duty motors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - In industrial processing environments, severe duty motors are essential for delivering robust performance and extended lifespan.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Bharat Bijlee Ltd

- Brook Crompton UK Ltd.

- Crompton Greaves Consumer Electricals Ltd.

- Elektrim Motors

- Havells India Ltd.

- Kirloskar Electric Co. Ltd.

- MGM Electric Motors

- Mitsubishi Electric Corp.

- Nidec Corp.

- Regal Rexnord Corp.

- Rockwell Automation Inc.

- Siemens AG

- Toledo Engineering Co. Inc.

- Toshiba Corp.

- WEG S.A

- Wolong Electric Group Co. Ltd.

- WorldWide Electric Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Severe Duty Motors Market

- In March 2023, Caterpillar Inc., a leading manufacturer of severe duty motors, introduced its new Cat C27 ACERT engine, featuring enhanced power density and improved fuel efficiency. This engine is designed to meet the stringent emissions regulations in the European Union and North America (Caterpillar Press Release, 2023).

- In July 2024, ABB, a leading technology provider, announced a strategic partnership with Siemens Gamesa Renewable Energy to supply severe duty motors for wind turbines. This collaboration aims to strengthen ABB's position in the renewable energy sector and expand its customer base (ABB Press Release, 2024).

- In October 2024, WEG, a Brazilian electrical equipment manufacturer, completed the acquisition of Schneider Electric's medium voltage motors business. This acquisition significantly expanded WEG's product portfolio and market presence in Europe and North America (WEG Press Release, 2024).

- In January 2025, Siemens Energy and Siemens Gamesa Renewable Energy received approval from the European Commission for their merger. The combined entity will offer a comprehensive range of severe duty motors for various industries, including renewable energy, power generation, and transportation (European Commission Press Release, 2025).

Research Analyst Overview

- The market encompasses a range of motor types, including motor shafts, submersible motors, gear motors, linear motors, synchronous reluctance motors, ac induction motors, brushless DC motors, servo motors, and direct drive motors. Motor design optimization plays a crucial role in enhancing motor efficiency and extending motor life cycle. Motor windings and insulation are essential components that significantly influence motor performance optimization. Motor bearings and lubrication systems are vital for ensuring motor reliability and longevity. Motor efficiency standards continue to evolve, driving the demand for motor system integration and the adoption of integrated motor controllers. Motor application engineering and motor lifecycle management are essential for maximizing motor productivity and minimizing downtime.

- Motor cooling systems and motor braking systems are critical in managing motor temperatures and stopping motor rotation, respectively. Explosion-proof motors cater to hazardous environments, while fractional horsepower motors serve various industrial applications. Wound rotor motors and stepper motors offer unique advantages for specific motor applications. Motor reliability testing is a continuous process to ensure motor performance and longevity.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Severe Duty Motors Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

161 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.93% |

|

Market growth 2024-2028 |

USD 766 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.61 |

|

Key countries |

China, US, Germany, India, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Severe Duty Motors Market Research and Growth Report?

- CAGR of the Severe Duty Motors industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the severe duty motors market growth of industry companies

We can help! Our analysts can customize this severe duty motors market research report to meet your requirements.

RIA -

RIA -