Soybean Derivatives Market Size 2025-2029

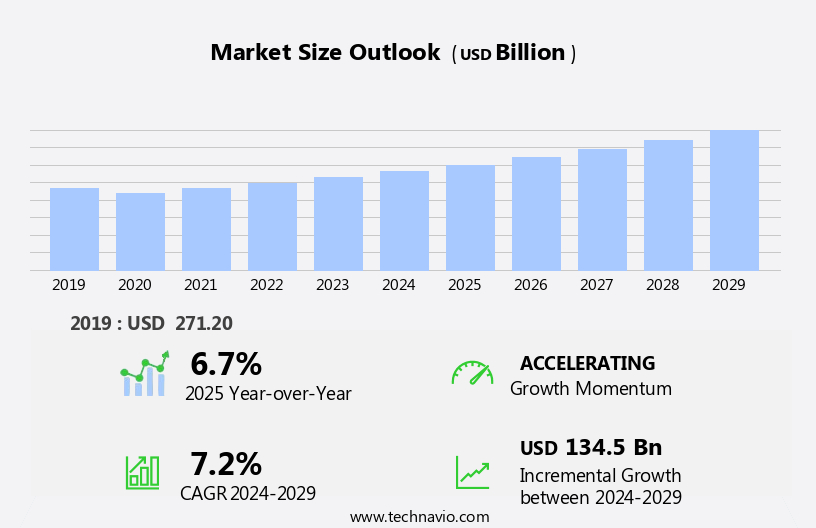

The soybean derivatives market size is forecast to increase by USD 134.5 billion, at a CAGR of 7.2% between 2024 and 2029.

- The market is experiencing significant growth due to the rising demand from lactose-intolerant and vegan consumers for alternative sources of protein. These consumers are increasingly turning to soybean derivatives, such as soy protein isolates and textured vegetable protein, as substitutes for dairy and meat products. Additionally, the animal feed industry is a major consumer of soybean derivatives, with soybean meal being a primary source of protein for livestock. However, the market faces challenges from the presence of soybean substitutes, such as pea and sunflower protein, which offer similar nutritional benefits. These substitutes are gaining popularity due to their lower environmental impact and potential for higher yields. Soybean derivatives, such as soy milk and tofu, are popular alternatives to dairy products and meat, respectively

- Furthermore, the volatility of soybean prices and trade policies, such as tariffs and quotas, can significantly impact the market's dynamics. Companies in the market must navigate these challenges by focusing on product innovation, sustainability, and supply chain efficiency to remain competitive. Additionally, the use of soybeans in animal feed is another growth factor. For instance, developing new applications for soybean derivatives in the food and beverage industry, improving production processes to reduce waste and increase yields, and exploring new markets and partnerships can help companies capitalize on market opportunities and mitigate risks.

What will be the Size of the Soybean Derivatives Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The market encompasses a wide range of applications and products, from soybean yield optimization and hull applications to soy meal composition and protein concentrates. Soybean cultivation practices continue to evolve, with a focus on disease management and sustainability practices. In the realm of product development, soybean ingredient innovation is driving the creation of new grades of soy lecithin and protein isolates. In the food industry, soy derivatives are used as functional ingredients in various applications, including baked goods, beverages, and processed food.

- Soybean pest resistance and environmental footprint are also critical factors influencing market dynamics. As the demand for sustainable and high-performing soybean derivatives continues to grow, so too will the innovation and collaboration within the industry. Industry collaborations and regulatory compliance are shaping the soybean industry landscape, with a growing emphasis on traceability systems and GMO labeling. Additionally, the market is expanding in sectors such as biodiesel due to the renewable nature of soy oil and its potential to reduce greenhouse gas emissions.

How is this Soybean Derivatives Industry segmented?

The soybean derivatives industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

