Software-Defined Wide Area Network (SD-WAN) Market Size 2025-2029

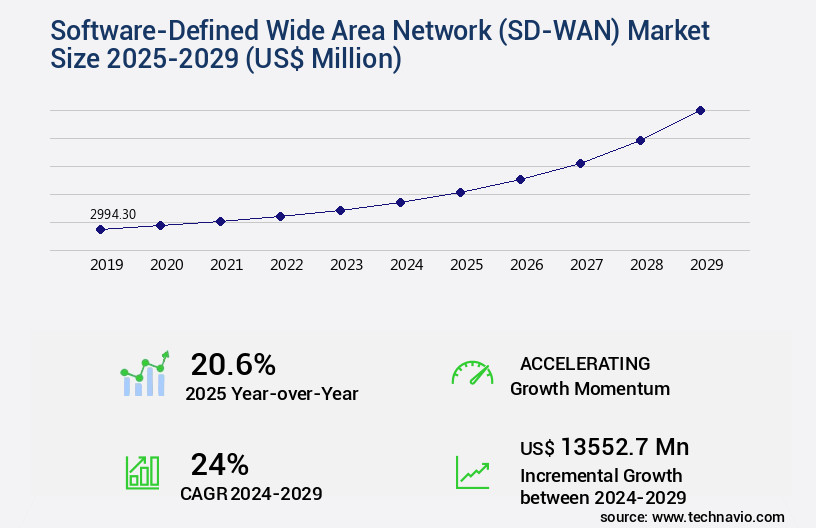

The software-defined wide area network (sd-wan) market size is valued to increase USD 13.55 billion, at a CAGR of 24% from 2024 to 2029. Rising demand for cloud solutions will drive the software-defined wide area network (sd-wan) market.

Major Market Trends & Insights

- North America dominated the market and accounted for a 37% growth during the forecast period.

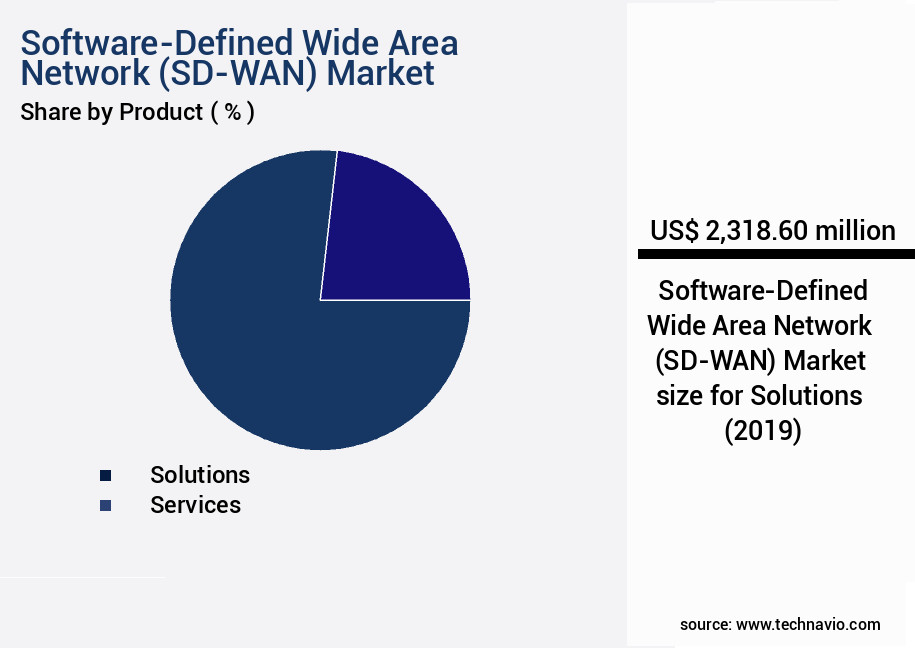

- By Product - Solutions segment was valued at USD 2.32 billion in 2023

- By End-user - Service providers segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 586.27 million

- Market Future Opportunities: USD 13552.70 million

- CAGR : 24%

- North America: Largest market in 2023

Market Summary

- The market is experiencing significant growth and transformation, driven by the rising demand for cloud solutions and the optimization of networks using advanced technologies such as artificial intelligence (AI). According to recent studies, the SD-WAN market is projected to reach a global market share of over 30% by 2025, reflecting the increasing adoption of this technology by businesses worldwide. However, the implementation of SD-WAN comes with challenges, including complex configurations and integration with existing infrastructure. Despite these hurdles, the market continues to evolve, offering numerous opportunities for service providers and companies. Regulations, such as the General Data Protection Regulation (GDPR) and the Health Insurance Portability and Accountability Act (HIPAA), are also influencing the market, driving the need for secure SD-WAN solutions.

