Skimmed Milk Market Size 2025-2029

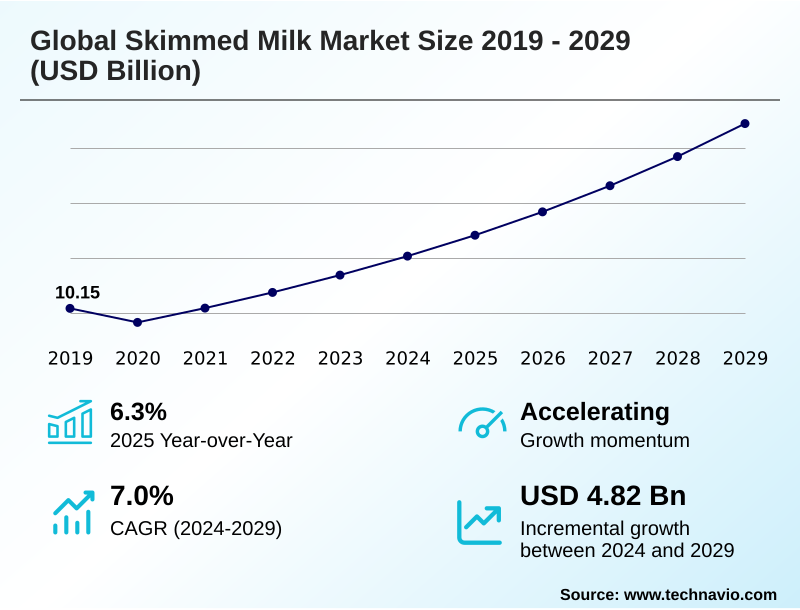

The skimmed milk market size is valued to increase by USD 4.82 billion, at a CAGR of 7% from 2024 to 2029. Heightened health and wellness consciousness driving demand for low-fat, high-protein diets will drive the skimmed milk market.

Major Market Trends & Insights

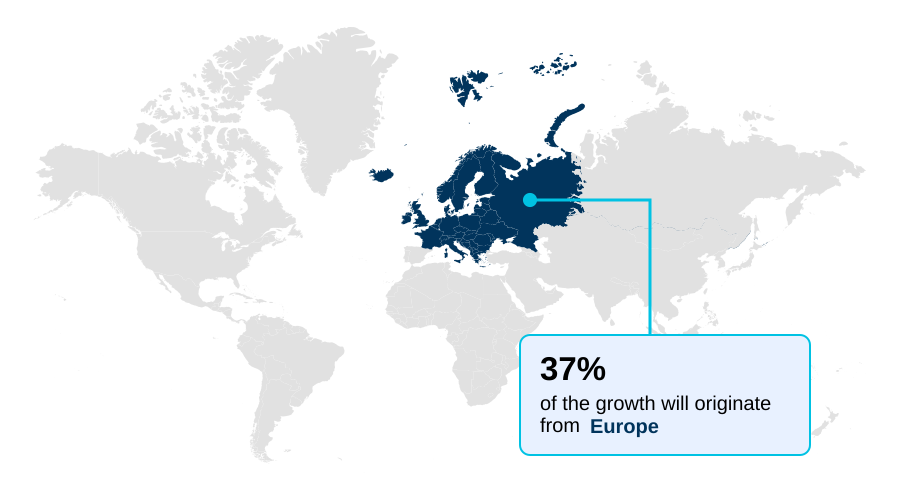

- Europe dominated the market and accounted for a 37.3% growth during the forecast period.