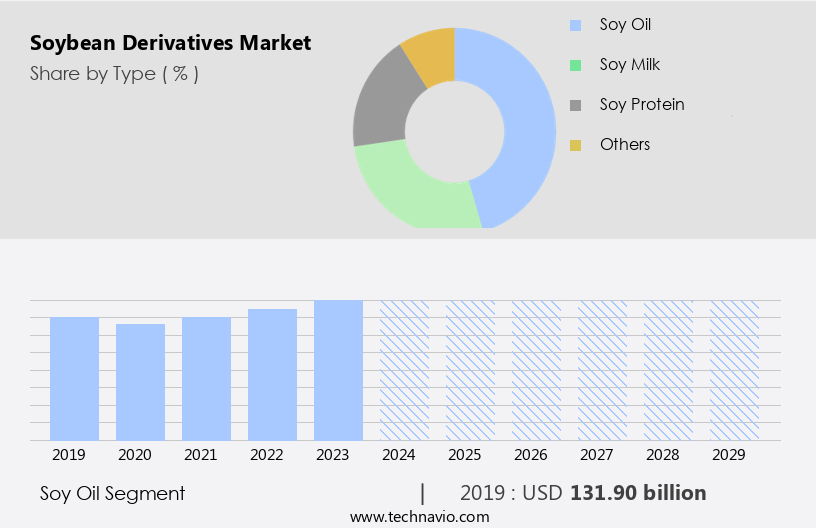

- Type

- Soy oil

- Soy milk

- Soy protein

- Others

- Distribution Channel

- Offline

- Online

- Application

- Food and beverage

- Animal feed

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Indonesia

- Japan

- South America

- Argentina

- Brazil

- Colombia

- Rest of World (ROW)

- North America

By Type Insights

The soy oil segment is estimated to witness significant growth during the forecast period. Soybean oil, derived from soybean processing, is a popular choice for health-conscious consumers due to its nutritional benefits. Rich in unsaturated fats, essential fatty acids, and vitamin E, soybean oil is a preferred cooking oil for various applications, including frying, sautéing, baking, and salad dressings. The environmental sustainability of soybean cultivation and the versatility of soybean derivatives have contributed to their increasing use in various industries. Soybean-based ingredients, such as soybean flakes, grits, and meal, have gained popularity in the animal feed industry due to their high nutritional value and protein content. Soybean meal is a valuable byproduct of soybean oil refining and is a primary source of protein for livestock. It is used as an emulsifier and stabilizer in various industries, including food, pharmaceuticals, and cosmetics.

Soybean sustainability is a critical concern for consumers and manufacturers alike, leading to an increased focus on sustainable sourcing and production practices. Soybean genetics and processing techniques are continually evolving to improve yield, quality, and sustainability. The market is diverse and dynamic, with applications ranging from food and animal feed to industrial and pharmaceutical uses. Soybean pest control and food safety standards are essential considerations in the production and distribution of soybean derivatives. Allergen concerns and GMO concerns are also important factors that influence the market dynamics. The market is a significant and growing industry, driven by the nutritional benefits, functional properties, and sustainability of soybean derivatives. From soybean oil refining to soybean cultivation, the entire soybean supply chain is continually evolving to meet the demands of various industries and consumers.

The Soy oil segment was valued at USD 131.90 billion in 2019 and showed a gradual increase during the forecast period.

The Soybean Derivatives Market is expanding due to increasing soybean demand in diverse food applications. Enhanced soybean extraction techniques improve yield and efficiency, ensuring optimal soybean quality for various uses. The development of soy protein concentrate and soy protein hydrolysate enables better nutrition and functional benefits in food formulations. Innovations in soy protein modification enhance texture and solubility, catering to evolving consumer preferences. Advancements in soybean disease resistance promote sustainable cultivation, reducing losses and improving productivity. Furthermore, soybean traceability ensures quality control and regulatory compliance throughout the supply chain. Continuous soybean innovation drives market growth, leading to superior products and expanded applications, making soybean derivatives a staple in global food production and nutrition solutions.

In the food industry, soybean derivatives are used for protein fortification and the production of functional foods. Soy protein isolate, concentrate, and hydrolysate are commonly used in food fortification and the production of plant-based meat alternatives. Functional properties, such as emulsification and texture enhancement, make soybean derivatives an essential ingredient in various industries. Soy lecithin, a phospholipid extracted from soybean oil, is widely used as an emulsifier and stabilizer in food and pharmaceutical applications. Soybean research continues to explore the potential of soybean derivatives in various industries, including biofuel production and disease resistance. The demand for soybean derivatives is driven by their nutritional value, functional properties, and sustainability.

