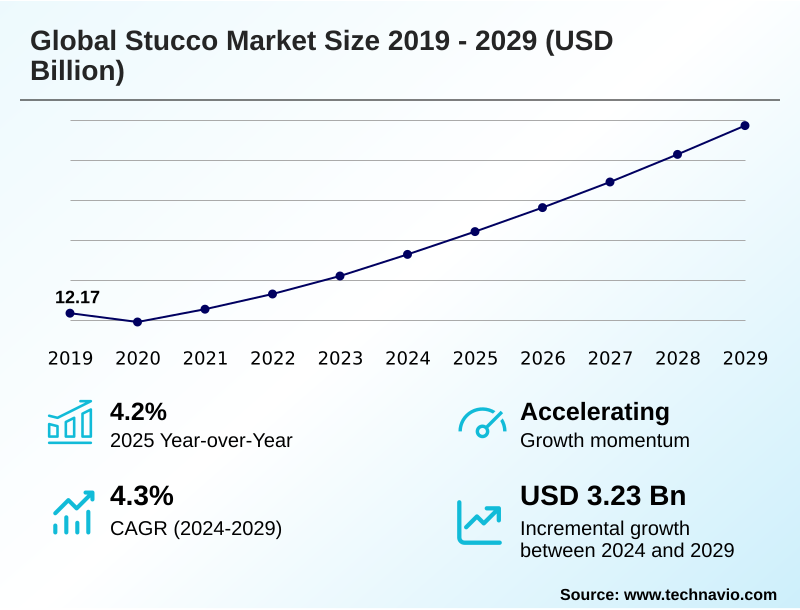

Stucco Market Size 2025-2029

The stucco market size is valued to increase by USD 3.23 billion, at a CAGR of 4.3% from 2024 to 2029. Resurgence in global construction and infrastructure development will drive the stucco market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 40.7% growth during the forecast period.