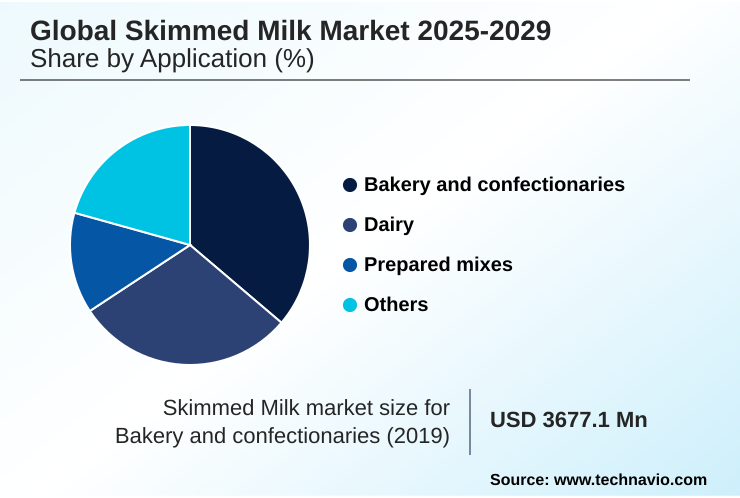

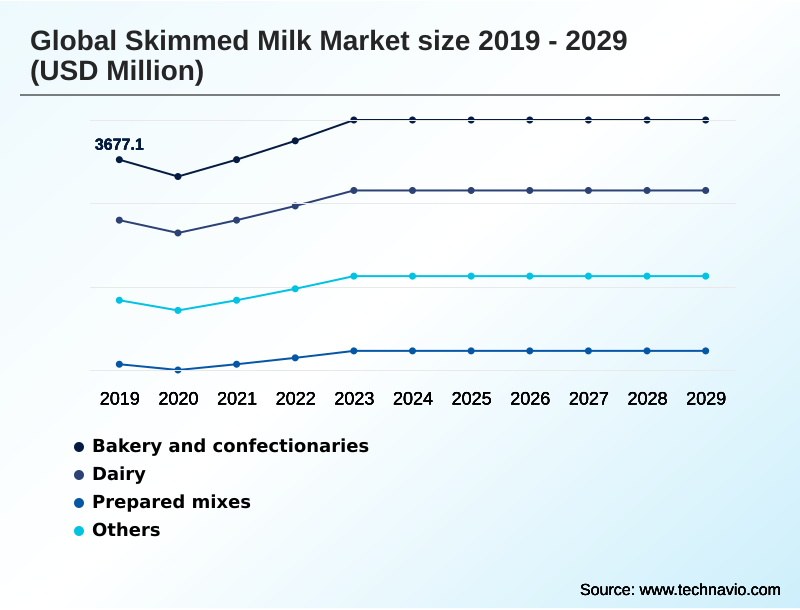

- By Application - Bakery and confectionaries segment was valued at USD 4.12 billion in 2023

- By Packaging - Cartons segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 6.71 billion

- Market Future Opportunities: USD 4.82 billion

- CAGR from 2024 to 2029 : 7%

Market Summary

- The skimmed milk market is evolving beyond its traditional role as a low-fat beverage, driven by its versatility as a critical dairy ingredient in diverse food processing applications. A pronounced consumer shift towards health and wellness underpins demand, with an emphasis on high-protein, low-calorie food options.

- This trend is compelling manufacturers to focus on dairy product innovation, such as developing fortified skimmed milk and lactose-free milk variants. The industry leverages advanced dairy processing technologies like membrane filtration and spray drying to produce high-quality skimmed milk powder with specific functional properties for food formulation.

- In a key business scenario, food manufacturers are optimizing their supply chains by using instant skim milk powder to streamline production of recombined dairy products in regions with limited fresh milk supply. This strategy not only ensures product consistency but also reduces logistical costs.

- However, the market faces challenges from the growing plant-based milk competition and skimmed milk price volatility, which necessitate continuous strategic adjustments in food ingredient sourcing and production planning to maintain profitability and market position.

What will be the Size of the Skimmed Milk Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Skimmed Milk Market Segmented?

The skimmed milk industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Bakery and confectionaries

- Dairy

- Prepared mixes

- Others

- Packaging

- Cartons

- Pouches

- Bags

- Drums

- Type

- Spray dried

- Roller dried

- Geography

- Europe

- Germany

- France

- Spain

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Turkey

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- Europe

By Application Insights

The bakery and confectionaries segment is estimated to witness significant growth during the forecast period.

The bakery and confectionaries segment represents a significant application area, where the functional properties of skimmed milk are integral.

The use of skimmed milk powder, particularly low-heat skim milk powder, in food formulation enhances texture, browning, and shelf life in a vast array of baked goods.

As consumer demand for healthier options rises, protein fortification of these products has become a key strategy, with dairy ingredients being a preferred choice for their clean label appeal.

This trend is driving innovation in bakery and confectionery ingredients, with manufacturers focusing on powder agglomeration techniques to improve solubility and consistency.

Efficient food ingredient sourcing for these value-added dairy products enables producers to achieve up to a 10% reduction in formulation costs while meeting demand in confectionery production and broader food processing applications.

The Bakery and confectionaries segment was valued at USD 4.12 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 37.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Skimmed Milk Market Demand is Rising in Europe Get Free Sample

The geographic landscape of the market is characterized by varied regional dynamics and trade flows, heavily influenced by local production capabilities and consumer preferences.