Regional Analysis

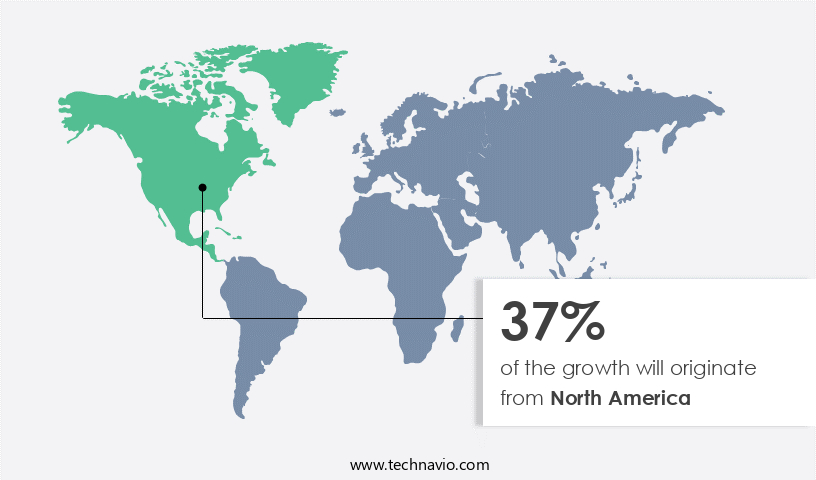

North America is estimated to contribute 37% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America experiences continuous growth due to the abundant production of soybeans and favorable agricultural conditions. This plentiful supply chain supports the production of various soybean derivatives such as soy protein, soybean oil, and soy-based ingredients. The increasing trend toward plant-based diets and the preference for plant-derived protein sources have significantly boosted the demand for these derivatives. Furthermore, the food industry's ongoing innovations, including the development of new soy-based products and formulations, catering to evolving consumer preferences, fuel regional market growth. Additionally, the consumption of processed and convenience foods, which frequently incorporate soybean derivatives as ingredients, further supports market expansion.

Soybean research advances disease resistance and functional properties, enhancing the nutritional value of these derivatives. Animal feed applications, biofuel production, food fortification, and food safety standards also contribute to the market's growth. The soybean supply chain's sustainability, including sustainable sourcing and yield optimization, addresses environmental concerns and consumer expectations. Soybean genetics and processing technologies enable protein modification, hydrolysis, and fiber production, expanding the market's scope. Despite GMO concerns, the market continues to adapt and innovate, addressing the diverse needs of various industries. The market's size is substantial, with continued growth driven by the increasing popularity of plant-based protein and the expanding use of soy derivatives in various industries.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Soybean Derivatives market drivers leading to the rise in the adoption of Industry?

- The surging interest from lactose-intolerant and vegan consumers for soybean derivatives serves as the primary catalyst for market growth. The market is experiencing significant growth due to the rising demand for lactose-free alternatives to dairy products. Soybean derivatives, such as soy milk, offer a viable solution for individuals with lactose intolerance, a condition that affects a large population in European countries, including Italy, Germany, Spain, Turkey, Poland, France, and the UK. Symptoms of lactose intolerance include bloating, cramps, diarrhea, and nausea. Soybean derivatives are produced from soy oil, a byproduct of soybean processing. The quality of soybeans is crucial in ensuring the production of high-quality soy oil and derivatives. Soybean genetics play a significant role in determining the yield and quality of soybeans.

- However, genetically modified organism (GMO) concerns have emerged in recent years, which may impact the market dynamics. Soybean protein modification is another trend in the market, with companies exploring ways to enhance the nutritional value and functional properties of soy protein. Sustainable sourcing is also a critical factor in the market, as consumers increasingly demand products produced using environmentally friendly practices. Soybean futures and pricing play a significant role in the market's growth. The market is expected to continue its upward trajectory during the forecast period, driven by the increasing demand for soybean derivatives as lactose-free alternatives.

What are the Soybean Derivatives market trends shaping the Industry?

- Soybeans are increasingly being utilized in animal feed as a market trend. This trend reflects the growing recognition of soybeans as an effective and sustainable source of nutrition for livestock. The market encompasses various products derived from soybeans, including soybean oil, soybean-based ingredients, soybean flakes, and soybean hulls. Soybean oil is extensively used in food processing and biodiesel production. Soybean-based ingredients find applications in the food and beverage industries for protein fortification and functional properties. Soybean flakes and hulls are utilized in animal feed and industrial applications.

- The growing demand for meat and animal products, driven by population growth and rising incomes, fuels the need for soybean meal in the animal feed industry. Additionally, the increasing popularity of vegetarian and plant-based diets for livestock due to changing consumer preferences and ethical concerns further boosts the demand for soybean meal. Moreover, the rise of vegetarian and vegan diets has further boosted demand for soy-based products, including tofu, soy milk, soy flour, and protein isolates.

How does Soybean Derivatives market face challenges during its growth?

- The expansion of the soybean industry is confronted by the emergence of viable substitutes, posing a significant challenge to its growth. The market faces challenges due to the availability of alternative plant-based proteins. Soybean-based products, including soy lecithin and soybean grits, have been popular in food fortification and biofuel production. However, consumer preferences are shifting towards other plant-proteins such as pea, wheat, rice, pulse, canola, flax, and chia.

- The food and beverage industry is responding by using low-soy protein alternatives to meet consumer demands for nutritional value and food labeling transparency. Unfavorable perceptions of soy products and their potential allergens are driving producers to explore alternatives. Additionally, the high cost of soybean derivatives compared to other plant-proteins is further impeding the market's expansion. In the food industry, soybean derivatives are used in processed foods, baked goods, snacks, and dairy alternatives.

