Spray Polyurethane Foam Market Size 2026-2030

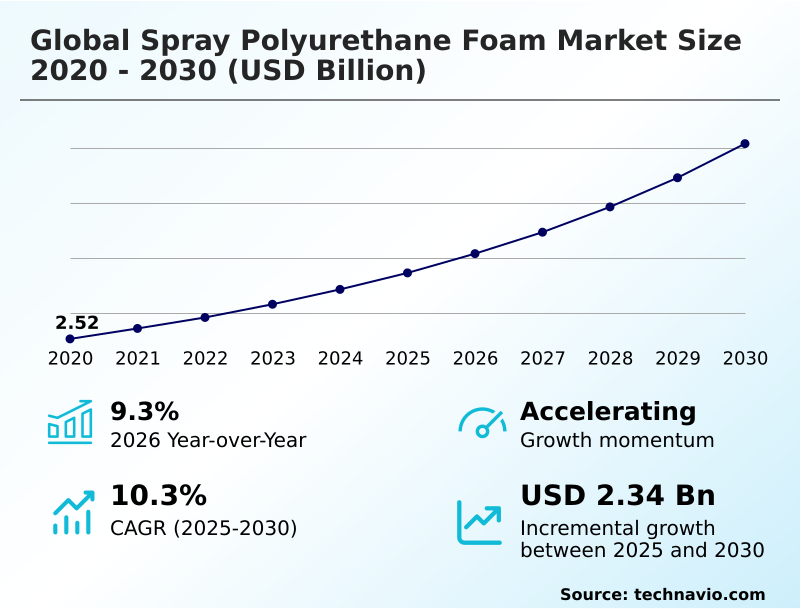

The spray polyurethane foam market size is valued to increase by USD 2.34 billion, at a CAGR of 10.3% from 2025 to 2030. Increasing demand for energy-efficient building solutions will drive the spray polyurethane foam market.

