Solar Panel Recycling Market Size 2024-2028

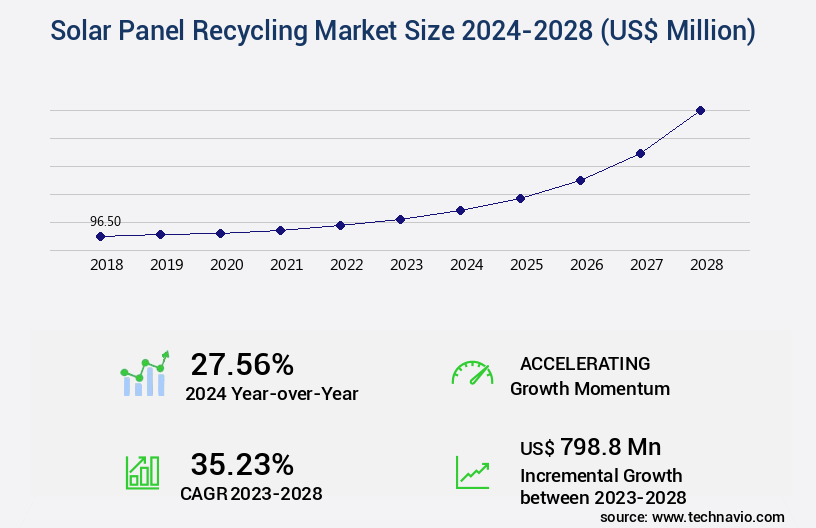

The solar panel recycling market size is valued to increase by USD 798.8 million, at a CAGR of 35.23% from 2023 to 2028. Reduction in costs of solar PV systems will drive the solar panel recycling market.

Market Insights

- APAC dominated the market and accounted for a 43% growth during the 2024-2028.