Exclusive Customer Landscape

The soybean derivatives market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the soybean derivatives market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, soybean derivatives market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ag Processing Inc. - The company specializes in soybean derivatives and provides high-quality feed ingredients for the livestock industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ag Processing Inc.

- AOS Products Pvt. Ltd.

- Archer Daniels Midland Co.

- Arpadis Group

- BASF SE

- Bunge Global SA

- Cargill Inc.

- CHS Inc

- Crown Soya Protein Group

- Fuji Oil Holdings Inc.

- Gujarat Ambuja Exports Ltd.

- Linyi Shansong Biological Products Co. Ltd.

- Nordic Soya Oy

- Olenex Sarl

- Patanjali Ayurved Ltd.

- Qingdao Foodrich Soya Tech Co. Ltd.

- Sonic Biochem Extraction Pvt. Ltd.

- The Scoular Co.

- Uday Oil Group

- Wilmar International Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Soybean Derivatives Market

- In March 2024, Cargill, a leading agricultural commodities trader, announced the launch of a new soybean derivative product, Cargill SoyCrush Derivatives, designed to help farmers and processors manage price risks in soybean crush markets (Cargill press release). This innovative product allows users to hedge against the price volatility of soybean oil and meal, thereby providing risk management solutions for the agribusiness sector.

- In July 2024, Archer Daniels Midland Company (ADM) and Bunge Limited, two major players in the market, entered into a strategic partnership to expand their origination, processing, and logistics capabilities in South America (ADM press release). This collaboration aims to strengthen their positions in the market by enhancing their supply chain efficiencies and improving their ability to serve customers in key markets.

- In February 2025, DuPont Nutrition & Biosciences, a leading biotech company, unveiled a new enzyme technology, Pro industrial, for soybean oil refining (DuPont press release). This technology is expected to improve the efficiency of soybean oil refining by up to 10%, thereby reducing production costs and increasing the competitiveness of soybean derivatives in the global market.

Research Analyst Overview

The market continues to evolve, driven by the versatility and applications of soybeans across various sectors. Soybean oil refining transforms crude soybean oil into consumer-ready products, while soybean-based ingredients find their way into food and industrial applications. Soybean flakes and hulls contribute to animal feed and biofuel production, respectively. Environmental impact is a significant factor shaping the market, with a focus on sustainability and protein fortification. Soybean research advances protein modification, disease resistance, and functional properties, expanding the scope of soybean derivatives. Animal feed applications, including soy meal, remain a substantial market, while soybean milk gains popularity as a plant-based alternative to dairy.

Soy lecithin, a byproduct of soybean oil refining, is used as an emulsifier in various industries. Food fortification and labeling requirements influence the market, with increasing demand for traceability and allergen concerns. Soybean industry trends include innovation in soybean derivatives, such as soy protein isolate, concentrate, and hydrolysate, as well as soy flour, soy oil, and soy sauce. Soybean supply chain optimization and sustainable sourcing are essential for maintaining quality and addressing GMO concerns. Soybean cultivation and yield improvements contribute to the market's growth, while soybean pricing and futures remain key factors influencing market dynamics. The market's continuous evolution reflects the ongoing unfolding of market activities and the integration of various sectors, including food, industrial, and animal feed applications.

The Soybean Derivatives Market is evolving with a focus on soybean sustainability practices and efficient soybean disease management to improve crop yield. Advancements in soy protein concentrates and diverse soy lecithin grades enhance nutritional benefits and functional properties in food formulations. Innovative soybean hull applications drive new uses in agriculture and industrial sectors. The industry's soybean traceability systems ensure transparency and compliance with soybean industry regulations. Changing soybean market dynamics influence demand, while soybean GMO labeling affects consumer perception. Efforts to reduce the soybean environmental footprint lead to eco-friendly production methods. Continuous soybean product development fosters innovation, strengthened by soybean industry collaborations that drive market expansion and sustainability in global food and industrial applications.

Dive into Technavio's strong research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Soybean Derivatives Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

223 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.2% |

|

Market growth 2025-2029 |

USD 134.5 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.7 |

|

Key countries |

US, Brazil, China, Canada, India, Argentina, Japan, Mexico, Colombia, and Indonesia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Soybean Derivatives Market Research and Growth Report?

- CAGR of the Soybean Derivatives industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, South America, Europe, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the soybean derivatives market growth of industry companies

We can help! Our analysts can customize this soybean derivatives market research report to meet your requirements.

RIA -

RIA -