Major Market Trends & Insights

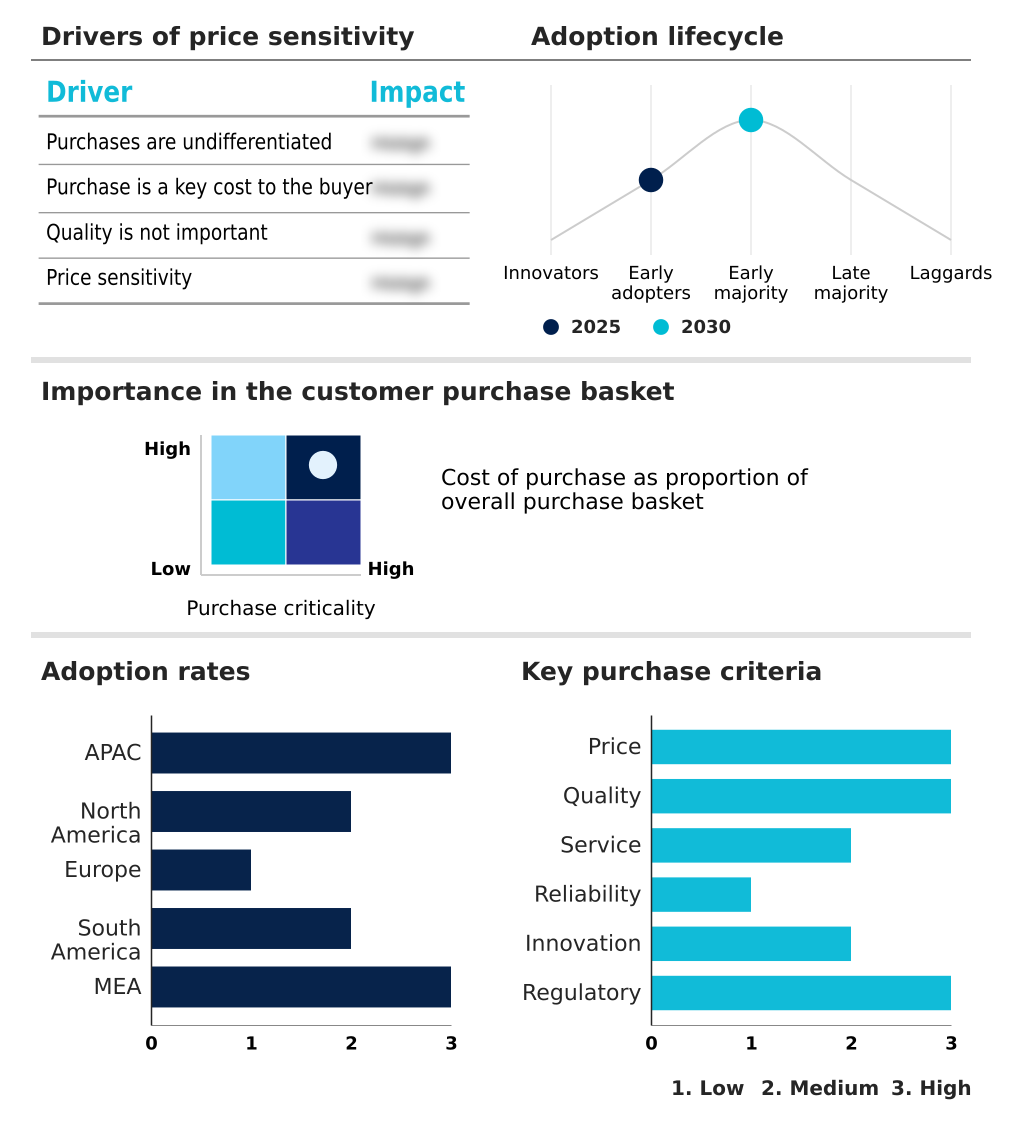

- APAC dominated the market and accounted for a 40.9% growth during the forecast period.

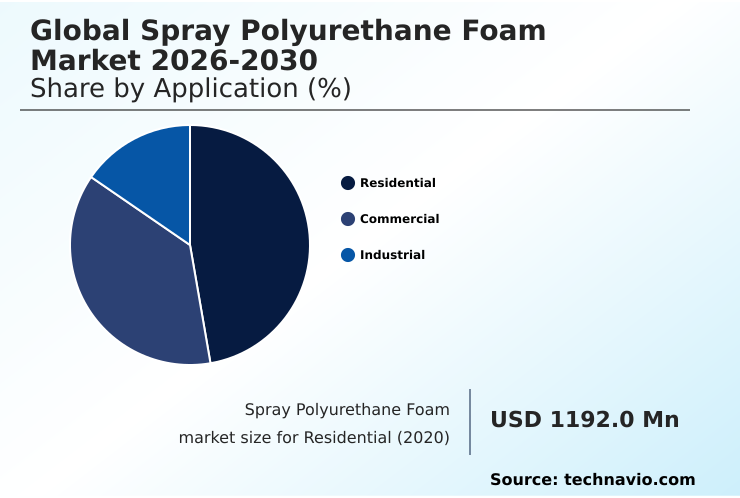

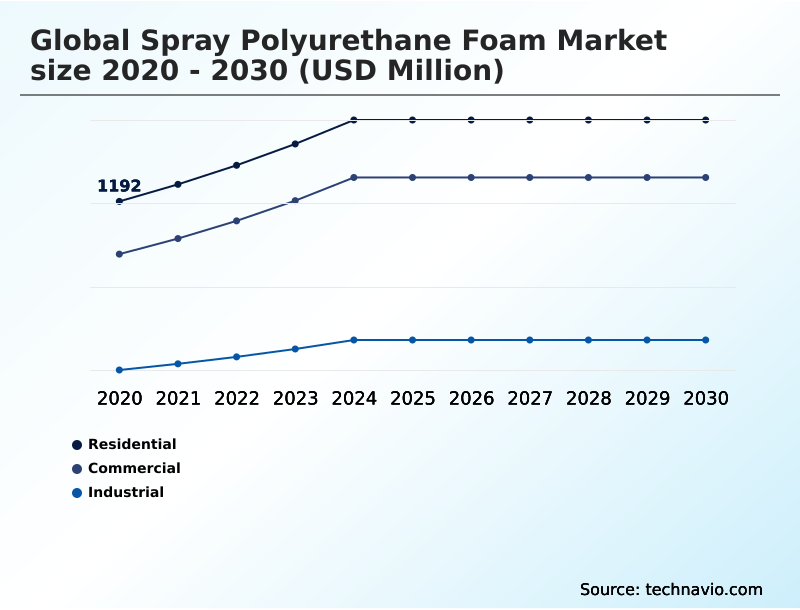

- By Application - Residential segment was valued at USD 1.58 billion in 2024

- By Type - Open cell segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.54 billion

- Market Future Opportunities: USD 2.34 billion

- CAGR from 2025 to 2030 : 10.3%

Market Summary

- The spray polyurethane foam market is driven by the global imperative for energy efficiency and the construction of resilient, airtight building envelopes. This technology, which includes both open-cell and closed-cell spray foam, offers superior thermal resistance r-value and serves as a moisture barrier, making it essential for modern building practices.