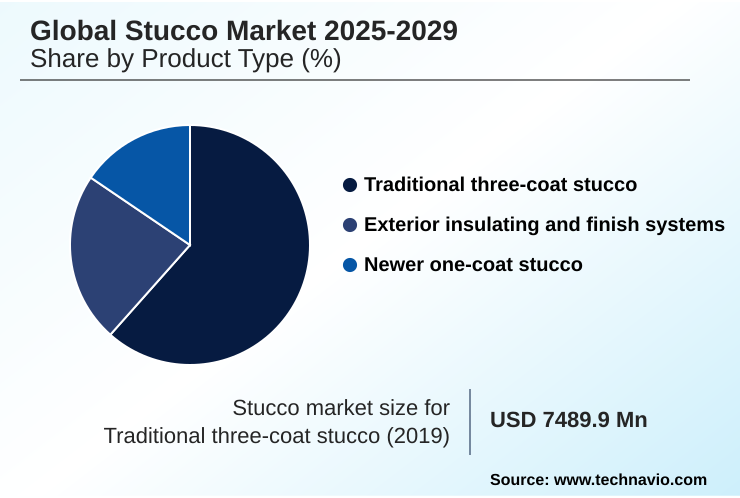

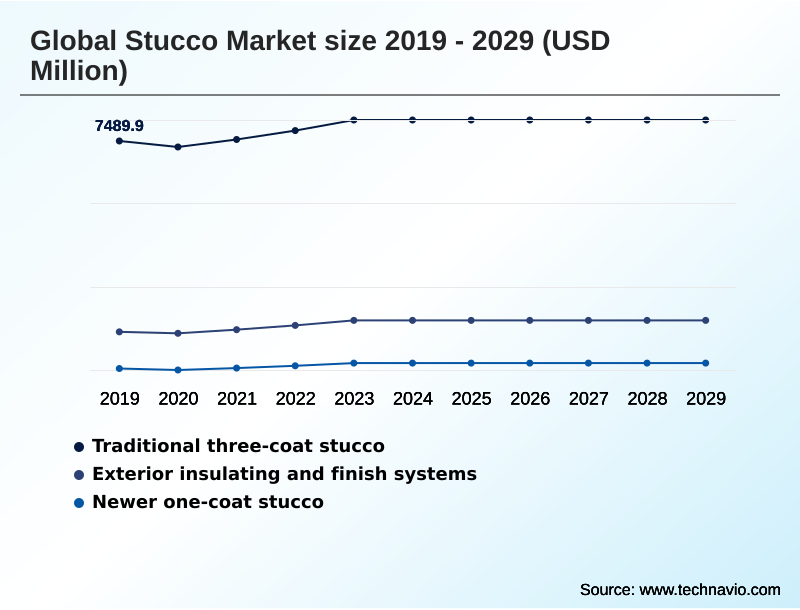

- By Product Type - Traditional three-coat stucco segment was valued at USD 8.01 billion in 2023

- By Application - Residential segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 4.70 billion

- Market Future Opportunities: USD 3.23 billion

- CAGR from 2024 to 2029 : 4.3%

Market Summary

- The stucco market is undergoing a significant transformation, driven by robust construction activity and an increasing focus on building performance. Valued for its durability and design flexibility, stucco is a primary choice for exterior cladding in residential and commercial sectors.

- However, the market's evolution is shaped by a dual focus: enhancing the performance of traditional systems and advancing modern alternatives like Exterior Insulation and Finish Systems (EIFS). A key trend is the adoption of sustainable materials and energy-efficient systems to meet stricter environmental regulations.

- For instance, a commercial developer planning a new retail complex might specify an EIFS with high thermal resistance not just for aesthetic appeal, but to achieve green building certification, which lowers long-term operational costs and attracts environmentally conscious tenants.

- This strategic decision highlights the market's shift from a purely aesthetic choice to an integral component of a building's energy and sustainability strategy. Challenges such as the shortage of skilled applicators and competition from alternative materials like fiber cement continue to influence market dynamics, pushing manufacturers toward innovation in both product formulation and application technology.

What will be the Size of the Stucco Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Stucco Market Segmented?

The stucco industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product type

- Traditional three-coat stucco

- Exterior insulating and finish systems

- Newer one-coat stucco

- Application

- Residential

- Commercial

- Industrial

- Material

- Cement-based

- Acrylic

- Lime-based

- Others

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Product Type Insights

The traditional three-coat stucco segment is estimated to witness significant growth during the forecast period.

The global stucco market is segmented by product type, application, and geography. Traditional three-coat stucco remains a cornerstone, prized for its durability in both residential construction and commercial buildings.

This system involves a meticulous, labor-intensive process applying distinct layers over a lath base to create a solid shell. The material composition, primarily portland cement, provides inherent fire-resistant cladding and excellent thermal mass properties.

This process ensures unmatched impact resistance and breathability due to its vapor permeability. Although requiring skilled labor for stucco, proper installation yields a finish with a service life that can exceed other exterior wall cladding options by over 50%.

Its application is prominent in high-end custom homes and historic building restoration projects where long-term performance is paramount.

The Traditional three-coat stucco segment was valued at USD 8.01 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 40.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Stucco Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the global stucco market 2025-2029 is diverse, with APAC leading demand, accounting for over 40% of the incremental growth opportunity. This is driven by massive urbanization and infrastructure projects requiring cost-effective materials like cementitious plaster.

North America remains a mature market, where demand is split between new construction in Sun Belt states and a robust renovation market focused on improving building envelope insulation. In this region, specifying climate-specific stucco is crucial.

Europe's market is defined by stringent regulations promoting energy efficiency, making advanced architectural coatings and thermal envelope solutions a priority. The supply chain logistics in this region are well-established, contrasting with challenges in emerging markets in South America and Africa.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the modern construction landscape requires a deep understanding of exterior cladding choices. For instance, analyzing the cost of eifs vs traditional stucco is a critical step for developers. While EIFS installation for energy efficiency may have a higher upfront cost, it often leads to significant long-term savings on utility bills.

