Smart Lighting Market Size 2026-2030

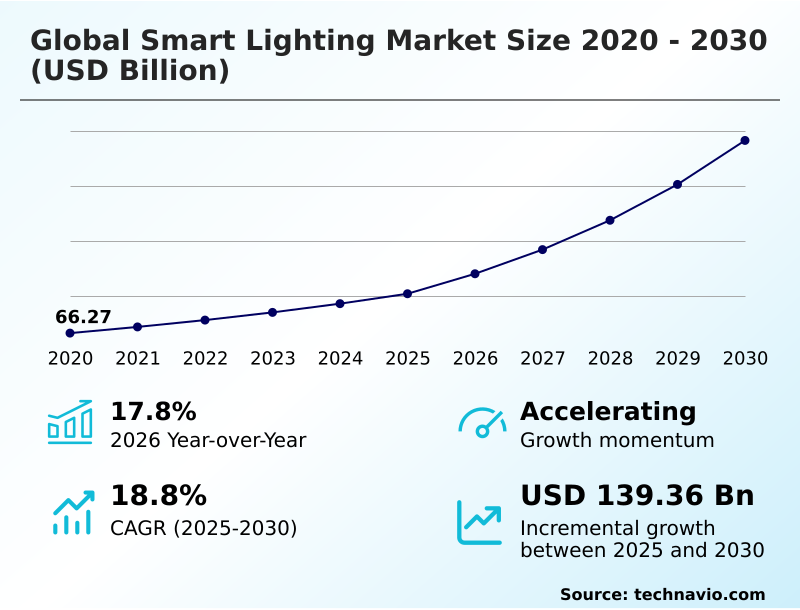

The smart lighting market size is valued to increase by USD 139.36 billion, at a CAGR of 18.8% from 2025 to 2030. Increasing emphasis on energy conservation and stringent governmental regulations will drive the smart lighting market.

Major Market Trends & Insights

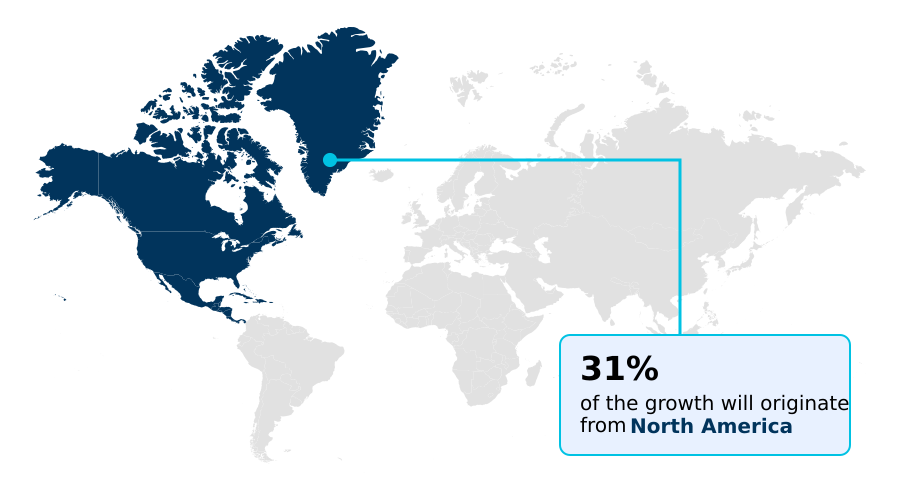

- North America dominated the market and accounted for a 31.2% growth during the forecast period.

