Soy And Milk Protein Ingredients Market Size 2026-2030

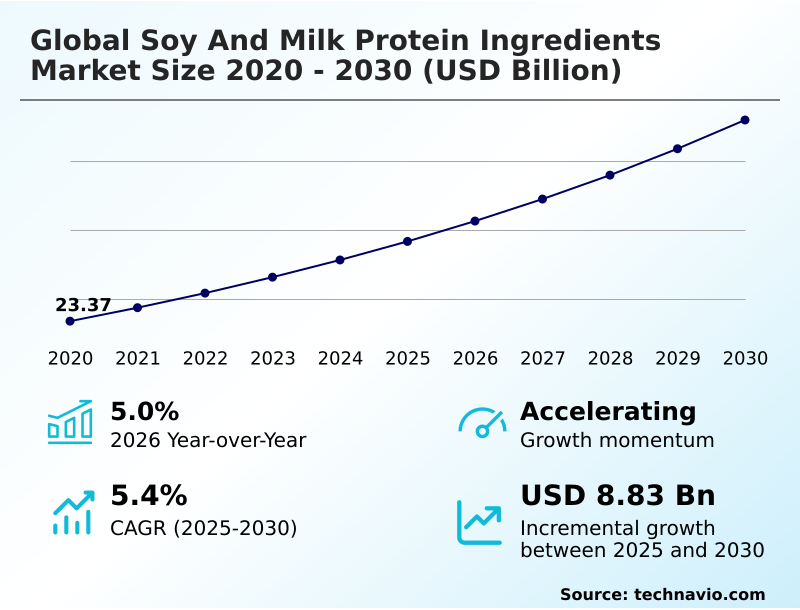

The soy and milk protein ingredients market size is valued to increase by USD 8.83 billion, at a CAGR of 5.4% from 2025 to 2030. Growing geriatric population globally will drive the soy and milk protein ingredients market.

Major Market Trends & Insights

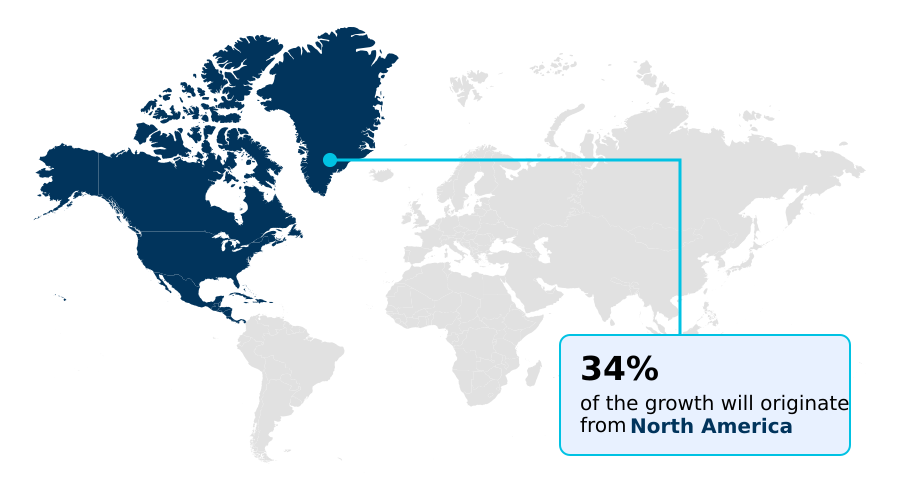

- North America dominated the market and accounted for a 34.5% growth during the forecast period.