- Key advancements focus on sustainable materials, such as bio-based polyols and the use of hydrofluoroolefin blowing agents, which have a near-zero global warming potential. A typical business scenario involves the retrofitting of an aging commercial building where spray foam is applied to the roof and walls.

- This single application creates a monolithic insulation layer, eliminating thermal bridges and improving structural rigidity, which reduces the building's energy consumption for heating and cooling. However, the industry contends with challenges related to the price volatility of methylene diphenyl diisocyanate (MDI) and the need for a skilled workforce proficient in precise application techniques.

- The ongoing digitalization of application equipment, incorporating IoT sensors for quality control, is a key trend addressing these operational hurdles. These systems ensure consistent foam density and optimal adhesion properties, which is crucial for achieving long-term performance and meeting stringent building codes.

What will be the Size of the Spray Polyurethane Foam Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Spray Polyurethane Foam Market Segmented?

The spray polyurethane foam industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Residential

- Commercial

- Industrial

- Type

- Open cell

- Closed cell

- Product

- Two component high pressure foam

- Two component low pressure foam

- One component foam

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Application Insights

The residential segment is estimated to witness significant growth during the forecast period.

The residential application segment is propelled by a global focus on energy conservation, with spray polyurethane foam emerging as a superior alternative to traditional materials.

Homeowners and developers prioritize this technology for its ability to create a monolithic insulation layer, significantly reducing air infiltration—a primary cause of heat loss. This application is common in attics, crawl spaces, and exterior walls.

Open-cell spray foam, in particular, has demonstrated the ability to reduce ambient noise levels by over 15 decibels in multi-family dwellings, enhancing acoustic comfort. The demand for bio-based polyols and polyol resin is also rising in this segment.

The structural rigidity and adhesion properties of the foam ensure long-term performance, making it a critical component for achieving high-efficiency building envelopes and meeting modern building codes.

The Residential segment was valued at USD 1.58 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 40.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Spray Polyurethane Foam Market Demand is Rising in APAC Get Free Sample

The global geographic landscape is defined by a divergence between mature and emerging regions.

In North America and Europe, the market is driven by stringent building codes and the retrofitting of aging infrastructure, where spray polyurethane foam is used to achieve a high thermal resistance R-value and an effective air barrier.

These regions see high adoption of hydrofluoroolefin blowing agents. In contrast, the APAC region, growing at a rate nearly 25% faster than North America, is propelled by rapid urbanization and the construction of new residential and commercial real estate.

In these markets, the material's function as a moisture barrier and its ability to provide a monolithic insulation layer are critical.

The expansion of cold storage logistics, particularly in China and India, further fuels demand for high-performance closed-cell spray foam, leveraging its superior insulation properties to ensure supply chain integrity.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the global spray polyurethane foam market 2026-2030 is increasingly focused on specialized applications and performance characteristics. The selection of spray foam insulation for attics is a primary method for improving residential energy efficiency, directly impacting homeowner utility costs.

- For commercial projects, the specification of fire retardant polyurethane foam is critical for meeting stringent building safety codes and minimizing liability. In industrial settings, the use of high-density spray foam for roofing provides a durable, seamless, and waterproof membrane, extending the life of the asset.

- The choice between open vs closed cell spray foam insulation depends on project requirements; open-cell is often preferred for interior sound dampening, while closed-cell offers superior thermal resistance and structural rigidity. Furthermore, the market for low-pressure spray foam kits is expanding, empowering smaller contractors to perform professional-grade air sealing and insulation repairs.

- These specialized product segments demonstrate that the market is evolving beyond general insulation, with operational costs in facilities using advanced systems being a fraction of those with outdated materials.

What are the key market drivers leading to the rise in the adoption of Spray Polyurethane Foam Industry?

