Subsea Sensors Market Size 2025-2029

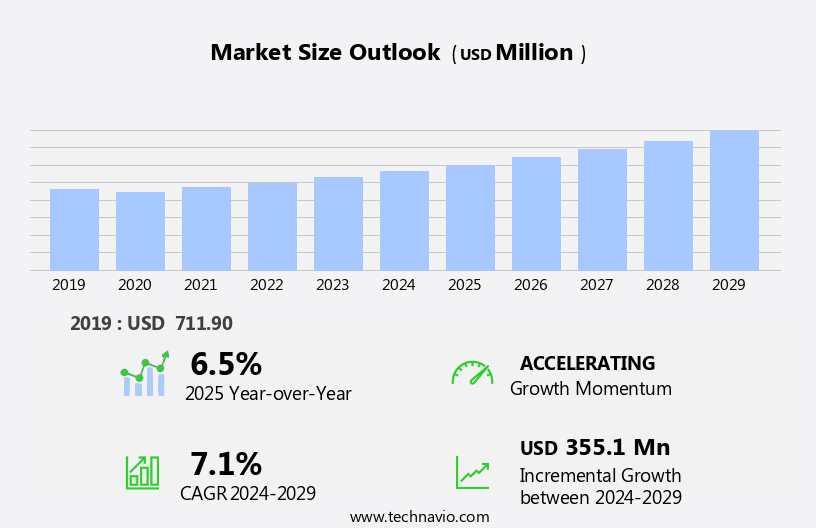

The subsea sensors market size is forecast to increase by USD 355.1 million, at a CAGR of 7.1% between 2024 and 2029.

- The market is driven by the expansion of the offshore oil and gas industry, which necessitates the deployment of advanced subsea sensing technologies for exploration and production activities. These sensors enable real-time monitoring of critical parameters such as pressure, temperature, and flow rate, ensuring optimal operational efficiency and safety. Researchers and scientists also utilize subsea sensors for oceanographic studies, while sensors manufacturers continue to innovate with technology advancements such as artificial intelligence and the Internet of Things. However, the market faces a significant challenge in the form of the limited battery life of subsea sensors. Given the harsh subsea environment and the inaccessibility of these sensors, replacing batteries or repairing them can be time-consuming and costly. As a result, there is a growing demand for sensors with longer battery life and improved durability.

- Companies investing in research and development to address this challenge and create more robust, long-lasting subsea sensors will gain a competitive edge in the market. Additionally, collaborations and partnerships between technology providers and oil and gas companies can lead to innovative solutions and mutual benefits.

What will be the Size of the Subsea Sensors Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market is characterized by its continuous evolution and dynamic nature, driven by advancements in technology and the expanding applications across various sectors. These sensors play a crucial role in depth and environmental monitoring, enabling real-time data acquisition and analysis for industries such as oil and gas, renewable energy, and marine research. The ongoing unfolding of market activities reveals a focus on enhancing sensor capabilities to meet the demands of harsh subsea conditions. This includes the development of sensors with high-pressure tolerances, corrosion resistance, and temperature and salinity compensation. Moreover, there is a growing emphasis on power management and data transmission solutions, enabling efficient power consumption and underwater communication for remote sensing and intervention.

The integration of machine learning and artificial intelligence (AI) in data analytics and signal processing is also transforming the market, enabling predictive maintenance procedures and structural health monitoring. Sensor deployment strategies continue to evolve, with a shift towards wireless communication and edge computing to minimize the need for manual intervention and reduce costs. The integration of multiple sensor types, including acoustic, optical, and pressure sensors, is also gaining popularity through sensor fusion and calibration techniques. Regulatory compliance and environmental impact remain key considerations, with a focus on minimizing the carbon footprint of subsea operations and ensuring sustainable practices.

The market is further expected to be influenced by emerging trends such as cloud computing, subsea robotics, and advanced data visualization tools. In conclusion, the market is a vibrant and evolving space, with ongoing innovation and development driving advancements in technology and applications across various industries. The market's continuous dynamism is reflected in the integration of various sensor technologies, deployment strategies, and data processing techniques to meet the demands of subsea operations in a sustainable and efficient manner.

How is this Subsea Sensors Industry segmented?