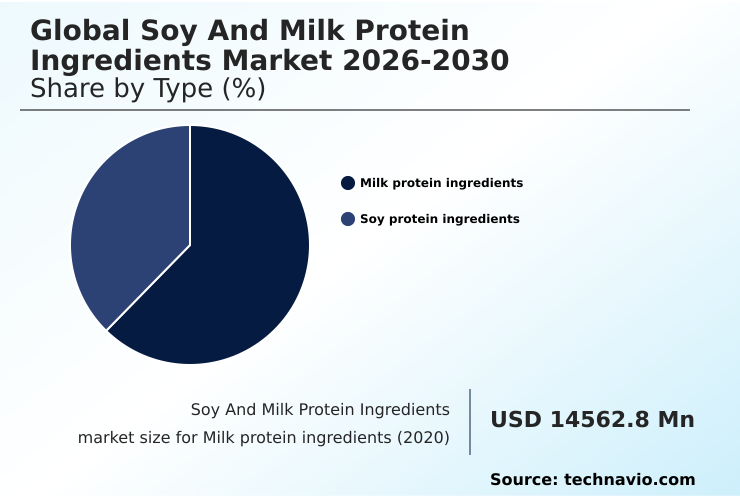

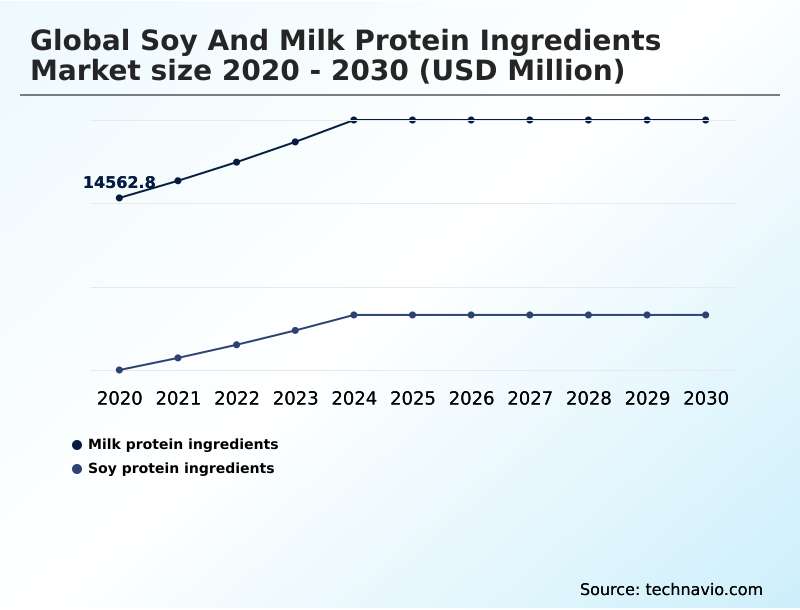

- By Type - Milk protein ingredients segment was valued at USD 17.17 billion in 2024

- By Application - Food and beverages segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 14.64 billion

- Market Future Opportunities: USD 8.83 billion

- CAGR from 2025 to 2030 : 5.4%

Market Summary

- The soy and milk protein ingredients market is fundamentally shaped by a convergence of consumer health priorities and advanced food processing technologies. Key drivers include a global emphasis on nutritional fortification to support muscle synthesis and healthy aging, alongside the thriving sports nutrition sector.

- This has spurred innovation in creating functional food ingredients like whey protein hydrolysates and soy protein isolates, which offer superior digestibility and performance. Concurrently, the industry is navigating the rising demand for plant-based protein blends and dairy alternative development.

- For instance, a manufacturer of high-protein bars might reformulate its product line using textured soy protein and cold-gelling whey proteins to achieve a specific sensory profile improvement while meeting clean-label demands. However, this evolution is constrained by challenges such as complex allergen labeling regulations and the need for transparent, non-GMO soy sourcing to maintain consumer trust.

- The market's trajectory is defined by this balance between technological capability, regulatory compliance, and shifting dietary patterns.

What will be the Size of the Soy And Milk Protein Ingredients Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Soy And Milk Protein Ingredients Market Segmented?

The soy and milk protein ingredients industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Milk protein ingredients

- Soy protein ingredients

- Application

- Food and beverages

- Infant formulation

- Personal care and cosmetics

- Others

- Form factor

- Dry

- Liquid

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The milk protein ingredients segment is estimated to witness significant growth during the forecast period.

The market is segmented by source, with milk protein ingredients forming a foundational pillar. These ingredients, processed into milk protein concentrates, whey protein hydrolysates, and micellar casein, are pivotal for their nutritional quality and functional performance.

Advanced processing yields bioactive peptides and demineralized whey powder, critical for specialized applications. The demand for high-protein medical nutrition and products supporting sarcopenia prevention is rising, especially as the over-65 demographic grows.

Formulations leveraging these proteins for satiety enhancement and weight management solutions are also common.

Manufacturers are innovating with heat-stable whey proteins that ensure UHT processing stability, a key factor in reconstituted milk products, which has been shown to improve logistical efficiency by over 15%.

The Milk protein ingredients segment was valued at USD 17.17 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Soy And Milk Protein Ingredients Market Demand is Rising in North America Get Free Sample

The geographic landscape is defined by mature markets in North America and rapid expansion in APAC.