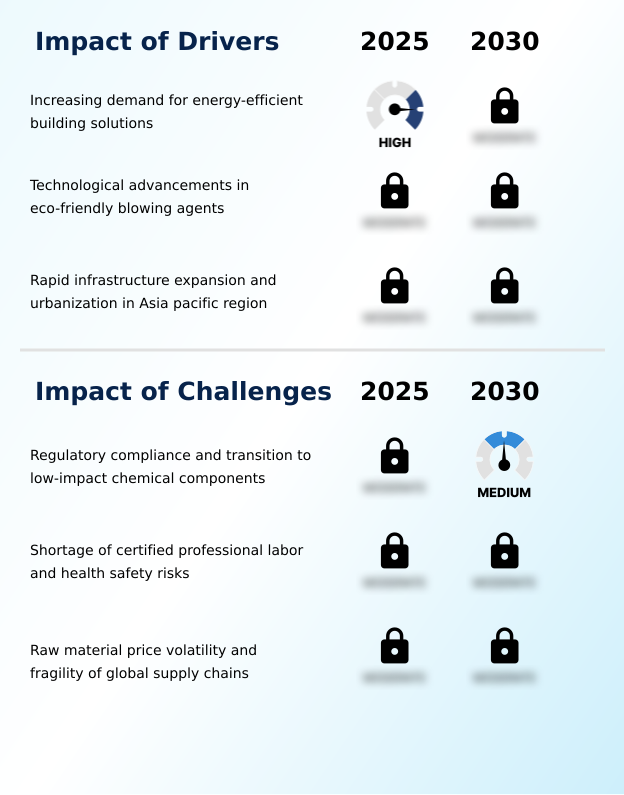

- The increasing demand for energy-efficient building solutions, driven by stringent regulations and rising energy costs, is a key driver for market growth.

- The market is primarily driven by the global demand for energy-efficient buildings and advancements in chemical technology.

- Stringent regulations, such as the European mandate for all new buildings to be zero-emission, compel developers to use high-performance materials like closed-cell spray foam, which provides a high thermal resistance r-value and improves a building’s energy rating by up to 40%.

- The transition to environmentally friendly hydrofluoroolefin blowing agents has also been a significant catalyst, aligning the industry with global sustainability goals.

- In APAC, rapid urbanization and the expansion of cold storage logistics are fueling demand, as spray foam’s ability to act as a moisture barrier and a continuous insulation layer is essential for these applications.

What are the market trends shaping the Spray Polyurethane Foam Industry?

- A significant market trend involves the integration of bio-based feedstocks and the adoption of circular economy principles in manufacturing processes. This shift aims to reduce environmental impact and enhance product sustainability.

- Key trends are reshaping the market, led by the integration of sustainable raw materials and digital technologies. The industry is moving toward a circular economy with the adoption of recycled polyethylene terephthalate (PET) and advanced chemical recycling, which can reduce the embodied carbon in insulation materials by over 25%.

- This shift addresses both environmental concerns and the price volatility of petrochemical feedstocks. Concurrently, digitalization is enhancing application precision. Modern spray rigs with IoT sensors ensure an optimal isocyanate to polyol ratio, with some systems featuring automated shut-offs if the mix deviates by more than 1%, significantly reducing installation failures and material waste.

- This focus on quality control helps create a superior air barrier, reinforcing the material's value in high-performance construction.

What challenges does the Spray Polyurethane Foam Industry face during its growth?

- Navigating complex regulatory compliance and managing the transition to low-impact chemical components presents a key challenge to industry growth.

- The industry faces significant challenges related to regulatory compliance and supply chain vulnerabilities. The mandatory phase-out of hydrofluorocarbons requires substantial R&D investment to reformulate products with new blowing agents, a capital-intensive process that smaller firms struggle to afford. This transition requires extensive testing to ensure foam density and adhesion properties are maintained.

- Additionally, the market's reliance on petrochemicals, such as methylene diphenyl diisocyanate (MDI), makes it susceptible to price volatility and supply disruptions. A major port shutdown can halt production for weeks, demonstrating the fragility of a supply chain concentrated among a few large chemical plants.

- The shortage of skilled labor proficient in creating a proper isocyanate to polyol ratio further compounds these issues.

Exclusive Technavio Analysis on Customer Landscape

The spray polyurethane foam market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the spray polyurethane foam market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Spray Polyurethane Foam Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, spray polyurethane foam market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

BASF SE - Key offerings in the market center on advanced chemical formulations for high-performance thermal insulation and air sealing applications, including both open-cell and closed-cell systems.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BASF SE

- Carlisle Spray Foam Insulation

- CertainTeed

- Covestro AG

- Dow Chemical Co.