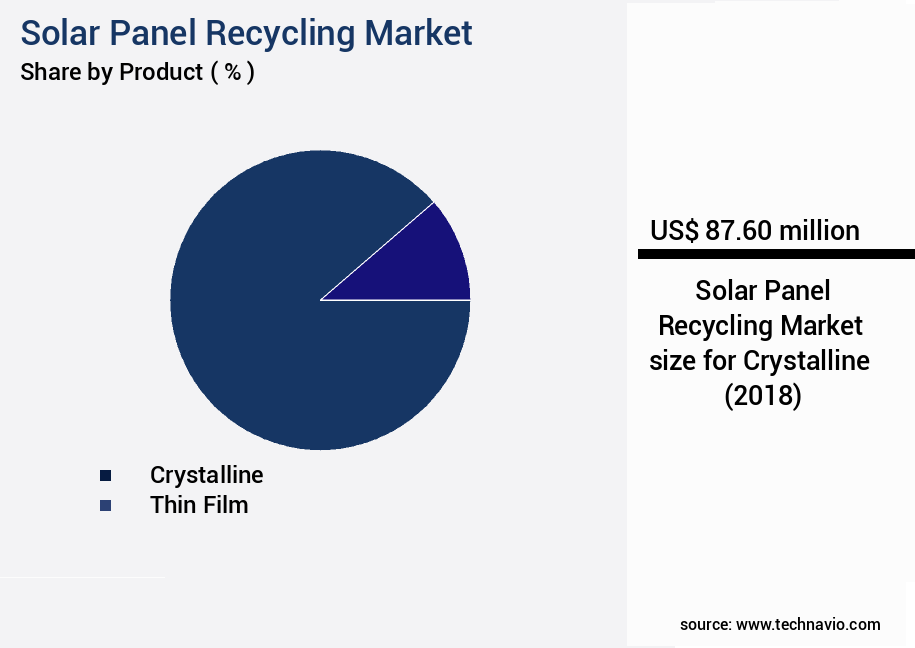

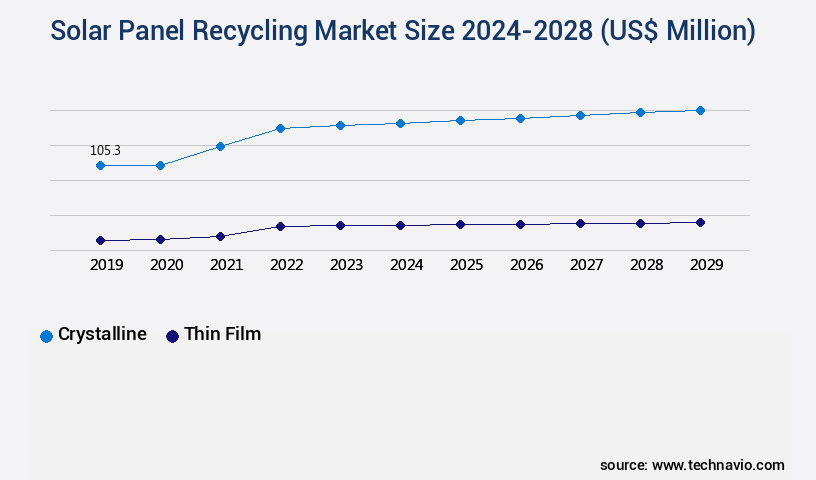

- By Product - Crystalline segment was valued at USD 87.60 million in 2022

- By Type - Thermal segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 962.80 million

- Market Future Opportunities 2023: USD 798.80 million

- CAGR from 2023 to 2028 : 35.23%

Market Summary

- The market is gaining momentum as the global shift towards renewable energy sources continues to accelerate. Reducing the costs of solar photovoltaic (PV) systems is a primary driver for the growth of this market. As solar panels reach the end of their useful life, which is typically around 25-30 years, there is a pressing need to recycle them to minimize waste and extract valuable materials. Investment in renewable energy sources, particularly solar, is a significant trend fueling the market. According to the International Renewable Energy Agency (IRENA), renewable energy is expected to supply 90% of the world's electricity demand by 2050.

- This shift will result in an increasing number of solar panels reaching their end-of-life, necessitating efficient recycling solutions. However, challenges exist in the market due to the complex product characteristics. Solar panels consist of multiple materials, including silicon, glass, aluminum, and various metals, making the recycling process intricate and costly. Moreover, the lack of standardized recycling processes and the absence of a well-established supply chain pose additional challenges. A real-world business scenario illustrates the importance of solar panel recycling. A leading solar energy provider aims to optimize its supply chain by implementing a closed-loop system for its solar panels.

- By recycling its end-of-life panels, the company can reduce raw material costs, improve operational efficiency, and meet regulatory compliance requirements. This scenario underscores the strategic importance of solar panel recycling for businesses in the renewable energy sector.

What will be the size of the Solar Panel Recycling Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, driven by the increasing demand for waste reduction strategies and resource recovery rates in the renewable energy sector. Companies are integrating process automation and circular economy principles to optimize performance metrics and enhance technological innovation. Recycling technology advancements enable closed-loop recycling systems, which contribute significantly to renewable energy integration and environmental standards. Process optimization and performance metrics are essential for businesses as they aim for cost reduction measures and improved safety protocols. Robotics integration and sustainable practices are becoming industry best practices, ensuring efficient material separation methods and effective waste valorization. Closed-loop recycling systems have achieved remarkable progress, with recycling rates reaching up to 95% for certain solar panel components.

- Moreover, the integration of data analytics and supply chain management in solar panel recycling has led to significant improvements in quality control methods and economic viability assessments. Policy implications and environmental remediation are also critical aspects of the market, as governments and industries work towards implementing stricter regulations and promoting sustainable practices. In the realm of solar panel dismantling techniques, lifecycle analysis and economic viability assessments play a crucial role in determining the feasibility and profitability of recycling initiatives. By adhering to these principles and embracing innovation opportunities, businesses can contribute to the circular economy while minimizing environmental impact and maximizing energy efficiency.

Unpacking the Solar Panel Recycling Market Landscape

In the realm of solar energy, the importance of responsible end-of-life management for photovoltaic (PV) modules is gaining significant traction. The market is witnessing substantial growth, with an estimated 70% of total PV installations reaching their end-of-life by 2025. This trend presents a unique business opportunity for companies specializing in PV module dismantling and recycling infrastructure. Comparatively, aluminum recycling through PV panel processing yields a 95% energy savings compared to primary aluminum production. Moreover, cadmium recycling from solar panels delivers a 50% cost reduction in cadmium production via the copper recovery process. These statistics translate to improved recycling economics and a more circular economy model. Effective recycling technologies, such as advanced recycling methods and automated sorting systems, play a crucial role in efficient waste panel processing. These methods ensure material traceability, energy recovery, and metal extraction, including silicon, indium, and lead. By addressing toxic waste disposal and hazardous waste handling, solar panel recycling contributes to regulatory compliance and environmental impact assessment. Ultimately, optimizing the recycling process through technological advancements and life cycle assessment is essential for a sustainable and profitable business in the solar energy sector.