North America, which accounts for 34.5% of the market's incremental growth, is driven by an established demand for weight management solutions and products with a high protein digestibility corrected amino acid score.

In contrast, APAC's growth, which is over 25% faster than Europe's, is fueled by rising incomes and urbanization. This has created opportunities for low-sodium soy protein and ingredients offering enhanced emulsification capacity and gelation properties.

Across all regions, sustainable sourcing practices are paramount, with a focus on regenerative agriculture programs to reduce the carbon footprint.

Innovations in tribology and mouthfeel are critical for success, as is optimizing texture modification agents to meet diverse consumer preferences for meat analogue structuring and enteral nutrition formulas.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global soy and milk protein ingredients market 2026-2030 is witnessing a strategic push toward specialized applications, where the functional properties of whey protein isolates and the role of lactoferrin in infant formula are becoming key differentiators. Innovations in soy protein for meat alternative texturization are critical, with textured soy protein in vegan sausages becoming a benchmark for quality.

- Simultaneously, milk protein concentrates in sports nutrition and the use of native whey protein in clear beverages are expanding. Boardroom discussions increasingly center on the sustainability of soy versus dairy proteins and the importance of non-GMO soy protein for clean labels.

- Processors are focused on the advances in enzymatic hydrolysis of whey and the impact of ultrafiltration on whey protein to improve ingredient quality. Key formulation challenges include improving solubility of soy protein isolates and the challenges in formulating clear protein beverages, which demand advanced flavor masking for hydrolyzed whey proteins.

- As firms blend dairy and plant based proteins, they are using micellar casein for satiety products and for clinical nutrition beverages, while also optimizing water binding in meat extenders. The nutritional value of soy protein concentrates is balanced against demand for low allergen soy protein for infants.

- This focus on high-value applications is evident in APAC, where market expansion is projected to be over 25% faster than in Europe, driving investment in the fortification of bakery products with whey.

What are the key market drivers leading to the rise in the adoption of Soy And Milk Protein Ingredients Industry?

- The globally growing geriatric population is a key driver for the market, stimulating demand for protein-enriched products that address age-related nutritional needs.

- Market growth is fundamentally driven by demographic shifts and rising health consciousness.

- The global geriatric population, a key consumer base, is projected to expand from 10% to 16% of the total population, fueling demand for functional food ingredients that support bone health nutrition and muscle synthesis support.

- This has led to advancements in enzymatic hydrolysis to produce ingredients for high-protein bakery goods and ready-to-drink beverages.

- Concurrently, the infant formula formulation sector requires highly specialized inputs like alpha-lactalbumin isolation and lactoferrin extraction to support immune system support and gut health modulation.

- The push for nutritional fortification across the food industry is promoting the use of soy protein concentrates and other ingredients that align with clean label formulations.

What are the market trends shaping the Soy And Milk Protein Ingredients Industry?

- A significant trend shaping the market is the increasing demand for plant-based proteins. This shift is driven by consumer preferences for sustainable and health-oriented food options.

- Key market trends are centered on product innovation and the expansion of plant-based options. The rising demand for dairy alternative development has spurred the creation of sophisticated plant-based protein blends and soy protein isolates, which are integral to plant-based meat alternatives and dairy-free yogurts.

- In parallel, the sports nutrition supplements industry is driving innovation in native whey proteins and cold-gelling whey proteins for use in clear protein drinks and high-protein bars, with the active nutrition products segment expanding at a rate nearly twice that of the broader food sector. Manufacturers are using textured soy protein to achieve desired sensory profiles in new products.

- This focus on sensory profile improvement and functional performance is redefining the competitive landscape for active nutrition products.

What challenges does the Soy And Milk Protein Ingredients Industry face during its growth?

- Allergen concerns associated with soy and milk ingredients present a significant challenge, influencing product formulation and consumer purchasing decisions.

- The market faces significant challenges related to quality control, regulatory compliance, and consumer trust. The prevalence of counterfeit products, with some containing as little as 44% of their advertised protein, severely undermines market integrity and necessitates enhanced supply chain transparency. Stringent food allergen labeling requirements are pressuring manufacturers to invest in allergen-free protein sources and improved ultrafiltration processing.