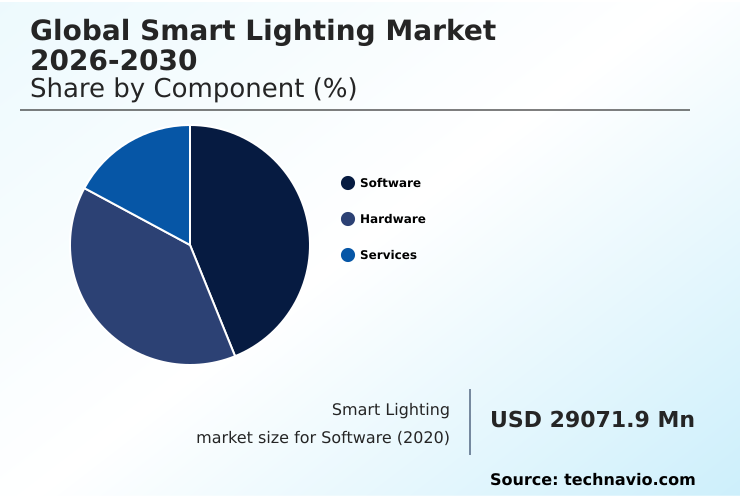

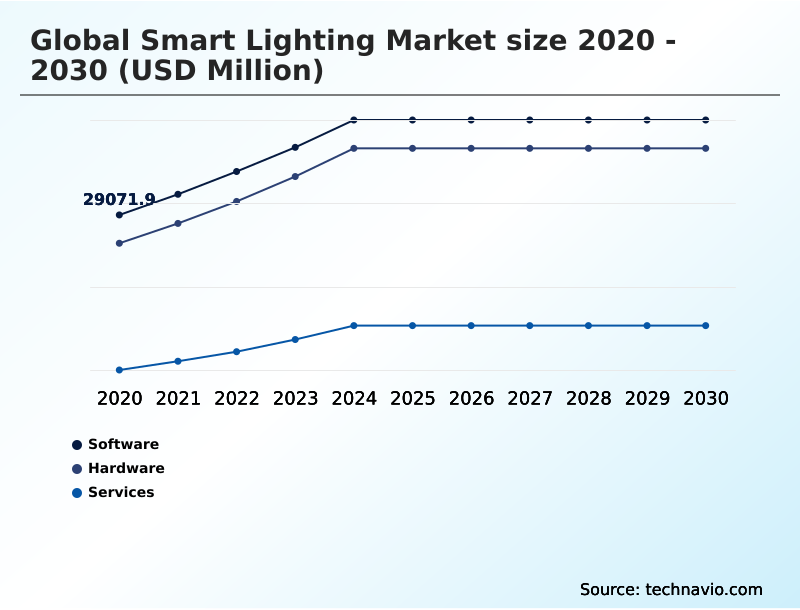

- By Component - Software segment was valued at USD 39.92 billion in 2024

- By Product - BMS segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 175.15 billion

- Market Future Opportunities: USD 139.36 billion

- CAGR from 2025 to 2030 : 18.8%

Market Summary

- The smart lighting market represents a significant technological shift, moving beyond basic illumination to become an integral component of the Internet of Things (IoT) ecosystem. This evolution is propelled by a global focus on energy efficiency, with intelligent controls and LED technology offering substantial operational cost reductions.

- A primary trend shaping the industry is the adoption of human-centric lighting, which aims to enhance occupant well-being and productivity by adjusting light characteristics to support natural circadian rhythms. However, significant challenges persist, including the high initial investment cost and the pervasive market fragmentation caused by a lack of interoperability standards between different manufacturers' systems.

- In a commercial facility management scenario, for instance, integrating data from lighting occupancy sensors with an HVAC system to dynamically manage climate control remains complex without unified protocols.

- Overcoming these hurdles is crucial for the market to realize its full potential as a foundational platform for creating truly intelligent, responsive, and sustainable built environments that cater to both efficiency and human experience.

What will be the Size of the Smart Lighting Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Smart Lighting Market Segmented?

The smart lighting industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Software

- Hardware

- Services

- Product

- BMS

- HVAC

- Lighting control

- Security and access control

- Others

- Connectivity

- Wireless

- Wired

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment serves as the intelligent control layer, shifting from device-level firmware to sophisticated cloud-based management platforms. These systems translate user intent into commands, with innovation centered on open application programming interfaces (APIs) that foster a vibrant developer ecosystem.