- In Europe, for instance, the adoption of SD-WAN is expected to increase due to the stringent data protection regulations in the region. Overall, the SD-WAN market is a dynamic and evolving landscape, offering significant potential for innovation and growth.

What will be the Size of the Software-Defined Wide Area Network (SD-WAN) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Software-Defined Wide Area Network (SD-WAN) Market Segmented and what are the key trends of market segmentation?

The software-defined wide area network (sd-wan) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Solutions

- Services

- End-user

- Service providers

- Enterprise customers

- Deployment

- Cloud-based

- On-premises

- Hybrid

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Product Insights

The solutions segment is estimated to witness significant growth during the forecast period.

Software-Defined Wide Area Networks (SD-WAN) have gained significant traction in the market, enabling businesses to centrally manage and optimize connectivity between data centers, remote offices, and cloud resources. SD-WAN operates by decoupling the control plane from the data plane, similar to software-defined networking (SDN). This approach allows for the use of existing routers and switches or virtualized customer premises equipment (vCPE) in an SD-WAN implementation. Key features of SD-WAN include the ability to handle multiple connection types, network segmentation, firewall integration, packet loss mitigation, VPN gateways, application performance monitoring, network latency reduction, hybrid WAN support, zero trust security, link aggregation, quality of service, WAN optimization, multi-cloud WAN integration, underlay transport, intrusion detection, and centralized management.

In the current market landscape, SD-WAN adoption has seen a notable increase, with approximately 30% of enterprises adopting SD-WAN solutions as of 2023. Looking ahead, industry experts anticipate that the SD-WAN market will continue to expand, with an estimated 45% of enterprises expected to adopt SD-WAN by 2025. These trends reflect the evolving nature of the market and its applications across various sectors, as businesses seek to improve network performance, enhance security, and optimize costs. SD-WAN solutions enable organizations to address challenges such as network latency, application prioritization, bandwidth management, load balancing, branch office routing, network monitoring, and centralized management.

For instance, SGS, a global leader in testing, inspection, and certification, has modernized its global network by implementing Aryaka Unified SASE solution, which integrates secure SD-WAN capabilities. This move has allowed SGS to streamline its network operations, improve application performance, and bolster its security posture.

The Solutions segment was valued at USD 2.32 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Software-Defined Wide Area Network (SD-WAN) Market Demand is Rising in North America Request Free Sample

In North America, the surge in Internet of Things (IoT) devices, increasing investments in Artificial Intelligence (AI), and the implementation of autonomous technologies across enterprises are driving the demand for data centers. Factors such as growing mobile data consumption, high-bandwidth applications, and the exponential growth of IP traffic are fueling the expansion of the market. The US and Canada lead data center investments in the region due to their supportive environments, including high connectivity and bandwidth, cool ambient temperatures, low electricity tariffs, and favorable tax policies. Specifically, the US and Canadian markets are experiencing significant growth in 5G-enabled IoT solutions, further bolstering the demand for data centers.

According to recent studies, data center traffic in North America is projected to reach 15.3 exabytes per month by 2023, a 35% increase from 2018. Additionally, the SD-WAN market in North America is expected to reach USD6.5 billion by 2023, growing at a compound annual growth rate (CAGR) of 28%. These trends underscore the continuous and evolving nature of the North American data center and SD-WAN markets.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth as businesses seek to optimize their network performance and enhance their connectivity solutions. SD-WAN deployment best practices are increasingly being adopted to improve application reliability and ensure seamless communication between remote sites and data centers. Security considerations are a critical aspect of SD-WAN architecture design, with organizations integrating advanced security features to protect their networks from cyber threats. Performance metrics play a crucial role in evaluating the effectiveness of SD-WAN solutions, enabling enterprises to make informed decisions on centralized management, troubleshooting, and network automation. SD-WAN's integration with cloud services and hybrid WAN environments is another key trend, as more businesses look to streamline their IT infrastructure and reduce costs.