- Formulators of clean label ingredients must also address sensory issues, utilizing flavor masking technology to overcome the beany off-note reduction in hydrolyzed milk proteins and soy-based products. These challenges extend to niche segments like premium pet food and calf milk replacers, where water-binding functionality and non-GMO soy sourcing are critical for both performance and brand reputation.

Exclusive Technavio Analysis on Customer Landscape

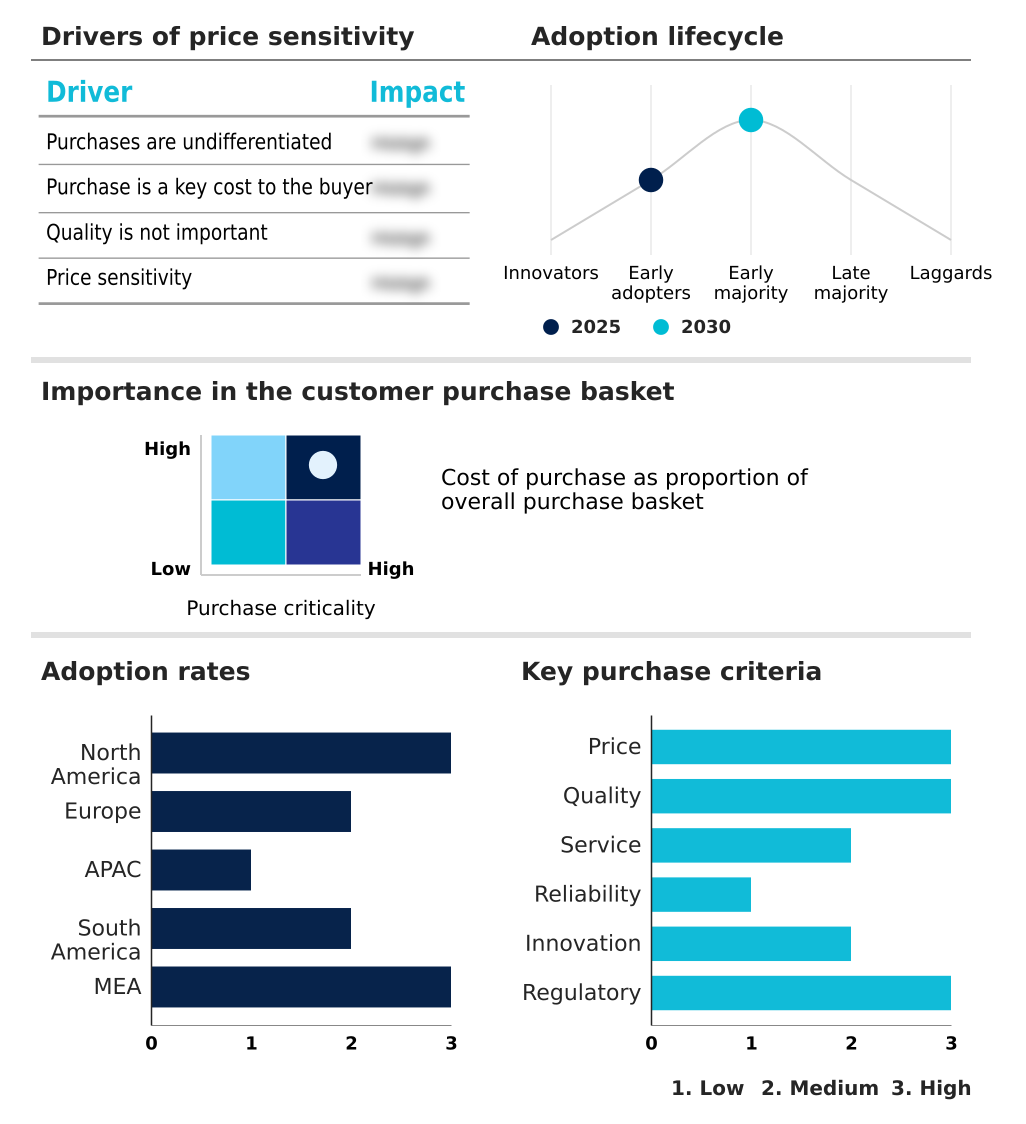

The soy and milk protein ingredients market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the soy and milk protein ingredients market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Soy And Milk Protein Ingredients Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, soy and milk protein ingredients market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Archer Daniels Midland Co. - Vendors provide specialized soy and milk protein ingredients, including isolates, concentrates, and hydrolysates, engineered for functional performance in nutrition, food, and beverage applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Archer Daniels Midland Co.