Europe accounts for over 37% of the market's incremental growth, driven by its established dairy industry and strong export channels.

In contrast, the APAC region shows the highest growth trajectory, with its rate exceeding North America's by 1.6 percentage points, fueled by rising incomes and awareness of nutritional food and beverage ingredients.

Key technologies such as ultra-high temperature processing (UHT) and aseptic packaging are crucial for serving these diverse regions, enabling the distribution of shelf-stable milk.

The efficiency of spray drying facilities dictates the supply of instant skim milk powder for the global dairy trade, where milk powder solubility is a critical quality metric for beverage manufacturing and other industrial uses.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global skimmed milk market 2025-2029 continues to be shaped by a complex set of factors influencing both supply and demand. Understanding the benefits of spray dried skim milk powder is crucial for food manufacturers, as this ingredient is fundamental in a wide range of applications. Its use in prepared food mixes and for confectionery applications highlights its versatility.

- The role of skimmed milk in infant nutrition remains a key demand driver, necessitating stringent quality controls. For instance, advancements in dairy processing technology have improved product safety, reducing contamination risks by over 30% compared to legacy systems. Processors are closely monitoring the impact of raw material costs on skim milk, which directly affects profitability.

- Strategic decisions, such as using skimmed milk for yogurt production, are balanced against the challenges of plant-based milk alternatives. The shelf life of UHT skimmed milk cartons is a significant advantage, supported by innovations in skimmed milk packaging. As low-fat dairy product consumer preferences evolve, the market sees new developments in lactose-free skimmed milk market trends.

- The functional properties of skimmed milk in food, particularly for protein-fortified foods and in recombined milk products, are a focus of R&D. Furthermore, the nutritional value of fortified skimmed milk and its use as a post-exercise beverage are prominent in marketing.

- Effective supply chain logistics for skim milk powder are essential for managing global distribution, while the industry also addresses sustainability in skimmed milk production. The application of skimmed milk powder in chocolate manufacturing remains a specialized but important niche.

What are the key market drivers leading to the rise in the adoption of Skimmed Milk Industry?

- The primary market driver is the heightened health and wellness consciousness among consumers, which is significantly increasing the demand for low-fat, high-protein dietary options like skimmed milk.

- A primary market driver is the escalating consumer focus on health, which has intensified the demand for low-fat dairy options.

- The preference for skim milk vs whole milk nutrition is clear among health-conscious demographics, who seek low-calorie food options without sacrificing essential nutrients.

- This shift has accelerated the adoption of advanced dairy processing technologies like membrane filtration and centrifugal separation to perfect milkfat removal while retaining protein content.

- Innovations in the lactose-free milk category have expanded the consumer base, with new enzymatic processes improving taste and digestibility, thereby increasing market penetration by 20% in key demographics.

- The rise of private label dairy products offering affordability and quality is also fueling market growth, alongside a broader industry push toward more sustainable dairy farming practices to meet evolving consumer expectations.

What are the market trends shaping the Skimmed Milk Industry?

- A significant market trend is the rising demand for fortified skimmed milk, driven by increasing health awareness among consumers. This is prompting manufacturers to innovate with nutritionally enhanced products.

- Market trends are increasingly shaped by consumer demand for functional and nutritionally enhanced products. The development of high-protein skim milk and other functional dairy products is a direct response to the growing interest in health and wellness. This has led to significant dairy product innovation, particularly in fortified skimmed milk for sports nutrition and infant formula.

- Ingredients like whey protein isolate and caseinates are being integrated to boost the nutritional profile of fortified dairy beverages, with formulations now achieving protein levels 50% higher than standard milk. In the nutritional beverage formulation space, companies are leveraging these ingredients to create products that support specific health goals, appealing to a wider demographic.

- The focus on consumer health trends is also driving the adoption of new processing methods to preserve the integrity of these dietary supplement ingredients, enhancing overall product value and market appeal.

What challenges does the Skimmed Milk Industry face during its growth?

- A key challenge affecting industry growth is the heightened competition from a growing array of plant-based milk alternatives.

- The market faces significant challenges, primarily from skimmed milk price volatility and intense plant-based milk competition. Fluctuations in global dairy solids trade create an unpredictable environment for producers of nonfat dry milk and reconstituted milk, impacting margins. To mitigate this, companies are focusing on dairy supply chain optimization, which has been shown to reduce logistical costs by up to 12%.

- Furthermore, the rise of dairy alternatives requires the traditional industry to emphasize the superior dairy protein functionality of products like milk protein concentrate and recombined dairy products. Adherence to stringent dairy industry regulations and food safety in dairy protocols adds another layer of operational complexity.