- The benefits of lime based stucco, such as its breathability and self-healing properties, make it a premier choice for historic restorations and high-end sustainable projects. Understanding the traditional three coat stucco application process is key to appreciating its unmatched durability, though it highlights the challenges of the skilled labor shortage for plasterers.

- To mitigate common failures, preventing moisture intrusion in stucco through modern drainage planes and flashing techniques is non-negotiable. For builders in warmer regions, selecting the best stucco for hot climates involves looking at formulations with high solar reflectivity. The industry is also addressing performance with innovations in polymer modified stucco crack resistance.

- For renovations, the feasibility of applying stucco over existing siding offers a transformative aesthetic upgrade. Specifiers are increasingly examining the long term durability of acrylic stucco and its performance in varied conditions, such as stucco in high humidity climates or regions with frequent stucco application in freeze-thaw cycles.

- The advantages of one-coat stucco systems, primarily speed of application, make them popular in production homebuilding. Meanwhile, the growing demand for unique aesthetics drives interest in diverse stucco finish textures and styles. To accelerate construction, prefabricated stucco panel installation is gaining traction.

- Finally, maintaining and cleaning stucco walls, choosing stucco for commercial properties, understanding the fire resistance of cementitious stucco, the impact of thermal bridging on buildings, and the role of stucco in green building are all crucial considerations.

- For example, adopting prefabricated systems has been shown to reduce on-site waste by a factor of two compared to traditional methods, directly impacting a project's compliance with green building standards.

What are the key market drivers leading to the rise in the adoption of Stucco Industry?

- A global resurgence in construction and infrastructure development serves as the primary driver fueling demand across the stucco market.

- The global stucco market 2025-2029 is primarily driven by a resurgence in global construction and the strong demand from the renovation and remodeling siding sector.

- In the new-build segment, lightweight cladding options that are also cost-effective are specified for large projects. In the renovation sector, applying insulated stucco systems to older structures has been shown to reduce heating and cooling costs by up to 25%.

- This focus on home energy retrofits is bolstered by government incentives. For instance, projects utilizing systems with a dedicated water-resistive barrier and proper moisture drainage systems have seen a 60% decrease in moisture-related warranty claims.

- The push for building resilience to weather further solidifies demand for durable decorative textured finishes and polymer binders.

What are the market trends shaping the Stucco Industry?

- The market is observing an accelerated adoption of sustainable and energy-efficient stucco systems. This trend is driven by stricter building codes and increasing demand for high-performance green building materials.

- A key trend in the global stucco market 2025-2029 is the shift toward advanced stucco formulations and high-performance exterior insulation and finish systems (EIFS), which improve building envelope performance. Innovations in polymer-modified stucco and elastomeric properties have led to a 40% reduction in reported shrinkage cracking. These energy-efficient stucco systems, incorporating continuous insulation, directly support green building certifications.

- We are also seeing the emergence of photocatalytic finishes, which can degrade airborne pollutants, and prefabricated stucco panels that reduce on-site construction cycle time by up to 30%. These innovations address long-standing challenges and align with stricter building energy codes, reflecting a move toward more sustainable building materials and enhanced architectural design flexibility with low-voc formulations.

What challenges does the Stucco Industry face during its growth?

- A pervasive shortage of skilled labor and installation expertise poses a significant challenge to the industry's growth and quality standards.

- The global stucco market 2025-2029 faces significant challenges from the pervasive shortage of skilled labor for stucco and intense competition from stucco vs fiber cement and other alternatives. This labor deficit increases installation costs by as much as 20% in some regions and elevates the risk of improper application, leading to concerns about the durability of exterior finishes.

- Lingering perceptions about moisture management in stucco, despite the development of advanced rainscreen technology, constrain market adoption. The need for meticulous stucco application techniques and strict building code compliance adds complexity, especially for EIFS. This environment makes it difficult for contractors to manage stucco repair methods and maintain profitability, highlighting the critical need for improved training and technology.