The integration of predictive maintenance algorithms enables proactive servicing, reducing system downtime by up to 25%. A key area of development is mitigating cybersecurity vulnerabilities through robust security protocols and ensuring data privacy compliance for an enhanced user experience.

The rise of generative AI lighting effects and edge computing in lighting, supported by a flexible integrated systems architecture and continuous firmware over-the-air (FOTA) updates, is redefining system capabilities and supporting human-centric lighting implementation for agile workspace design.

The Software segment was valued at USD 39.92 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 31.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Smart Lighting Market Demand is Rising in North America Get Free Sample

The global smart lighting market 2026-2030 landscape is shaped by distinct regional drivers, with North America contributing 31% of incremental growth, Europe 30%, and APAC 28%.

In North America, the market is propelled by a strong demand-side pull for smart home ecosystem integration. Europe leads in regulatory-driven adoption, with stringent green building certification standards mandating advanced control systems.

APAC's growth is fueled by massive government-led smart city projects deploying intelligent street lighting, which can reduce municipal energy costs by over 60%.

Advanced applications like indoor positioning systems and asset tracking beacons are gaining traction globally, transforming connected building networks into platforms for creating a digital twin of building operations.

Technologies such as Power over Ethernet (PoE) and luminaire level lighting control (LLLC) are enabling this shift, supporting automated demand response and agile workspace design within a broader smart building IoT network.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic value of the global smart lighting market 2026-2030 is increasingly defined by its integration capabilities and specialized applications. Boardroom discussions now evaluate the impact of smart lighting on productivity, where studies show that implementing the benefits of human-centric lighting in offices can improve employee alertness.

- A critical use case is integrating smart lighting with HVAC systems, which can more than double a building's overall energy savings compared to standalone system management. This synergy is a core component of optimizing building operations with smart lighting.

- The debate over a wireless vs wired smart lighting comparison often centers on deployment flexibility versus network security, with Power over Ethernet lighting system advantages in reliability being weighed against the ease of retrofitting with wireless. Cybersecurity risks in connected lighting systems and data privacy concerns with smart lighting remain paramount, influencing technology choices.

- Business models are also evolving, with the lighting as a service ROI calculation becoming a key factor for shifting from capital to operational spending. The role of smart lighting in sustainability goals is expanding beyond simple energy management, as seen in smart lighting for retail customer engagement, where dynamic illumination enhances the shopping experience.

- For municipalities, smart street lighting benefits for cities include improved safety and a foundational network for IoT services. The emergence of unified standards like the Matter protocol affects smart lighting by simplifying integration. Advanced functionalities now include using smart lighting for asset tracking and deploying daylight harvesting sensors in commercial buildings, which are critical for effective energy management.

- These systems, particularly smart lighting solutions for healthcare facilities, create tailored residential smart lighting automation scenes, directly influencing the smart lighting impact on circadian rhythm and paving the way for the future of generative AI in lighting design.

What are the key market drivers leading to the rise in the adoption of Smart Lighting Industry?