- Elastochem Specialty Chemicals

- Foam Supplies Inc.

- Gaco Western LLC

- Huntsman International LLC

- Isothane Ltd.

- Johns Manville Corp.

- Kingspan Group Plc

- NCFI Polyurethanes

- Owens Corning

- Pearl Polyurethane Systems LLC

- Rhino Linings Corporation

- SES Foam LLC

- SOPREMA SAS

- Specialty Products Inc.

- Stepan Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Spray polyurethane foam market

- In October 2025, Honeywell International Inc. introduced an upgraded liquid blowing agent optimized for low-pressure spray foam kits, expanding access to sustainable insulation technology.

- In July 2025, BASF SE launched a new series of spray foam polyols derived entirely from chemically recycled plastic waste, advancing circular economy principles in the sector.

- In June 2025, the US Environmental Protection Agency finalized a rule accelerating the prohibition of specific high-global-warming-potential substances in foam production, impacting manufacturers' chemical roadmaps.

- In May 2025, the European Commission adopted the revised Energy Performance of Buildings Directive, mandating that all new buildings be zero-emission by 2030, driving demand for advanced insulation.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Spray Polyurethane Foam Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.3% |

| Market growth 2026-2030 | USD 2343.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.3% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The spray polyurethane foam market is characterized by intense innovation driven by regulatory pressures and sustainability mandates. A primary focus for boardroom-level strategy is the transition to advanced chemical formulations, particularly the adoption of hydrofluoroolefin blowing agents, to comply with environmental protocols. This requires significant investment in R&D to ensure new products maintain high thermal resistance r-value and foam density.

- The use of bio-based polyols and recycled polyethylene terephthalate (PET) is becoming a key differentiator, reducing the embodied carbon of building materials. For instance, the use of intelligent application equipment has led to a 30% reduction in material waste and rework. Performance is also enhanced by creating a continuous insulation layer with excellent adhesion properties.

- Products like open-cell spray foam and closed-cell spray foam offer distinct benefits, from acoustic insulation to providing a robust air barrier and moisture barrier. The structural rigidity and isocyanate to polyol ratio are critical metrics that manufacturers must optimize for diverse applications, from residential walls to industrial roofing, ensuring a monolithic insulation layer.

What are the Key Data Covered in this Spray Polyurethane Foam Market Research and Growth Report?

-

What is the expected growth of the Spray Polyurethane Foam Market between 2026 and 2030?

-

USD 2.34 billion, at a CAGR of 10.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Residential, Commercial, and Industrial), Type (Open cell, and Closed cell), Product (Two component high pressure foam, Two component low pressure foam, and One component foam) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for energy-efficient building solutions, Regulatory compliance and transition to low-impact chemical components

-

-

Who are the major players in the Spray Polyurethane Foam Market?

-

BASF SE, Carlisle Spray Foam Insulation, CertainTeed, Covestro AG, Dow Chemical Co., Elastochem Specialty Chemicals, Foam Supplies Inc., Gaco Western LLC, Huntsman International LLC, Isothane Ltd., Johns Manville Corp., Kingspan Group Plc, NCFI Polyurethanes, Owens Corning, Pearl Polyurethane Systems LLC, Rhino Linings Corporation, SES Foam LLC, SOPREMA SAS, Specialty Products Inc. and Stepan Co.

-

Market Research Insights

- Market dynamics are shaped by a pronounced shift toward high-performance materials that deliver measurable business outcomes. For instance, facilities retrofitted with closed-cell spray foam systems have demonstrated energy consumption reductions of up to 40%, directly impacting operational overhead. The adoption of advanced chemical formulations enables such efficiencies.

- In cold storage applications, the implementation of a continuous insulation layer has been shown to lower energy use by 20% compared to traditional methods. Furthermore, the use of intelligent application equipment, which ensures the correct polyol resin to isocyanate ratio, reduces material waste by over 5%, improving project profitability.

- These quantifiable benefits, coupled with the material's ability to serve as a durable moisture barrier, underscore its strategic value in modern construction and industrial settings. The focus on life-cycle performance and sustainability continues to influence procurement decisions.

We can help! Our analysts can customize this spray polyurethane foam market research report to meet your requirements.

RIA -

RIA -