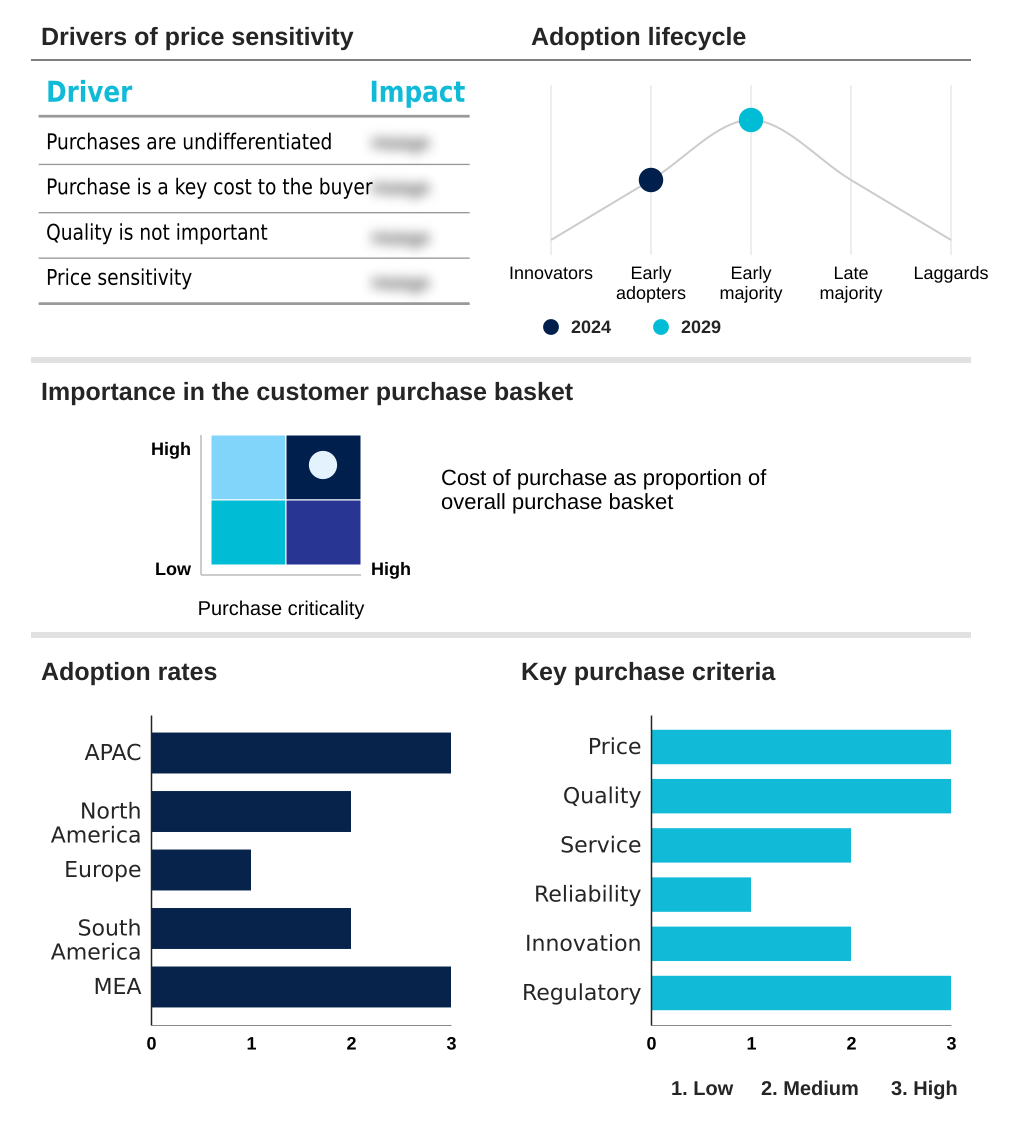

Exclusive Technavio Analysis on Customer Landscape

The stucco market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the stucco market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Stucco Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, stucco market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Stucco - Offers integrated facade solutions, from EIFS and one-coat systems to various architectural coatings, meeting modern construction's performance and aesthetic demands.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Stucco

- CEMEX SAB de CV

- Compagnie de Saint Gobain SA

- Knauf Digital GmbH

- LaHabra Stucco

- Master Wall Inc.