The subsea sensors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

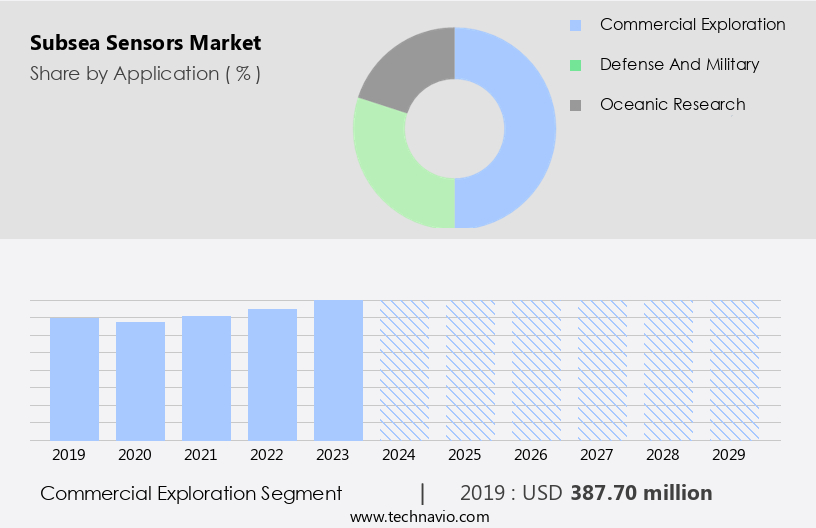

- Commercial exploration

- Defense and military

- Oceanic research

- Type

- Pressure

- Temperature

- Acoustic

- Image or optical

- Others

- End-user

- Oilfield service companies

- Defense contractors

- Research institutions

- Renewable energy firms

- Depth

- Shallow Water

- Deepwater

- Ultra-Deepwater

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The commercial exploration segment is estimated to witness significant growth during the forecast period.

Subsea sensors play a pivotal role in various commercial exploration activities, particularly in the oil and gas industry, as traditional onshore reserves deplete and focus shifts to deeper offshore waters. These sensors are indispensable for monitoring conditions, managing production processes, and maintaining infrastructure integrity in challenging underwater environments. Strict safety and environmental regulations, especially in offshore operations, necessitate the use of advanced subsea sensors. Technological advancements, such as deep learning, artificial intelligence, and edge computing, are driving the exploration of extreme underwater environments, including deep-sea trenches, hydrothermal vents, and seamounts. Subsea sensors enable researchers to collect critical data on temperature, pressure, salinity, and other environmental parameters in these environments.

Additionally, sensors are integral to pipeline monitoring, leak detection, cable monitoring, subsea intervention, maintenance procedures, and sensor maintenance. High-pressure tolerances, data transmission, and wireless communication are essential features for these sensors. Machine learning and signal processing enhance data analytics, while cloud computing facilitates data storage and access. Corrosion monitoring, structural health monitoring, and sensor calibration ensure the longevity and accuracy of these sensors. Offshore wind energy, sonar systems, positioning systems, and sensor fusion further expand the application scope of subsea sensors. Material science, temperature compensation, and salinity compensation contribute to enhancing sensor performance. Deployment strategies, data logging, sensor integration, and operating temperature are crucial considerations for sensor selection and implementation.

Subsea inspection and sensor networks are essential for maintaining the integrity of underwater infrastructure.

The Commercial exploration segment was valued at USD 387.70 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

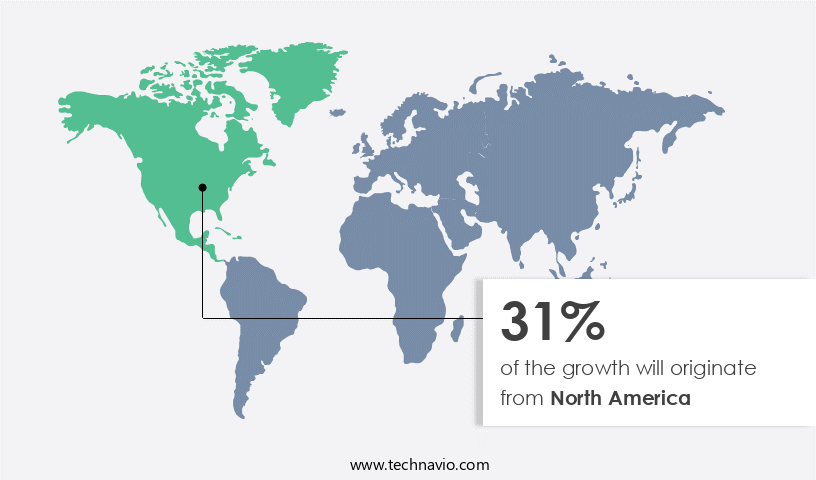

North America is estimated to contribute 31% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the expanding offshore energy sector of North America, subsea sensors play a pivotal role, particularly in the Gulf of Mexico and off the Canadian coast, where significant oil and gas reserves lie. As exploration and production activities delve deeper into the ocean, there is a growing demand for these sensors to monitor well conditions, pipeline integrity, and environmental factors. The emergence of offshore wind energy along the US East Coast and in certain Canadian regions further boosts this need. Subsea sensors are indispensable for assessing environmental conditions, such as water currents and seabed stability, ensuring the successful installation and operation of offshore wind turbines.