- Navigating these challenges requires strategic sourcing and production planning to ensure a stable supply of key ingredients like medium-heat skim milk powder.

Exclusive Technavio Analysis on Customer Landscape

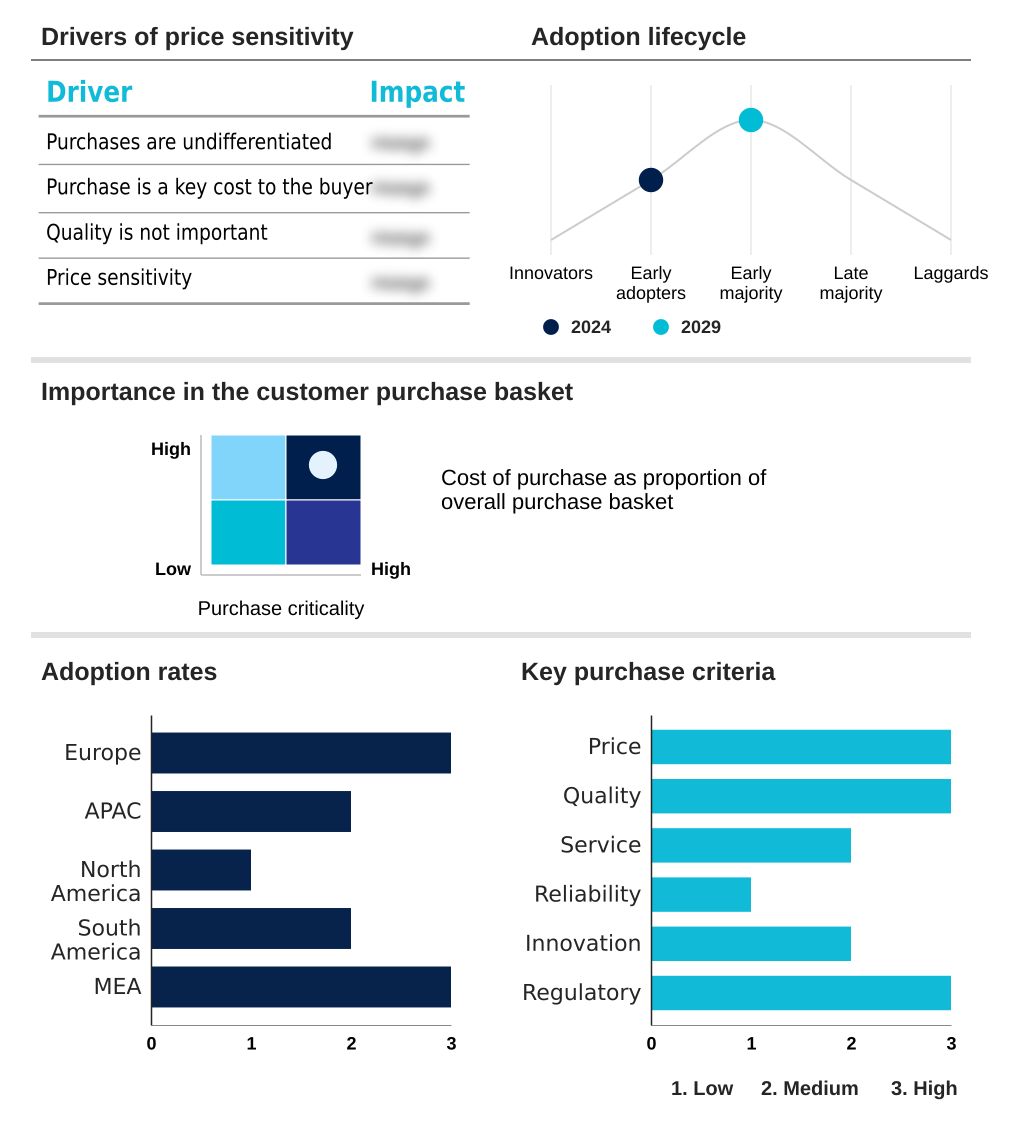

The skimmed milk market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the skimmed milk market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Skimmed Milk Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, skimmed milk market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agri Mark Inc. - The vendor landscape offers a diverse portfolio of skimmed milk products, including specialized powders and liquids tailored for food manufacturing, nutritional applications, and direct consumption.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agri Mark Inc.

- Agropur Dairy Cooperative

- Alpen Food Group BV

- Arla Foods amba

- Dairy Farmers of America Inc.