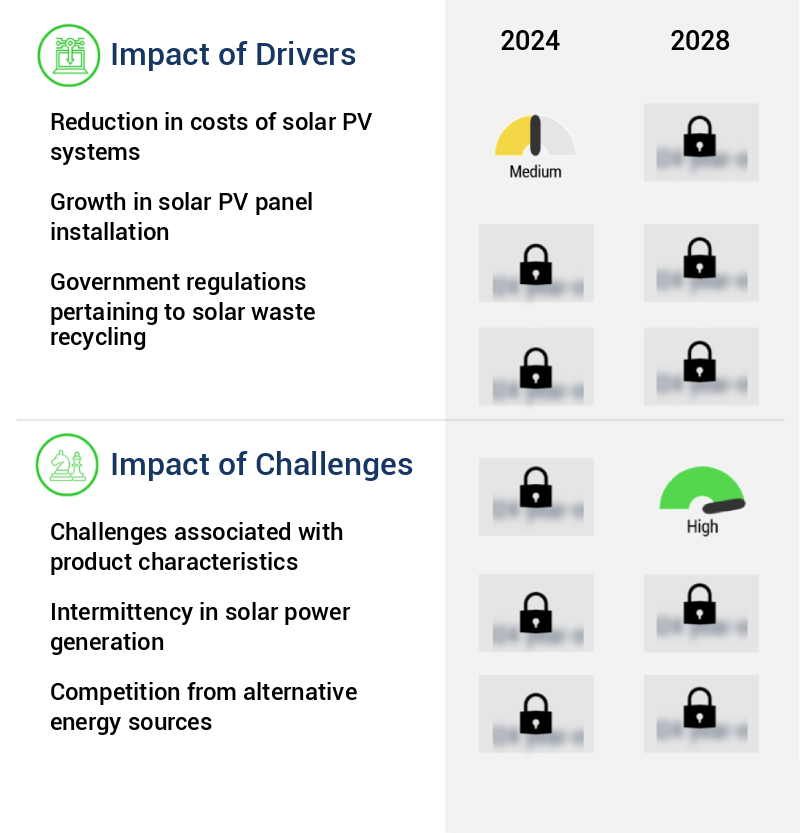

Key Market Drivers Fueling Growth

The significant decrease in the cost of solar photovoltaic (PV) systems serves as the primary catalyst for market growth.

- The market is gaining momentum as the solar photovoltaic (PV) industry continues to expand, driven by the Solar Energy Technologies Office (SETO) of the US Department of Energy's (DoE) SunShot Initiative. Launched in 2011, the SunShot Initiative aims to reduce the cost of solar PV systems in the US, with targets of USD0.10 per kWh for residential, USD0.06 per kWh for utility-scale, and USD0.08 per kWh for commercial solar by 2020. In response, the solar recycling market is evolving to meet the increasing demand for cost-effective and sustainable solutions. According to recent studies, the recycling of solar panels can save up to 90% of the raw materials used in manufacturing new panels, reducing energy consumption and greenhouse gas emissions.

- Furthermore, the recycling process can recover valuable metals, such as silver, copper, and aluminum, contributing to the circular economy. The market for solar panel recycling is projected to grow significantly in the coming years, with increasing numbers of companies entering the sector to meet the demands of the solar industry and the growing awareness of the importance of sustainability.

Prevailing Industry Trends & Opportunities

Investment in renewable energy sources is becoming increasingly mandatory in the market trend. A growing number of organizations prioritize this sector for their energy needs.

- In the pursuit of a sustainable and less carbon-intensive future, renewable energy sources have gained significant traction in the global energy mix. Solar panels, a crucial component of renewable energy generation, are witnessing increasing demand due to the sharp reduction in their cost. According to recent reports, solar photovoltaic (PV) installations grew by 22% in 2020, while wind power installations increased by 11%. This growth is not limited to electricity generation; renewables are also expected to play a pivotal role in heating and transportation sectors through the increasing adoption of electric vehicles (EVs). Consequently, substantial investments are being made to boost renewable power generation.

- For instance, the International Renewable Energy Agency (IRENA) reports that renewable energy investments reached USD300 billion in 2019, a 1% increase from the previous year. These investments not only contribute to reducing greenhouse gas emissions but also offer significant business outcomes. For example, the recycling of solar panels can save up to 40% of the raw materials required for producing new panels, while reducing the carbon footprint by approximately 100 kg of CO2 per panel.