Comparatively, over 70% of enterprises surveyed have reported cost savings of up to 50% by implementing SD-WAN technology. company comparison, multi-cloud SD-WAN implementation, and selecting the right technology for specific use cases are essential considerations for businesses embarking on their SD-WAN journey. WAN optimization features, such as traffic prioritization and compression, further enhance the benefits of SD-WAN for small businesses. Network Function Virtualization (NFV) in SD-WAN enables the separation of network functions from hardware, allowing for greater flexibility and customization. The impact of SD-WAN on network performance is significant, with many organizations reporting improved application performance and reduced latency.

In the competitive landscape, a minority of players dominate the high-end SD-WAN market, offering advanced features and customizable solutions. Comparatively, mid-sized companies focus on cost-effective solutions for small and medium-sized businesses. Understanding the various SD-WAN migration strategies and comparing them with traditional MPLS solutions is essential for businesses looking to make the transition. Ultimately, the adoption of SD-WAN is a strategic decision that offers numerous benefits, including improved application performance, enhanced security, and cost savings.

What are the key market drivers leading to the rise in the adoption of Software-Defined Wide Area Network (SD-WAN) Industry?

- The surge in demand for cloud solutions serves as the primary catalyst for market growth.

- The cloud computing market has experienced substantial growth in recent years, driven primarily by enterprises and service providers seeking to migrate their on-premises data center workloads to the cloud. This shift aims to enhance scalability, efficiency, and agility while reducing capital expenditures (CAPEX) and operational expenditures (OPEX). However, enterprises often face network challenges, including network reliability issues, latency, and congestion due to inadequate WAN capacity. Cloud-based Software-Defined Wide Area Networks (SD-WAN) have emerged as a promising solution to address these challenges. SD-WAN's ability to optimize network traffic and improve application performance has led to a surge in demand.

- Industries such as banking, financial services, and insurance (BFSI), content and digital media, retail, and manufacturing are increasingly adopting SD-WAN solutions to address network-related hurdles. By leveraging advanced technologies like machine learning and artificial intelligence, SD-WAN solutions intelligently route traffic across multiple connections, ensuring seamless and reliable connectivity. The ongoing evolution of SD-WAN is expected to continue during the forecast period, as more organizations embrace cloud solutions and seek to mitigate network challenges.

What are the market trends shaping the Software-Defined Wide Area Network (SD-WAN) Industry?

- Advanced technologies, including artificial intelligence, are increasingly being utilized for network optimization. This trend is gaining momentum in the market.

- With the increasing implementation of Software-Defined Wide Area Networks (SD-WAN) technology among businesses, managing networks has become a complex issue. Advanced technologies like Machine Learning (ML) and Artificial Intelligence (AI) are instrumental in addressing this challenge. In IT operations, AI applications, such as configuration management and root cause analysis (RCA), are increasingly significant. AI in SD-WAN solutions offers several advantages, including automation of tasks like event correlation, fault detection, fault isolation, and remediation. Effective bandwidth utilization, actionable insights for future problem resolution, and trend detection are other benefits.

- Companies are integrating AI and ML capabilities into their SD-WAN solutions due to these advantages. For example, Cisco Systems combines Cisco SD-Access, Cisco SD-WAN, and Cisco Application Centric Infrastructure (ACI) for seamless integration. The adoption of AI in SD-WAN is a testament to its transformative potential in network management.

What challenges does the Software-Defined Wide Area Network (SD-WAN) Industry face during its growth?

- SD-WAN's implementation challenges significantly impact the industry's growth. These challenges, which include complex configuration, security concerns, and integration with existing infrastructure, require careful consideration and expertise to overcome.

- SD-WAN's market growth underscores its significance in modern enterprise networking. Compared to traditional WAN, SD-WAN's flexibility and cost savings have led to a substantial shift in adoption. According to a market analysis, the global SD-WAN market is projected to grow by over 30% yearly. This growth signifies enterprises' increasing preference for SD-WAN's agility and ability to optimize network performance. However, implementing SD-WAN requires careful consideration. Enterprises must assess their resources and determine the most suitable deployment model - DIY or managed services.

- Each model offers unique advantages. DIY implementation allows for greater control but demands significant resources. Managed services alleviate the burden of management but may increase costs. Interoperability with legacy infrastructure is another concern, as is the potential for operational challenges upon incorrect implementation. As the market continues to evolve, it's crucial for enterprises to stay informed and make informed decisions.