The integration of advanced technologies like big data, artificial intelligence (AI), deep learning, and machine learning into subsea sensors enhances their capabilities. Real-time monitoring, power management, and data acquisition systems facilitate efficient and effective data processing. High-pressure tolerances, corrosion resistance, and temperature and salinity compensation ensure the sensors' durability and accuracy. Edge computing and wireless communication enable data transmission and analysis in real-time. Subsea intervention, maintenance procedures, and sensor maintenance are crucial aspects of subsea sensor applications. Structural health monitoring, signal processing, and sensor fusion provide valuable insights into pipeline conditions and potential issues. Regulatory compliance, leak detection, and corrosion monitoring are essential for ensuring safety and minimizing environmental impact.

Subsea robotics, acoustic sensors, and remote sensing contribute to the development of advanced subsea sensor networks. Cloud computing and data visualization tools facilitate data analysis and interpretation. Operating depth, environmental monitoring, and sensor life are critical factors in the selection and deployment of subsea sensors. Deployment strategies, data logging, sensor integration, and operating temperature are essential considerations for optimizing sensor performance and longevity. Subsea inspection and sensor deployment are crucial for maintaining the integrity of offshore energy infrastructure. The integration of advanced technologies and the growing demand for subsea sensors underscore the market's dynamic and evolving nature.

Market Dynamics

The global subsea sensors market is experiencing significant expansion, primarily driven by the demands of offshore oil & gas (subsea sensors), particularly for subsea production monitoring and crucial pipeline integrity monitoring. The expanding subsea sensors market size and dynamic subsea sensors market trends underscore the critical role of advanced subsea sensor technology. Real-time data acquisition is facilitated by real-time subsea monitoring capabilities and advancements in wireless subsea communication. Beyond oil & gas, the market sees growing applications in oceanography & marine research and the burgeoning offshore wind energy sector. Key product categories include subsea pressure sensors, subsea temperature sensors, subsea flow sensors, and subsea acoustic sensors. The integration of remote operated vehicles (ROVs) sensors and autonomous underwater vehicles (AUVs) sensors is revolutionizing data collection. Furthermore, the rise of IoT in subsea and the application of AI for subsea data analytics are transforming environmental monitoring (subsea) and operational efficiency.

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Subsea Sensors Industry?

- The expansion of the offshore oil and gas industry serves as the primary catalyst for market growth.

- The global offshore oil and gas industry is expanding its exploration and production activities in deeper waters and remote locations to meet escalating energy demands. Subsea sensors play a crucial role in monitoring the condition of underwater infrastructure, ensuring safety and efficiency. With traditional onshore reserves depleting, the focus on subsea resources is increasing. Subsea sensors provide real-time data on the health of pipelines, wellheads, and other critical equipment, enabling operators to proactively address potential issues. These sensors employ advanced technologies such as data analytics, high-pressure tolerances, wireless communication, and signal processing for effective data transmission and edge computing.

- Structural health monitoring, data visualization, and subsea robotics are other essential applications of subsea sensors. Ensuring the reliability and maintenance of these sensors is vital for the success of subsea intervention and maintenance procedures.

What are the market trends shaping the Subsea Sensors Industry?

- Subsea sensor technology is currently experiencing significant advancements, making it a prominent market trend in the industry. This technological progression offers enhanced capabilities for underwater exploration and resource extraction.

- Subsea sensors have witnessed significant advancements due to technological innovations, enabling the development of compact and high-performing sensors for harsh underwater environments. Fiber optics, acoustic sensors, and advanced raw materials are some of the sensing technologies driving the enhancement of subsea sensors' capabilities. These sensors can measure various parameters, including temperature, pressure, salinity, dissolved oxygen, and hydrocarbons, with increased accuracy and precision. Wireless communication technologies, such as underwater acoustic modems, satellite communication, and autonomous underwater vehicles (AUVs), facilitate real-time remote monitoring of subsea sensors. Regulatory compliance and corrosion monitoring are essential applications for subsea sensors, particularly in the offshore wind energy sector.

- Sensor fusion and calibration, along with cloud computing and machine learning, contribute to improving data processing and analysis. Corrosion resistance is a critical factor in ensuring the longevity and reliability of subsea sensors. Sonar systems and positioning systems further enhance the functionality of subsea sensors, providing valuable data for underwater exploration and resource management.

What challenges does the Subsea Sensors Industry face during its growth?

- The limited battery life of subsea sensors poses a significant challenge to the growth of the industry, as it necessitates frequent maintenance or replacement, increasing operational costs.