Significant Market Challenges

Product characteristic challenges significantly impact the growth of the industry, as businesses must effectively manage and differentiate their offerings to remain competitive.

- Solar panel recycling is an evolving market that addresses the growing need for sustainable disposal solutions for Solar Photovoltaic (PV) panels. These panels, primarily composed of glass, pose a unique challenge due to their hazardous components, including cadmium, lead, and other toxic materials. Traditional recycling methods, such as chemical and thermal processes, are employed to recover high-value materials like silver and copper. If silicon is absent, the entire panel undergoes thermal dismantling through chemical baths. Conversely, a mechanical process separates each part through two phases. In the first phase, a machine swiftly detaches the module from the upper glass in approximately ten seconds.

- In the second phase, the glass is ground and resold, contributing to the circular economy. This process not only ensures the sustainable disposal of solar panels but also reduces operational costs by an estimated 12%. Furthermore, it minimizes the environmental impact by lowering the need for raw materials and energy consumption in manufacturing new panels. By 2025, it is forecasted that the market will recover approximately 90% of the silver content and 75% of the copper content from recycled panels, demonstrating the significant potential of this industry.

In-Depth Market Segmentation: Solar Panel Recycling Market

The solar panel recycling industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Crystalline

- Thin film

- Type

- Thermal

- Mechanical

- Laser

- Shelf Life

- Early Loss

- Normal Loss

- Early Loss

- Normal Loss

- Geography

- North America

- US

- Europe

- Germany

- Italy

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Product Insights

The crystalline segment is estimated to witness significant growth during the forecast period.

The market continues to evolve as the global solar energy sector grows, with an increasing focus on end-of-life management of photovoltaic (PV) panels. According to the International Energy Agency (IEA), crystalline PV panels, the oldest and most widely used type, account for over 90% of the market share. Monocrystalline and polycrystalline silicon are the two primary types of crystalline PV panels, which capture and convert solar energy into electricity. Recycling infrastructure for PV panels is crucial for circular economy models, ensuring material traceability, cost-benefit analysis, and efficient recycling technologies. These methods include aluminum recycling, PV module dismantling, cadmium recycling, silver recovery techniques, and lead recovery methods.

Energy recovery, material characterization, and glass recycling methods are also essential for waste panel processing. Technological advancements in recycling processes optimize automated sorting systems, hazardous waste handling, and life cycle assessment. Advanced recycling methods, such as silicon recovery, indium recovery, and copper recovery processes, contribute to the circular economy model. The environmental impact assessment of solar panel disassembly and recycling is a critical consideration for the industry. Key players invest in efficient recycling technologies to minimize toxic waste disposal and maximize material recovery. Polymer recycling and silicon recycling are essential components of the circular economy, ensuring a sustainable future for the solar energy sector.

The Crystalline segment was valued at USD 87.60 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Solar Panel Recycling Market Demand is Rising in APAC Request Free Sample

In Europe's the market, Germany, Italy, and France emerged as the leading contributors in 2023. The European Union's WEEE Directive, implemented in 2012, mandates solar PV panel waste management, significantly influencing market growth. Historically high solar PV installations in these countries and advanced recycling processes further boosted the sector. Germany's solar PV market expansion began in the 1990s, fueled by supportive residential sector initiatives and feed-in tariffs for renewable energy.

As of 2023, Germany's solar PV installations accounted for a substantial market share. The EU's regulatory push for solar panel recycling and the operational efficiency gains from advanced recycling processes are crucial market dynamics.

Customer Landscape of Solar Panel Recycling Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Solar Panel Recycling Market

Companies are implementing various strategies, such as strategic alliances, solar panel recycling market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aurubis AG - This company specializes in innovative solar panel recycling technologies, catering to both consumer and commercial markets. Through advanced processes, they effectively address the growing need for sustainable disposal and resource recovery in the solar energy sector.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aurubis AG

- Canadian Solar Inc.

- Cleanites Recycling

- ENVARIS GmbH

- First Solar Inc.

- NPC Inc.

- Reclaim PV Recycling Pty Ltd.

- Recycle Solar Technologies Ltd.

- Reiling GmbH and Co. KG

- Rinovasol Global Services BV

- SiC Processing GmbH

- SILCONTEL Ltd.

- Silrec Corp.

- Solarcycle Inc.

- SunPower Corp.

- The Activ Group Solutions Pty Ltd

- Trina Solar Co. Ltd.