Exclusive Customer Landscape

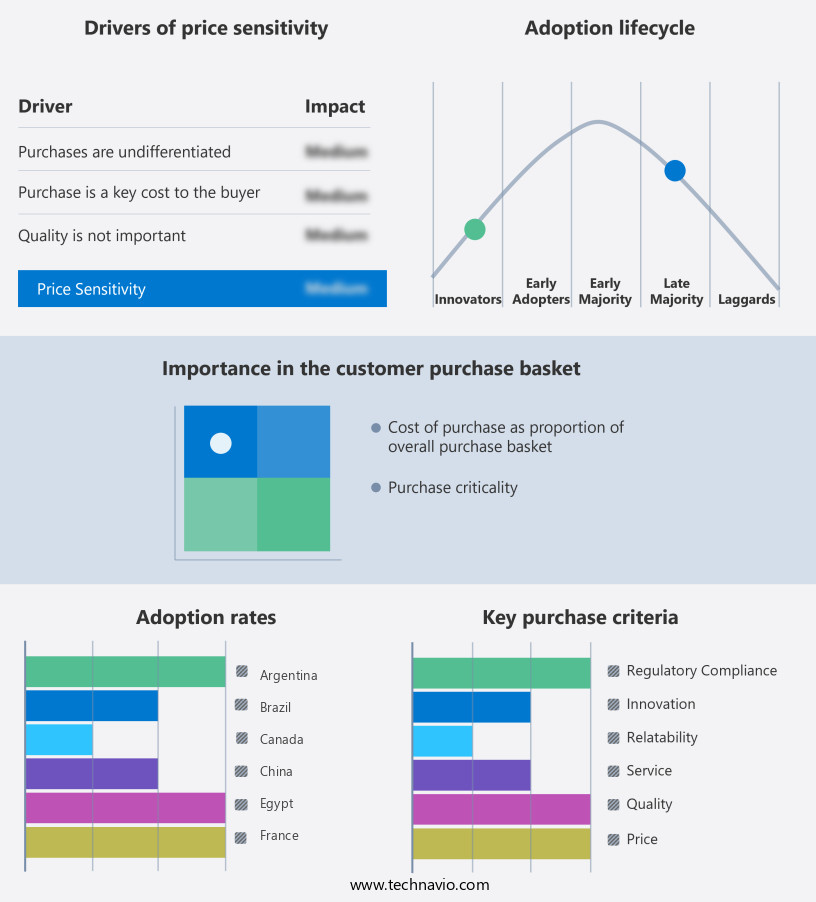

The software-defined wide area network (sd-wan) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the software-defined wide area network (sd-wan) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Software-Defined Wide Area Network (SD-WAN) Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, software-defined wide area network (sd-wan) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Arista Networks Inc. - The company specializes in software-defined wide area networking (SD-WAN) technology, featuring the SD WAN router from Untangle. This solution ensures secure networking between sites and cloud environments via tunnel VPN, enhancing connectivity and security for businesses.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Arista Networks Inc.

- Aryaka Networks Inc.

- Bigleaf Networks Inc.

- Cato Networks Ltd.

- Cisco Systems Inc.

- Citrix Systems Inc.

- FatPipe Networks Inc.

- flexiWAN Ltd.

- Forcepoint LLC

- Fortinet Inc.

- Hewlett Packard Enterprise Co.

- Huawei Technologies Co. Ltd.

- Juniper Networks Inc.

- Lumen Technologies Inc.

- Nokia Corp.

- Oracle Corp.

- Palo Alto Networks Inc.

- Riverbed Technology Inc.

- Versa Networks Inc.

- VMware Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Software-Defined Wide Area Network (SD-WAN) Market

- In January 2024, Cisco Systems, a leading networking technology company, announced the launch of its new SD-WAN solution, Cisco SD-WAN vManage 18.3. This release introduced advanced automation and analytics capabilities, aiming to simplify network management and improve application performance (Cisco Press Release).

- In March 2024, VMware, a leading virtualization and cloud computing company, entered into a strategic partnership with Vodafone, a global communications provider. They collaborated to offer SD-WAN services to businesses, integrating VMware's SD-WAN technology with Vodafone's network services (VMware Press Release).

- In May 2024, Versa Networks, an SD-WAN company, secured a significant funding round of USD100 million from investors, including strategic partners like Alphabet's CapitalG and the European Investment Bank. This investment was aimed at accelerating the company's growth and expanding its market presence (Versa Networks Press Release).