- Darigold Inc.

- Fonterra Cooperative Group Ltd.

- Grassland Dairy Products Inc.

- Gujarat Co Milk Ltd.

- Kruger GmbH and Co. KG

- LACTALIS Ingredients

- Nestle SA

- Royal Friesland Campina NV

- Saputo Inc.

- Schreiber Foods Inc.

- Sterling Agro Industries Ltd.

- Synlait Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Skimmed milk market

- In August, 2024, Germany's Deutsches Milchkontor GmbH entered into a collaboration with the Kazakhstan Milk dairy plant to establish a new cheese production facility, a strategic move impacting milk allocation for other dairy products.

- In January, 2025, Tetra Pak and Lactalis announced the launch of an aseptic beverage carton incorporating certified recycled polymers, signaling a significant step toward circularity in milk packaging.

- In January, 2025, Nissha Metallizing Solutions and Tetra Pak revealed a collaboration on an aseptic beverage carton featuring a paper-based barrier, increasing the renewable content to 90% and reducing reliance on aluminum.

- In February, 2025, a leading food and beverage corporation announced a new line of ready-to-drink nutritional beverages featuring high-protein fortified skimmed milk, targeting the growing sports nutrition and wellness segments.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Skimmed Milk Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 293 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7% |

| Market growth 2025-2029 | USD 4823.4 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 6.3% |

| Key countries | Germany, France, Russia, Poland, Spain, Italy, China, India, Japan, Indonesia, Australia, South Korea, US, Canada, Mexico, Brazil, Argentina, Colombia, Iran, Turkey, Egypt, Saudi Arabia and South Africa |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The skimmed milk market is defined by its integral role as a foundational dairy ingredient and a staple low-fat dairy product. Advanced dairy processing techniques, including centrifugal separation for milkfat removal and subsequent evaporation process and spray drying, are central to producing various grades of skimmed milk powder, such as low-heat and medium-heat variants.

- These powders, along with milk protein concentrate and whey protein isolate, are vital for food formulation across bakery, confectionery, and nutritional sectors. The trend toward nutritional fortification has spurred dairy product innovation, leading to the launch of high-protein and fortified skimmed milk products.

- In the boardroom, the decision to invest in technologies like membrane filtration for milk fractionation is now directly linked to a product differentiation strategy. For example, such investments enable the creation of specialized ingredients, offering a 15% margin premium over standard nonfat dry milk.

- The market also sees growth in shelf-stable UHT skimmed milk, facilitated by aseptic packaging, which meets demand for convenience without compromising quality.

What are the Key Data Covered in this Skimmed Milk Market Research and Growth Report?

-

What is the expected growth of the Skimmed Milk Market between 2025 and 2029?

-

USD 4.82 billion, at a CAGR of 7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Bakery and confectionaries, Dairy, Prepared mixes, and Others), Packaging (Cartons, Pouches, Bags, and Drums), Type (Spray dried, and Roller dried) and Geography (Europe, APAC, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, APAC, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Heightened health and wellness consciousness driving demand for low-fat, high-protein diets, Heightened competition from plant based alternatives

-

-

Who are the major players in the Skimmed Milk Market?

-

Agri Mark Inc., Agropur Dairy Cooperative, Alpen Food Group BV, Arla Foods amba, Dairy Farmers of America Inc., Darigold Inc., Fonterra Cooperative Group Ltd., Grassland Dairy Products Inc., Gujarat Co Milk Ltd., Kruger GmbH and Co. KG, LACTALIS Ingredients, Nestle SA, Royal Friesland Campina NV, Saputo Inc., Schreiber Foods Inc., Sterling Agro Industries Ltd. and Synlait Ltd.

-

Market Research Insights

- The market is shaped by a dynamic interplay between consumer health trends and technological advancements in food processing applications. The demand for functional and fortified dairy beverages is expanding, with products now delivering enhanced nutritional profiles.

- This push for innovation has led to measurable improvements in production; for instance, advanced aseptic carton technology has extended product shelf life by over 25% for UHT skimmed milk. Furthermore, optimizing dairy supply chain operations through better demand forecasting has reduced inventory holding costs by 15%.

- As the plant-based milk competition intensifies, dairy manufacturers are focusing on value-added dairy propositions and leveraging clean label dairy ingredients to appeal to discerning consumers, highlighting the clear nutritional benefits of skim milk vs whole milk nutrition to maintain market relevance.

We can help! Our analysts can customize this skimmed milk market research report to meet your requirements.

RIA -

RIA -