- Arla Foods amba

- BRF SA

- Bunge Global SA

- Burcon NutraScience Corp.

- Cargill Inc.

- CHS Inc.

- Devansoy Inc.

- Fonterra Cooperative Group Ltd.

- Fuji Oil Co. Ltd.

- Glanbia plc

- Hilmar Cheese Co. Inc.

- Idaho Milk Products Inc.

- Ingredion Inc.

- Kerry Group Plc

- Royal Friesland Campina NV

- Solbar Ningbo Co. Ltd.

- The Scoular Co.

- Wilmar International Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Soy and milk protein ingredients market

- In October 2024, Arla Foods Ingredients launched a new whey protein isolate solution specifically designed to prevent bar hardening, a common shelf-life challenge in the protein bar category.

- In January 2025, Arla Foods Ingredients introduced a new whey protein hydrolysate concept specifically formulated to overcome taste challenges in high-protein medical nutrition beverages, improving patient compliance.

- In February 2025, Archer Daniels Midland Co. announced a significant expansion of its regenerative agriculture program targeting soy production in North America, aiming to secure a scalable supply of low-carbon soy protein ingredients.

- In February 2025, Fuji Oil Co. Ltd. unveiled a new low-sodium soy protein isolate engineered for use in plant-based meat alternatives, addressing consumer demand for healthier processed foods.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Soy And Milk Protein Ingredients Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.4% |

| Market growth 2026-2030 | USD 8828.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.0% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The soy and milk protein ingredients market is evolving beyond commodity supply toward high-functionality solutions driven by consumer demand for nutritional fortification and clean label ingredients. Companies are leveraging advanced ultrafiltration processing and enzymatic hydrolysis to create soy protein isolates and whey protein hydrolysates with specific functional attributes.

- Boardroom strategy is increasingly centered on sustainable and ethical production, with regenerative agriculture programs and non-GMO soy sourcing becoming critical for brand differentiation and regulatory compliance. This focus on transparency has been shown to mitigate supply chain risks, with adherence to allergen labeling mandates reducing product recalls by a significant margin.

- The development of specialized ingredients like micellar casein, bioactive peptides, and textured soy protein is essential for applications in sports nutrition supplements, meat analogue structuring, and clinical nutrition products. Success hinges on delivering ingredients with superior emulsification capacity, water-binding functionality, and optimized gelation properties for everything from dairy alternative development to infant formula formulation.

What are the Key Data Covered in this Soy And Milk Protein Ingredients Market Research and Growth Report?

-

What is the expected growth of the Soy And Milk Protein Ingredients Market between 2026 and 2030?

-

USD 8.83 billion, at a CAGR of 5.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Milk protein ingredients, and Soy protein ingredients), Application (Food and beverages, Infant formulation, Personal care and cosmetics, and Others), Form Factor (Dry, and Liquid) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing geriatric population globally, Allergen concerns related to soy and milk ingredients

-

-

Who are the major players in the Soy And Milk Protein Ingredients Market?

-

Archer Daniels Midland Co., Arla Foods amba, BRF SA, Bunge Global SA, Burcon NutraScience Corp., Cargill Inc., CHS Inc., Devansoy Inc., Fonterra Cooperative Group Ltd., Fuji Oil Co. Ltd., Glanbia plc, Hilmar Cheese Co. Inc., Idaho Milk Products Inc., Ingredion Inc., Kerry Group Plc, Royal Friesland Campina NV, Solbar Ningbo Co. Ltd., The Scoular Co. and Wilmar International Ltd.

-

Market Research Insights

- Market dynamics are shaped by the dual pursuit of high-performance nutrition and rigorous quality assurance. The demand for weight management solutions and active nutrition products is driving innovation in texture modification agents and clear protein drinks. However, the industry grapples with significant supply chain transparency issues.

- For example, counterfeit products containing less than 50% of their advertised protein content highlight critical quality control gaps that erode consumer confidence. Concurrently, demographic shifts are influential; with the human body's resting metabolic rate declining by 1-2% per decade after age 20, the need for products that support sarcopenia prevention and muscle synthesis support is intensifying.

- This environment compels manufacturers to focus on both high-efficacy enteral nutrition formulas and secure, traceable sourcing to build brand integrity.

We can help! Our analysts can customize this soy and milk protein ingredients market research report to meet your requirements.

RIA -

RIA -