- Merlex Stucco, Inc

- Oikos

- Omega Products International Inc.

- Owens Corning

- Sika AG

- SPEC MIX, LLC

- STO Corp.

- Stucco Italiano

- Stucco Supply Co.

- Tesuque Stucco Company

- Total Wall

- Wacker Chemie AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Stucco market

- In September 2024, Sika AG announced the full transition of its North American cementitious product lines to utilize Portland Limestone Cement (PLC), reducing the embodied carbon of its stucco mixes by an average of 10%.

- In November 2024, STO Corp. launched a new prefabricated panelized EIFS incorporating advanced drainage capabilities and a factory-applied finish, designed to reduce on-site construction time by up to 25% for commercial projects.

- In February 2025, Compagnie de Saint-Gobain acquired a specialized US-based manufacturer of lime-based plasters, expanding its portfolio to meet growing demand in the historic preservation and high-end residential segments.

- In April 2025, Wacker Chemie AG introduced a new generation of silicone resin emulsion paints for stucco finishes, offering a 15-year warranty against fading and water repellency degradation, setting a new industry benchmark for durability.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Stucco Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.3% |

| Market growth 2025-2029 | USD 3226.2 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 4.2% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The stucco market is evolving beyond traditional applications, driven by innovations in material science and a heightened focus on building envelope performance. While traditional systems remain prevalent, growth is concentrated in advanced formulations such as polymer-modified stucco and comprehensive Exterior Insulation and Finish Systems (EIFS). These modern systems offer significant advantages, including enhanced flexibility, crack resistance, and superior thermal insulation.

- The integration of continuous insulation in EIFS, for instance, is a key strategy for reducing thermal bridging and meeting stringent energy codes. A critical decision for architectural firms and developers now involves balancing the upfront cost of these high-performance systems against long-term operational savings.

- Projects that specify advanced EIFS with integrated moisture management have demonstrated a measurable impact, achieving up to 30% lower energy consumption for climate control. This shift positions stucco not just as a protective or decorative finish, but as a critical component in the design of resilient and energy-efficient buildings, influencing budgeting and product strategy at the highest levels.

What are the Key Data Covered in this Stucco Market Research and Growth Report?

-

What is the expected growth of the Stucco Market between 2025 and 2029?

-

USD 3.23 billion, at a CAGR of 4.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product Type (Traditional three-coat stucco, Exterior insulating and finish systems, and Newer one-coat stucco), Application (Residential, Commercial, and Industrial), Material (Cement-based, Acrylic, Lime-based, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Resurgence in global construction and infrastructure development, Pervasive shortage of skilled labor and installation expertise

-

-

Who are the major players in the Stucco Market?

-

Advanced Stucco, CEMEX SAB de CV, Compagnie de Saint Gobain SA, Knauf Digital GmbH, LaHabra Stucco, Master Wall Inc., Merlex Stucco, Inc, Oikos, Omega Products International Inc., Owens Corning, Sika AG, SPEC MIX, LLC, STO Corp., Stucco Italiano, Stucco Supply Co., Tesuque Stucco Company, Total Wall and Wacker Chemie AG

-

Market Research Insights

- Market dynamics are shaped by a confluence of construction activity, regulatory pressures, and material innovation. The renovation sector has shown particular resilience, with spending on exterior upgrades remaining robust. Projects incorporating modern stucco systems with integrated moisture management have reported a 60% reduction in callbacks related to water intrusion compared to older installations.

- Furthermore, the adoption of one-coat stucco systems in residential construction can decrease application schedules by up to 40%, directly addressing labor shortages and improving project turnaround times. This efficiency is critical as builders navigate fluctuating material costs.

- Concurrently, the push for energy efficiency continues, with buildings using EIFS demonstrating up to 30% lower energy consumption for heating and cooling, aligning with increasingly stringent building codes.

We can help! Our analysts can customize this stucco market research report to meet your requirements.

RIA -

RIA -