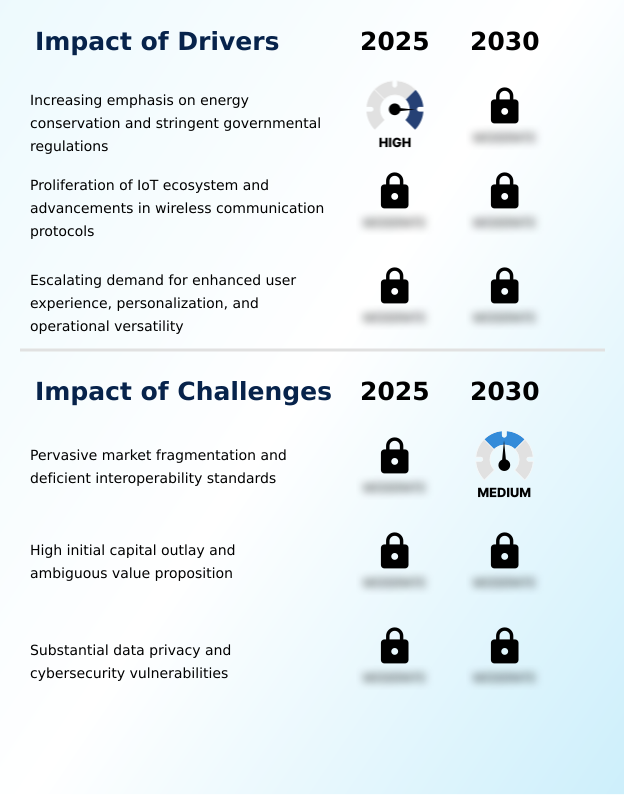

- A primary driver for market expansion is the intensifying global emphasis on energy conservation, which is reinforced by stringent governmental regulations and sustainability mandates.

- Market growth is fundamentally propelled by stringent energy conservation mandates and the rapid expansion of the integrated smart environment.

- The widespread adoption of energy-efficient light emitting diodes (LED) and wireless communication protocols provides the foundation, while intelligent components like occupancy sensors and daylight harvesting sensors deliver significant operational savings.

- A robust return on investment (ROI) analysis consistently shows that integrated building management systems can reduce energy costs by over 40% compared to conventional lighting.

- This synergy, combined with the increasing demand for smart home ecosystem integration to meet corporate sustainability goals, drives adoption.

- Furthermore, the capability for remote monitoring and control is a critical factor, enabling automated demand-response programs that enhance grid stability and further optimize energy use.

What are the market trends shaping the Smart Lighting Industry?

- The ascendancy of human-centric lighting marks a significant market evolution, shifting the focus beyond simple illumination and energy efficiency. This trend prioritizes the influence of light on human health, productivity, and overall well-being.

- Key trends are reshaping the market, moving beyond basic illumination toward enhancing human well-being and operational efficiency. The rise of the light as a service (LaaS) model, driven by a human-centric design approach, is converting capital costs into predictable operational expenditure (OpEx), making advanced systems more accessible.

- This is closely tied to the adoption of human-centric lighting principles, which leverage tunable-white LED modules for circadian rhythm regulation to improve occupant comfort optimization. Such systems can enhance productivity by over 15%. This light as a service business model is crucial for effective building lifecycle management.

- The use of space utilization analytics, another key trend, allows organizations to optimize their physical footprint, with some achieving a 20% improvement in space efficiency.

What challenges does the Smart Lighting Industry face during its growth?

- Pervasive market fragmentation, caused by a lack of universally adopted communication protocols and interoperability standards, remains a significant challenge to accelerated market growth.

- Persistent challenges hinder widespread adoption, primarily stemming from a lack of interoperability standards among competing wireless technologies like the zigbee protocol, bluetooth mesh networking, and z-wave standard. This fragmentation complicates facility management optimization and increases the total cost of ownership, as integrating disparate networked lighting controls often requires custom solutions.

- The high initial capital expenditure (cap-ex) remains a significant barrier, particularly when the technology adoption rate is slowed by an unclear value proposition. This is amplified by the complexities of system-on-a-chip (soc) for lighting design and achieving a high color rendering index (CRI) with some budget options. Overcoming the demand-side pull for lower-cost, non-standardized products is essential for market maturation.