- Subsea sensors play a crucial role in environmental monitoring and subsea inspection, particularly in assessing the impact of human activities on marine ecosystems. However, the extreme operating conditions in underwater environments, including high pressure, low temperature, and the corrosive nature of seawater, pose significant challenges to the longevity and efficiency of these sensors. One of the primary challenges is the limited battery life of subsea sensors, which can result in shorter operational lifespans and the need for frequent battery replacements or recharging. This issue can lead to increased maintenance costs, downtime, and disruptions to monitoring activities.

- Material science advancements, such as temperature and salinity compensation, and deployment strategies, including data logging and sensor integration, can help extend battery life and improve overall sensor performance. Maintaining sufficient battery life for long-term deployments of subsea sensors, especially in remote or deepwater environments, can be challenging. Alternative power sources, such as renewable energy or hydrothermal vents, are being explored to address this challenge. Effective sensor design and deployment strategies, including proper material selection and temperature compensation, are essential to ensure the reliability and accuracy of subsea sensor data.

Exclusive Customer Landscape

The subsea sensors market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the subsea sensors market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, subsea sensors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AIS - CRP Subsea Ltd., a subsidiary of the company, specializes in providing advanced subsea sensors and monitoring systems for offshore infrastructure, including risers, umbilicals, pipelines, and cables. These innovative solutions enhance safety, efficiency, and reliability in the offshore energy sector.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AIS

- Amphenol Corp.

- Baker Hughes Co.

- Blueprint Subsea

- ClampOn AS

- Covelya Group Ltd.

- Emerson Electric Co.

- GP 50 NY LTD.

- Hydrotechnik Test Engineering Ltd.

- Impact Subsea Ltd.

- James Fisher and Sons Plc

- NATEC Sensors GmbH

- Norwegian Subsea AS

- Seatools

- Sensor Technik Sirnach AG

- Siemens Energy AG

- SUCO Robert Scheuffele GmbH and Co. KG

- TE Connectivity Ltd.

- Teledyne Technologies Inc.

- TTL Subsea Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Subsea Sensors Market

- In January 2024, Schneider Electric, a leading energy management and automation company, announced the launch of its new subsea pressure sensor, the TeSys Sense 3300, designed for deep-sea applications. This sensor is expected to enhance the reliability and accuracy of underwater oil and gas exploration and production (E&P) operations (Schneider Electric Press Release, 2024).

- In March 2024, Honeywell and Subsea 7, a leading subsea engineering, construction, and services company, entered into a strategic partnership to develop and integrate Honeywell's advanced sensing technologies into Subsea 7's subsea production systems. This collaboration aims to improve operational efficiency and safety in the oil and gas industry (Honeywell Press Release, 2024).

- In May 2024, Emerson, a global technology and engineering company, completed the acquisition of Aventics, a leading provider of pneumatic components and systems. The acquisition is expected to strengthen Emerson's position in the market by expanding its product portfolio and enhancing its capabilities in the design and manufacturing of advanced pneumatic components for subsea applications (Emerson Press Release, 2024).

- In April 2025, the US Bureau of Ocean Energy Management (BOEM) approved the use of Sonardyne International Ltd.'s Long Baseline (LBL) acoustic positioning system for deepwater oil and gas exploration and production activities in the Gulf of Mexico. This approval marks a significant milestone for Sonardyne, as it expands its presence in the US offshore energy market and demonstrates the company's commitment to providing advanced subsea positioning solutions (Sonardyne Press Release, 2025).

Research Analyst Overview

- The market encompasses a range of technologies, including dissolved oxygen sensors, wave measurement systems, multibeam sonar, current meters, fiber optic sensors, temperature sensors, underwater lighting, subsea construction equipment, network security solutions, data integrity tools, water quality monitoring systems, data security platforms, oceanographic research instruments, underwater cameras, sediment transport monitors, ph sensors, turbidity sensors, seismic survey equipment, underwater positioning systems, pressure transducers, and conductivity sensors. These sensors play a crucial role in various applications, from climate change mitigation and ocean acidification research to fisheries management and hydrographic surveying. The market is driven by the growing demand for accurate and reliable data in the maritime industry, as well as the increasing importance of underwater infrastructure, such as subsea power cables and underwater archaeology sites.

- As such, trends in the market include advancements in sensor technology, integration of artificial intelligence and machine learning, and the growing importance of network security and data integrity. Additionally, geophysical surveys, wave measurement, and tidal monitoring are gaining traction due to their applications in renewable energy and coastal monitoring. Overall, the market is a dynamic and evolving industry that continues to shape the future of underwater exploration and infrastructure development.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Subsea Sensors Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

233 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.1% |

|

Market growth 2025-2029 |

USD 355.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.5 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Subsea Sensors Market Research and Growth Report?

- CAGR of the Subsea Sensors industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the subsea sensors market growth of industry companies

We can help! Our analysts can customize this subsea sensors market research report to meet your requirements.

RIA -

RIA -