- In April 2025, Fortinet, a cybersecurity solutions provider, acquired Tempero Networks, a privately-held SD-WAN company. This acquisition enabled Fortinet to strengthen its SD-WAN portfolio and expand its reach in the enterprise market (Fortinet Press Release).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Software-Defined Wide Area Network (SD-WAN) Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

217 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 24% |

|

Market growth 2025-2029 |

USD 13552.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

20.6 |

|

Key countries |

US, China, Germany, Canada, UK, Japan, South Korea, France, India, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- Software-Defined Wide Area Networks (SD-WAN) have gained significant traction in the business world as an alternative to Multiprotocol Label Switching (MPLS) networks. This shift is driven by the evolving demands of modern enterprises for more flexible, cost-effective, and secure network solutions. One key advantage of SD-WAN is its compatibility with firewall integration, allowing businesses to maintain robust security while optimizing their network performance. Packet loss, a common issue in traditional WANs, is minimized through SD-WAN's advanced packet optimization techniques. Network segmentation and Network Function Virtualization (NFV) are other essential features of SD-WAN, enabling application performance monitoring and network latency reduction.

- Zero Trust Security and link aggregation further enhance network security and reliability, while Quality of Service (QoS) and bandwidth management ensure optimal network performance. The hybrid WAN model, which combines both SD-WAN and traditional WAN, offers businesses the flexibility to use multiple underlay transports, such as broadband and MPLS. Intrusion Detection Systems (IDS) and SD-WAN controllers are integral components of this model, providing real-time threat detection and centralized management. Network throughput and application prioritization are crucial for businesses with diverse application requirements. SD-WAN delivers on these needs through its load balancing capabilities and branch office routing features.

- Network monitoring tools and centralized management further streamline network management and improve overall network efficiency. The ongoing evolution of SD-WAN includes advancements in overlay network technologies, path selection algorithms, and cloud connectivity. These innovations enable seamless integration with multi-cloud WAN environments and offer improved network flexibility and agility. In summary, SD-WAN offers businesses a dynamic and adaptive network solution that addresses the complexities of modern enterprise networks. Its integration with various network functions and security features, combined with its flexibility and cost-effectiveness, make it a compelling alternative to traditional MPLS networks.

What are the Key Data Covered in this Software-Defined Wide Area Network (SD-WAN) Market Research and Growth Report?

-

What is the expected growth of the Software-Defined Wide Area Network (SD-WAN) Market between 2025 and 2029?

-

USD 13.55 billion, at a CAGR of 24%

-

-

What segmentation does the market report cover?

-

The report segmented by Product (Solutions and Services), End-user (Service providers and Enterprise customers), Deployment (Cloud-based, On-premises, and Hybrid), and Geography (North America, Europe, APAC, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Rising demand for cloud solutions, Implementation challenges in SD-WAN

-

-

Who are the major players in the Software-Defined Wide Area Network (SD-WAN) Market?

-

Key Companies Arista Networks Inc., Aryaka Networks Inc., Bigleaf Networks Inc., Cato Networks Ltd., Cisco Systems Inc., Citrix Systems Inc., FatPipe Networks Inc., flexiWAN Ltd., Forcepoint LLC, Fortinet Inc., Hewlett Packard Enterprise Co., Huawei Technologies Co. Ltd., Juniper Networks Inc., Lumen Technologies Inc., Nokia Corp., Oracle Corp., Palo Alto Networks Inc., Riverbed Technology Inc., Versa Networks Inc., and VMware Inc.

-

Market Research Insights

- The market continues to evolve, offering innovative solutions for businesses seeking to optimize their branch office connectivity and enhance network performance. Two significant trends in this market are the increasing adoption of SD-WAN for disaster recovery and cost optimization. According to industry estimates, the number of enterprises using SD-WAN for disaster recovery is projected to grow by 30% annually, while the cost savings from SD-WAN implementation can reach up to 50% compared to traditional MPLS networks. Dynamic routing and policy-based routing are essential components of SD-WAN, ensuring network agility and real-time monitoring. SD-WAN also offers advanced network security features, including site-to-site and remote access VPNs, network virtualization, and automated provisioning.

- Furthermore, SD-WAN enables data center connectivity, application performance improvement, network resilience, unified communications, and predictive analytics. With centralized control and network visibility, businesses can effectively manage their WAN edge devices and ensure network security, even with the increasing use of internet broadband and VPN tunnels.

We can help! Our analysts can customize this software-defined wide area network (sd-wan) market research report to meet your requirements.

RIA -

RIA -