Exclusive Technavio Analysis on Customer Landscape

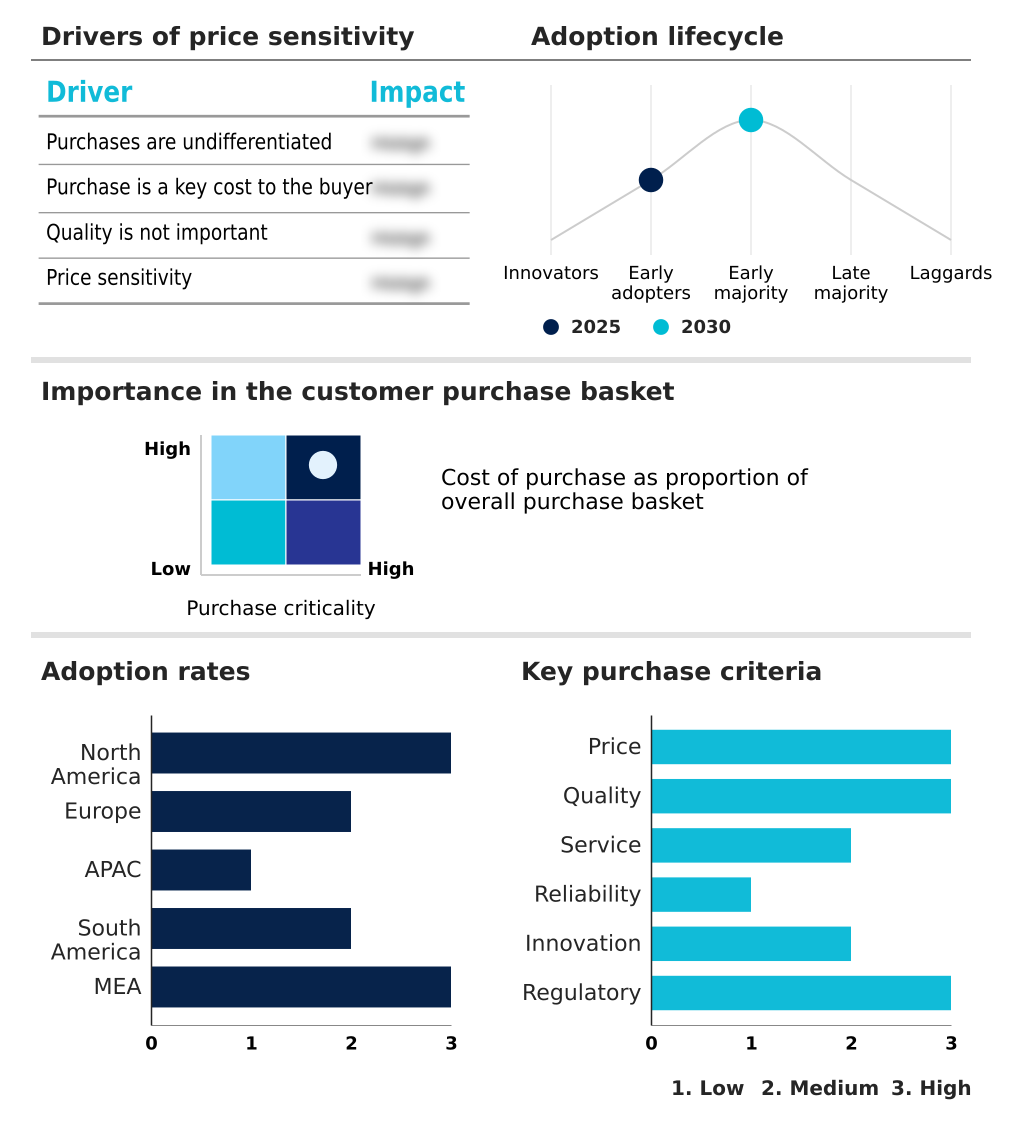

The smart lighting market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the smart lighting market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Smart Lighting Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, smart lighting market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Acuity Brands Inc. - Delivering integrated intelligent lighting systems and connected controls for commercial and residential applications, enhancing space functionality through advanced wireless and embedded solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acuity Brands Inc.

- ams OSRAM AG

- Cree Lighting

- Current Lighting Solutions LLC

- Digital Lumens Inc.

- Eaton Corp. Plc

- Govee

- Hubbell Inc.

- Legrand SA

- Leviton Manufacturing Co. Inc.