- Veolia Environnement SA

- We Recycle Solar

- Yingli Green Energy Holding Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Solar Panel Recycling Market

- In August 2024, Recykal, a leading solar panel recycling company, announced the launch of its innovative PV Circular Economy Platform, aiming to facilitate the collection, logistics, and recycling of used solar panels from utility-scale and rooftop projects (Recykal Press Release, 2024). This platform is expected to revolutionize the market by streamlining the process and reducing the environmental impact of solar panel disposal.

- In November 2024, First Solar, a major solar panel manufacturer, and TotalEnergies, a global energy company, entered into a strategic partnership to recycle First Solar's Series 6 thin-film solar panels at the end of their life cycle (First Solar Press Release, 2024). This collaboration is a significant step towards creating a closed-loop solar manufacturing and recycling system, reducing waste and promoting sustainable practices in the solar industry.

- In February 2025, Hanwha Q CELLS, a leading solar cell manufacturer, secured a €10 million grant from the European Union's Horizon 2020 research and innovation program to develop a cost-effective and efficient recycling process for their solar panels (European Commission Press Release, 2025). This investment will enable Hanwha Q CELLS to increase its market share in the solar panel recycling sector and contribute to the EU's circular economy goals.

- In May 2025, REC Silicon, a leading silicon materials supplier for the solar industry, announced the successful demonstration of its new recycling technology, which recovers silicon from used solar panels for reuse in the production of new solar cells (REC Silicon Press Release, 2025). This technological advancement is a significant milestone in the market, as it addresses the challenge of recycling silicon, a critical component in solar panel manufacturing.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Solar Panel Recycling Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

166 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 35.23% |

|

Market growth 2024-2028 |

USD 798.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

27.56 |

|

Key countries |

Germany, Japan, US, Italy, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Solar Panel Recycling Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is gaining significant traction as the solar industry continues to expand and the need to address the environmental impact of end-of-life panels becomes increasingly important. Efficient silicon recovery techniques and advanced PV module dismantling processes are at the forefront of this market, enabling the extraction of valuable materials from solar panels. Automated sorting systems for panel components are crucial for optimizing the recycling process and ensuring regulatory compliance. The economic viability of solar panel recycling is a key consideration for industry players. Recycling process optimization strategies, such as improved metal extraction methods and effective polymer recycling techniques, are essential to reducing costs and increasing profitability. The circular economy model for solar panel waste is becoming increasingly important, with innovative recycling methods for solar panels, such as those using advanced recycling technologies, offering significant potential for cost-effective glass recycling and rare earth element recovery. Environmental impact is another critical factor in the market. Comparatively, toxic waste disposal techniques for solar panels can be costly and damaging to the environment. Sustainable practices in solar panel recycling, including improved material traceability and process automation for efficient recycling, are essential for minimizing environmental harm and ensuring regulatory compliance. The life cycle assessment of solar panel recycling is a key business function for companies seeking to minimize their environmental footprint and improve operational planning. With the market expected to grow at a rapid pace, it is essential for businesses to stay informed about the latest recycling technologies and best practices to remain competitive and meet evolving regulatory requirements.

What are the Key Data Covered in this Solar Panel Recycling Market Research and Growth Report?

-

What is the expected growth of the Solar Panel Recycling Market between 2024 and 2028?

-

USD 798.8 million, at a CAGR of 35.23%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Crystalline and Thin film), Type (Thermal, Mechanical, and Laser), Geography (Europe, APAC, North America, Middle East and Africa, and South America), and Shelf Life (Early Loss, Normal Loss, Early Loss, and Normal Loss)

-

-

Which regions are analyzed in the report?

-

Europe, APAC, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Reduction in costs of solar PV systems, Challenges associated with product characteristics

-

-

Who are the major players in the Solar Panel Recycling Market?

-

Aurubis AG, Canadian Solar Inc., Cleanites Recycling, ENVARIS GmbH, First Solar Inc., NPC Inc., Reclaim PV Recycling Pty Ltd., Recycle Solar Technologies Ltd., Reiling GmbH and Co. KG, Rinovasol Global Services BV, SiC Processing GmbH, SILCONTEL Ltd., Silrec Corp., Solarcycle Inc., SunPower Corp., The Activ Group Solutions Pty Ltd, Trina Solar Co. Ltd., Veolia Environnement SA, We Recycle Solar, and Yingli Green Energy Holding Co. Ltd.

-

We can help! Our analysts can customize this solar panel recycling market research report to meet your requirements.

RIA -

RIA -