- LIFX

- Lutron Electronics Co. Inc.

- Nanoleaf Canada Ltd.

- RAB Lighting Inc.

- Samsung Electronics Co. Ltd.

- Shengdi Smart Technology Co. Ltd

- Signify NV

- TP Link Corp. Ltd.

- YEELIGHT

- Zumtobel Group AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Smart lighting market

- In January 2025, Philips Hue, a brand of Signify NV, introduced a generative AI lighting assistant at the Consumer Electronics Show, designed to create personalized lighting scenes via text or voice commands.

- In January 2025, the Connectivity Standards Alliance updated its universal standard with the release of Matter 1.4, aimed at improving seamless interoperability between smart lighting devices from different manufacturers.

- In May 2025, Brilliant launched its second-generation smart home control panels, offering higher-resolution screens and faster responsiveness for integrated management of lighting and other connected home systems.

- In April 2025, Signify NV initiated a patent infringement lawsuit against Nanoleaf Canada Ltd., highlighting the increasing strategic importance of intellectual property in the competitive landscape.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Smart Lighting Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 331 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 18.8% |

| Market growth 2026-2030 | USD 139361.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 17.8% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The smart lighting market has evolved from a hardware-centric industry to a strategic enabler of intelligent building infrastructure, driven by advancements in light emitting diodes (LED) and networked lighting controls. The integration of occupancy sensors and daylight harvesting sensors is now standard for energy management, but the true value emerges from sophisticated system intelligence.

- The implementation of a light as a service (LaaS) business model, supported by cloud-based management platforms, allows enterprises to adopt advanced solutions like human-centric lighting and circadian rhythm regulation without prohibitive upfront investment. For corporate boards, the decision to deploy tunable-white LED modules is no longer just a facilities upgrade but a strategic investment in talent retention and productivity.

- For example, systems incorporating predictive maintenance algorithms demonstrate a clear operational benefit, reducing unscheduled service calls by over 30%. This shift positions lighting as a critical data-generating asset within integrated building management systems, essential for optimizing modern workspaces.

What are the Key Data Covered in this Smart Lighting Market Research and Growth Report?

-

What is the expected growth of the Smart Lighting Market between 2026 and 2030?

-

USD 139.36 billion, at a CAGR of 18.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, Hardware, and Services), Product (BMS, HVAC, Lighting control, Security and access control, and Others), Connectivity (Wireless, and Wired) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing emphasis on energy conservation and stringent governmental regulations, Pervasive market fragmentation and deficient interoperability standards

-

-

Who are the major players in the Smart Lighting Market?

-

Acuity Brands Inc., ams OSRAM AG, Cree Lighting, Current Lighting Solutions LLC, Digital Lumens Inc., Eaton Corp. Plc, Govee, Hubbell Inc., Legrand SA, Leviton Manufacturing Co. Inc., LIFX, Lutron Electronics Co. Inc., Nanoleaf Canada Ltd., RAB Lighting Inc., Samsung Electronics Co. Ltd., Shengdi Smart Technology Co. Ltd, Signify NV, TP Link Corp. Ltd., YEELIGHT and Zumtobel Group AG

-

Market Research Insights

- The market's momentum is increasingly defined by tangible business outcomes derived from an integrated smart environment and smart home ecosystem integration. Enterprises leveraging an integrated systems architecture are reporting that remote monitoring and control capabilities can reduce manual oversight costs by up to 30%.

- Furthermore, the adoption of human-centric lighting implementation, guided by a human-centric design approach, is tied to productivity gains of over 10% in corporate settings. This shift from novelty to necessity is underscored by a compelling return on investment (ROI) analysis, with the total cost of ownership for connected systems being offset by significant energy savings and operational efficiencies.

- These quantifiable benefits are aligning with corporate sustainability goals, making adoption a strategic priority for facility management optimization.

We can help! Our analysts can customize this smart lighting market research report to meet your requirements.

RIA -

RIA -